May 18, 2026

When Sanctions Meet Supply Shocks: The Architecture of U.S. Energy Statecraft

Few instruments in modern geopolitical strategy reveal the tension between principle and pragmatism as clearly as energy sanctions waivers. The decision by the Trump administration to allow General License 134B to lapse on May 16, 2026 — a move widely described as Trump allows Russian oil waiver to expire — has crystallised precisely this dynamic. When Washington constructs a sanctions regime around an adversary's primary revenue source and then carves out exceptions to protect allied economies, the resulting policy architecture becomes a study in competing priorities.

When big ASX news breaks, our subscribers know first

What General License 134B Actually Did, and Why It Mattered

Within the Office of Foreign Assets Control's enforcement framework, a general licence functions as a bounded permission structure rather than a suspension of sanctions. It does not dissolve restrictions but creates a time-limited corridor through which specific transaction types can proceed legally. General License 134B, issued by the Treasury Department, authorised transactions involving Russian seaborne oil cargoes that had already been loaded onto tankers before applicable sanctions deadlines took effect.

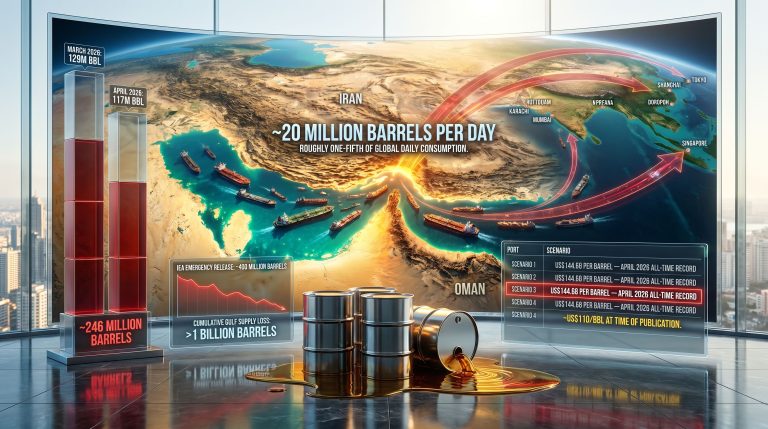

The practical effect was significant. Major Asian importers, most prominently India, were able to continue processing shipments of Russian crude already in transit, avoiding the abrupt supply disruptions that immediate full enforcement would have triggered. The waiver was first introduced in March 2026, extended in April, and ultimately allowed to expire without renewal on May 16.

The contextual backdrop matters here. At the time of the waiver's introduction, Brent crude had broken above $111 per barrel, driven by escalating instability around the Strait of Hormuz — one of the world's most strategically critical oil transit chokepoints through which roughly 20% of global oil supply passes. Against that backdrop, permitting the continued flow of already-loaded Russian cargoes was framed as a temporary market stabilisation measure rather than a political concession. Notably, the broader consequences of an oil price shock of this magnitude reverberate well beyond any single policy decision.

A general licence under OFAC's framework does not suspend sanctions permanently. It creates a time-limited corridor for specific transaction types, and its non-renewal carries equivalent policy weight to an active expansion of enforcement.

The Lifecycle of a Sanctions Waiver

| Phase | Action | Effective Period | Primary Beneficiaries |

|---|---|---|---|

| Initial Issuance | GL 134B introduced | March 2026 | India, Indonesia, Asian refiners |

| First Extension | Renewed by Treasury | April 2026 | Major Asian importers |

| Expiration | Non-renewal confirmed | May 16, 2026 | N/A, restrictions reimposed |

| Potential Next Phase | Narrower carve-out speculated | TBD | Select refiners including Indian sector |

The Political Calculus Behind Non-Renewal

The decision not to renew reflected a confluence of factors that made continued extension politically untenable, even if the underlying market logic for an extension remained compelling.

Bipartisan congressional pressure played a significant role. Democratic senators Jeanne Shaheen and Elizabeth Warren wrote to the administration on May 15 arguing that the waiver had generated no measurable reduction in fuel costs for American consumers while sustaining Russian oil revenues that flow directly into Moscow's wartime budget. Their position — that the policy was simultaneously ineffective domestically and harmful strategically — was difficult to rebut publicly.

Republican framing took a different but ultimately convergent path. Brian Mast, chairman of the House Foreign Affairs Committee, expressed support for maintaining sanctions pressure on Russia but drew attention to what he characterised as a structural design problem in U.S. sanctions architecture. His concern centred on the "harm asymmetry" challenge: sanctions must be calibrated to deliver greater damage to adversaries than to allied economies.

His argument was that European nations in particular had developed energy dependencies on Russia that made rapid decoupling economically severe, and that sanctions policy needed to account for this asymmetry rather than ignore it. Furthermore, the evolving nature of Russian oil sanctions has consistently complicated enforcement efforts across multiple administrations.

