June 30, 2026

The Arithmetic of a Broken Safety Net: Understanding the Hormuz Supply Crisis

Energy markets are built on layers of redundancy. Strategic reserves exist precisely because physical infrastructure is fragile, geopolitical situations are volatile, and the consequences of supply failure cascade far beyond the energy sector itself. The architecture of global oil security has always rested on the assumption that no single disruption could outpace the combined buffer of coordinated emergency reserves, alternative routing capacity, and demand-side adjustment. The Strait of Hormuz closure in early 2026 is now stress-testing every one of those assumptions simultaneously, and the results are exposing just how thin the IEA oil safety net depleted Strait of Hormuz closure has made global energy buffers.

When big ASX news breaks, our subscribers know first

How a Single Waterway Became the World's Most Critical Energy Artery

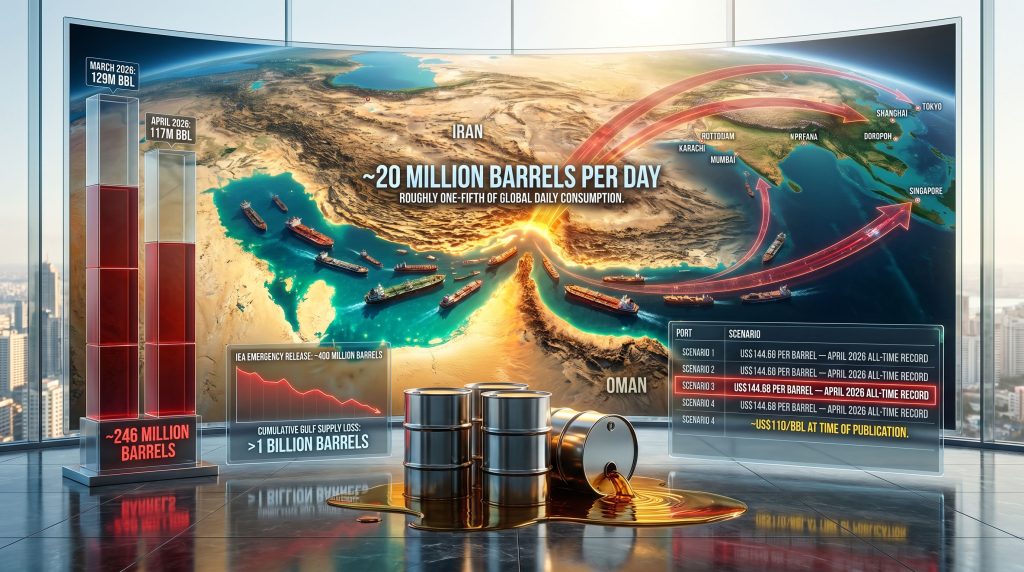

The Strait of Hormuz, the narrow passage connecting the Persian Gulf to the Gulf of Oman, handles approximately 20 million barrels of oil and oil products every single day under normal operating conditions. That figure represents roughly one-fifth of total global consumption and a substantial share of internationally traded liquefied natural gas. No other maritime corridor comes close to replicating that throughput.

The concentration of energy flow through a passage only 33 kilometres wide at its narrowest navigable point is not an accident of policy. It is a product of geology, infrastructure investment history, and the economic gravity of Gulf producer nations whose reserves sit predominantly on the eastern side of the Arabian Peninsula. Decades of upstream development oriented toward deepwater tanker loading means that the overwhelming majority of Gulf export capacity has no viable land-based alternative.

Which Economies Carry the Most Exposure?

Vulnerability to a Hormuz disruption is not distributed evenly. The Atlantic Basin, anchored by North American and Brazilian production, holds a degree of structural insulation that Asia-Pacific import-dependent economies simply do not have.

The nations facing the sharpest near-term impact include:

- India, where household LPG cooking fuel arrivals have fallen more than 40% below pre-conflict baselines, producing widespread queuing at distribution points

- Pakistan, the Philippines, and Sri Lanka, each of which has introduced four-day working weeks to compress industrial and commercial energy consumption

- Southeast Asian nations broadly, several of which have implemented work-from-home mandates to reduce transport fuel demand

- European and East Asian buyers on long-term Qatari LNG contracts, now facing multi-year supply disruption following infrastructure damage at Ras Laffan

The vulnerability hierarchy matters for investors and policymakers alike. Nations without domestic production capacity, alternative supplier relationships, or significant strategic reserve holdings face a fundamentally different risk profile than those with access to Atlantic Basin supply chains.

