June 22, 2026

When Mining Giants Reshape Their Portfolios, the Whole Industry Shifts

The global mining industry operates in long, grinding cycles where strategic decisions made today ripple through commodity markets for decades. When a top-tier diversified miner decides to exit an entire commodity class, the consequences extend far beyond a single balance sheet adjustment. Asset ownership changes hands, supply chain relationships are renegotiated, and an entirely new class of operators steps in to fill the void left by institutional sellers who have decided the future lies elsewhere.

This dynamic is precisely what is unfolding with the Anglo American Australian coal mines sale, a transaction that has become one of the most closely watched mining M&A events of 2026. The deal is not simply about moving an asset from one owner to another. It represents the culmination of a multi-year corporate transformation, a dramatic legal dispute, and a fundamental question about who will own the world's most strategically important steelmaking coal assets in the decade ahead.

When big ASX news breaks, our subscribers know first

What Makes the Bowen Basin So Strategically Significant?

Before examining the transaction itself, it is worth understanding why these particular assets attracted such intense buyer interest despite a challenging coal price environment. Queensland's Bowen Basin is not merely a prolific coal-producing region. It is the world's single most important source of premium hard coking coal, the specific grade of metallurgical coal that blast furnace steelmakers depend upon for efficient iron ore reduction.

The chemistry matters enormously here. Premium hard coking coal is distinguished by several technical characteristics that lower-grade alternatives cannot replicate:

- Caking strength, measured by the Coke Strength after Reaction (CSR) index, which determines how well coal holds its structure inside a blast furnace under extreme heat and pressure

- Volatile matter content, typically between 18% and 26% for premium grades, which governs combustion efficiency during the coking process

- Ash content, ideally below 10%, which reduces the burden on the furnace and improves steel quality

- Sulfur content, which must remain extremely low to prevent brittleness in finished steel products

The Moranbah North and Grosvenor mines produce coal that consistently meets or exceeds these benchmarks, which explains why steelmakers across Japan, South Korea, India, and Taiwan pay substantial premiums for Bowen Basin product. Furthermore, this is not a commodity that can simply be substituted with material from other regions when supply tightens. Shifts in iron ore markets and broader steel supply chains only reinforce the strategic weight these assets carry.

"The chemical irreplaceability of premium hard coking coal in blast furnace operations creates a form of demand inelasticity that insulates Bowen Basin producers from competition in ways that thermal coal producers never enjoyed."

Why Anglo American Is Exiting Australian Coal

The Copper Pivot and the Logic of Portfolio Concentration

Anglo American's decision to divest its Australian steelmaking coal operations reflects a strategic assessment that has been building for several years. The company's leadership concluded that the energy transition would reward miners concentrated in copper, the metal most critical to electrification infrastructure, over those maintaining diversified exposure to industrial commodities with uncertain long-term demand trajectories.

The planned merger with Canada's Teck Resources accelerates this logic considerably. The combined entity is being designed specifically as a copper-focused mining heavyweight, and maintaining significant steelmaking coal exposure within that portfolio would create both narrative confusion for investors and genuine capital allocation friction. Copper-focused institutional investors and ESG-conscious funds require a clean portfolio story, and steelmaking coal, despite its operational cash flow potential, complicates that story substantially.

Anglo American's official press release confirmed that CEO Duncan Wanblad framed this transaction as completing the company's full exit from steelmaking coal, describing it as the final step in a deliberate repositioning rather than a reactive response to market conditions.

The ESG Pressure That Rarely Gets Discussed Openly

While the strategic copper narrative dominates the official communications around this transaction, a less frequently examined factor is the role of ESG-driven capital constraints in accelerating the coal exit timeline. Steelmaking coal operations at the Bowen Basin assets were estimated to represent a disproportionate share of Anglo American's total Scope 1 and 2 emissions profile, creating pressure from institutional shareholders who face their own portfolio decarbonisation commitments.

This dynamic creates a structural mispricing opportunity that sophisticated buyers like Dhilmar can exploit. When sellers are motivated by factors beyond pure economics, specifically investor relations management and index inclusion requirements, assets can trade at discounts that reflect the seller's urgency rather than the asset's intrinsic cash flow value.

