June 21, 2026

When Supply Chains Break: The Anatomy of a Commodity Shock

Global commodity markets rarely experience true supply shocks. Most price dislocations are demand-driven, cyclical, or the product of gradual structural shifts. Genuine supply disruptions — the kind that simultaneously cut feedstock access, damage production infrastructure, and block export corridors — are uncommon enough that markets are often poorly positioned to absorb them when they arrive.

The aluminum supply shock in the Middle East, triggered by conflict escalation in the Gulf region, is a case study in precisely this kind of multi-vector disruption. It has simultaneously threatened the feedstock pipeline into Gulf smelters, damaged production facilities directly, and blocked the maritime corridor through which both raw materials arrive and finished metal departs. Understanding why prices have not yet reached the catastrophic levels initially feared requires looking well beyond headline production data, into the hidden mechanics of supply chain improvisation, regulatory ambiguity, and shadow inventory dynamics that rarely surface in mainstream financial coverage.

When big ASX news breaks, our subscribers know first

The Gulf's Structural Role in a 76-Million-Tonne Market

To appreciate the significance of what has unfolded, it helps to understand the Gulf's position in global aluminum supply chains before the conflict began. The Middle East accounts for approximately 7 million tonnes of annual aluminum smelting capacity, representing roughly 9 to 10% of total global supply in a market that produces around 76 million tonnes per year.

Gulf producers have historically operated at the competitive frontier of global aluminum economics. Their structural advantages include access to subsidised natural gas, low-cost energy infrastructure, and strategic proximity to alumina import routes originating from Australia and West Africa. These factors have made Gulf smelters among the most cost-efficient operations worldwide, enabling them to compete globally even as Chinese capacity has expanded dramatically. Furthermore, global aluminium producers have long viewed Gulf capacity as a critical stabilising force within the broader supply ecosystem.

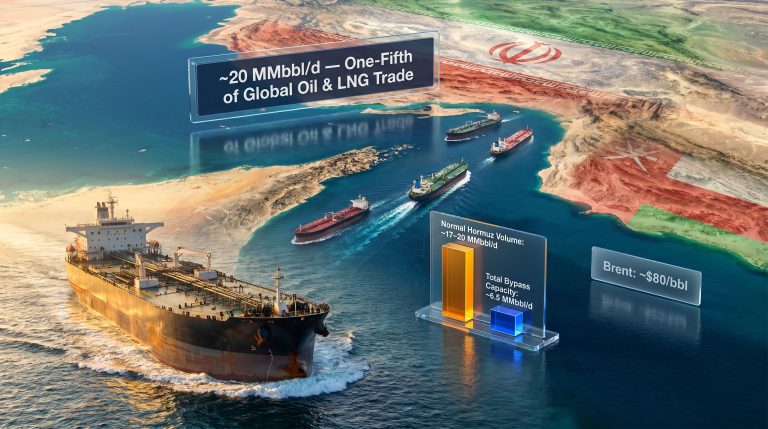

The region's vulnerability, however, lies in a structural irony: the same maritime corridor that enables Gulf smelters to import alumina and export finished metal is the Strait of Hormuz, one of the world's most geopolitically sensitive waterways. Both raw material inflows and product outflows depend on this single chokepoint, creating a dual exposure that no amount of operational efficiency can fully hedge.

For Western buyers in the U.S. and Europe who have built meaningful import dependencies on Gulf aluminum, this creates an asymmetric risk profile. Unlike Asian buyers with faster access to Chinese and Indonesian alternative supply, Western importers face longer lead times and fewer near-term sourcing options when Gulf exports are disrupted. The metal pricing dynamics that emerge from this imbalance have significant knock-on effects across downstream industries.

How the Disruption Unfolded: Infrastructure Strikes and Feedstock Starvation

The aluminum supply shock in the Middle East did not arrive as a single event. It developed through a compounding sequence of disruptions that analysts struggled to model in real time.