What the IEA Oil Safety Net Depletion Actually Means

The phrase IEA oil safety net depleted Strait of Hormuz closure is widely used but rarely unpacked with precision. Understanding what it actually describes requires examining how the emergency stockholding system is designed to function, and where that design is now under its most severe strain. Furthermore, oil market disruption of this magnitude has rarely been observed in modern energy history.

How Strategic Petroleum Reserves Are Structured and Triggered

IEA member nations are obligated to maintain emergency oil stocks equivalent to at least 90 days of net imports. These reserves are held by governments directly, by national oil companies under government mandate, or through industry stockholding obligations. Coordinated release decisions are made collectively when supply disruptions meet threshold criteria.

Historical precedents for coordinated releases include:

- The Gulf War supply shock of 1990 to 1991, when Iraqi production was removed from global markets

- The Libyan civil conflict in 2011, which briefly removed approximately 1.4 million barrels per day of light crude

- The post-COVID demand recovery period, when releases were used to cap price spikes driven by demand-supply imbalances

None of these precedents involved a simultaneous disruption of six major producers combined with physical closure of the world's most critical maritime chokepoint.

The 400 Million Barrel Intervention: Scale Against Context

Following the onset of conflict, the IEA initiated an emergency release programme totalling 400 million barrels. In scale, this is among the largest coordinated emergency interventions in the organisation's history. Relative to the magnitude of the supply shock, however, it has proven structurally insufficient. According to the IEA, the scale of reserve depletion now unfolding is unprecedented in the organisation's recorded history.

| Metric | Figure |

|---|---|

| IEA emergency barrels released | ~400 million barrels |

| Inventory draw in March 2026 | 129 million barrels |

| Inventory draw in April 2026 | 117 million barrels |

| Combined two-month draw | ~246 million barrels |

| Cumulative Gulf supply loss to date | >1 billion barrels |

| Projected total deficit by September 2026 | ~900 million barrels |

The mathematics are stark. The two-month inventory drawdown of 246 million barrels consumed more than 60% of the entire emergency release in just eight weeks. The cumulative Gulf output loss, exceeding one billion barrels, dwarfs every prior single-event disruption in the IEA's recorded history.

The Asymmetry Between Depletion and Replenishment

One of the least-discussed dynamics in the current crisis is the fundamental asymmetry between how quickly strategic reserves can be drawn down and how slowly they can be rebuilt. The IEA has assessed that restoring depleted global stockpiles would require approximately one million barrels per day of sustained surplus supply maintained over three consecutive years, layered on top of normal underlying demand growth.

That timeline assumes a relatively prompt conflict resolution. Consequently, every additional week of closure extends the replenishment horizon further.

When the IEA's safety net is described as depleted, it does not mean reserves have reached zero. It means the buffer between a supply shock and direct market impact has narrowed to the point where any secondary disruption, however modest, could trigger cascading price effects with no meaningful absorption capacity remaining.

Scenario-by-Scenario Breakdown of Production Loss Trajectories

The range of outcomes from here depends primarily on conflict duration and the extent of infrastructure damage already sustained. Four distinct scenarios frame the plausible trajectory space.

Scenario 1: The Strait Reopens in Mid-2026

Even in the most optimistic case, recovery is not swift. The US Department of Defense has indicated that clearing sea mines from the Strait alone could require several months of sustained naval operations. Following any physical reopening, shipping normalisation is estimated to take a further two to three months before upstream production recovers meaningfully.

Under this scenario, the IEA projects full-year 2026 global oil supply averaging approximately 100 million barrels per day, a decline of 3.9 million barrels per day year-on-year. The market would remain in deficit through at least the fourth quarter.

Scenario 2: Infrastructure Damage Extends the Timeline

Qatar's Ras Laffan Industrial City, the world's largest LNG production hub, sustained critical damage from airstrikes in early March 2026. QatarEnergy has indicated that some facility repairs could take three to five years to complete. The Mesaieed facility has also been critically impaired.

The LNG implications extend well beyond oil pricing. Indeed, the disruption to global LNG supply infrastructure at Ras Laffan creates multi-year gaps that cannot be filled quickly from alternative sources, given the capital-intensive nature of LNG liquefaction infrastructure.

Scenario 3: Inventories Continue Drawing at the Current Pace

North Sea Dated crude reached US$144.68 per barrel in April 2026, an all-time record surpassing the 2008 financial crisis high. Prices have since retreated to approximately US$110 per barrel, but the market remains structurally in deficit.

