August 6, 2026

The Rough Diamond Market's Structural Fault Line: Why Supply Alone Can No Longer Save Natural Stone Prices

The natural rough diamond market is not simply experiencing a cyclical downturn. It is undergoing a fundamental restructuring driven by the convergence of three long-term forces: the maturation of laboratory-grown diamond (LGD) manufacturing at commercial scale, a sustained demand correction in key consumer markets following the post-pandemic jewellery boom, and a decade-long expansion in rough diamond supply from newer African producers. Understanding how these forces interact is essential context for assessing what Angola rough diamond production cuts actually mean for the global industry.

The under-one-carat polished segment sits at the epicentre of this crisis. LGD penetration in this category now exceeds 80% in certain consumer segments, according to industry tracking data, effectively commoditising the natural small rough market. When a product category loses its scarcity premium, supply management becomes both more urgent and less effective as a standalone remedy.

When big ASX news breaks, our subscribers know first

Angola's Production Paradox: Record Growth Into a Contracting Market

Angola presents one of the more paradoxical narratives in global mining. Between 2022 and 2025, the country executed one of the most significant production ramp-ups in the diamond industry's recent history, while simultaneously entering the period of the deepest rough price compression since the 2008 financial crisis. For context on how this fits into broader patterns, the global mining landscape reveals just how competitive the race for resource dominance has become.

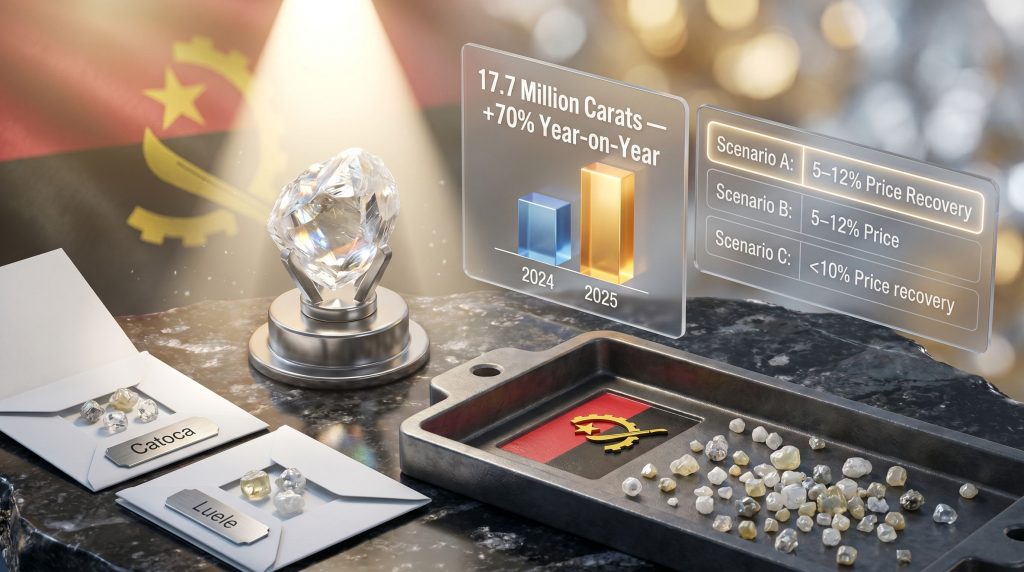

The numbers are striking. Angola's rough diamond production grows with exports reaching 17.7 million carats in 2025, representing a 70% year-on-year increase, while total production climbed to 15.2 million carats. The government's medium-term target of 17 million carats by 2027 signals that this growth trajectory was never intended to slow. The primary engine behind this expansion is the Luele mine, one of the largest kimberlite discoveries made anywhere in the world in recent decades, which commenced commercial operations in 2023.

Yet the very characteristics that make Luele geologically significant also create a commercial vulnerability. The mine's production profile is weighted toward smaller-size rough categories. Combined with the continued output of the Catoca mine, Angola's longest-operating large-scale kimberlite operation, the country's aggregate carat growth has occurred almost entirely in the size grades facing the most acute LGD-driven price erosion.

The result has been a revenue paradox: Angola's carat volumes surged, but average per-carat realisations declined as the production mix shifted increasingly toward goods that the downstream market was simultaneously de-pricing. This is not a subtle dynamic. It is a structural mismatch between geological output and market appetite that Endiama's leadership has now chosen to address directly.

Understanding Kimberlite Size Distributions and Why They Matter

For readers less familiar with mining economics explained, understanding the significance of rough diamond size classifications is essential. Kimberlite pipes, the volcanic rock formations that host the majority of the world's gem diamonds, produce a distribution of diamond crystal sizes that varies by geological formation. Mines producing a higher proportion of large stones, such as Lesotho's Liqhobong or some of Botswana's Jwaneng pipe material, generate disproportionately higher revenue per tonne processed.