Phase One: Maritime Closure and Feedstock Starvation

The initial phase involved the closure of the Strait of Hormuz to normal commercial traffic, cutting the primary feedstock supply route for Gulf smelters. The bauxite supply chain underpins this entire process — alumina, the refined intermediate product derived from bauxite, is not produced locally in sufficient quantities within the Gulf. Smelters are therefore structurally dependent on alumina imports, primarily from Australia, making maritime route closures an existential operational threat rather than a temporary inconvenience.

Early analyst warnings were stark: without rapid restoration of alumina supply routes, Gulf smelters could exhaust their raw material stockpiles within weeks. This assessment drove the initial price surge, with LME aluminum futures reaching a range of $3,450 to $3,672 per tonne during peak escalation — levels not seen since the commodity disruptions of recent years.

Phase Two: Direct Infrastructure Strikes

The second phase involved direct missile strikes on Gulf aluminum production infrastructure. This escalation crystallised a broad institutional consensus that aluminum would rank among the most severely affected commodity markets outside of oil and gas, prompting trading house Mercuria's metals division to characterise the situation as a black swan supply event with a potential deficit of at least 2 million tonnes by year-end if disruptions persisted.

Dark Transits and the Clandestine Alumina Supply Chain

What happened next is one of the more operationally remarkable stories in recent commodity market history. Rather than accepting widespread smelter closures as inevitable, Gulf producers engineered a series of unconventional logistics solutions that partially restored their feedstock security.

The most operationally audacious of these involved vessels conducting what maritime analysts describe as dark transits through the Strait of Hormuz. By disabling their AIS (Automatic Identification System) tracking signals, a small number of ships moved alumina cargoes through the strait without broadcasting their positions. This tactic, which mirrors methods used to keep oil flowing through contested maritime zones during geopolitical crises, maintained a critical trickle of raw material supply into the Gulf even while the strait remained formally closed to normal commercial shipping.

Ship-tracking analysis from firms monitoring vessel movements documented this activity, noting that while the volumes involved were limited, they represented a meaningful contribution to smelter feedstock security. The economics are straightforward: keeping even a single large aluminum smelter operational generates revenues that dwarf the logistical costs of an irregular maritime operation.

Larger volumes arrived through an entirely different route. Alumina cargoes were offloaded at Omani ports, which sit outside the effective closure zone, and then transported overland via truck convoys to Gulf smelting facilities. This land-bridge solution converted what had been a purely maritime supply chain into a hybrid road-and-sea operation, testing regional logistics infrastructure at a scale rarely seen outside wartime resupply operations.

Ben Ayre, an analyst at ship-tracking firm Kpler, noted that the solutions emerging from this crisis were operationally exceptional, reflecting the high economic value that smelter operators placed on maintaining production continuity. Consequently, vessel-tracking data showed that alumina imports into the Persian Gulf returned to pre-war levels in May — a data point that significantly revised the market's worst-case supply loss estimates.

The Shadow Inventory Dimension: The Market's Hidden Buffer

Beyond the logistics improvisation, the global market impact of the aluminum supply shock in the Middle East has been substantially absorbed by a mechanism that receives far less attention in mainstream analysis: the drawdown of privately held, off-exchange aluminum inventories.

Unlike LME-registered warehouse stocks, which are publicly visible and closely monitored by traders and analysts, shadow inventories are held by producers, traders, fabricators, and industrial consumers outside formal exchange systems. Their total volume is unknown, they are not reported to any central authority, and their drawdown is visible only indirectly through physical market tightness signals.

Greg Shearer, JPMorgan's head of base and precious metals research, has described client conversations that consistently confirm physical tightness in the market, while identifying privately held stocks as the primary source of supply relief to date. His analytical framework points toward a sequential process: shadow stocks are drawn first, then exchange-visible inventories come under pressure, and it is the second phase that drives the most significant price discovery.

This sequence explains a counterintuitive feature of the current market: LME warrant cancellations, particularly concentrated in Port Klang, Malaysia, indicate that traders are actively pulling deliverable metal from exchange-registered stocks. This behaviour tightens the pool of metal available for LME settlement independently of total global production volumes, creating physical premium pressure even when headline supply data appears more benign.

