July 22, 2026

The Aluminium Extrusion Margin Trap: Growth at the Surface, Crisis Beneath

Few industrial sectors illustrate the gap between macroeconomic optimism and factory-floor reality more sharply than aluminium extrusion. Volume metrics point upward across virtually every end-use market — electric vehicles, renewable energy infrastructure, construction, and consumer electronics all consume extruded aluminium at expanding rates. Yet beneath this demand supercycle, a structural profitability crisis has taken hold. The aluminium extrusion margin trap describes precisely this condition: a state in which producers generate more revenue than ever while earning less per tonne than at almost any point in recent history.

Understanding how this paradox emerged, and whether it can be resolved, requires moving beyond headline demand data and examining the fundamental economics of extrusion manufacturing — from raw material procurement through press operations to finished product pricing.

When big ASX news breaks, our subscribers know first

What Is the Aluminium Extrusion Margin Trap?

The aluminium extrusion margin trap is a structural condition, not a cyclical dip. It describes a manufacturing environment in which extruders face simultaneous upward pressure on input costs and downward pressure on finished product pricing, compressing operating margins even as output volumes rise. Unlike a conventional downturn where demand weakness drives temporary margin erosion, the current trap persists despite strong demand — which is precisely what makes it structurally dangerous rather than cyclically manageable.

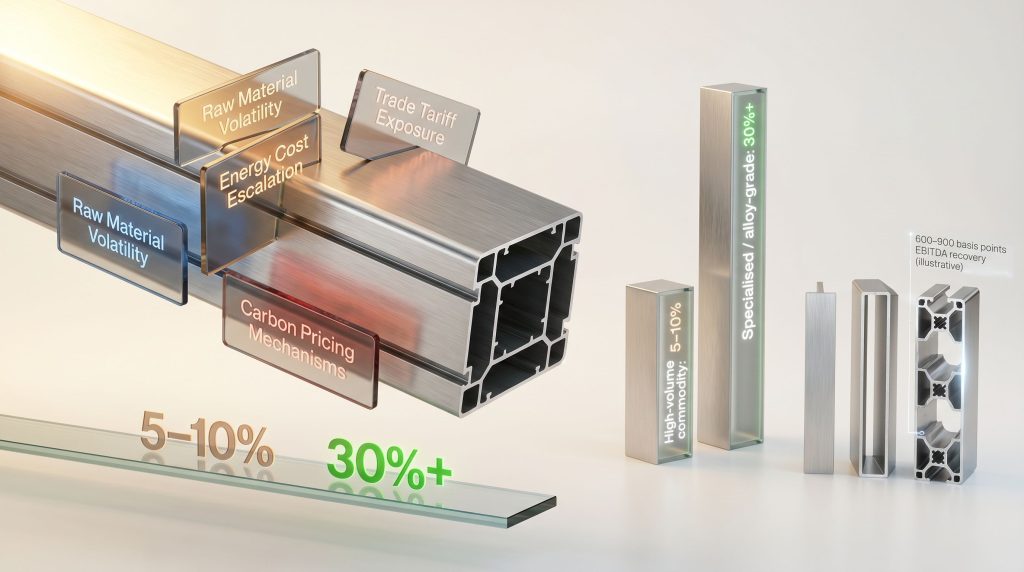

The trap operates through four primary compression vectors acting in combination:

| Compression Vector | Primary Driver | Margin Impact |

|---|---|---|

| Raw Material Volatility | LME aluminium price swings | Direct cost-of-goods erosion |

| Energy Cost Escalation | Gas and electricity pricing cycles | Operating cost inflation |

| Trade Tariff Exposure | Cross-border duty structures | Competitive displacement |

| Carbon Pricing Mechanisms | EU CBAM and equivalent schemes | Regulatory cost burden |

What separates the margin trap from a standard cyclical downturn is its self-reinforcing architecture. In a typical commodity cycle, falling margins eventually reduce supply as uneconomic capacity exits, restoring pricing power for survivors. In the current extrusion environment, several structural factors prevent this natural rebalancing. Global overcapacity — particularly from Asian producers operating on razor-thin margins to maintain market share — establishes a persistent global pricing floor that suppresses finished product prices regardless of local cost conditions.

