August 6, 2026

The Anatomy of a Chokepoint: Why the Strait of Hormuz Cannot Simply Be Switched Off

Every few years, the global energy system receives a stark reminder of just how concentrated its vulnerabilities really are. A single corridor of water, barely 21 nautical miles wide at its narrowest navigable point, sits between the Persian Gulf and the Gulf of Oman. Through this corridor flows roughly one-fifth of all oil and liquefied natural gas traded on earth. When Iran declared the Strait of Hormuz closed in June 2026, energy traders, shipowners, and governments held their breath. Then the tankers kept moving.

Understanding why oil continues flowing through the Strait of Hormuz despite Iran's closure claim requires more than a geopolitical headline. It demands a granular look at how maritime chokepoints actually function, what the difference between a declared closure and a physical blockade really means, and why the gap between rhetoric and operational reality at Hormuz is a recurring feature of Middle Eastern energy geopolitics rather than a new phenomenon.

When big ASX news breaks, our subscribers know first

What the Strait of Hormuz Actually Controls

The Strait of Hormuz is not simply an important shipping lane. It is the singular arterial outlet for the majority of Persian Gulf hydrocarbon production. Saudi Arabia, the UAE, Kuwait, Iraq, and Iran itself all depend on Hormuz access to reach export markets. There is no geographically or logistically equivalent alternative.

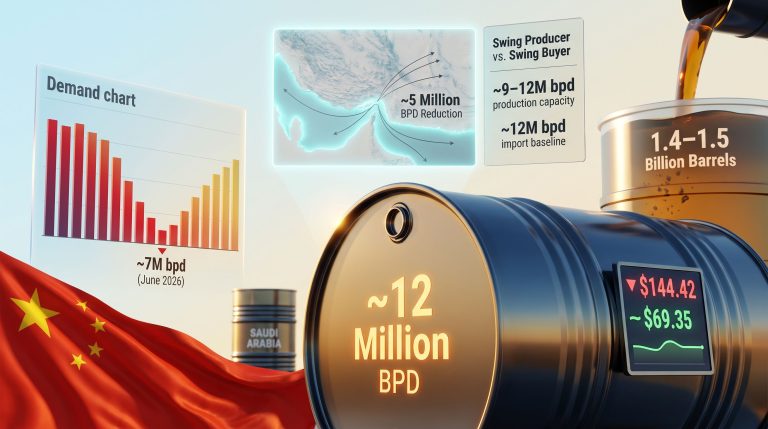

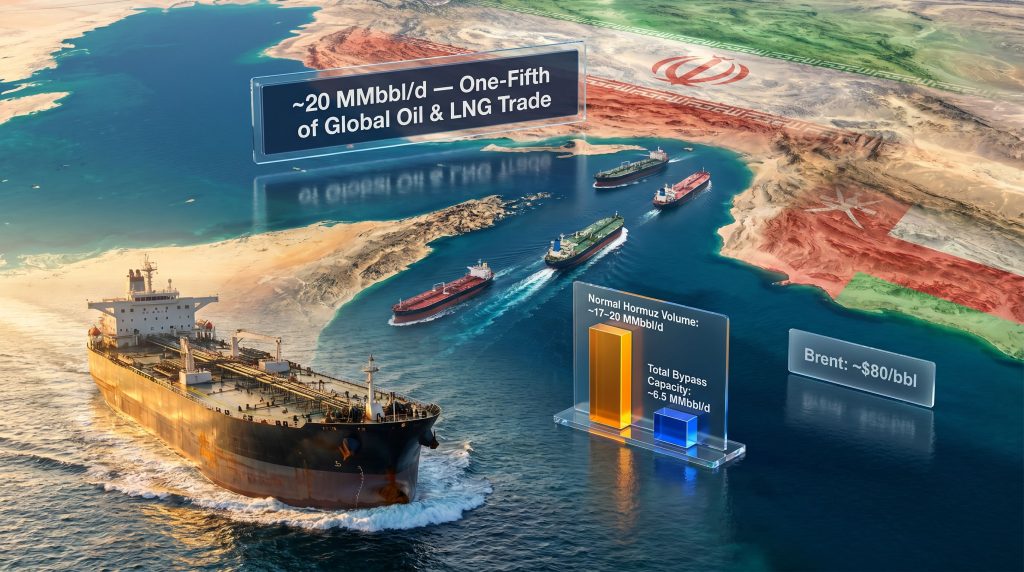

According to the U.S. Energy Information Administration (EIA), approximately 20 million barrels per day (MMbbl/d) transited the strait during 2024, a figure that encompasses crude oil, refined petroleum products, and liquefied natural gas. The LNG component is particularly significant: Qatar, one of the world's largest LNG exporters, routes virtually all of its output through Hormuz. This makes the strait a critical node for European and Asian gas supply chains, and understanding global LNG supply dynamics is essential to appreciating the full scale of exposure.

