June 13, 2026

Understanding Aluminium's Economic Footprint

Industrial metals often operate beneath the radar of mainstream economic analysis, yet their influence ripples through every sector of modern commerce. Aluminium global economic impact exemplifies this hidden economic force, functioning as both a fundamental building block of industrial civilisation and a sophisticated indicator of macroeconomic health. While representing a modest direct contribution to global economic output, this versatile metal orchestrates complex value chains that amplify its economic significance far beyond its apparent market size.

The metal's economic footprint extends through construction frameworks that define urban skylines, transportation systems that connect global markets, and energy infrastructure that powers modern economies. Within the context of a global economy valued at approximately $114 trillion according to the International Aluminium Institute's latest economic assessments, aluminium's direct economic contribution appears deceptively small at roughly 0.15-0.23 percent of total output.

However, this perspective overlooks the interconnected nature of modern industrial systems. Aluminium consumption patterns reveal themselves as sophisticated proxies for economic momentum, responding predictably to changes in underlying growth dynamics across multiple sectors simultaneously. When construction projects accelerate, manufacturing scales increase, and transportation networks expand, aluminium demand follows with characteristic reliability.

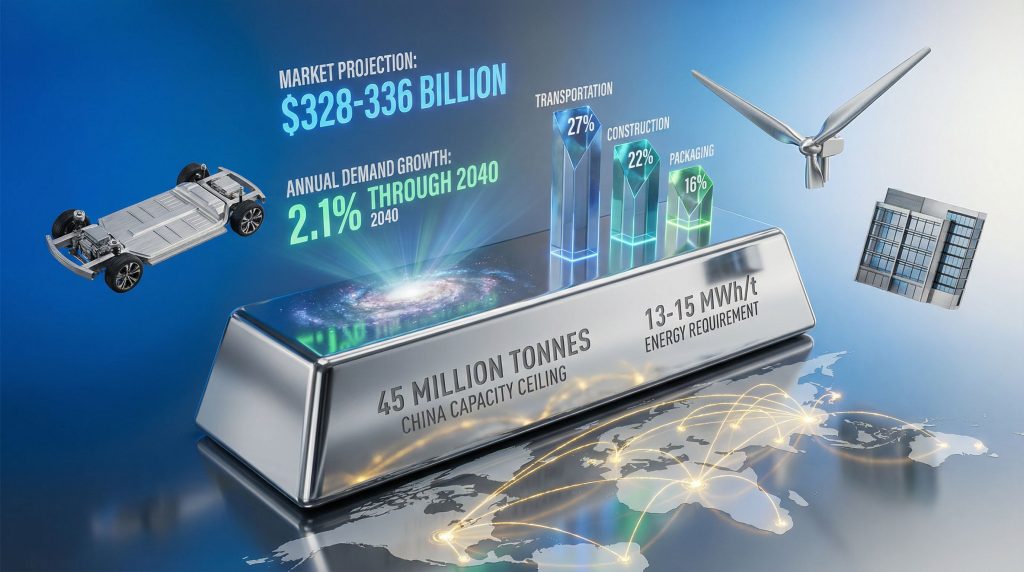

The metal's presence spans critical economic sectors in measurable proportions based on AL Circle's analysis of 104 million tonnes of global consumption:

- Transportation sector commands 27 percent of total demand

- Building and construction accounts for 22 percent

- Packaging applications represent 16 percent

- Electrical and electronics consume 14 percent

- Industrial applications utilise 8 percent

- Various other uses comprise the remaining 13 percent

This distribution reflects aluminium's role as an enabler rather than a driver of economic activity, positioning the metal at the intersection of infrastructure development, industrial expansion, and technological advancement.

When big ASX news breaks, our subscribers know first

The GDP Correlation Phenomenon

Economic indicators traditionally fall into three categories: leading indicators that predict future activity, coincident indicators that move simultaneously with economic conditions, and lagging indicators that confirm trends after they occur. Aluminium demand functions as a reliable lagging indicator, responding consistently to economic momentum changes with characteristic timing patterns.

Global economic growth projections reveal a moderating trajectory that directly influences aluminium consumption patterns. Current estimates indicate world GDP expansion of approximately 2.6 percent for both 2025 and 2026, representing a decline from 2.9 percent recorded in 2024 and falling below the pre-pandemic average of roughly 3.0 percent, according to AL Circle's Global Aluminium Industry Outlook 2026.