Simultaneously, long-term supply contracts with automotive and construction customers typically cap price escalation, preventing extruders from passing through sudden cost spikes. The result is a system where the margin trap can persist indefinitely, even through periods of strong demand growth.

The aluminium extrusion margin trap is not a problem of insufficient demand. It is a problem of structural pricing asymmetry — where input cost volatility is absorbed by producers while output pricing remains anchored by customer contracts and global competition.

The Demand Supercycle Is Real — But It Does Not Rescue Margins

The demand side of the aluminium extrusion story is genuinely compelling. Three structural forces are driving multi-decade volume expansion across the sector.

Electric Vehicle Lightweighting

Battery electric vehicles require significantly more aluminium than their internal combustion counterparts. Structural battery enclosures, crash management systems, thermal management profiles, and floor structures all rely on precision-extruded aluminium components. As fleet electrification accelerates under regulatory pressure across the EU, US, and China, automotive aluminium demand has expanded substantially — with extrusion-intensive applications growing particularly fast due to their ability to achieve complex cross-sectional geometries in a single production step.

Green Infrastructure Buildout

Solar mounting systems, curtain wall framing, window systems, and grid-scale energy storage housings collectively consume enormous quantities of extruded aluminium. Government-mandated renewable energy targets across major economies have converted this into a near-captive demand stream that shows little sensitivity to economic cycles. The construction sector remains the largest single consumer of aluminium extrusions globally, and the intersection of green building standards with renewable energy infrastructure has created a multi-decade demand runway.

Regulatory Lightweighting Mandates

Fleet emissions standards in the EU, United States, and China continue to create substitution demand away from steel toward aluminium in transportation applications. This regulatory-driven substitution represents structural rather than discretionary demand, providing a level of volume certainty that most industrial sectors cannot match.

Aluminium's intrinsic material properties underpin all of these demand drivers. Its superior strength-to-weight ratio, excellent thermal conductivity, corrosion resistance, and theoretical infinite recyclability make it materially superior to competing materials across most lightweight structural applications. These advantages are not diminishing — if anything, they are becoming more valued as sustainability requirements tighten across manufacturing supply chains.

Furthermore, understanding the broader aluminum and alumina markets provides essential context for how upstream dynamics filter directly through to extrusion-level profitability.

Volume growth without pricing power is a revenue illusion. In commoditised segments of the extrusion market, expanding output can accelerate losses when fixed costs are not adequately absorbed by margin-per-tonne.

The critical insight that many industry observers miss is that strong demand does not automatically translate to pricing power when the competitive structure of the supplying industry remains highly fragmented. The extrusion sector globally comprises thousands of producers, many of whom compete primarily on price in standard-profile segments. This fragmentation, combined with significant overcapacity in key producing regions, means that demand growth is absorbed by volume expansion across many producers rather than being captured as margin improvement by individual firms.

How Severe Is the Margin Compression? A Cost Structure Analysis

The financial reality of the aluminium extrusion margin trap varies significantly by business model and product complexity. The following ranges, drawn from publicly available industry data and sector analyses, illustrate the structural bifurcation within the industry:

| Business Model | Gross Margin Range | Net Margin Range |

|---|---|---|

| High-volume commodity extrusion | 5–10% | 2–5% |

| Mid-market standard profiles | 25–35% | 10–15% |

| Custom and precision extrusion | 15–25% net | 15–25% |

| Specialised technical and alloy-grade profiles | 30%+ | 18–25%+ |

Note: These figures are indicative estimates derived from publicly available industry project reports and market summaries. Actual margins vary by geography, production scale, energy cost environment, and product mix.

