June 15, 2026

When Energy Security Assumptions Collapse: Inside the 2026 Oil Supply Crisis

Energy markets operate on the assumption that supply buffers will hold. Commercial inventories exist precisely to absorb the kind of disruption that pipelines burst, weather events interrupt, or geopolitical tensions briefly elevate. For decades, this architecture functioned well enough that even analysts who worried about chokepoint vulnerability could point to stockpiles, alternative routing, and coordinated reserve mechanisms as credible backstops. The events of early 2026 have challenged every one of those assumptions simultaneously, and the IEA warns commercial oil inventories are depleting rapidly, placing the global energy system in terrain it has not navigated before.

When big ASX news breaks, our subscribers know first

The Architecture of an Inventory Shock

Understanding why this moment is structurally different from previous disruptions requires stepping back from the headline numbers and examining how oil inventory systems actually function. Commercial stocks are not passive accumulations of stored crude. They are working capital for the refining sector, operational buffers that allow refiners to maintain throughput independent of day-to-day fluctuations in tanker arrivals.

When traders and analysts refer to days of forward cover, they are describing the period over which a refinery, a country, or the global system can sustain current consumption rates without receiving a single additional barrel. Furthermore, understanding oil's global importance helps contextualise why these buffers are so critical to economic stability worldwide.

Normal operating conditions see commercial inventories maintained at roughly 60 to 90 days of forward cover globally, though this varies significantly by region and product type. The IEA's recent language, describing cover measured in weeks rather than months, signals that this operational buffer has been compressed to a point where any additional supply disruption, shipping delay, or demand spike has the potential to cause actual refinery run cuts rather than merely statistical inventory drawdowns.

What makes 2026 categorically different from prior disruptions is the combination of magnitude, speed, and seasonality. Previous shocks were large or fast or poorly timed, but rarely all three simultaneously.

The Strait of Hormuz and the Chokepoint Premium

Why No Alternative Route Fully Compensates

Approximately 20 to 21 percent of global seaborne oil trade transits the Strait of Hormuz under normal conditions. This single maritime corridor, roughly 33 kilometres wide at its narrowest navigable point, serves as the primary export gateway for Saudi Arabia, the UAE, Kuwait, Iraq, and Iran. When conflict disrupted transit beginning in late February 2026, the cascading effect through supply chains was not linear but exponential, because no credible short-term alternative routing exists at sufficient scale.

The East-West pipeline across Saudi Arabia and the Abu Dhabi Crude Oil Pipeline have combined export capacity of roughly 5 to 6 million barrels per day, a fraction of the 17 to 20 million barrels per day that typically moves through Hormuz under normal market conditions. This capacity gap is why even partial disruption translates into an immediate supply vacuum for Asian importers, who collectively account for the majority of Gulf crude purchases and have the fewest alternative supplier options.

The disruption that began following U.S. and Israeli military operations against Iran at the end of February 2026 did not merely slow tanker movements. It effectively closed the corridor for meaningful commercial transit, triggering what energy analysts classify as a structural supply loss rather than a short-cycle disruption. The distinction matters because short-cycle losses measured in days or weeks can be bridged by drawing on inventory buffers. Structural losses measured in months begin consuming the buffer itself, and that is precisely what the March and April data now confirm.

