June 8, 2026

Understanding Aluminium's Forward Curve Before Looking at Any Single Session

Commodity markets rarely tell their full story through a single price point. The real intelligence lies in the relationship between different points on the forward curve, the behaviour of physical inventory, and how regional pricing benchmarks diverge from global standards. When these signals align, they confirm a directional market view. When they contradict each other, as they did during the June 5 LME aluminium session, the market is communicating something more nuanced: a near-term equilibrium sitting beneath a structurally more bullish medium-term outlook.

The LME aluminium cash price and stocks dipped while contracts gained on June 5, creating a pattern that requires more than surface-level reading. Understanding why requires first building a framework for how the LME price curve actually works, what inventory data genuinely signals, and where regional pricing fits into the global picture.

When big ASX news breaks, our subscribers know first

What the LME Price Curve Is Actually Measuring

The London Metal Exchange operates multiple simultaneous contract markets for aluminium, each representing the expected price of physical metal at a different future delivery point. The cash price, sometimes called the prompt price, reflects the cost of metal available for immediate delivery. The three-month contract is the most actively traded benchmark and serves as the reference point for most physical supply contracts globally. Beyond that, long-dated contracts like the December 2027 tenor represent market expectations for aluminium pricing roughly 18 months or more into the future.

The shape of the curve connecting these points is not arbitrary. It encodes collective market expectations about supply availability, demand trajectory, financing costs, and storage economics. Two primary curve configurations dominate:

-

Contango occurs when the cash price trades below the forward price, suggesting that near-term physical metal is adequately available and there is no urgency premium on immediate delivery. Holders of physical metal can be compensated for storage costs through the higher future price.

-

Backwardation occurs when the cash price trades above the forward price, indicating immediate tightness in physical supply. Buyers are willing to pay a premium to secure metal now rather than wait, compressing or eliminating the financial incentive to hold inventory.

The shape of the LME forward curve is one of the most reliable real-time indicators of physical market conditions in any base metal. A steepening contango signals comfort in near-term supply; a flattening or inverting curve signals emerging tightness long before official inventory data fully confirms it.

During the June 5 session, the LME aluminium cash price traded above the three-month forward price, a structural condition consistent with a market where the spot premium reflects some degree of physical demand relative to forward expectations. For broader context on how aluminum and alumina markets have been evolving, this dynamic is part of a wider structural story.

The June 5 Session: Reading Each Price Move in Context

The LME aluminium cash price and stocks dipped while contracts gained during the June 5 trading session, but the magnitude and direction of each move tells a differentiated story across the curve.

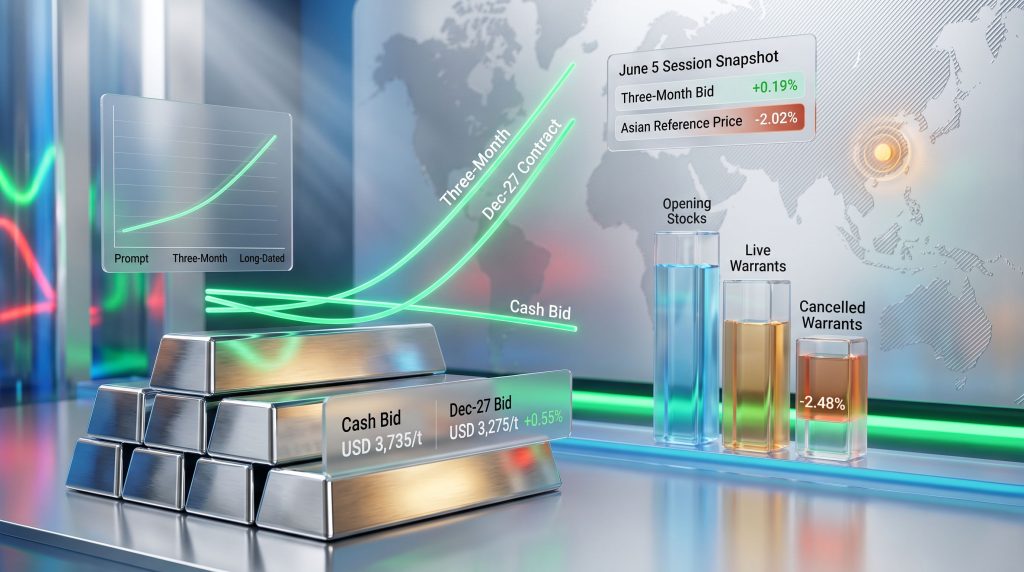

Session Data Summary: June 5 vs. June 4

- Cash bid: USD 3,738/t → USD 3,735/t (−0.08%)

- Cash offer: USD 3,739/t → USD 3,736/t (−0.08%)

- Three-month bid: USD 3,662/t → USD 3,669/t (+0.19%)

- Three-month offer: USD 3,663/t → USD 3,669.5/t (+0.18%)

- Dec-27 bid: USD 3,257/t → USD 3,275/t (+0.55%)

- Dec-27 offer: USD 3,262/t → USD 3,280/t (+0.55%)

- Asian Reference Price (three-month): USD 3,666/t → USD 3,592/t (−2.02%)

The cash price retreated by a marginal USD 3/t, a movement so small that it carries limited directional significance on its own. What gives the session analytical weight is the divergence: as the cash price softened slightly, every forward benchmark gained. The three-month contract added approximately USD 6.5/t on the bid side, while the December 2027 contract posted the session's strongest performance at +0.55%, rising USD 18/t on the bid.