The divergence between commodity and specialised segments is the defining economic characteristic of the modern extrusion industry. Standard-profile, high-volume operations face the most acute margin compression because they compete directly with Asian producers operating at scale under lower labour cost structures. These operations typically lock in long-term supply agreements at thin margins to maintain press utilisation, creating a structural inability to improve profitability without fundamental product mix transformation.

The Energy Cost Multiplier

Aluminium extrusion is an energy-intensive manufacturing process. Heating billets to extrusion temperature, maintaining press hydraulics, and managing post-extrusion heat treatment operations consume significant quantities of electricity and natural gas. European extruders, in particular, have faced severe margin compression from energy cost escalation, with industrial electricity prices in some EU markets more than doubling between 2021 and 2024.

For operations where energy represents 15–25% of total production costs, a 100% increase in energy pricing effectively destroys all net margin in commodity segments without compensating price increases from customers. Investments in low-carbon aluminium operations consequently offer extruders a dual benefit: reduced energy cost exposure and improved sustainability credentials.

Raw Material Pass-Through Limitations

The structural inability to pass through aluminium price increases is one of the most persistently damaging features of the margin trap. LME aluminium prices are notoriously volatile, swinging by 20–40% within single calendar years during periods of market disruption. While large automotive and construction customers increasingly accept LME-linked pricing mechanisms, smaller customers and spot market transactions often lack these protections.

Furthermore, even LME-linked contracts typically feature price adjustment lags of one to three months, creating windows of margin exposure during rapid price movements. The aluminium tariff impacts flowing from recent trade policy shifts have added an additional layer of cost unpredictability that compounds these existing raw material challenges.

Labour and Logistics as Secondary Compression Layers

Beyond energy and raw materials, labour cost inflation and logistics complexity add secondary compression layers. Skilled press operators, die technicians, and quality control personnel command increasing wages in most developed market extrusion centres, while logistics costs — particularly for operations serving just-in-time automotive supply chains — have increased substantially since the supply chain disruptions of the early 2020s. These secondary factors alone would not create the margin trap, but they compound primary compression vectors to the point where standard-profile operations in high-cost economies face structurally unviable economics.

Competitive Intensity and the Race to the Bottom

The competitive landscape of the aluminium extrusion sector amplifies every cost pressure described above. In standard-profile segments serving construction and industrial applications, pricing competition has become the dominant competitive dimension — a dynamic that systematically destroys value for all participants over time.

The competitive positioning of extruders can be mapped across three distinct categories, each with substantially different margin resilience:

| Competitive Position | Pricing Power | Margin Resilience | Substitution Risk |

|---|---|---|---|

| Standard profile, high volume | Low | Fragile | High |

| Engineered and precision profile | Moderate to High | Stable | Low to Moderate |

| Proprietary alloy and R&D-led | High | Strong | Very Low |

Extruders competing primarily on price in standard-profile segments face the highest structural risk. Without differentiation, the margin floor in these segments can approach breakeven under adverse input cost conditions.

Global overcapacity in standard extrusion capacity represents perhaps the single most intractable element of the margin trap. Chinese aluminium extrusion capacity has expanded aggressively over the past decade, creating a global supply overhang that suppresses finished product pricing regardless of demand conditions in other markets. Import competition from lower-cost producing regions has disrupted domestic extruder economics in Europe, North America, and Australia, forcing pricing adjustments that eliminate margin for producers operating under higher cost structures.

The trade tariff landscape has provided partial protection for domestic producers in some markets, but tariff structures are inherently unstable. The broader consequences of aluminum and steel tariffs on domestic manufacturers illustrate precisely how quickly competitive dynamics can shift when policy changes alter the cost calculus for imported material. Furthermore, tariffs address only direct import competition — they do not protect against indirect competitive effects such as Chinese producers redirecting exports to third markets and undercutting regional producers who serve those markets.