How the Peabody Deal Collapsed and What It Revealed

The Sequence of Events

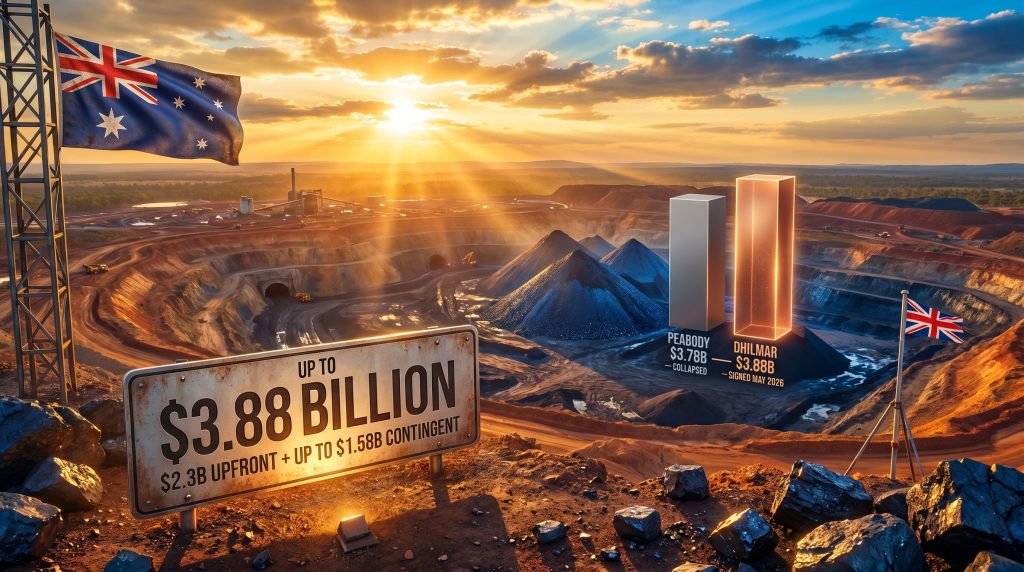

The Anglo American Australian coal mines sale did not arrive at Dhilmar cleanly. It passed through a turbulent prior transaction that exposed significant vulnerabilities in large-scale mining M&A deal structures. Tracking the Anglo coal sale status through its various stages reveals just how dramatically the process evolved.

| Deal Stage | Counterparty | Agreed Value | Outcome |

|---|---|---|---|

| Original agreement | Peabody Energy | $3.78 billion (fixed) | Collapsed after mine fire |

| New transaction | Dhilmar (UK-based) | Up to $3.88 billion | Signed May 18, 2026 |

| Legal recovery | Peabody Energy | Damages TBD | Arbitration ongoing |

The sequence unfolded as follows: Anglo American signed a $3.78 billion fixed-price agreement with Peabody Energy for the Australian coal assets. A fire incident subsequently occurred at the Moranbah North mine. Peabody characterised this event as a material adverse change, a defined legal threshold within the acquisition agreement that, if validly triggered, would entitle the buyer to exit the transaction without penalty. Anglo American disputed this characterisation and refused to accept the deal's unilateral termination. Arbitration proceedings were formally initiated by Anglo American against Peabody and remain ongoing.

For broader context on how that agreement unravelled, the Peabody coal acquisition process and its breakdown offer valuable insight into the risks embedded in fixed-price mining M&A structures.

What Material Adverse Change Clauses Actually Mean in Mining M&A

The Peabody dispute introduced broader industry attention to how MAC clauses function in mining acquisition contracts, a topic that rarely receives detailed public examination.

In most large-scale mining transactions, a material adverse change clause defines specific categories of events that would fundamentally alter the value proposition of the asset being acquired. These clauses are heavily negotiated, with sellers seeking narrow definitions and buyers seeking broad ones. The key interpretive question is whether an event is genuinely material, meaning it permanently impairs the asset's value, or merely temporal, representing a recoverable disruption.

A mine fire of limited duration would typically be characterised by sellers as a recoverable event, while buyers facing softening commodity prices simultaneously have incentive to interpret the same incident as meeting the MAC threshold. The Moranbah North situation appears to have involved precisely this interpretive conflict, complicated by the fact that metallurgical coal prices declined materially between the signing of the Peabody agreement and the moment the fire occurred, giving the buyer additional motivation to seek an exit. Reporting from the AFR at the time of Peabody's withdrawal highlights just how rapidly market sentiment shifted during this period.

"The Peabody collapse serves as a cautionary example for the entire resources M&A sector: fixed-price deal structures in volatile commodity markets create substantial execution risk that neither party fully controls once market conditions shift after signing."