Historical economic cycles demonstrate aluminium's consistent response patterns to GDP fluctuations:

- 2004-2007 pre-crisis period: 4.4 percent average annual growth supported robust aluminium demand

- 2009 financial crisis: 1.4 percent growth corresponded with significant demand contraction

- 2010-2019 recovery decade: 3.0 percent average growth sustained moderate aluminium consumption increases

- 2020 pandemic impact: 3.0 percent GDP contraction severely impacted industrial metal demand

- 2021 reopening surge: 6.4 percent growth rebound drove exceptional aluminium demand recovery

- 2023-2026 projected period: 2.7 percent average growth suggests moderate consumption expansion

Major economies exhibit similar moderation patterns affecting global aluminium markets. The United States faces projected growth of 1.8 percent in 2025 declining to 1.5 percent in 2026, while China, historically the engine of global aluminium demand, expects deceleration from 5.0 percent in 2025 to 4.6 percent in 2026. Furthermore, this outlook must consider the potential impact of US economic tariffs on global trade dynamics, substantially below its pre-pandemic pace of approximately 6.7 percent.

The temporal relationship between GDP changes and aluminium demand reflects the practical realities of industrial project development cycles. Economic growth signals typically require 6-12 months to translate into material demand as investment decisions progress through planning, procurement, and implementation phases.

Market Valuation and Volume Projections

Global aluminium consumption demonstrates steady upward trajectory despite economic headwinds, with volumes projected to increase from 101.6 million tonnes in 2024 to 104.0 million tonnes in 2025, reaching an estimated 106.8 million tonnes by 2026 according to AL Circle's industry analysis. This represents a compound annual growth rate of approximately 2.1 percent, closely aligned with broader economic expansion patterns.

Current London Metal Exchange pricing ranges between $2,700-$3,192 per tonne, reflecting multiple economic pressures including trade policy impacts, energy cost volatility, and supply chain constraints. However, the tariff impact on markets continues to create pricing volatility and uncertainty. These price levels, combined with projected volume growth, indicate substantial market values despite economic moderation.

Sectoral demand distribution reveals the structural foundations supporting continued consumption growth:

| Sector | Share of Consumption | Key Growth Drivers |

|---|---|---|

| Transportation | 27% | Electric vehicle adoption, aerospace expansion |

| Construction | 22% | Infrastructure investment, urbanisation |

| Packaging | 16% | Consumer spending resilience, sustainability trends |

| Electronics | 14% | Technology proliferation, 5G infrastructure |

| Industrial | 8% | Manufacturing modernisation, automation |

| Other Applications | 13% | Renewable energy, emerging technologies |

The transportation sector's dominant position reflects ongoing structural transformation toward electrification, where battery electric vehicles typically require significantly more aluminium content than conventional internal combustion vehicles due to battery housing, thermal management systems, and lightweight body structures compensating for battery weight.

Construction sector demand maintains strong correlation with GDP growth as infrastructure spending, both public and private, responds directly to economic expansion cycles. This sector's reliability makes it a cornerstone of aluminium demand forecasting models.

Supply Constraints and Market Dynamics

China's strategic decision to limit primary aluminium smelting capacity at approximately 45 million tonnes creates structural supply dynamics extending beyond commodity markets into broader economic implications. This capacity ceiling, combined with energy constraints and environmental regulations, forces global supply chain recalibration affecting regional manufacturing competitiveness and international trade patterns.

Multi-year inventory depletion signals structural supply-demand imbalances that could constrain economic growth in aluminium-intensive sectors. Conservative industry projections suggest:

- 2025: Potential 100,000-tonne supply deficit affecting spot market pricing

- 2026: Estimated 365,000-tonne deficit creating pressure on industrial consumers

- 2027: Projected 722,000-tonne deficit potentially limiting production capacity in downstream sectors

These supply constraints interact with energy market dynamics, as aluminium smelting requires approximately 13-15 megawatt-hours per tonne of production. This energy intensity creates vulnerabilities to electricity price volatility and grid stability issues, while simultaneously driving innovation in renewable energy integration and energy efficiency technologies.

Regional competitive advantages increasingly depend on access to low-cost, reliable electricity, particularly renewable sources. This trend redirects investment flows toward locations with hydroelectric, solar, or wind power advantages, reshaping the global geography of aluminium production.

Trade Policy and Currency Impacts

Current US trade policies demonstrate aluminium's sensitivity to protectionist measures, with 50 percent import tariffs creating domestic price premiums that ripple through manufacturing cost structures. These policy interventions showcase how commodity markets transmit geopolitical decisions across entire economic systems. Additionally, US steel, aluminum tariffs continue to reshape global metal trading patterns.

Supply chain reorganisation accelerates as manufacturers seek alternative sourcing regions to avoid tariff impacts, favouring trade relationships with non-tariff jurisdictions. This restructuring process creates investment opportunities in some regions while disadvantaging others, illustrating aluminium's role in economic geography shifts.

Currency fluctuations significantly influence aluminium trade patterns, as a weaker US dollar enhances competitiveness for non-US buyers and exporters while simultaneously reducing import costs for dollar-denominated purchases. These dynamics create arbitrage opportunities and influence central bank policy considerations in commodity-dependent economies.

International trade flow modifications reflect aluminium's strategic importance to national economic security, with governments increasingly treating the metal as critical infrastructure material rather than merely a commodity input.