Regulatory and Trade Pressures: The Carbon Dimension

The European Union's Carbon Border Adjustment Mechanism represents a new and increasingly significant cost dimension for the aluminium extrusion sector. Progressively implemented from 2026 onward, CBAM introduces embedded carbon costs into aluminium imports based on their production emissions intensity. For extruders operating in high-emission energy environments — or sourcing primary aluminium from carbon-intensive smelters — this mechanism creates a structural cost disadvantage that will intensify over time as carbon prices increase.

The CBAM's implications extend beyond direct import duties. The mechanism effectively establishes a global carbon pricing regime for aluminium that will progressively reshape trade flows, sourcing decisions, and production economics across the entire value chain. Extruders who have not invested in low-carbon production methods or certified low-carbon aluminium sourcing face an increasing cost burden that compounds existing margin pressures.

Key regulatory dimensions affecting extrusion margins include:

- EU CBAM implementation progressively raising costs for carbon-intensive aluminium products entering European markets from 2026

- Scope 3 emissions reporting requirements forcing automotive and construction customers to account for supply chain emissions, creating demand for certified low-carbon aluminium

- Energy efficiency mandates in manufacturing sectors raising compliance costs for older extrusion equipment

- Trade tariff structures across major consuming markets creating complex competitive dynamics for internationally active producers

The geopolitical dimension adds further complexity. Supply disruptions driven by conflict, sanctions, and trade policy realignment have created periodic spikes in primary aluminium availability and pricing that ripple directly through extrusion economics. These disruptions are increasingly frequent and unpredictable, making input cost management significantly more challenging than in previous decades.

The next major ASX story will hit our subscribers first

Can Metallurgical Innovation Break the Margin Trap?

The most transformative long-term escape route from the aluminium extrusion margin trap may lie not in commercial strategy but in materials science. Nano-level alloy research is actively rewriting the fundamental economics of extrusion by enabling properties — strength, formability, fatigue resistance, and thermal performance — that command substantial pricing premiums over standard-grade products.

The dominant 6xxx series alloys that underpin most commodity extrusion production have remained relatively unchanged for decades. These alloys — based primarily on aluminium-magnesium-silicon compositions — offer adequate mechanical properties for general structural applications but provide limited differentiation in high-performance markets. Advanced alloy development programs are now targeting modified 7xxx series alloys, nano-reinforced composites, and novel heat treatment protocols that dramatically expand the performance envelope of extruded products.

The recyclability dimension of this innovation story is particularly important. According to the Aluminium Extrusion Manual, the industry is increasingly recognising that recycled and low-carbon aluminium credentials are not simply sustainability marketing but genuine sources of pricing power:

- Recycled content premiums are emerging as green procurement mandates enable extruders supplying certified recycled-content products to command above-market pricing from sustainability-focused customers

- Scrap-fed billet strategies reduce primary metal dependency, lowering cost-of-goods and reducing LME price exposure simultaneously

- Low-carbon aluminium certification enables access to sustainability-linked supply contracts with OEM customers who face their own Scope 3 reporting obligations

The step-by-step pathway from commodity positioning to innovation-led margin recovery follows a logical investment sequence:

- Invest in die design capability to reduce scrap rates and improve first-pass yield on complex profiles

- Qualify advanced alloy grades to enable entry into aerospace, defence, and EV structural applications

- Certify low-carbon supply chains to access green premium pricing from sustainability-focused buyers

- Develop proprietary surface treatment capabilities — anodising, powder coating, and thermal break assembly as margin-accretive value-add services

- Adopt Industry 4.0 process controls for real-time monitoring to reduce energy consumption per tonne extruded

Each step in this sequence moves an extruder further from commodity pricing dynamics and closer to specification-led, relationship-driven sales where pricing power is substantially higher. In addition, AI-driven process optimisation is increasingly being deployed by leading operators to accelerate this transition.