The commodity breakdown of normal Hormuz transit volumes illustrates the breadth of exposure:

| Commodity | Estimated Daily Volume | Share of Global Trade |

|---|---|---|

| Crude Oil | ~17 MMbbl/d | ~17% of global supply |

| LNG | Significant Qatari volumes | ~20% of global LNG trade |

| Refined Products | Secondary but material | Regional distribution hub |

This multi-commodity dependency is one reason why closure threats carry such weight in energy markets. A sustained disruption would not simply affect crude oil prices. It would simultaneously compress global LNG availability, spike freight rates, and trigger emergency drawdowns of strategic petroleum reserves across the U.S., IEA member nations, and major Asian consumer economies including Japan, South Korea, and China.

Declared Closed Versus Physically Blocked: A Critical Distinction

One of the most important and least widely understood dynamics in Hormuz crisis episodes is the difference between a sovereign declaration of closure and the physical capacity to enforce it. These are fundamentally different conditions, and conflating them leads to systematically distorted risk assessments.

A formal closure declaration carries legal and diplomatic implications. It signals Iran's intent to restrict access and can trigger war risk insurance adjustments, rerouting decisions, and diplomatic responses. However, it does not automatically stop ships from moving.

Enforcing a complete physical blockade of Hormuz would require Iran to intercept, deter, or destroy vessels across both the Omani-adjacent and Iranian-adjacent transit corridors simultaneously. Iran's naval capacity, including its Islamic Revolutionary Guard Corps Navy (IRGCN) and conventional naval forces, is substantial in asymmetric contexts. However, it has historically operated through harassment, seizure of individual vessels, and threat posturing rather than the kind of sustained force projection required for a full chokepoint blockade.

When a closure is declared but not fully enforced, according to Tufts University analysis, three operational scenarios typically emerge:

- Full physical blockade — complete cessation of all vessel movement; historically rare, unsustained, and requiring significant escalation of military force.

- Selective restriction — passage permitted for specific flag states, cargo types, or vessels that have obtained prior Iranian authorisation, creating a two-tier transit environment.

- Harassment and deterrence — naval presence and warning communications that slow vessel movements, inflate insurance costs, and push some operators to reroute without achieving a complete halt of flows.

The June 2026 episode appears to reflect the third scenario shading toward the second. Vessel-tracking data based on satellite-derived Automatic Identification System (AIS) signals confirmed that multiple laden supertankers carrying Saudi Arabian and UAE crude continued transiting Hormuz on June 21 and 22, 2026, even as Iranian state media reported the waterway as closed. U.S. Central Command subsequently confirmed that more than 17 MMbbl of crude oil moved through the strait during that weekend period alone.

The persistence of tanker traffic does not indicate that the strait is operating normally. It indicates the closure is contested, partial, or selectively enforced rather than absolute. That distinction carries enormous implications for how both markets and policymakers should interpret Iranian statements.

The Geopolitical Architecture Behind the June 2026 Closure

Iran's stated justification for its renewed June 2026 closure was the alleged violation of a ceasefire agreement in southern Lebanon. This framing is strategically significant in ways that go beyond the immediate crisis. It demonstrates Iran's established doctrine of using Hormuz as a multi-theater geopolitical instrument, capable of linking Persian Gulf energy infrastructure to conflict dynamics occurring thousands of kilometres away in the eastern Mediterranean.

This is not a new tactic. Iran has invoked Hormuz closure threats during nuclear negotiations, sanctions escalation cycles, and regional conflict flashpoints over several decades. The broader geopolitical risk landscape affecting commodities consistently demonstrates that such straits function less as conventional military targets and more as negotiating levers within a state's broader strategic toolkit.

The June 2026 episode introduced a compounding complication. Earlier in the month, Washington and Tehran had reached an interim agreement to reopen Hormuz trade routes following approximately four months of disruption that had elevated freight rates and driven significant rerouting activity across global tanker markets. The interim deal briefly generated optimism: Brent crude retreated from elevated levels as supply continuity expectations improved.

