June 21, 2026

The Energy Paradox at the Heart of Modern Aluminium Production

Few industries embody the contradictions of the global energy transition quite like aluminium. It is simultaneously one of the most electricity-hungry manufacturing processes on the planet and one of the most indispensable material inputs for the clean energy infrastructure the world urgently needs to build. Solar panel frames, wind turbine housings, electric vehicle body panels, high-voltage transmission cables: virtually every physical expression of the energy transition contains aluminium. Yet the role of renewable energy in aluminium industry supply chains remains underdeveloped, with production at scale still overwhelmingly dependent on coal-fired electricity in the world's largest producing nations.

That contradiction is now being forced into resolution. The global renewable energy buildout has reached a scale and a cost trajectory that makes the continued reliance on fossil-fuel-powered smelting not just environmentally indefensible but increasingly economically irrational. Understanding what this structural shift means for aluminium producers, across China, Europe, the United States, and India, requires looking carefully at both the pace of the clean power transition and the unique technical demands that make aluminium smelting one of the most challenging industrial loads to decarbonise.

When big ASX news breaks, our subscribers know first

How Fast Is the Renewable Energy Buildout Actually Moving?

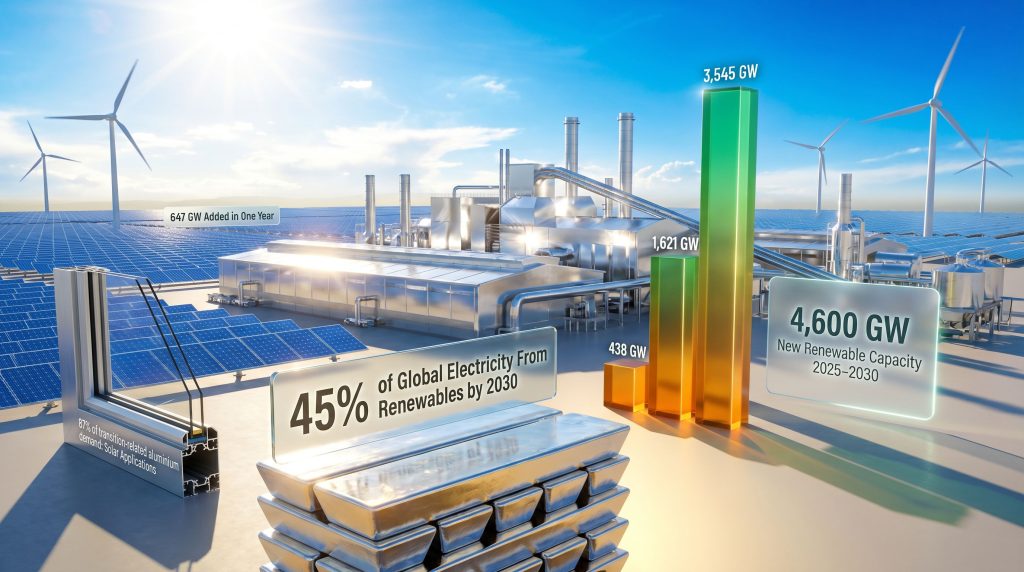

The numbers involved in the global renewable energy expansion have moved well beyond the realm of incremental progress. According to the International Energy Agency's Renewables 2025 Global Status Report, global renewable power capacity additions between 2025 and 2030 are projected to reach approximately 4,600 GW, nearly double the approximately 2,400 GW added during the prior five-year period from 2019 to 2024. The implication is not simply that renewables are growing: it is that the rate of growth itself is accelerating.

Solar photovoltaic technology is the dominant force behind this expansion, accounting for roughly 80% of all new renewable electricity capacity additions projected through 2030. By the end of 2025, cumulative global solar PV capacity had reached approximately 2,900 GW, following a single-year addition of 647 GW. Combined solar and wind installations in 2025 reached 814 GW, lifting total global installed renewable capacity to approximately 4,174 GW, according to IEA data.

Wind energy, while growing more slowly than solar in percentage terms, still recorded a significant year-on-year acceleration. New wind capacity additions rose from approximately 113 GW in 2024 to 167 GW in 2025, representing a 47% annual increase, with total installed wind capacity reaching around 1,300 GW globally by the end of 2025.