How Profile Complexity Affects Manufacturing Economics

One of the less-discussed dimensions of the aluminium extrusion margin trap is the relationship between profile complexity and manufacturing economics. Not all extrusion profiles are financially equivalent, and the failure to correctly price for complexity is one of the most common sources of margin destruction in the industry.

Profile geometries featuring extreme aspect ratios, thin-walled hollow sections, or asymmetric void distributions impose disproportionate tooling and scrap costs — factors that can eliminate margin entirely on short production runs if not priced correctly at the quoting stage.

Complex profiles impose higher costs across multiple dimensions. Die manufacturing costs increase non-linearly with profile complexity — a hollow section with multiple voids may cost three to five times more to tool than a simple solid profile. Die failure rates are higher for complex geometries, and each die failure on a short production run can eliminate the entire margin for that order.

Scrap rates during press startup and profile transitions are substantially higher for complex cross-sections, and the specialist operator knowledge required to consistently produce tight-tolerance profiles commands labour cost premiums. The operational disciplines that separate high-margin extruders from average performers include:

- Rigorous complexity pricing models that capture all incremental costs associated with difficult geometries

- Die life management systems that track tooling costs against individual profile families

- First-pass yield optimisation through advanced billet preparation and press parameter control

- Proactive customer design engagement to simplify profiles during specification stages without compromising functional requirements

Strategic Pathways Out of the Margin Trap

There are three credible strategic archetypes through which aluminium extruders can escape the margin trap, each requiring different capital investment profiles, capability development timelines, and risk tolerances.

Archetype 1: The Specialisation Play

Migrating product mix toward precision, tight-tolerance, or technically demanding profiles is the most direct route to structural margin improvement. Aerospace, defence, medical device, and advanced EV structural applications all require extrusion capabilities that commodity producers cannot easily replicate, providing genuine barriers to competitive entry and supporting sustainable pricing premiums. This approach accepts lower volume in exchange for meaningfully higher margin-per-tonne.

Archetype 2: The Vertical Integration Play

Backward integration into billet casting or scrap aggregation reduces exposure to LME spot pricing and captures upstream margin that would otherwise accrue to billet suppliers. Extruders with captive billet casting capability can source metal at cost-plus rather than market pricing, providing structural cost advantages during periods of primary aluminium price spikes. This approach requires significant capital investment but provides durable competitive advantage in cost-sensitive market segments.

Archetype 3: The Value-Added Services Play

Expanding downstream into fabrication, machining, assembly, and surface treatment converts commodity profile revenue into solution-based contract revenue. This transformation fundamentally changes the customer relationship — from a transactional supplier of standard profiles to an integrated manufacturing partner supplying finished assemblies. The resulting switching costs create customer retention dynamics that support pricing stability and margin resilience unavailable to pure-play extrusion operations.

To illustrate the financial logic, consider a hypothetical mid-tier extruder operating three press lines at annual output of 25,000 tonnes, predominantly serving the construction and industrial sectors. Under current energy and raw material conditions, standard-profile margins have compressed to approximately 8–12% gross. By reallocating 30% of press capacity toward precision automotive profiles and introducing in-house anodising, the same operation could theoretically recover 600–900 basis points of EBITDA margin — illustrating the transformative financial impact available through strategic repositioning. The role of aluminium supply chain leaders in enabling these transitions, through reliable access to certified and responsibly sourced material, should not be underestimated.

Frequently Asked Questions: Aluminium Extrusion Margins

What is a typical profit margin for an aluminium extrusion business?

Margins vary significantly by segment. High-volume commodity extruders typically operate on gross margins of 5–10% and net margins of 2–5%. Mid-market operations achieve gross margins of 25–35%, while specialised and precision extruders can achieve net margins of 15–25% or higher. These figures are indicative estimates that vary by geography, energy cost environment, and product mix.

Why are aluminium extrusion margins so thin in standard product segments?

Standard-profile segments face intense competition from globally dispersed producers, particularly from Asian manufacturers operating at scale under lower cost structures. This creates persistent downward pressure on finished product pricing that standard-profile extruders cannot easily escape without product differentiation.