Record Drawdowns: Dissecting the March and April Data

Two Months That Rewrote the Record Books

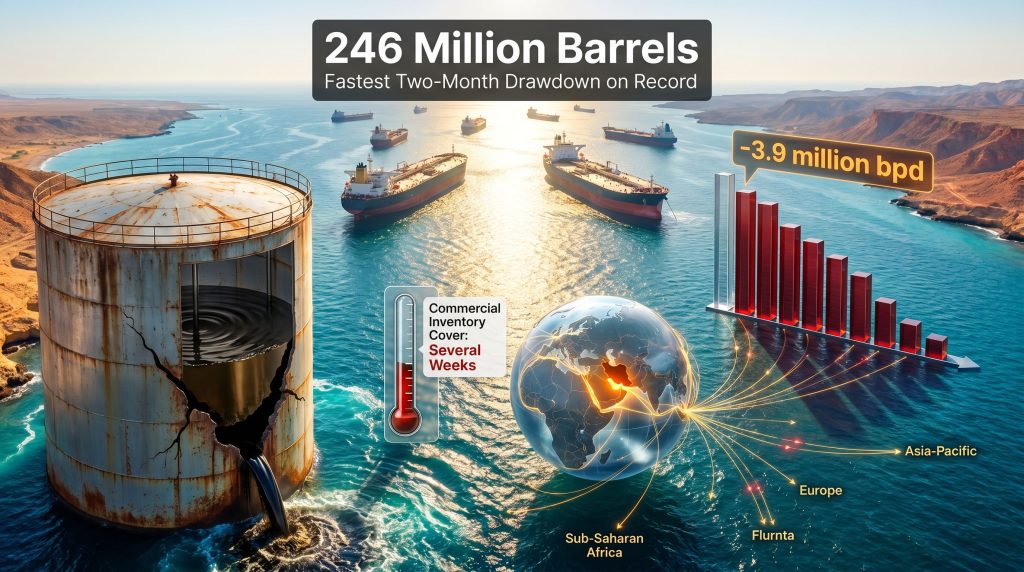

The IEA's monthly oil market report confirmed that global observed inventories fell by a combined 246 million barrels across March and April 2026, split roughly evenly between the two months. According to Bloomberg's coverage of the IEA findings, these drawdowns represent a historic pace of depletion driven directly by the Iran conflict shock.

| Metric | Figure |

|---|---|

| March 2026 inventory draw | ~129 million barrels |

| April 2026 inventory draw | ~117 million barrels |

| Combined March-April draw | ~246 million barrels |

| April supply decline | ~1.8 million barrels per day |

| Cumulative supply losses since February 2026 | ~12.8 million barrels per day |

| Production capacity currently offline | >14 million barrels per day |

| Share of global supply offline | ~15% |

| Cumulative Gulf producer supply losses | >1 billion barrels |

To appreciate the severity of these figures, consider that the most severe inventory draws during the 2020 COVID demand collapse were driven by demand destruction on a scale that had no modern precedent, yet those drawdowns occurred over a longer period and were partially offset by OPEC+ production cuts within weeks. The 2022 Russia-Ukraine disruption removed meaningful supply from European markets but did not simultaneously sever the primary export arteries of the world's most prolific producing region. The 2026 episode combines supply removal at the source with the closure of the exit corridor, removing the system's ability to self-correct through rerouting.

Key distinction for readers: The term observed inventories refers specifically to commercial stocks that are physically tracked and reported by member governments and industry bodies. This category does not include strategic petroleum reserves held by governments, oil in transit aboard tankers, or informal floating storage. When the IEA describes inventories as having only weeks of cover remaining, the reference is to this operationally critical commercial layer, not to all oil in existence.

The 400-Million-Barrel Response: Scale, Deployment, and the Replenishment Trap

The Largest Coordinated Reserve Release in History

The IEA coordinated a collective release from the strategic petroleum reserves of its 32 member nations beginning in March 2026, agreeing to withdraw a total of 400 million barrels from national strategic stockpiles. As of May 8, 2026, approximately 164 million barrels had been deployed into commercial markets, representing roughly 41 percent of the total commitment and adding approximately 2.5 million barrels per day to effective market supply during the drawdown period.

Placing this action in historical context illustrates why it is genuinely unprecedented:

| Event | Year | Volume Released | Duration |

|---|---|---|---|

| Gulf War supply disruption | 1991 | ~33.75 million barrels | Short-term |

| Hurricane Katrina aftermath | 2005 | ~60 million barrels | Weeks |

| Libya supply disruption | 2011 | 60 million barrels | One-time |

| Russia-Ukraine conflict response | 2022 | ~240 million barrels (phased) | Several months |

| Iran conflict / Hormuz closure | 2026 | 400 million barrels (committed) | Ongoing |

The 2026 commitment is nearly 67 percent larger than the 2022 response, which was itself the previous record. Yet despite this unprecedented deployment, the IEA has been explicit that these reserves are finite, and that the pace of commercial inventory depletion has not been fully arrested, merely slowed.

The Mechanics and Hidden Cost of SPR Deployment

Strategic petroleum reserves function as emergency bridges rather than structural supply solutions. Their deployment sequence works as follows:

- Member governments authorise withdrawals from nationally held strategic stockpiles

- Released oil enters commercial channels, either through direct sale or loan arrangements with refiners

- The additional supply temporarily suppresses spot prices and slows commercial inventory depletion

- Once the disruption resolves, governments must replenish reserves, purchasing oil at prevailing market prices

This final step contains what analysts sometimes call the replenishment trap. If the disruption is resolved while prices remain elevated, reserve repurchasing occurs at a significant cost premium relative to the prices at which reserves were originally built. If governments delay replenishment to avoid paying elevated prices, they leave the system exposed to the next shock with a diminished buffer. The IEA's own acknowledgment that these reserves are not endless is not rhetorical caution but a mathematically grounded operational warning.