The critical distinction for market analysts is not total global production, which remains substantial, but the much smaller pool of deliverable metal accessible through established trade routes and exchange-registered warehouses. These are structurally different quantities, and conflating them leads to systematic underestimation of physical market tightness.

China's Regulatory Ceiling and the Enforcement Gamble

Before the Gulf conflict began, a structural narrative was already forming in China's aluminum sector that had significant implications for global supply. The broader China industrial demand backdrop provides essential context here. Domestic smelters were approaching a regulatory production cap of 45 million tonnes per annum, a policy ceiling designed to bring a decades-long era of chronic oversupply to an end and restore pricing discipline to global aluminum markets.

Since the conflict began, official Chinese production statistics have shown smelters running at an annualised rate of approximately 47 million tonnes, comfortably above the regulatory limit. April data confirmed this overshoot, and Chinese exports simultaneously surged as global buyers sought to replace disrupted Gulf supply with available Asian alternatives.

Is Chinese Overcapacity Sustainable?

The analytical challenge this creates is substantial. Chinese smelters operating above their designed power intake levels face genuine engineering constraints. One industry veteran characterised the process as analogous to balancing an elephant on a finger: technically achievable in the short term but structurally unsustainable. Power systems not designed for sustained overload degrade, and the cumulative risk of equipment failure rises with every week of overcapacity operation.

The more consequential uncertainty is regulatory rather than technical. Whether Beijing will enforce the 45-million-tonne cap or allow continued overproduction to capitalise on elevated global prices represents one of the most consequential binary variables in current aluminum market modelling. Strict enforcement would meaningfully tighten global supply; continued non-enforcement provides an ongoing buffer that suppresses price discovery toward the upside.

The next major ASX story will hit our subscribers first

Indonesia: The Wildcard That Could Rewrite the Supply Equation

A third geography has entered the analytical frame in ways that most institutional models have not yet formally incorporated. Indonesia's emerging role as a significant aluminum exporter has sharpened market focus on its capacity expansion trajectory, particularly in the context of an energy reallocation dynamic that could accelerate new supply additions.

Indonesia's aluminum expansion has historically been constrained by power availability rather than resource access or capital. The country's energy grid has limited the pace at which new smelting capacity can be commissioned and ramped. This bottleneck has kept Indonesian aluminum supply additions on a predictable, relatively conservative timeline.

The disruption to this trajectory comes from an unexpected direction: the compressed economics of nickel smelting. Indonesian nickel operations have faced significant margin pressure, while elevated aluminum premiums driven by the Gulf supply shock have made aluminum smelting comparatively more attractive. The result is a growing financial incentive for Indonesian energy operators to redirect scarce electricity toward aluminum plants at the expense of nickel facilities.

Amy Gower, head of metals and mining strategy at Morgan Stanley, has flagged this dynamic as a model-changing risk. The core insight is that power reallocation from nickel to aluminum could allow Indonesian supply additions to arrive materially faster than previously projected — a scenario that has not yet been reflected in most consensus forecasts. In addition, the aluminum and steel tariffs currently shaping trade flows add yet another layer of complexity to how Indonesian supply might be routed and absorbed globally.

Institutional Price Forecasts: A Market Deeply Divided

The range of institutional price forecasts and supply balance assessments currently circulating in the aluminum market is unusually wide, reflecting genuine analytical uncertainty rather than normal forecasting variance. As ING's structural deficit analysis highlights, the combination of supply disruption and demand resilience creates conditions that are genuinely difficult to model with precision.

| Institution | Price Forecast | Supply Balance View |

|---|---|---|

| Goldman Sachs | ~$3,000/tonne (12-month) | Supply recovery; bearish trajectory |

| JPMorgan Chase | $4,000/tonne (delayed, not abandoned) | Significant deficits remain; bullish medium-term |

| Citigroup | Not specified | Largest supply shock in 50+ years |

| Bank of America | Not specified | Market broadly balanced on 76Mt basis |

| Bank of China International | Neutral/stabilising | Operational buffers now depleted |

| BMO Capital Markets | Peak deficit likely passed | Bearish near-term; recovery underway |

Three structural uncertainties are driving this divergence:

-

Gulf smelter loss opacity: Middle Eastern producers have not publicly disclosed the full scale of output reductions, and the clandestine nature of their supply chain workarounds makes independent verification extremely difficult.