How does energy cost affect aluminium extrusion profitability?

Energy typically represents 15–25% of total production costs for extrusion operations. Significant energy price increases — as experienced across European markets in recent years — can eliminate all net margin in commodity segments without compensating price increases from customers.

What is CBAM and how does it affect aluminium extruders?

The EU Carbon Border Adjustment Mechanism introduces embedded carbon costs into aluminium imports based on their production emissions intensity, progressively implemented from 2026. It creates structural cost disadvantages for extruders in high-emission environments and rewards those who invest in low-carbon production methods.

Can recycled aluminium improve extrusion margins?

Yes, in two ways. Scrap-fed billet production reduces cost-of-goods by eliminating primary metal price exposure. Separately, certified recycled-content products can command pricing premiums from sustainability-focused customers facing their own Scope 3 reporting obligations.

What types of extrusion products carry the highest margins?

Specialised technical profiles for aerospace, defence, medical, and advanced automotive applications consistently carry the highest margins due to technical barriers to competitive entry, low substitution risk, and specification-led rather than price-led purchasing decisions.

How does profile complexity affect scrap rates and profitability?

Complex profiles with thin walls, hollow sections, or asymmetric void distributions impose disproportionate tooling, scrap, and startup costs that must be correctly captured in quoting models. Failure to price for complexity accurately is one of the most common sources of margin destruction in extrusion operations.

Key Takeaways: Navigating the Aluminium Extrusion Margin Trap

| Key Metric | Range or Estimate |

|---|---|

| Commodity extrusion gross margin | 5–10% |

| Mid-market extrusion gross margin | 25–35% |

| Specialised and custom extrusion net margin | 15–25% |

| Potential EBITDA recovery via specialisation | 600–900 basis points (illustrative) |

| Primary cost compression drivers | Energy, raw materials, carbon pricing, tariffs |

The aluminium extrusion sector sits at a genuine strategic inflection point. Demand conditions are structurally favourable across every major end-use market, providing a volume foundation that most manufacturing sectors would envy. Yet demand alone cannot rescue an industry whose margin architecture is under simultaneous attack from multiple structural forces.

The extrusion businesses best positioned for the decade ahead share several characteristics: they have invested in technical capability that generates genuine pricing power, they have diversified away from pure-play standard-profile commodity revenue, and they have positioned their supply chains to capture sustainability premiums rather than simply absorb sustainability costs. These differentiators are not easily or quickly replicated, meaning that extruders who have made these investments early will enjoy durable competitive advantages as the margin trap tightens further for those who have not.

The central strategic tension of the aluminium extrusion industry is now unambiguous: it is a growth market where the rewards of that growth are increasingly concentrated among differentiators, while volume players face structurally deteriorating economics regardless of how favourable the macroeconomic demand environment becomes. The margin trap is real, it is structural, and escaping it requires deliberate strategic transformation rather than simply waiting for market conditions to improve.

Disclaimer: Margin ranges and financial estimates cited in this article are indicative figures drawn from publicly available industry analyses and market summaries. They should not be relied upon as precise financial benchmarks for specific operations. Forward-looking statements and scenario projections are illustrative only and do not constitute financial advice. Readers should conduct independent research and seek professional advice before making investment or operational decisions based on industry trend analysis.

For readers seeking additional perspectives on aluminium downstream processing economics and pricing dynamics, AL Circle's coverage of smart manufacturing in extrusion provides ongoing analysis of how AI and technology shifts are reshaping the global sector. In addition, Capral's extrusion product range offers a practical reference point for the diversity of profile solutions available within the Australian market.

Want to Invest in the Companies Reshaping the Aluminium Supply Chain?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including those driving the low-carbon aluminium and critical materials supply chains underpinning the extrusion sector's structural transformation. Explore historic discoveries and the returns they generated, then begin your 14-day free trial to position yourself ahead of the broader market.