This pattern, where near-term prices ease while long-dated contracts strengthen, is a recognisable market configuration with several potential explanations.

Three Mechanisms Behind the Cash-Forward Divergence

1. Near-term supply adequacy suppressing the cash premium

When physical metal is readily available for prompt delivery, there is no urgency premium embedded in the cash price. Buyers can source metal without competing aggressively for immediate delivery, which moderates the spot price even if medium and long-term demand expectations remain constructive.

2. Deferred demand expectations from structural end-use sectors

The strength in December 2027 contracts at +0.55% is particularly telling. Market participants pricing aluminium at those tenors are not reacting to today's inventory levels. They are expressing a view about aluminium consumption 18 months from now, a period closely associated with continued growth in electric vehicle production, renewable energy infrastructure, and lightweight construction materials — all of which are aluminium-intensive sectors operating on multi-year procurement cycles.

3. Regional arbitrage and currency-adjusted hedging

The Asian Reference Price dropped 2.02% in a single session, falling from USD 3,666/t to USD 3,592/t. This divergence from the global three-month benchmark, which actually rose during the same session, suggests that regional factors — potentially including currency movements, local demand shifts, or hedging activity from Asian smelters and consumers — were driving price behaviour independently of global market fundamentals. Furthermore, the aluminium tariff impact of recent trade policy shifts adds another layer of complexity to these regional pricing dynamics.

Decoding the Inventory Data: Stocks, Warrants, and What Each Signals

LME warehouse inventory data is not a single figure. It comprises three distinct metrics that each tell a different part of the physical market story.

| Inventory Metric | June 4 Level | June 5 Level | Change | Market Signal |

|---|---|---|---|---|

| Opening Stocks | 335,450 tonnes | 335,200 tonnes | −0.07% | Gradual physical drawdown |

| Live Warrants | 254,625 tonnes | 254,625 tonnes | 0.00% | Stable immediate availability |

| Cancelled Warrants | 80,575 tonnes | 78,575 tonnes | −2.48% | Moderation in pending withdrawals |

Opening stocks represent the total volume of aluminium held in LME-registered warehouses at the start of the trading session. The 0.07% decline from 335,450 tonnes to 335,200 tonnes is a reduction of just 250 tonnes, functionally negligible relative to total stock levels but directionally consistent with a gradual physical tightening trend.

Live warrants are the portion of warehouse stock that is immediately available for delivery against LME contracts. Their stability at 254,625 tonnes across both sessions indicates that the supply available for immediate physical delivery did not change, supporting the interpretation that the slight cash price decline reflected market mechanics rather than actual physical stress.

Cancelled warrants represent metal that has been earmarked for withdrawal from LME warehouses but has not yet physically departed. A decline in cancelled warrants from 80,575 tonnes to 78,575 tonnes (−2.48%) means that some previously flagged metal withdrawals were either deferred or cancelled. This is the subtlest but potentially most analytically interesting data point from the session.

A rising cancelled warrant figure is typically interpreted as a leading indicator of physical demand pressure, as buyers who have committed to taking delivery are pulling metal out of the exchange warehouse system. A declining cancelled warrant figure, as seen on June 5, suggests that some of this pending demand was absorbed, deferred, or redirected, which may partly explain the minor softening in the cash price.

The Asian Reference Price Divergence: A Signal Worth Watching

The 2.02% single-session decline in the LME aluminium three-month Asian Reference Price stands apart from every other movement in the June 5 session. While London-settled contracts across all tenors moved higher, the Asian Reference Price — which reflects pricing benchmarks relevant to physical transactions in Asian markets — fell sharply from USD 3,666/t to USD 3,592/t.

This type of regional divergence can arise from several dynamics that operate independently of the global LME benchmark:

- Localised demand weakness in key consuming regions such as China, Japan, or South Korea

- Currency movements that alter the effective cost of aluminium in local terms relative to USD-denominated contracts

- Regional smelter hedging activity that applies downward pressure to Asian-specific contract pricing

- Differences in physical market conditions between Asian warehouse locations and European or American LME depots

For traders and physical buyers operating across both markets, a divergence of this magnitude in a single session creates potential arbitrage signals that warrant monitoring over subsequent sessions to determine whether the gap closes or widens. In addition, the behaviour of top aluminium producers in response to these regional shifts can significantly influence how quickly such gaps are resolved.