The five-year comparison reveals just how dramatically deployment rates have shifted across technologies:

| Technology | 2013-2018 Capacity (GW) | 2019-2024 Capacity (GW) | 2025-2030 Projection (GW) | Period-on-Period Change |

|---|---|---|---|---|

| Solar PV (Utility + Distributed) | 438 | 1,621 | 3,545 | +118% (2019-24 to 2025-30) |

| Onshore + Offshore Wind | 297 | 565 | 872 | +54% (2019-24 to 2025-30) |

| Combined Installed Renewables (End 2025) | – | – | ~4,174 | +47% wind YoY (2025) |

The consequence of this buildout for energy-intensive industries is straightforward but profound. As the IEA notes, levelised costs of electricity for utility-scale solar PV have fallen by approximately 90% since 2010, while onshore wind costs have declined by roughly 70% over the same period. For aluminium smelters evaluating long-term power procurement strategies, this cost trajectory signals a structural erosion of the economic case for coal-based power, independent of any carbon pricing mechanism.

"The global renewable buildout is on track to supply 45% of all electricity generation worldwide by 2030, representing a fundamental restructuring of power systems that no energy-intensive industry can afford to ignore." (IEA, Renewables 2025)

Why Electricity Is the Defining Variable in Aluminium Economics

The Energy Intensity Problem No Other Industry Shares

Aluminium smelting via the Hall-Heroult electrolysis process consumes approximately 13 to 15 megawatt-hours of electricity per tonne of primary metal produced. This makes it one of the most electricity-intensive industrial operations on earth, and it means that the source of that electricity is not merely an environmental consideration: it is a primary cost and competitive variable that shapes entire business models.

The industry's current carbon footprint reflects this dependency. Aluminium production accounts for approximately 2% of global greenhouse gas emissions, with the vast majority of that total attributable to coal-fired electricity powering smelting operations, particularly in China. Furthermore, the emissions differential between power sources is stark:

| Power Source | Relative CO2 Emissions | Decarbonisation Potential |

|---|---|---|

| Coal-fired grid power | Baseline (highest) | Low without grid transition |

| Natural gas | ~40-50% lower than coal | Moderate (transition fuel only) |

| Hydropower | Near-zero operational emissions | High, proven at scale |

| Solar + Wind (direct or PPA) | Near-zero operational emissions | High, rapidly scaling |

| Nuclear | Near-zero operational emissions | High, dispatchable baseload |

A coal-powered aluminium smelter generates roughly five times more CO2 per tonne of metal than an equivalent facility operating on renewable electricity. This emissions gap is not a marginal compliance issue: it is the central variable that will determine competitive positioning in green supply chains over the coming decade. Major aluminium mining companies are increasingly factoring this reality into their long-term capital allocation strategies.

Where the World's Largest Aluminium Producers Stand

China: Scale, Coal Dependency, and the Pace of Transition

China produces approximately 55% of global primary aluminium and remains the world's largest single source of smelting-related emissions, with the majority of its output tied to coal-heavy provincial electricity grids. The structural tension here is significant: China simultaneously leads the world in annual solar and wind capacity additions (adding approximately 216 GW of solar alone in 2024, according to China's National Energy Administration) while maintaining an aluminium industry that still draws most of its power from fossil fuels.

This creates the single largest decarbonisation challenge in the global aluminium supply chain. Provincial grid composition varies considerably across China, with provinces like Yunnan and Sichuan offering substantially lower-carbon power profiles due to hydropower resources, while Xinjiang and Inner Mongolia, which host significant smelting capacity, remain coal-dominated. The pace at which China's renewable buildout translates into lower-carbon aluminium production will define the global industry's emissions trajectory more than any other single factor.

Europe: Carbon Pricing as the Accelerant

European aluminium producers operate within the world's most demanding carbon pricing environment. The EU Emissions Trading System (ETS) applies a cost to carbon-intensive production, while the Carbon Border Adjustment Mechanism (CBAM), now in its transitional phase, is designed to impose equivalent carbon costs on aluminium imports from high-emissions jurisdictions. This mechanism fundamentally alters competitive dynamics by removing the cost advantage that coal-powered foreign producers have historically held in the European market.