Seasonal Demand as a Compounding Force

The supply shock has arrived at the worst possible moment in the annual demand cycle. The northern hemisphere's spring and summer seasons generate predictable consumption increases across multiple fuel categories, each of which is now competing for barrels from an already-depleted commercial inventory pool:

- Diesel: Spring agricultural planting across North America, Europe, and parts of Asia drives elevated demand from farm machinery and logistics networks servicing food supply chains

- Fertiliser feedstocks: Nitrogen-based fertilisers derived from oil and gas byproducts face tightening supply precisely when agricultural demand for soil nutrients peaks ahead of planting cycles

- Jet fuel: Summer travel season drives aviation fuel demand to annual highs across transatlantic and transpacific routes

- Gasoline: Road transport consumption peaks between June and August across major consuming regions

The convergence of structural supply loss with peak seasonal demand creates a compounding pressure dynamic. Neither factor alone would produce the current inventory trajectory. Together, they accelerate depletion at a rate that pushes the timeline for potential refinery run cuts uncomfortably close. In addition, the oil market impacts from broader geopolitical tensions have further complicated the demand outlook heading into the second half of 2026.

The next major ASX story will hit our subscribers first

The Physical-Financial Divergence: An Under-Appreciated Risk

Why Futures Prices Do Not Always Tell the Real Story

One of the analytically important observations communicated by IEA leadership at the G7 finance meeting in Paris concerns a divergence between what is happening in physical oil markets and what financial market pricing appears to reflect. This gap is not unusual in early-stage supply disruptions, but its persistence creates both analytical risk and potential for sharp price corrections.

Futures markets are fundamentally forward-looking instruments. They price expected supply and demand balances at specific future dates, incorporating assumptions about disruption duration, recovery timelines, and macro demand trajectories. When recession fears are prominent, algorithmic trading models may incorporate demand destruction assumptions that suppress futures prices even as physical spot markets tighten severely. The result is a structural lag between physical reality and financial market pricing.

For market participants: The most technically informative indicator of physical market stress is the shape of the futures curve, specifically the degree of backwardation, where prompt crude prices trade at a premium above deferred futures contracts. Deep backwardation signals that physical barrels available now are scarce relative to expected future supply, and that market participants are paying a premium for immediate delivery. When physical inventory data diverges sharply from financial pricing, historical precedent suggests a significant repricing event typically follows.

Supply Forecast Revision: The Magnitude of the Analytical Miss

How Dramatically the Outlook Has Shifted

The IEA's revised global supply projections for 2026 represent one of the most significant forecast reversals the agency has published in recent memory. Consequently, understanding current oil price trends has become essential for investors, policymakers, and industrial consumers trying to plan ahead.

| Forecast Category | Previous IEA Projection | Revised IEA Projection | Change |

|---|---|---|---|

| Annual global supply impact | -1.5 million bpd | -3.9 million bpd | -2.4 million bpd revision |

| Full-year supply balance | Surplus expected | Deficit projected | Full reversal |

| Inventory trajectory | Building through 2026 | Depleting at record pace | Complete inversion |

The revision from a 1.5 million bpd supply decline to 3.9 million bpd represents a 160 percent upward revision in projected supply loss magnitude. Against global consumption running at approximately 103 to 104 million barrels per day, a 3.9 million bpd structural shortfall represents roughly a 3.7 to 3.8 percent system-wide deficit, a figure large enough to drive sustained price escalation and, ultimately, demand destruction if not resolved.

Three Scenarios for Market Rebalancing

- Base case (disruption persists through Q3 2026): Commercial inventories remain under acute pressure, prices stay elevated, and refinery run cut risks intensify heading into autumn

- Optimistic case (partial transit resumption by mid-Q3): Gradual supply recovery begins, but inventory rebuilding requires 6 to 12 months; price relief is modest and delayed by the replenishment dynamic

- Adverse case (disruption extends into Q4 and beyond): Strategic reserves approach critically low operational levels, refinery throughput reductions become widespread, and demand destruction emerges as the market's self-correcting mechanism at significant economic cost

Downstream Vulnerability: Refiners Caught in the Crossfire

When crude availability tightens, refiners face a set of increasingly painful operational choices. Run cuts reduce throughput but preserve the refinery's crude supply position. Feedstock switching to alternative crude grades is possible in some cases but typically imposes yield penalties and processing cost increases. Drawing down refined product inventories buys time but accelerates the downstream tightening that eventually reaches consumers.