Hamad Hussain, Climate and Commodities Economist at Capital Economics, has assessed that if the Strait remains effectively closed and commercial oil inventories continue drawing down at recent rates, market conditions would be consistent with Brent crude prices approaching record highs during the northern hemisphere summer of 2026. This level of crude oil volatility is placing extraordinary pressure on import-dependent economies with limited hedging capacity.

Scenario 4: Extended Conflict and Permanent Capacity Destruction

The most severe scenario involves distinguishing between temporary logistics disruption and permanent capacity destruction. Gulf producer output is running 14.4 million barrels per day below pre-war levels across Saudi Arabia, Iraq, the UAE, Kuwait, Iran, and Qatar combined.

| Scenario | Hormuz Status | Price Trajectory | Recovery Timeline |

|---|---|---|---|

| Optimistic | Reopens June 2026 | Gradual decline from US$110/bbl | 2-3 years to full restocking |

| Base Case | Reopens Q3 2026 | Elevated through Q4 2026 | 3+ years with infrastructure damage |

| Adverse | Remains closed H2 2026 | Approaches record highs above US$144/bbl | 4-5 years; structural LNG shortfall |

| Severe | Extended conflict and infrastructure destruction | Sustained price shock; rationing risk | Decade-scale for full Qatar LNG restoration |

Atlantic Basin Compensation: Record Output Against a Structural Ceiling

The United States reached a record crude output of 14 million barrels per day in April 2026, while Brazil recorded its third consecutive production milestone. Combined, Atlantic Basin exports have risen by approximately 3.5 million barrels per day above pre-conflict baselines. This additional volume has been redirected urgently toward energy-stressed markets east of the Suez Canal.

This represents a meaningful supply-side response. However, it does not come close to arithmetically closing a 14.4 million barrel per day Gulf deficit. The oil price shock reverberating through energy markets illustrates precisely how inadequate even record Atlantic Basin output is against a disruption of this magnitude.

Several structural factors limit the Atlantic Basin's compensatory capacity:

- Port infrastructure constraints at US Gulf Coast and Brazilian export terminals limit the pace at which additional barrels can be loaded and dispatched

- Refinery configuration mismatches mean that replacement crude varieties do not always align with refinery feedstock specifications in Asian import markets calibrated for Gulf crude grades

- Tanker availability and voyage economics are stretched by the extended routing distances involved, with Cape of Good Hope rerouting adding significant time and cost

Pipeline Bypass Routes: Useful but Finite

Saudi Aramco's East-West Pipeline and the UAE's Fujairah route provide the most operationally viable bypass mechanisms currently available. Saudi Arabia has ramped Red Sea exports through the East-West corridor, while the UAE has directed additional volumes through the Abu Dhabi Crude Oil Pipeline to Fujairah for export.

Both routes are operating, but both carry throughput ceilings that represent a fraction of normal Hormuz volumes. Their contribution is to soften the supply gap, not eliminate it.

Demand Destruction: Significant, Insufficient, and Unevenly Distributed

The IEA now forecasts global oil demand to contract by 420,000 barrels per day year-on-year in 2026, a swing of 1.3 million barrels per day from the pre-conflict growth forecast. This demand destruction, while historically significant, is not large enough to rebalance markets at current inventory draw rates.

Sector-level impacts illustrate how demand destruction is playing out in practice:

- Petrochemicals: LPG and naphtha demand across Asia has collapsed as Gulf feedstock supply chains have fractured, echoing patterns last seen during the 2008 financial crisis

- Aviation: Global Revenue Passenger Kilometres declined 0.6% year-on-year in March 2026, the first contraction in five years, driven by Middle East airspace closures and route disruptions

- Retail fuel: UK petrol station sales surged approximately 39% in early March as panic-buying behaviour took hold

- Household energy: India's LPG cylinder distribution system is under acute stress, with cooking fuel arrivals down more than 40% from pre-war levels

- Industrial activity: Multiple South and Southeast Asian economies have introduced compressed working weeks and work-from-home mandates to reduce fuel demand

The distributional dimension of demand destruction deserves particular attention. High-income economies adjust primarily through behavioural shifts and price-induced efficiency. Lower-income import-dependent nations, however, face forced rationing with direct welfare and food security consequences.

The next major ASX story will hit our subscribers first

Cascading Systemic Risks Beyond the Oil Price Headline

Food Security and Agricultural Supply Chains

The disruption extends well beyond transport fuel. Fertiliser production is heavily dependent on natural gas and LPG feedstocks, many of which have been disrupted by the same supply chain fractures affecting oil markets. Import-dependent agricultural nations in South and Southeast Asia are facing compounding food and fuel stress simultaneously, a combination that carries historical echoes of the 1973 oil embargo's agricultural transmission effects.