Alumina Pricing: The Input Cost That Holds Steady

LME Alumina Platts remained unchanged at USD 305 per tonne, matching the prior session's close. Alumina is the primary raw material input for aluminium smelting, and its price stability is significant for understanding the margin environment facing primary aluminium producers.

When alumina costs are stable while aluminium output prices are broadly supported by rising forward contracts, smelters operating at normal efficiency rates face a relatively predictable cost structure. This reduces urgency around production curtailments and may partially explain why cancelled warrants declined rather than accelerated during the session, as smelters facing stable input economics have less incentive to rush physical metal withdrawals. The LME aluminium price data published by the exchange itself remains the authoritative reference for tracking these movements in real time.

The next major ASX story will hit our subscribers first

What the Full Picture Suggests for Market Positioning

Reading the June 5 session in isolation risks misinterpreting individually small signals. Reading them together, however, reveals a coherent narrative:

| Market Signal | Direction | Interpretation |

|---|---|---|

| Cash price | −0.08% | Near-term supply adequacy; no urgency premium |

| Three-month forward | +0.19% | Neutral-to-constructive medium-term demand view |

| December 2027 contract | +0.55% | Structural long-term demand expectations intact |

| Asian Reference Price | −2.02% | Regional divergence; potential arbitrage signal |

| Opening stocks | −0.07% | Gradual physical tightening in progress |

| Live warrants | 0.00% | Immediate physical availability unchanged |

| Cancelled warrants | −2.48% | Pending withdrawals moderating |

| LME Alumina Platts | 0.00% | Stable smelter input costs |

The composite picture is one of a market where near-term physical conditions are comfortable enough to prevent cash price escalation, but where forward expectations — particularly at long-dated tenors — remain constructive. The divergence between cash softness and futures strength is not a contradiction. It is an accurate reflection of a market with adequate prompt supply and a structurally supported longer-term demand outlook. Consequently, these dynamics also feed into broader conversations around the global steel outlook and cross-metal sentiment, as investors and procurement teams assess relative value across industrial metals. Furthermore, emerging conversations around green steel pricing suggest that sustainability-driven demand shifts are increasingly intersecting with traditional LME pricing mechanics.

Frequently Asked Questions: LME Aluminium Pricing and Inventory Mechanics

What is the LME aluminium cash price and how is it set?

The LME aluminium cash price is determined through open outcry and electronic trading during official LME ring sessions. It reflects the price for metal available for immediate delivery, with settlement typically occurring two business days after the trade date. Both a bid (the price a buyer will pay) and an offer (the price a seller will accept) are quoted simultaneously, with the spread between them reflecting market liquidity conditions.

What is the difference between live warrants and cancelled warrants?

Live warrants represent physical aluminium sitting in LME-registered warehouses that is available for delivery against open LME contracts. Cancelled warrants represent metal that a warrant holder has formally requested to withdraw from the warehouse system. Once a warrant is cancelled, the metal is no longer deliverable against LME contracts and is in the process of being physically removed from the warehouse.

Why does the Asian Reference Price sometimes move differently from the global benchmark?

The LME publishes Asian Reference Prices that reflect specific pricing windows aligned with Asian trading hours. These prices can diverge from London-session benchmarks due to differences in regional physical demand conditions, local currency movements against the USD, and the participation of different market participants who may be hedging against regional, rather than global, physical positions.

Can LME aluminium stocks fall while the cash price also declines?

Yes, and this is precisely what occurred during the June 5 session. Inventory drawdowns do not automatically translate into cash price increases if the drawdown is marginal and sufficient metal remains available for immediate delivery. The relationship between inventory levels and price is nonlinear, with price responses typically accelerating only when stocks fall toward critically low levels that threaten prompt delivery availability.

What does a rising December 2027 contract signal about long-term aluminium demand?

Rising long-dated contracts indicate that market participants are willing to pay higher prices for aluminium delivered well into the future. This is typically driven by expectations of sustained or growing demand from sectors like electric vehicles, grid-scale energy storage, and construction. Furthermore, aluminium price trends tracked by commodities data providers show how these long-term contract movements compare to historical patterns, combined with uncertainty about whether future smelter capacity will be sufficient to meet that demand at current price levels.

Readers seeking historical LME aluminium price data across multiple contract tenors can access benchmark pricing through the AL Circle price history portal. This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity price movements involve significant uncertainty, and past price patterns do not guarantee future market behaviour.

Want to Position Yourself Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into clear, actionable insights for both short-term traders and long-term investors — begin your 14-day free trial today and explore how historic discoveries have generated extraordinary returns for those who moved early.