May 11, 2026

The global aluminium market continues experiencing unprecedented transformation as supply chain disruptions and energy transition demands reshape fundamental industry dynamics. While traditional industrial applications face declining consumption, emerging technology sectors drive substantial price momentum through specialized aluminium requirements. This structural shift creates distinct competitive advantages for vertically integrated producers capable of adapting their product mix and geographic footprint to capture evolving market opportunities.

Understanding Vertical Integration in Modern Aluminium Production

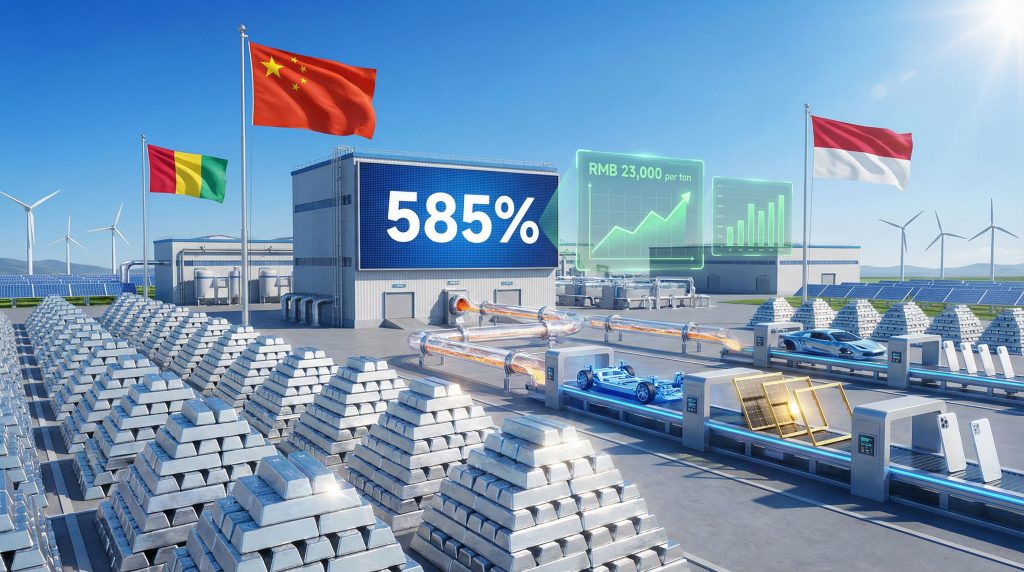

China Hongqiao Group shares surge represents a remarkable 585% stock increase since 2019, exemplifying how strategic vertical integration delivers competitive advantages during market volatility. The company operates an integrated production ecosystem spanning three continents, including power generation facilities in China, bauxite mining operations in Guinea established around 2014, and alumina refining capabilities in Indonesia.

This geographic diversification strategy addresses critical vulnerabilities in the global aluminium supply chain. With global primary aluminium output reaching approximately 73 million tonnes in 2024, securing upstream raw material access becomes increasingly vital for maintaining cost competitiveness and production reliability.

Furthermore, the integrated model provides several strategic benefits:

- Cost Management: Direct control over raw material sourcing reduces exposure to bauxite price volatility

- Supply Security: Multiple geographic sources minimize disruption risks from political instability

- Operational Flexibility: Integrated operations enable rapid product mix adjustments based on market demand

- Margin Optimization: Capturing value across the entire production chain improves overall profitability

Regional smelters in the Middle East account for roughly 9% of global aluminium production, making supply chain resilience a competitive differentiator. However, companies with diversified operational footprints can better navigate geopolitical disruptions and maintain consistent production schedules, particularly given the potential aluminum tariff impacts affecting global trade flows.

When big ASX news breaks, our subscribers know first

Analyzing Current Market Price Dynamics

Aluminium prices reached a four-year high on March 9, 2026, reflecting fundamental supply-demand imbalances driving market conditions. The metal has experienced a 25% price increase over the past year, supported by multiple converging factors affecting global production and consumption patterns.

Supply constraints originate from several sources creating cumulative market pressure. Geopolitical Disruptions include Middle Eastern production disruptions and Strait of Hormuz transport bottlenecks that constrain metal delivery to global markets. These regional challenges may increase reliance on Chinese producers to meet international demand requirements.

Raw Material Restrictions emerge from political instability in Guinea and Indonesian export restrictions that limit bauxite availability for global smelters. Indonesia's domestic processing mandate promotes local trading and production while reducing global export volumes.

Infrastructure Limitations affect metal distribution, particularly from regions experiencing geopolitical tensions. In addition, tariff exemptions for metals may influence global trading patterns and pricing structures.

| Supply Constraint Factor | Global Impact | Duration |

|---|---|---|

| Middle East Disruptions | 9% of global production | Ongoing |

| Indonesian Export Restrictions | Reduced global bauxite supply | Policy-dependent |

| Guinea Political Instability | Mining operation uncertainties | Variable |

| Transport Bottlenecks | Distribution delays | Event-driven |

These supply-side pressures coincide with strengthening demand from energy transition sectors, creating favourable pricing conditions for established producers with secure supply chains and flexible production capabilities.

Energy Transition Demand Drivers

The energy transition represents a fundamental shift in aluminium consumption patterns, with electric vehicles, solar panels, and wind turbines requiring specialised aluminium products. Major Chinese technology firms including Huawei Technologies, Xiaomi, and BYD source aluminium from integrated producers, highlighting the importance of technology sector partnerships.

Electric vehicle manufacturing demands specific aluminium grades optimised for weight reduction, thermal management, structural integrity, and corrosion resistance. These requirements create opportunities for producers capable of delivering high-specification materials while maintaining competitive pricing.