Shipping Economics and Global Trade

Tankers rerouting around the Cape of Good Hope add significant voyage time and operating costs compared to Hormuz transit. Port congestion cascades as delayed cargo creates downstream logistics gridlock across multiple commodity classes. War-risk insurance premiums have become a structural cost increase embedded across global shipping, not merely a temporary surcharge.

The 1970s Parallel: Structural Shock or Cyclical Disruption?

Analyst comparisons to 1970s-style oil shocks are meaningful in some respects. Supply concentration, a geopolitical trigger mechanism, and demand-side rigidity are all present. However, several important differences distinguish the current situation from that historical precedent.

Non-OPEC supply diversity is substantially greater today. Furthermore, OPEC's market influence, whilst still significant, operates within a far more complex global supply landscape than it did in 1973. Demand-side adjustment mechanisms, including fuel efficiency standards, electric vehicle penetration, and digital substitutes for physical travel, operate faster than in the 1970s.

The critical variable is conflict duration. If the disruption proves shorter than the 1973 to 1974 episode, market adjustment mechanisms may prevent a structural dislocation. A prolonged conflict, in contrast, converts a cyclical supply shock into an architectural problem for global energy systems.

The Three-Year Restocking Challenge and Policy Pathways Forward

The IEA's assessment of what full market restoration requires is sobering. Approximately one million barrels per day of sustained surplus supply maintained over three consecutive years, above and beyond normal demand growth, would be needed to rebuild depleted global inventories to pre-crisis levels.

Emergency policy options that remain available to IEA member nations include:

- Additional coordinated strategic reserve releases if physical supply conditions deteriorate further

- Demand-side policy interventions including fuel efficiency mandates, industrial consumption caps, and formal rationing frameworks in the most exposed import economies

- Accelerated diplomatic engagement with major non-IEA consumers, particularly China and India, to coordinate inventory management and prevent competitive stockpiling behaviour

The Hormuz crisis has not merely created a short-term supply problem. It has exposed three structural vulnerabilities in global energy architecture that will shape infrastructure investment and policy priorities for years beyond any ceasefire: excessive concentration of energy flows through a single maritime chokepoint, insufficient strategic reserve depth relative to major producer-region disruption scenarios, and inadequate infrastructure redundancy across both supply routing and downstream storage systems.

Frequently Asked Questions

What does it mean when the IEA oil safety net is described as depleted?

The IEA oil safety net refers to the coordinated strategic petroleum reserve system maintained by member nations, designed to release emergency supply during major disruptions. Describing the IEA oil safety net depleted Strait of Hormuz closure as a critical threshold signals that the buffer between a supply shock and direct market impact has narrowed dangerously. The combined March and April 2026 inventory draws of 246 million barrels consumed more than 60% of the emergency release programme in eight weeks, leaving remaining buffers dangerously thin relative to the ongoing supply deficit. Analysts tracking the crisis warn that any secondary disruption could now trigger cascading price effects with no meaningful absorption capacity remaining.

Can Saudi Arabia's pipelines replace Hormuz shipping capacity?

No. Saudi Aramco's East-West Pipeline and the UAE's Fujairah route provide valuable partial bypass capacity, but their combined throughput is a fraction of pre-closure Hormuz volumes. These routes reduce, but cannot arithmetically close, a supply gap exceeding 14 million barrels per day.

How long would rebuilding global oil inventories take after a reopening?

The IEA estimates that full inventory restoration would require approximately one million barrels per day of surplus supply sustained over three years, on top of underlying demand growth. Mine clearance alone could take months following any reopening, with two to three additional months needed for shipping normalisation before upstream production recovers meaningfully.

Which countries face the most severe near-term consequences?

South and Southeast Asian import-dependent economies carry the greatest acute exposure. India, Pakistan, the Philippines, and Sri Lanka are all experiencing significant supply stress, with several implementing four-day working weeks or work-from-home mandates to compress energy consumption. Nations without domestic production, diversified supplier relationships, or strategic reserve holdings face welfare and food security consequences that extend well beyond fuel pricing.

Want to Stay Ahead of the Commodity Shifts Reshaping Energy Markets?

When supply shocks of this magnitude ripple through global markets, the flow-on effects reach far beyond oil — and Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries that could represent actionable opportunities amid the volatility. Explore historic examples of major discoveries and their returns to understand the scale of opportunity, then begin a 14-day free trial to position ahead of the next significant find.