-

Chinese regulatory ambiguity: The 45-million-tonne cap creates a near-binary enforcement scenario with materially different supply balance implications depending on Beijing's policy posture.

-

Shadow inventory depth: The total volume of privately held aluminum stocks globally is structurally unknowable, making it impossible to model precisely when exchange-visible inventory drawdowns will begin in earnest.

Amelia Xiao Fu, head of commodities strategy at Bank of China International, has noted that while the market survived the acute phase of the crisis by drawing down operational inventories, those buffers have now been substantially reduced. The implication is that the market's margin of safety has shrunk, even if the immediate crisis has been averted.

Three Scenarios: Where Aluminum Prices Go From Here

The current market sits at an inflection point where three plausible forward scenarios carry meaningfully different price implications.

| Scenario | Key Conditions | Price Trajectory |

|---|---|---|

| Bull: Deficit Squeeze | Shadow stocks exhausted; China enforces cap; Indonesia delayed | $4,000+/tonne |

| Base: Gradual Recovery | Gulf supply slowly normalises; China partially complies; Indonesia on schedule | $3,200 to $3,500/tonne |

| Bear: Supply Surplus | China overproduces; Indonesia accelerates; Gulf recovers faster than expected | $2,800 to $3,000/tonne |

The bull case, which JPMorgan continues to maintain as delayed rather than abandoned, requires the sequential exhaustion of shadow inventories to drive exchange stock drawdowns that force physical buyers into spot markets at elevated premiums. JPMorgan's Shearer has characterised the current period as a deferral of the deficit-driven price move, not its cancellation.

The bear case rests on a combination of Chinese regulatory non-enforcement, accelerated Indonesian capacity additions, and faster-than-expected Gulf smelter recovery. Goldman Sachs' $3,000/tonne twelve-month forecast reflects this scenario, with the return of Persian Gulf alumina imports to pre-war levels in May cited as evidence that feedstock security has been substantially restored.

Helen Amos, head of commodities research at BMO Capital Markets, has articulated the bear case with notable directness, arguing that the inventory squeeze that bulls predicted would force a final price surge has been slow enough in developing that the market may have already passed the point of maximum deficit stress.

What Investors and Industrial Buyers Should Monitor

For those tracking the aluminum supply shock in the Middle East and its forward implications, several indicators carry disproportionate signal value:

-

LME warrant cancellations in Port Klang and other major delivery points: Rising cancellations signal active depletion of exchange-deliverable stocks — the mechanism that drives the transition from shadow inventory drawdown to visible market tightness.

-

Chinese export data: Monthly export volumes from Chinese smelters will indicate whether the overproduction response is sustained, accelerating, or beginning to normalise as engineering constraints or regulatory pressure intensify.

-

Indonesian power allocation announcements: Any formal reallocation of grid capacity from nickel to aluminum smelting in Indonesia would represent a concrete signal that the Morgan Stanley scenario is materialising.

-

Gulf smelter production disclosures: Even partial transparency on actual output losses from Middle Eastern producers would significantly narrow the range of credible supply balance estimates and reduce analytical uncertainty.

-

Physical market premiums in the U.S. and Europe: As the buyers furthest from alternative Asian supply sources, Western physical premiums will be an early indicator of whether deliverable metal availability is genuinely tightening.

Disclaimer: This article contains forward-looking statements, price forecasts, and institutional projections that reflect analyst opinions as of the time of writing. Commodity markets are subject to rapid change, and none of the price scenarios or supply balance assessments presented here should be interpreted as investment advice. Readers should conduct independent research and consult qualified financial advisors before making investment decisions.

Want to Stay Ahead of the Next Major Commodity Disruption?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including those tied to aluminium, bauxite, and other commodities at the centre of global supply chain shifts — so subscribers can identify actionable opportunities before the broader market reacts. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.