Solar panel and wind turbine applications require aluminium components with distinct specifications. For instance, solar panels need corrosion-resistant frames for 25+ year operational life, whilst wind turbines require lightweight nacelle construction for reduced tower stress.

Moreover, the renewable energy transformation creates new demand patterns that favour producers with flexible manufacturing capabilities. Traditional industrial demand patterns show declining consumption trends, requiring producers to adapt product mix strategies.

Companies successfully transitioning production toward higher-value applications demonstrate superior financial performance and market positioning. This shift aligns with broader mining industry evolution trends toward sustainability and technological advancement.

Geographic Risk Management Strategies

Hongqiao's strategic relocation of smelting operations to Yunnan province exemplifies effective geographic arbitrage, utilising hydropower access to reduce energy costs significantly. Energy represents approximately 30-40% of aluminium production costs, making power source optimisation critical for maintaining competitive margins.

Hydropower advantages include cost stability, environmental benefits, operational reliability, and regulatory compliance. The company's bauxite mining operations in Guinea, established around 2014, provide upstream supply security while diversifying geographic risk exposure.

Guinea contains approximately 25% of global bauxite reserves, making strategic partnerships essential for long-term raw material access. Indonesian alumina refining facilities complete the integrated supply chain, though domestic processing mandates create both opportunities and challenges.

Effective geographic diversification requires balancing operational efficiency with risk mitigation across multiple jurisdictions and regulatory environments. Consequently, companies with well-diversified operations demonstrate greater resilience during market volatility.

Market Structure and Competitive Positioning

China Hongqiao Group shares surge reflects the company's integrated production capabilities that provide significant influence over supply dynamics and market perceptions within the global aluminium industry. The company's strategic positioning enables rapid response to demand fluctuations while maintaining cost competitiveness through operational flexibility.

Key competitive advantages include production flexibility, product mix optimisation, cost management, and market intelligence. The company's relationships with major technology firms demonstrate successful customer diversification beyond traditional industrial applications.

This strategic positioning proves particularly valuable as energy transition accelerates and technology sector aluminium requirements expand. Furthermore, the company's ability to adapt to changing market conditions provides a significant competitive advantage.

Financial Performance and Market Valuation

The 585% stock price appreciation since 2019 reflects both company-specific strategic execution and broader aluminium market strength. This performance significantly outpaces broader market indices and commodity sector benchmarks, indicating effective management of operational and financial resources.

Several factors contribute to sustained financial outperformance, including margin expansion through vertical integration, volume growth via market share gains, product mix enhancement toward higher-margin applications, and cost optimisation through geographic arbitrage.

The recent 3%+ price increase in early March 2026 demonstrates continued investor confidence in the company's strategic direction and market positioning. Strong stock performance reflects expectations for sustained demand growth from energy transition sectors combined with effective supply chain management.

According to Bloomberg, the company recently announced plans for a $1.2 billion share sale, demonstrating confidence in future growth prospects and market conditions.

Market valuation metrics suggest investor recognition of the company's competitive advantages and growth prospects within the evolving aluminium industry landscape.

The next major ASX story will hit our subscribers first

Risk Assessment and Market Challenges

Despite strong market positioning, aluminium producers face several risk factors that could impact future performance and industry dynamics. Understanding these challenges enables better investment decision-making and strategic planning.

Macroeconomic Risks include global economic slowdown reducing industrial demand, trade tensions affecting international trade flows, currency volatility impacting export competitiveness, and interest rate changes affecting financing costs.

Industry-Specific Challenges encompass energy cost volatility, environmental regulations increasing compliance costs, technology disruption from alternative materials, and capacity additions affecting global supply balance. Additionally, tariffs impact markets through trade flow disruptions and pricing adjustments.

Operational Risks involve supply chain disruptions, political instability in key jurisdictions, equipment failures requiring maintenance, and safety incidents causing operational disruptions.

Effective risk management requires diversified operations, strong balance sheet positioning, and proactive adaptation to changing market conditions and regulatory environments.

Future Market Outlook and Strategic Considerations

The aluminium industry continues evolving as energy transition acceleration reshapes demand patterns and supply chain requirements. Companies positioned to capitalise on these structural changes demonstrate superior long-term growth prospects and financial performance potential.

Demand Growth Drivers include electric vehicle expansion requiring specialised grades, renewable energy infrastructure development, technology sector growth, and urbanisation trends in emerging markets.

Supply Side Developments encompass new capacity additions, technology improvements enhancing efficiency, recycling enhancement improving secondary production, and regulatory evolution affecting production methods.

Successful aluminium producers demonstrate several common characteristics: vertical integration capabilities, geographic diversification, technology sector partnerships, and operational flexibility. These attributes enable effective navigation of market volatility whilst capturing growth opportunities from structural demand shifts.

However, as reported by MarketWatch, aluminum stocks in Hong Kong and China continue rising amid Middle East supply disruptions, highlighting the ongoing market dynamics affecting the sector.

China Hongqiao Group shares surge reflects both company-specific strategic execution and favourable industry fundamentals supporting continued outperformance potential. The combination of supply constraints, demand growth from energy transition applications, and operational advantages creates a compelling investment thesis for well-positioned aluminium producers.

This analysis is based on publicly available information and should not be considered investment advice. Potential investors should conduct independent research and consult financial professionals before making investment decisions. Past performance does not guarantee future results, and all investments carry inherent risks including potential loss of principal.

Looking to Capitalise on the Aluminium Market Transformation?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including aluminium and bauxite opportunities, empowering subscribers to identify actionable trading positions ahead of broader market recognition. Begin your 14-day free trial today to secure a market-leading advantage in capturing the next major discovery as supply chain disruptions and energy transition demands continue reshaping global metal markets.