European smelters are increasingly securing long-term Power Purchase Agreements with wind and solar developers to lock in clean electricity at predictable rates, shielding themselves from both carbon cost escalation and wholesale electricity price volatility. Initiatives such as Gladstone aluminium repowering demonstrate how major producers are actively restructuring their energy infrastructure to meet these new demands.

United States: Industrial Policy and Reshoring Dynamics

The Inflation Reduction Act has created substantial financial incentives for industrial decarbonisation in the United States, including clean electricity tax credits directly relevant to energy-intensive manufacturers. US aluminium tariffs have added further complexity to reshoring decisions, making access to competitively priced clean power an even more critical factor in new investment planning. American aluminium producers are exploring direct integration with solar and wind projects, particularly across the southwest and plains states where renewable resources are most abundant.

Reshoring of domestic aluminium capacity under current industrial policy frameworks is increasingly conditional on access to clean power, creating a structural link between renewable energy availability and new investment decisions. The Alcoa renewable power venture with Ignis and EQT illustrates precisely how leading producers are responding to this dynamic, establishing dedicated clean energy partnerships to underpin smelter operations.

India: The Inflection Point Approaching

India is among the fastest-growing renewable energy markets globally, with solar capacity expanding aggressively toward government targets exceeding 500 GW by 2030. The Central Electricity Authority reports that India added approximately 13 GW of solar capacity in calendar year 2024, with cumulative solar capacity projected to exceed 200 GW by 2026. For domestic aluminium producers, clean power procurement costs are approaching, and in some regions beginning to undercut, coal-based electricity alternatives, creating a genuine economic inflection point in the energy transition calculus.

Aluminium's Dual Role: Consumer and Enabler of the Energy Transition

The Materials Demand Loop That Makes This Sector Unique

What distinguishes aluminium from most other carbon-intensive industries is its indispensability to the clean energy transition itself. According to IRENA's analysis of reaching zero with renewables, the renewable energy sector is projected to require an additional 5.2 million tonnes of aluminium by 2030, driven by escalating demand across solar arrays, wind turbines, electric vehicles, battery storage systems, and grid modernisation infrastructure.

Critically, an estimated 87% of all incremental aluminium demand generated by the energy transition originates from solar energy applications, primarily structural framing systems and electrical wiring components in utility-scale and distributed solar arrays. This creates a self-reinforcing dynamic: every gigawatt of solar capacity added increases demand for aluminium, which must in turn be produced with increasing quantities of renewable electricity.

| Application | Aluminium Role | Primary Demand Driver |

|---|---|---|

| Solar PV Arrays | Structural frames, mounting systems, wiring | 87% of transition-related AL demand |

| Wind Turbines | Nacelle housings, structural components | Offshore wind scale-up |

| Electric Vehicles | Body panels, battery enclosures, drive motors | Global EV fleet expansion |

| Battery Storage Systems | Casing, current collectors | Grid-scale storage deployment |

| Power Transmission | High-voltage cables, conductors | Grid modernisation globally |

"The aluminium industry faces a structural paradox: it must decarbonise its own production processes at pace while simultaneously supplying the physical materials that make decarbonisation possible across the broader economy. This dual role makes the sector's energy transition both uniquely urgent and strategically complex."

The Viable Pathways to Decarbonising Aluminium Smelting

Pathway 1: Hydropower Integration

Hydropower remains the most operationally proven renewable energy source for aluminium smelting. It provides continuous, dispatchable baseload power at near-zero carbon intensity, meeting the critical 24-hour operational requirement that intermittent sources like solar cannot fulfil without storage. Norway's aluminium industry represents the benchmark model, with dedicated hydro infrastructure supplying approximately 10 TWh of clean energy annually across more than 20 operating hydropower stations.

The hydropower model is geographically constrained but defines the performance standard against which all other decarbonisation pathways are evaluated. The broader pursuit of a zero-carbon metals strategy is increasingly influencing how major producers approach energy sourcing decisions across their entire portfolio of operations.