Regional exposure varies considerably:

| Region | Primary Exposure | Key Risk Factor |

|---|---|---|

| Asia-Pacific | High dependence on Middle East crude imports | Limited alternative supply routes |

| Europe | Moderate; diversified supply base | Elevated jet fuel and diesel demand |

| North America | Lower direct exposure | Indirect via global price benchmarks |

| Sub-Saharan Africa | High vulnerability | Limited SPR capacity; import-dependent |

| Middle East (non-Gulf) | Variable | Proximity to conflict zone |

Asia-Pacific importers, particularly Japan, South Korea, India, and China, are structurally most exposed given their heavy reliance on Gulf crude grades and their geographic distance from alternative Atlantic Basin suppliers. The cost premium for rerouting supply from West Africa or the North Sea to Asian refineries is significant and erodes refining margins even before feedstock scarcity is factored in.

Frequently Asked Questions

What are commercial oil inventories and why are they the critical metric right now?

Commercial inventories are the working stocks of crude oil and refined products held by private-sector entities, including refiners, traders, and fuel distributors. They are operationally distinct from government-held strategic reserves. Commercial stocks function as the immediate buffer between production flows and consumption demand. When the IEA warns commercial oil inventories are depleting rapidly, the concern is not that the world is running out of oil but that the operational cushion allowing refineries to maintain throughput through short-term supply gaps is approaching a critically thin level.

What happens when strategic petroleum reserves are depleted?

Reduced SPR levels diminish the energy system's capacity to absorb future shocks. They also create the replenishment obligation described above. In extreme scenarios, if reserves approach minimum operational levels, governments may be forced to choose between continuing drawdowns that leave them exposed to the next crisis or allowing prices to rise sharply by reducing release volumes. Neither outcome is straightforward. Furthermore, OPEC's market influence over production decisions adds an additional layer of complexity to any recovery scenario.

Could demand destruction become the rebalancing mechanism?

Demand destruction occurs when sustained high prices force consumers and industries to reduce consumption, reducing the supply deficit through reduced demand rather than recovered supply. It is an effective but economically painful rebalancing path. Industrial users reduce output, freight costs rise across global supply chains, and agricultural input costs escalate in ways that ultimately affect food prices. Demand destruction has historically preceded recessions when it occurs at scale and speed.

Structural Lessons From a System Under Stress

The 2026 oil supply shock has exposed a fundamental tension at the core of global energy architecture. Despite decades of discussion about supply diversification, the system remains acutely vulnerable to disruption at a small number of geographic chokepoints. The Strait of Hormuz is the most consequential single point of failure in the global energy supply chain, and the current crisis demonstrates that no combination of pipeline alternatives, strategic reserve mechanisms, and demand-side adjustments can fully compensate for its closure at short notice.

The episode also underscores the importance of distinguishing between the long-run energy transition narrative and the near-term physical reality. The intersection of oil and geopolitics has rarely been more consequential, with supply shocks of this magnitude carrying macroeconomic consequences that reach far beyond the energy sector. These consequences touch food production costs, freight economics, consumer purchasing power, and ultimately monetary policy as central banks navigate inflation pressures driven by energy input costs.

However, the IEA warns commercial oil inventories are depleting rapidly not merely as a short-term market signal but as a structural alert about the fragility of a system that has underinvested in resilience. The Euronews analysis of the IEA's findings confirms that renewed price swings remain a credible near-term risk as stocks continue to drain at record pace.

This article is based on publicly available information from IEA reports and Reuters news agency coverage. It contains forward-looking analysis and scenario projections that involve significant uncertainty. Readers should not interpret any section of this article as financial or investment advice. Market conditions can change rapidly, and all figures relating to inventory levels, supply forecasts, and reserve deployment are subject to revision as new data becomes available.

For ongoing coverage of global oil market developments and Middle East energy sector dynamics, Zawya's energy and commodities section at zawya.com tracks real-time developments across Gulf producer markets and international commodity flows.

Want to Capitalise on the Market Volatility Created by Historic Supply Shocks Like This One?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.