Treasury Secretary Scott Bessent had also made prior public commitments to non-renewal that functioned as credibility anchors. Walking those commitments back would have carried its own political costs, particularly with U.S. gasoline prices elevated and midterm elections on the horizon.

India's Exposure and the Asian Importer Dilemma

No economy faced more direct consequences from the waiver's expiration than India. During the sanctions period, India emerged as one of the largest buyers of Russian seaborne crude, with import volumes reaching record highs in the weeks preceding the May 16 deadline as refiners front-loaded purchases ahead of anticipated enforcement tightening.

India's government engaged in active diplomatic lobbying for an extension, with energy security expected to feature prominently on the agenda of U.S. Secretary of State Marco Rubio's upcoming visit to New Delhi. India's refiners, including major operators such as Reliance Industries, have been assessed by analysts as having sufficient supply chain flexibility to absorb short-term disruption through diversification toward Middle Eastern OPEC+ volumes, African crude blends, and expanded U.S. export flows.

However, the cost premium associated with replacing discounted Russian barrels with market-rate alternatives is non-trivial, particularly for a country simultaneously grappling with wholesale inflation already at a 3.5-year high and fuel cost increases of approximately 25%. These Asian energy pressures are compounding an already challenging regional economic environment.

Indonesia and other energy-dependent Asian economies faced analogous pressures, with strategic petroleum reserve levels declining across the region. The collective diplomatic weight of Asian importers was considered substantial enough that sanctions specialists assessed a high probability of either a further temporary extension or a narrower carve-out benefiting select refiners within weeks of the formal expiration.

Alternative Supply Corridors Under Evaluation

- Increased OPEC+ allocation from Gulf producers, particularly Saudi Arabia and the UAE

- African crude blends including Bonny Light and Angolan grades

- Expanded U.S. crude export volumes facilitated by elevated domestic production

- Australian and Canadian supply relationships as longer-term diversification options

The Strategic Whiplash Problem

Sanctions specialists monitoring U.S. policy toward Russia have identified a recurring pattern that fundamentally undermines the deterrent logic of the sanctions architecture. Treasury has repeatedly adopted assertive public stances on enforcement only to soften restrictions once energy-market pressures intensify sufficiently.

This oscillation — described by Brett Erickson of Obsidian Risk Advisors as a structural collision between geopolitical ethics and market crisis — creates what amounts to a predictable relief valve that sophisticated market participants, including Russian export planners, can factor into their strategic calculations.

Erickson characterised the dilemma facing Washington as a choice between two strategically uncomfortable outcomes: either continuing to allow Russian oil revenues to flow by maintaining relief mechanisms, or cutting off one of the remaining major energy pressure valves for Asian economies during one of the most severe supply disruption episodes in recent history. Neither option aligns cleanly with stated U.S. foreign policy objectives.

Sanctions analysts have noted that Treasury has historically adopted hard public lines on Russia only to soften restrictions once energy-market pressures intensify — a pattern that raises fundamental questions about the long-term credibility of the current enforcement posture.

The probability matrix for what follows the expiration reflects this structural ambiguity.

| Scenario | Trigger Conditions | Probability Assessment | Market Impact |

|---|---|---|---|

| Full reimposition maintained | Geopolitical pressure holds; oil prices stabilise | Moderate | Upward pressure on Asian crude premiums |

| Narrower carve-out issued | Asian diplomatic pressure intensifies; supply crunch deepens | High per analyst consensus | Limited price relief for select importers |

| Full waiver restoration | Severe global energy shortage materialises | Low to moderate | Significant downward pressure on crude benchmarks |

| Escalated enforcement | Ukraine diplomatic progress; political window opens | Low | Meaningful reduction in Russian export revenues |

Moscow's Unintended Windfall: The Price Paradox

One of the more analytically striking dimensions of this policy episode is the degree to which the same geopolitical crisis used to justify the waiver has simultaneously enriched the sanctioned party. Higher global crude benchmarks driven by Hormuz instability translate directly into elevated Russian export revenues, regardless of what happens to the volume of Russian barrels reaching Asian refiners.

Russia's oil revenues increased by approximately $6.3 billion as elevated prices more than offset any production-level constraints imposed by sanctions enforcement. This revenue multiplication effect creates a structural paradox at the heart of current sanctions strategy: tightening restrictions on Russian barrels may reduce volume marginally, but the supply squeeze itself drives up the price of remaining Russian exports, partially compensating Moscow for reduced throughput.

Russia has also been actively expanding the logistical infrastructure that enables it to route oil outside Western-supervised transaction pathways. According to reporting from the Washington Examiner, four additional vessels were added to Russia's Arctic LNG carrier fleet, extending the so-called "dark fleet" network that operates beyond conventional maritime insurance and banking channels.