Pathway 2: Power Purchase Agreements with Solar and Wind Developers

In regions without hydropower access, long-term PPAs between smelter operators and renewable energy developers are emerging as the primary decarbonisation mechanism. As LCOE for solar and wind continues its structural decline, PPAs are becoming cost-competitive with coal-based grid power across more markets. Structuring effective agreements requires smelter operators to carefully balance:

- Contract tenor and price certainty over the operational life of the smelter

- Capacity guarantees and penalties for generation shortfalls

- Intermittency risk management through hybrid portfolios or co-located storage

- Transmission access and grid connection costs

- Regulatory and offtake credit recognition under green product certification schemes

Pathway 3: Process-Level Innovation

Several emerging technologies target the smelting process itself, rather than simply the power source. The Clean Energy Council has highlighted a number of these innovations as critical to forging a genuinely sustainable future for domestically produced aluminium:

- Inert anode technology replaces carbon-based anodes with non-consumable inert materials, eliminating direct CO2 emissions from electrolysis independent of the grid's carbon intensity. If commercialised at scale, this represents the most transformative process-level innovation in primary aluminium production history.

- Aluminium chloride electrolysis offers an alternative smelting chemistry with lower direct process emissions than the conventional Hall-Heroult method.

- Bio-carbon anodes substitute fossil-carbon anode materials with bio-based alternatives, reducing process emissions without requiring wholesale process redesign.

- Carbon capture, utilisation, and storage (CCUS) provides an interim solution for smelters where full renewable power transition is not immediately feasible.

- Renewable Metal Fuels (ReMeF) represents a lesser-known but intriguing concept: aluminium produced with renewable electricity can function as a long-duration energy storage medium by reacting with water to generate hydrogen for fuel cells, with negligible energy loss over months of storage. This positions green aluminium not merely as a decarbonised product but as a potential energy carrier in its own right.

Pathway 4: Recycling and Circular Economy Acceleration

Secondary aluminium production from scrap requires approximately 95% less energy than primary smelting, making recycling the most immediately accessible decarbonisation lever available to the industry. However, recycling alone cannot resolve the supply challenge: scrap availability is structurally constrained by the long lifecycle of aluminium embedded in buildings, infrastructure, and vehicles, and recycled metal cannot always meet the metallurgical specifications required for high-performance structural applications.

The industry consensus, reflected in major sustainability frameworks including the Aluminium Stewardship Initiative (ASI), is that accelerated recycling rates and systematic transition of primary smelting to renewable power must advance in parallel, not as alternatives.

The next major ASX story will hit our subscribers first

The Cost of Getting This Right, and the Risk of Getting It Wrong

A Nearly One Trillion Dollar Transition

Transitioning the global aluminium sector to renewable energy and achieving net-zero emissions by 2050 is estimated to require close to $1 trillion in additional capital investment, encompassing renewable power infrastructure, smelter retrofits, process technology upgrades, and grid connection projects. This positions aluminium decarbonisation as one of the largest industrial capital allocation challenges of the coming three decades.

| Scenario | Required Emissions Reduction by 2050 | Aluminium Demand Change | Investment Requirement |

|---|---|---|---|

| 1.5 degrees C Aligned Pathway | -77% vs. current baseline | +50-80% from renewables sector | ~$1 trillion additional |

| 2 degrees C Pathway | -50-60% vs. current baseline | +30-50% from renewables sector | Significant but lower |

| Business as Usual | Minimal reduction | Demand growth unaddressed | Stranded asset risk escalates |

Three Forces Reshaping the Competitive Hierarchy

The window for strategic positioning is narrowing as three mutually reinforcing forces converge:

- Falling renewable electricity costs are progressively eroding the economic rationale for coal-based smelting, even in markets without carbon pricing mechanisms. As LCOE for solar continues declining, the cost parity point with coal power is being reached across an expanding number of geographies.

- Regulatory escalation through carbon border taxes, emissions trading systems, and green procurement standards is accelerating the timeline for investment decisions. The CBAM in particular is introducing a direct financial penalty for high-emissions aluminium entering the EU market, restructuring competitive dynamics for exporters from coal-dependent producing nations.