Energy Intensity and Economic Vulnerability

Aluminium smelting's extreme electricity requirements position the industry at the centre of energy transition discussions. The 13-15 megawatt-hours required per tonne of production makes aluminium global economic impact directly sensitive to regional energy policies, renewable integration challenges, and grid modernisation investments.

Industrial electricity demand from aluminium production competes with residential and commercial users, creating potential conflicts during peak demand periods or supply constraints. This competition influences electricity pricing across entire regional grids, extending aluminium's economic impact beyond direct industrial users.

What role does decarbonisation play in aluminium economics?

Energy security considerations increasingly drive smelter location decisions, favouring regions with diverse generation portfolios and stable regulatory environments. Moreover, decarbonisation in mining creates new economic opportunities across the supply chain. This trend accelerates investment in renewable energy in mining as smelter operators seek long-term cost and supply certainty.

Carbon pricing mechanisms represent emerging cost factors that could dramatically alter aluminium production economics. European Union carbon border adjustments and similar policies under consideration globally threaten to reshape international competitiveness based on production methods' carbon intensity.

The next major ASX story will hit our subscribers first

Long-term Economic Transformation Indicators

The transition toward sustainable aluminium production signals broader economic shifts beyond the metal itself. Hydro-powered smelting capacity expansion in regions with renewable energy advantages creates new industrial development patterns while challenging traditional production centres dependent on fossil fuel-based electricity.

Recycling technology advancement reduces dependence on primary production while creating new economic opportunities in circular economy systems. Secondary aluminium processing requires only 5 percent of the energy needed for primary production, making recycled content increasingly valuable as energy costs rise and carbon restrictions tighten.

Green finance mechanisms directing capital toward low-carbon aluminium production demonstrate how environmental considerations increasingly influence industrial investment decisions. These financial instruments suggest sustainable production methods may eventually command price premiums, fundamentally altering industry economics.

Regional development strategies leveraging renewable energy resources for aluminium production indicate how the metal serves as an anchor industry for broader economic diversification plans. Countries with abundant hydroelectric, solar, or wind resources view aluminium smelting as a pathway to industrial development and export revenue generation.

Investment and Innovation Catalysts

Market dynamics drive technological innovation in energy-efficient smelting processes, with research focusing on reducing electricity consumption and integrating renewable energy sources. These developments suggest potential productivity gains that could offset rising energy costs while reducing carbon footprints.

Infrastructure investment in recycling and circular economy systems creates new economic sectors while reducing raw material dependence. The development of advanced sorting technologies, remelting facilities, and quality control systems represents emerging opportunities for equipment manufacturers and technology providers.

Supply chain resilience investments aim to reduce single-source dependencies while building redundancy into critical material flows. These initiatives involve geographic diversification, inventory management improvements, and alternative material development, creating opportunities across multiple industrial sectors.

Strategic partnerships between aluminium producers and end-users increasingly focus on sustainability metrics and supply security rather than price alone. These relationships suggest evolving business models that prioritise long-term stability over short-term cost optimisation.

Future Economic Integration Pathways

Aluminium's integration with renewable energy infrastructure positions the metal at the heart of decarbonisation efforts across multiple economic sectors. Wind turbine construction, solar panel frameworks, and electricity transmission systems all require substantial aluminium inputs, creating sustained demand linked to climate policy implementation.

Smart grid development and energy storage deployment represent emerging demand sources as electrical infrastructure modernises to accommodate renewable energy integration. Aluminium's conductivity properties and corrosion resistance make it essential for next-generation electrical systems.

Electric vehicle adoption continues driving structural demand increases, though specific growth rates vary by region based on policy support, charging infrastructure development, and consumer acceptance patterns. The automotive industry's lightweighting efforts to offset battery weight create additional aluminium demand beyond direct electrification impacts.

Aerospace industry recovery and expansion, particularly in commercial aviation and space applications, provide high-value demand segments less sensitive to economic cycles than traditional construction and packaging markets. According to the Aluminium Association of Canada's economic contribution report, these sectors demonstrate resilient demand patterns even during economic downturns.

Despite representing less than 0.25 percent of direct global GDP contribution, the aluminium global economic impact as an economic enabler positions it centrally within macroeconomic trends shaping industrial development patterns. The metal's correlation with GDP growth, sectoral distribution across critical industries, and sensitivity to energy and trade policies make it both an indicator of economic health and a driver of structural economic transformation.

Projected supply deficits, evolving price dynamics, and changing trade relationships suggest aluminium markets will continue influencing broader economic conditions through manufacturing costs, regional competitiveness shifts, and infrastructure investment requirements. Understanding these interconnections provides valuable insights into economic resilience, industrial strategy development, and the transition toward sustainable growth models that balance environmental objectives with economic development needs.

Ready to Capitalise on Critical Resource Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical metals like aluminium that underpin global economic infrastructure. Position yourself ahead of market movements by exploring historic discovery returns and begin your 30-day free trial today to gain immediate access to actionable investment opportunities.