Malaysia flagged a significant increase in ship-to-ship transfer activity linked to Iranian crude logistics, with parallel evasion patterns observed in Russian seaborne crude operations. These developments suggest that even sustained enforcement pressure faces a growing counter-infrastructure designed to reduce its practical effect.

The next major ASX story will hit our subscribers first

Ukraine's Position and the Revenue Arithmetic of War

Kyiv has consistently maintained that sanctions dilution — even temporary and ostensibly market-driven dilution — carries real military consequences. Vladyslav Vlasiuk, a senior adviser to President Volodymyr Zelenskyy, has argued that stronger and more consistent sanctions enforcement accelerates the conditions necessary for meaningful peace negotiations, while any relief mechanism effectively subsidises continued Russian military capacity.

Ukraine's position on the waiver rested on a specific empirical challenge: whether Russian crude export volumes are actually significant enough to materially offset supply disruptions originating from Hormuz instability. The argument was that the supply-shock justification for the waiver may have overstated Russia's role as an indispensable swing supplier.

The Deeper Credibility Problem for U.S. Sanctions Architecture

Beyond the immediate market and diplomatic implications, the fact that Trump allows Russian oil waiver to expire raises a structural vulnerability in how sanctions regimes are designed and maintained. When temporary exemptions become predictable features of enforcement rather than genuine exceptions, three compounding effects emerge.

First, the deterrent value of the broader regime erodes. Adversaries and third-party importers alike calibrate their behaviour based on the expectation of eventual relief, reducing the front-end deterrent pressure that sanctions are designed to generate.

Second, allied cohesion weakens. European officials privately expressed frustration that inconsistent U.S. enforcement complicated coalition management, with some members questioning whether the sanctions framework was being applied with sufficient seriousness to justify the economic costs of their own compliance.

Third, and most consequentially over the long run, repeated waiver cycles incentivise the development of durable evasion infrastructure. The expanded dark fleet, the growth of ship-to-ship transfer networks, and the deepening of non-Western payment and insurance corridors are not temporary adaptations. They represent permanent additions to the global energy system's capacity to route supply around Western-supervised channels.

In addition, OPEC's market influence remains a critical variable in how effectively any enforcement gap can be filled by alternative suppliers. Furthermore, the broader context of US-China trade impacts continues to shape how Asian economies weigh energy security decisions against geopolitical alignment pressures.

FAQ: Trump's Russian Oil Waiver Expiry Explained

What Was General License 134B?

It was a Treasury Department authorisation permitting transactions involving Russian seaborne oil cargoes already loaded before applicable sanctions deadlines. First issued in March 2026, extended in April, and allowed to expire on May 16, 2026.

Why Did the Trump Administration Not Renew It?

Non-renewal reflected bipartisan congressional pressure, prior public commitments from Treasury Secretary Scott Bessent, and criticism that the waiver delivered no measurable fuel price relief for U.S. consumers while sustaining Russian oil export revenues.

Which Countries Are Most Affected?

India is the most directly exposed major importer given its record-high Russian crude purchase volumes during the waiver period. Indonesia and other Asian importers face supply and cost adjustments. European economies with residual Russian energy dependency face secondary pricing effects.

Will There Be Another Waiver or Carve-Out?

Sanctions analysts consider a further temporary extension or narrower carve-out to be a realistic near-term possibility, particularly for major Indian refiners, if global energy supply conditions deteriorate further. As reported by au.investing.com, the expiration occurs against a backdrop of significant crude price pressures that make future policy adjustments difficult to rule out entirely.

How Does This Affect Oil Prices?

Tighter restrictions on Russian seaborne crude reduce one available supply channel for Asian importers, adding upward pressure to benchmarks already elevated by Hormuz instability. The net price effect depends on whether OPEC+ volumes, U.S. exports, and African blends can absorb the displacement.

What Is Ukraine's Position?

Ukraine has consistently opposed any sanctions dilution, arguing that consistent enforcement accelerates peace negotiation conditions and that even temporary waivers generate billions in additional wartime revenue for Moscow. The case that Trump allows Russian oil waiver to expire represents a meaningful policy shift remains, however, a matter of ongoing analytical debate.

This article is intended for informational purposes only and does not constitute financial or investment advice. All references to price levels, revenue figures, and policy timelines reflect publicly available reporting as of the date of publication. Readers should conduct independent research before making any decisions based on the information presented here.

Want to Stay Ahead of the Next Major Resource Opportunity Emerging From Global Energy Disruptions?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable investment insights — explore how historic discoveries have generated extraordinary returns and begin a 14-day free trial at Discovery Alert to position yourself ahead of the broader market.