Within days, however, Iran announced that vessels would require Iranian authorisation to transit the strait, a condition that sits in tension with established principles of international maritime law governing passage rights. This was followed by the renewed closure declaration, creating a rapidly shifting framework of uncertainty for shipowners, charterers, and energy traders. The timeline captures the volatility of the period:

| Date | Event | Market/Operational Impact |

|---|---|---|

| Early June 2026 | ~4 months of Hormuz disruption continuing | Elevated freight rates; active rerouting |

| ~June 14, 2026 | U.S.-Iran interim deal to reopen Hormuz | Brent crude retreats; sentiment improves |

| ~June 20, 2026 | Iran announces renewed closure citing Lebanon ceasefire violations | Fresh uncertainty; tanker operators on high alert |

| June 21–22, 2026 | AIS data and CENTCOM confirm 17+ MMbbl transited | Market reprices from worst-case scenario |

| Late June 2026 | U.S.-Iran negotiations scheduled in Switzerland | Traders monitor for durable framework signals |

How Energy Markets Price a Partial Closure

Brent crude settled near $80 per barrel on Friday, June 20, 2026, after pulling back earlier in the week when the interim U.S.-Iran agreement had temporarily improved supply outlook sentiment. That price level reflects something more analytically nuanced than a simple open/closed market verdict on Hormuz. It reflects a probability-weighted assessment of multiple scenarios running simultaneously.

Furthermore, energy traders have become increasingly sophisticated at distinguishing between headline geopolitical risk and operational supply risk. The availability of real-time AIS vessel-tracking data has been transformative in this regard. In earlier decades, a closure declaration from Tehran would have triggered sharp immediate price spikes because market participants had no independent means of verifying whether tankers were actually moving.

Today, satellite-derived AIS data provides near-real-time confirmation of vessel positions, heading, speed, and cargo status, compressing the information asymmetry that once made Hormuz threats far more market-moving. Consequently, oil price movements in similar episodes have increasingly reflected this more granular, data-driven market assessment rather than headline-driven panic.

This phenomenon can be described as a credibility discount in energy market pricing. Repeated instances where declared closures were not fully enforced have reduced the immediate shock response to new declarations, with markets instead applying probabilistic frameworks that weight:

- Observed tanker traffic as a supply continuity signal.

- The degree of military escalation visible from satellite and open-source intelligence.

- The state of diplomatic negotiations and the proximity of potential resolution frameworks.

- Iran's own economic incentives, since Iranian oil exports also transit Hormuz, creating a structural self-limiting constraint on any prolonged full closure.

Traders are simultaneously tracking two parallel indicators: continued tanker movement as a near-term supply confirmation signal, and the outcome of upcoming U.S.-Iran talks in Switzerland as the key determinant of medium-term framework durability.

The shipping industry's response reflects this calibrated approach. War risk insurance premiums for Hormuz-transiting vessels have been adjusted upward, reflecting genuine operational uncertainty. Yet major charterers have not fully abandoned the route. The continued entry of empty tankers into the Persian Gulf in preparation for future cargo loadings is a particularly telling indicator. Operators willing to position vessels for future loadings are implicitly betting that the route will remain commercially viable in the near term.

The Bypass Arithmetic That Exposes Global Vulnerability

Perhaps the most sobering dimension of the Hormuz situation is the stark mathematics of bypass capacity relative to normal throughput volumes. Two major pipeline systems exist that can route Persian Gulf crude to export terminals bypassing the strait entirely:

| Bypass Route | Operator | Capacity (MMbbl/d) | Destination Port |

|---|---|---|---|

| ADCOP Pipeline | ADNOC | ~1.5 | Fujairah, UAE |

| Petroline (East-West) | Saudi Aramco | ~5.0 | Yanbu, Saudi Arabia |

| Total Bypass Capacity | — | ~6.5 | — |

| Normal Hormuz Volume | — | ~17–20 | — |

The arithmetic is unambiguous. Combined pipeline bypass capacity of approximately 6.5 MMbbl/d covers less than 40% of normal Hormuz throughput. A genuine full closure would leave an unbridgeable near-term shortfall of approximately 10 to 13 MMbbl/d, a volume that no combination of strategic petroleum reserve releases, demand destruction, and alternative routing could offset quickly.

Strategic petroleum reserves maintained by the U.S., IEA member nations, and major Asian consumer economies represent a short-term buffer. However, SPR releases are typically designed to cover weeks to months of disruption, not structural supply gaps of this magnitude. No new pipeline infrastructure capable of replacing Hormuz at scale has been developed, and no such project could realistically be constructed within any policy-relevant timeframe.

This structural reality is precisely why energy markets treat Hormuz differently from virtually every other geopolitical risk variable. It is not that a full closure is highly probable. It is that the consequences of a full closure would be categorically different from any other supply disruption scenario in the modern energy era.

The next major ASX story will hit our subscribers first

Decoding Iran's Signalling and the Switzerland Negotiations

Is Iran Using Hormuz as a Negotiating Lever?

Reading Iran's Hormuz declarations as pure operational military announcements misses their primary function. Across decades of historical precedent, these declarations have most often served as renegotiation signals rather than terminal breakdown indicators. The pattern is consistent: Iran escalates through a Hormuz declaration at a moment of maximum diplomatic leverage, creating pressure for concessions in parallel negotiations, then manages the physical enforcement question separately.