Who Is Dhilmar and Why Does Their Emergence Matter?

Profile of the New Owner

Dhilmar is a privately held mining group headquartered in the United Kingdom. Its emergence as the buyer of one of the world's most significant metallurgical coal portfolios represents a broader trend that has been quietly reshaping global mining asset ownership over the past several years.

The company's existing flagship asset is the Eleonore gold mine in Canada, acquired from Newmont Corporation. This acquisition profile reveals a deliberate strategy: Dhilmar identifies high-quality operational assets being divested by major listed miners during their own portfolio restructuring cycles, then acquires them at valuations that reflect the seller's strategic motivation to exit rather than the asset's full cash flow potential.

Dhilmar's CEO, Alexander Ramlie, brings operational experience from the Indonesian mining sector, including prior roles connected to PT Amman Mineral Internasional, an Indonesian gold and copper producer. This background suggests familiarity with managing complex, capital-intensive mining operations in challenging environments, which is directly relevant to the operational demands of underground longwall coal mining in the Bowen Basin.

Why Private Capital Is Winning These Auctions

Dhilmar's success in securing this transaction over other reported interested parties reflects a structural advantage that private mining groups increasingly enjoy over listed competitors. Several factors are at play:

- No ESG disclosure obligations that would create investor relations complications from acquiring coal assets

- Patient capital that does not require quarterly earnings guidance management or analyst consensus alignment

- Operational focus rather than portfolio narrative management that occupies significant management bandwidth at listed majors

- Flexibility to accept contingent payment structures without the complex accounting treatment challenges these present for publicly listed acquirers

Other parties reportedly evaluating the assets included Stanmore Resources, Mitsubishi Corporation, and BUMA Internasional, reflecting the breadth of strategic interest in Bowen Basin metallurgical coal despite the ESG headwinds affecting listed buyer appetite.

Decoding the $3.88 Billion Deal Structure

Why the Contingent Payment Mechanism Is Significant

The architecture of the Dhilmar transaction is as informative as the headline number. The $3.88 billion total consideration comprises two distinct components:

- $2.3 billion in upfront cash payable at completion

- Up to $1.58 billion in contingent payments linked to future metallurgical coal price performance

This structure reflects the reality that metallurgical coal prices at the time of the Dhilmar agreement were materially lower than when the original Peabody deal was negotiated. Rather than bridging the valuation gap through a fixed price adjustment, the parties agreed to share future price risk through the contingent component, allowing Anglo American to maintain potential upside exposure while giving Dhilmar price protection in a challenged near-term market.

For Anglo American, this structure accomplishes several objectives simultaneously. It secures immediate balance sheet improvement through the $2.3 billion cash component, maintains a credible total transaction value that compares favourably against the failed Peabody deal, and retains participation in any coal price recovery driven by renewed infrastructure spending or steel demand acceleration in emerging markets. Consequently, for Dhilmar, the contingent structure reduces the real acquisition cost in weak market conditions while accepting higher effective costs if markets recover.

The next major ASX story will hit our subscribers first

The Teck Resources Merger Connection

Why Debt Reduction Is the Critical Path Variable

The proceeds from the Anglo American Australian coal mines sale are earmarked primarily for debt reduction, a destination that is directly connected to the requirements for completing the Teck Resources merger. Creating a copper-focused mining heavyweight through a merger of this scale requires both parties to arrive at the transaction with balanced balance sheets and clear capital allocation capacity.

The upfront $2.3 billion cash component immediately improves Anglo American's leverage ratios, while the contingent $1.58 billion provides additional potential debt reduction capacity as coal markets evolve. This debt reduction enables more favourable financing terms for the merged entity and removes the operational distraction of managing a coal business during the complex integration process that major mergers require.

What the Merged Anglo-Teck Entity Would Look Like

The copper-focused identity of the planned merged company represents a calculated bet on long-term demand driven by electrification, renewable energy infrastructure buildout, and electric vehicle production scaling. Copper's supply deficit projections over the next decade, combined with the long lead times required to bring new copper mines into production, create a structural case for premium valuations for copper-concentrated producers.

By completing its steelmaking coal exit before finalising the Teck merger, Anglo American ensures the combined entity can present institutional investors with a coherent portfolio narrative centred entirely on transition-relevant metals. This is especially important given the complications that a significant coal position would create for ESG-focused fund inclusion or sustainability-linked financing arrangements. In addition, trends in China steel demand and evolving green steel pricing dynamics further reinforce why listed majors are accelerating their exits from traditional steelmaking coal exposure.