- Demand-side pressure from automotive, construction, and packaging customers requiring verified low-carbon aluminium is creating a measurable green premium that rewards producers who can credibly demonstrate clean power credentials. This customer-driven signal is amplifying regulatory pressure and creating commercial urgency independent of policy timelines.

Smelters that secure long-term renewable power agreements during the current buildout window will gain a durable competitive cost advantage. Producers that delay face compounding exposure: rising carbon costs, stranded coal-power assets, and progressive exclusion from the green supply chains that will define high-value aluminium markets through 2030 and beyond.

Frequently Asked Questions

What share of global primary aluminium is currently produced with renewable electricity?

Estimates suggest that roughly 30% of global primary aluminium is produced using low-carbon electricity, with the majority of that figure attributable to hydropower in Norway, Canada, Iceland, and Brazil. The precise figure varies depending on methodology and how regional grid composition is accounted for. The remaining 70% is predominantly coal-powered, concentrated in China's major smelting provinces.

Why is hydropower the preferred renewable source for aluminium smelters?

Aluminium smelters operate continuously, 24 hours a day, and cannot tolerate power interruptions without significant process disruption and equipment damage to the electrolytic cells. Hydropower provides dispatchable baseload power at consistent output, a profile that solar and wind cannot replicate without co-located storage infrastructure. This reliability characteristic makes hydro the benchmark against which all other clean power options are measured for smelting applications.

How does the EU Carbon Border Adjustment Mechanism affect aluminium trade?

The CBAM applies an effective carbon cost to aluminium imported into the European Union from jurisdictions with lower or no equivalent carbon pricing. This creates a direct financial incentive for exporters, particularly from high-emissions producing nations in Asia and the Middle East, to decarbonise their production or accept a competitive disadvantage in the EU market. As the mechanism moves beyond its transitional phase, its impact on aluminium trade flows and investment decisions is expected to intensify.

Can recycled aluminium fully replace primary production?

Recycling is critical but structurally insufficient as a standalone solution. Scrap supply is constrained by the long in-use lifecycle of aluminium in infrastructure and construction, and recycled metal cannot always achieve the metallurgical specifications required for certain high-performance applications. Both primary smelting and recycling must decarbonise, with the two pathways advancing concurrently rather than sequentially.

What makes inert anode technology potentially transformative?

Conventional aluminium electrolysis consumes carbon anodes that react during the smelting process, generating direct CO2 emissions regardless of the power source. Inert anode technology replaces these consumable carbon materials with non-reactive alternatives, eliminating process-level CO2 emissions entirely. Combined with renewable electricity, inert anode smelting could reduce aluminium's carbon footprint to near zero across both scope 1 and scope 2 emissions categories. Commercial-scale deployment remains in development, but successful industrialisation would represent the most significant process innovation in primary aluminium production since Hall and Heroult developed electrolysis in the 1880s.

The Strategic Outlook Through 2030 and Beyond

The integration of renewable energy in the aluminium industry has moved decisively from aspiration to structural necessity. The projected addition of 4,600 GW of global renewable capacity by 2030, led by the exponential growth of solar PV, will materially reduce the cost of clean electricity across every major aluminium-producing region. The economic, regulatory, and commercial signals are now aligned in the same direction for the first time.

Consequently, producers who resolve aluminium's dual role — decarbonising their own operations while supplying the materials the broader energy transition demands — will define the next competitive hierarchy in global aluminium markets. Those who treat the energy transition as a future compliance exercise rather than a present strategic priority risk finding themselves on the wrong side of a cost curve, a regulatory framework, and a customer base that is moving faster than the industry's traditional investment cycles.

This article contains forward-looking statements and projections based on data published by the International Energy Agency and other third-party sources. Projections regarding renewable capacity additions, investment requirements, emissions reductions, and demand growth are inherently uncertain and subject to change based on policy, technology, and market developments. Nothing in this article constitutes financial or investment advice.

Want To Identify The Next Major Mineral Discovery Before The Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including those powering the materials driving the global energy transition — instantly turning complex data into actionable investment insights. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.