The June 2026 sequence fits this pattern with notable precision. The renewal of the closure declaration came immediately after an interim deal had been struck, suggesting the intent was to inject leverage into the next phase of negotiations rather than to permanently halt flows. The Conversation's analysis of shadow tankers further illustrates how Iran's own economic dependency on Hormuz transit reinforces this reading — sustained full enforcement would damage Iranian oil export revenue at a time when sanctions pressure is already significant.

The upcoming U.S.-Iran negotiations in Switzerland represent the most consequential near-term variable for the trajectory of this situation. Several structural issues require resolution for any framework to achieve durability:

- The vessel authorisation requirement Iran has asserted, and whether an internationally acceptable mechanism for managing this can be agreed upon.

- Ceasefire monitoring mechanisms linked to the Lebanon conflict that Iran has explicitly connected to its Hormuz posture.

- Sanctions relief sequencing and the conditions under which Iranian oil exports would be permitted to operate without restriction.

Oman has historically served as a back-channel facilitator between Iran and Western parties in sensitive negotiations, a role it has played discreetly across multiple diplomatic cycles. Third-party facilitation of this kind has often been a prerequisite for meaningful progress on Hormuz-adjacent issues, suggesting Muscat's involvement in any durable resolution framework would be a positive indicator.

Frequently Asked Questions: Strait of Hormuz and Iran's Closure Claim

Is oil still flowing through the Strait of Hormuz right now?

Yes. Despite Iran's formal closure declaration, AIS vessel-tracking data confirmed that multiple laden supertankers continued transiting the strait as of June 21 and 22, 2026. U.S. Central Command reported that over 17 MMbbl of crude moved through Hormuz during that weekend, confirming that the closure has not been fully enforced.

How much oil normally passes through the Strait of Hormuz?

The EIA estimates that approximately 20 MMbbl/d transited the Strait of Hormuz in 2024, representing roughly one-fifth of combined global oil and LNG trade.

Why can't the world simply reroute around the Strait of Hormuz?

Existing pipeline bypass infrastructure provides a combined capacity of only approximately 6.5 MMbbl/d, far below the 17 to 20 MMbbl/d that normally flows through the strait. No near-term infrastructure solution can bridge this gap at scale.

What is Iran's stated reason for the June 2026 closure?

Iran cited alleged violations of a ceasefire agreement in southern Lebanon as justification, linking Persian Gulf shipping access to a separate regional conflict dynamic in the eastern Mediterranean.

What does Brent crude near $80/bbl tell us about market confidence?

It reflects a market pricing continued, if uncertain, supply flows rather than a worst-case full disruption. The persistence of tanker traffic and scheduled Switzerland negotiations are both moderating extreme price responses. In addition, crude oil market dynamics suggest traders are increasingly calibrated to distinguish between declaratory risk and operational supply risk.

What happens to LNG if Hormuz is fully closed?

LNG carriers transporting Qatari exports would face the same disruption risk as crude tankers. Given Qatar's position as one of the world's largest LNG exporters, a sustained closure would carry major supply implications for European and Asian gas markets. This dimension of Hormuz risk is often underweighted in crude-focused analysis.

Key Takeaways

- Oil continues flowing through the Strait of Hormuz despite Iran's closure claim because the declared closure has not been translated into full physical enforcement — a distinction that matters enormously for both markets and policy analysis.

- Real-time AIS vessel-tracking technology now provides an independent verification layer that reduces the information asymmetry that once made Hormuz declarations automatically more market-moving.

- The 17 MMbbl confirmed transiting over the June 21–22 weekend demonstrates operational continuity even under declared closure conditions.

- Combined pipeline bypass capacity of ~6.5 MMbbl/d covers less than 40% of normal Hormuz throughput, meaning a genuine full closure would represent a systemic global energy shock without historical precedent in the modern era.

- Iran's self-limiting economic dependency on Hormuz transit, combined with the historical pattern of closure declarations functioning as negotiating levers, supports the interpretation that the current episode is a renegotiation signal rather than a terminal disruption event.

- Commodity market volatility of this nature underscores the need for robust risk frameworks, as the Switzerland negotiations remain the critical near-term variable requiring resolution of vessel authorisation disputes, ceasefire monitoring linkages, and sanctions sequencing simultaneously.

This article is provided for informational purposes only and does not constitute financial or investment advice. Energy market forecasts and geopolitical assessments involve significant uncertainty. Readers should consult independent professional advice before making investment or commercial decisions based on the information presented here.

Want to Stay Ahead of the Next Major Commodity Discovery?

While geopolitical disruptions like the Strait of Hormuz closure send shockwaves through global energy markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex commodity data into actionable insights for investors at every level — explore historic discoveries and their exceptional returns, then begin your 14-day free trial to position yourself ahead of the broader market.