Risks That Remain on Both Sides of This Transaction

Operational Challenges at Moranbah North

The Moranbah North mine, which was at the centre of the Peabody MAC dispute, presents ongoing operational considerations for Dhilmar as the new owner. Underground longwall coal mining in the Bowen Basin carries inherent geological and safety risks that have historically affected production continuity across multiple operators in the region. The Bowen Basin's coal seams are characterised by elevated methane content and complex geological structures that require continuous monitoring and adaptive operational management.

Dhilmar's ability to realise the full value of the contingent payment components depends substantially on demonstrating credible production recovery and operational stability at Moranbah North. Any further disruptions to output would not only affect revenue generation but could also reduce the coal price-linked contingent consideration payable to Anglo American, creating an unusual alignment of interests between the buyer and seller around operational performance during the post-completion period.

The Arbitration Wildcard

The ongoing arbitration proceedings between Anglo American and Peabody Energy introduce financial uncertainty that remains unresolved independent of the Dhilmar transaction. Anglo American is seeking damages for the failed transaction, and the outcome of this process could deliver meaningful additional capital recovery.

Beyond the direct financial implications, this arbitration will likely establish interpretive precedents that influence how MAC clauses are drafted and contested in future large-scale mining transactions, particularly regarding the treatment of operational incidents occurring during the interim period between signing and closing.

Commodity Price Scenarios

The contingent payment structure creates a direct link between Dhilmar's total acquisition cost and future metallurgical coal markets. The key price scenarios and their implications are:

| Scenario | Coal Price Trajectory | Contingent Payment Outcome | Anglo Total Proceeds |

|---|---|---|---|

| Bear case | Continued decline from current levels | Minimal or zero trigger | ~$2.3 billion |

| Base case | Gradual recovery toward historical averages | Partial trigger | ~$2.9-3.3 billion |

| Bull case | Strong recovery driven by Asian infrastructure demand | Full trigger | ~$3.88 billion |

The range of outcomes is substantial, and investors in Anglo American should model all three scenarios rather than relying on the headline $3.88 billion figure as a guaranteed outcome.

What This Deal Signals for the Global Mining M&A Landscape

The Anglo American Australian coal mines sale is structurally significant beyond its immediate financial parameters. It establishes several precedents and reinforces several trends that will shape mining M&A activity through the remainder of this decade:

- Contingent payment structures are becoming the preferred mechanism for bridging valuation gaps in volatile commodity markets, replacing fixed-price negotiations that create binary outcomes

- Private capital is increasingly competitive in acquiring assets that listed majors are compelled to divest, exploiting the valuation discount created by seller ESG obligations

- Mine safety events are now capable of derailing multi-billion-dollar transactions, elevating operational risk management as a formal component of pre-signing due diligence for future buyers

- The copper concentration trend among major miners is accelerating portfolio simplification across the industry, creating a pipeline of high-quality divested assets across multiple commodity categories

- Specialist operators with deep commodity knowledge and patient capital structures are better positioned than generalist miners to extract value from these divested assets

"The broader message from this transaction is that the energy transition is not just reshaping what metals get mined. It is reshaping who owns the mines that produce the metals the world still fundamentally needs."

Metallurgical coal will remain indispensable to global steel production for at least the next two decades, given the capital intensity and timeline required to transition blast furnace capacity to green hydrogen-based alternatives. The question is not whether these Bowen Basin assets will generate substantial cash flows under Dhilmar's ownership. The question is whether the full contingent consideration will be realised, and whether the arbitration against Peabody delivers the additional recovery Anglo American is seeking.

This article contains analysis of publicly reported information regarding the Anglo American Australian coal mines sale. Figures relating to contingent payments, commodity price projections, and merger outcomes involve inherent uncertainty and should not be interpreted as forecasts or investment advice. Readers should conduct independent research before making investment decisions related to any companies or assets discussed herein.

Want to Stay Ahead of the Next Major ASX Mining Discovery?

While major miners like Anglo American reshape their portfolios around copper and transition metals, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly alerting subscribers to significant mineral discoveries across 30-plus commodities before the broader market reacts — explore historic discovery returns on Discovery Alert's discoveries page and begin a 14-day free trial to secure a genuine market-leading edge.