Conversely, operations like Catoca and portions of Luele that produce predominantly smaller goods, typically stones that will yield polished diamonds under one carat, face an inherently lower value-per-carat ceiling even in healthy market conditions. In the current environment, where LGDs have compressed small polished prices to levels approaching manufacturing cost, that ceiling has dropped further still.

- Rough diamonds are typically sorted into sieve sizes measured in mesh grades, with smaller mesh numbers indicating larger stones

- Goods yielding polished diamonds under 0.30 carats are the most heavily LGD-substituted category

- The 1-carat polished threshold has historically represented a significant natural diamond price premium, a premium that remains more intact than in smaller categories

- Angola's Luele pipe geology, while extraordinary in volume terms, does not produce the concentration of large, high-value crystals seen at mines like Botswana's Jwaneng

This geological reality explains why Endiama's supply restriction is targeted specifically at smaller-size rough. Furthermore, the intervention is not arbitrary — it reflects a precise diagnosis of where Angola's production mix is most commercially exposed.

Endiama's Supply Restriction: Mechanism, Scope, and Market Ambiguity

Angola's state diamond company, Endiama, announced at the JCK Las Vegas industry meetings that it would reduce supply of small diamonds released from both Catoca and Luele operations. The initial restriction window spans three months, with the possibility of extension depending on price recovery in the downstream market.

The commercial rationale was articulated clearly by Endiama's Commercial Director, Elton Escrivão, whose position emphasised that the measure is designed to protect the value of Angolan production and support broader market stability. This framing is significant: it represents a deliberate pivot from volume-maximisation as the primary performance metric toward a value-per-carat philosophy that prioritises price realisation over tonnage.

What remains publicly unclear, however, is the precise mechanism Endiama will employ. Three pathways exist, each with materially different implications for the market:

| Mechanism | Description | Price Support Durability | Revenue Impact |

|---|---|---|---|

| Genuine mining volume reduction | Lower extraction rates at Catoca and Luele | High, structural | Immediate revenue sacrifice |

| Deferred sales and stockpiling | Mining continues, inventory withheld | Moderate, temporary | Revenue delayed, not lost |

| Size-category realignment | Small goods redirected to blending or industrial use | Low to moderate | Mixed, depends on alternative realisation |

The distinction between a genuine production cut and deferred sales is one of the most underappreciated nuances in rough diamond supply management. Stockpiling creates a future supply overhang that can reverse any price recovery the moment inventory is released, particularly if downstream demand has not sufficiently recovered in the interim. Genuine volume reduction, by contrast, removes carats from the system permanently and provides a more durable floor under prices.

Endiama has committed to releasing further operational details in coming weeks. Market participants, particularly the large cutting and polishing centres in Surat, Antwerp, and Dubai, are watching closely. The midstream pipeline, which purchases rough diamonds and transforms them into polished goods, has faced severe margin compression throughout the current cycle and will consequently be the most immediate beneficiary of any meaningful supply relief.

How Angola Compares to Other Major Diamond Producers

Angola's decision to implement Angola rough diamond production cuts takes on additional significance when viewed against the production strategies of the world's other major producers. Indeed, the largest global mines illustrate just how sharply production strategies can diverge across nations.

| Producer Nation | 2024-2025 Production Trend | Supply Strategy | Primary Market Pressure |

|---|---|---|---|

| Angola | Expanding, record 15.2M carats (2025) | Targeted small-rough restriction | LGD competition, price erosion |

| Botswana | Constrained and declining | Output reduction, sales deferral | Demand weakness, De Beers restructuring |

| Russia (ALROSA) | Under significant pressure | Sanctioned, limited Western market access | Geopolitical trade restrictions |

| Canada | Declining | Operational constraints | Mine depletion at Diavik and Ekati |

| Namibia | Stable to modest growth | Marine mining expansion | Logistical and geological boundaries |

Angola now occupies a structurally unique position in this landscape. It is simultaneously the industry's most rapidly expanding major producer and the country now voluntarily applying supply discipline. No other current diamond producer has attempted this combination, making Angola's intervention genuinely novel from a market management perspective.

The closest historical analogy is the OPEC swing producer dynamic, where the largest volume grower accepts a disproportionate share of the supply restriction burden to protect collective price levels. The long-term sustainability of this posture depends on whether other producers reciprocate with equivalent discipline or simply allow Angola to absorb the revenue sacrifice alone.

Botswana and Angola have reportedly been engaged in discussions regarding their respective interests in the De Beers ownership structure. If these two nations align commercially, their combined share of global rough diamond production would give any coordinated supply strategy meaningful market weight. This potential alignment deserves considerably more attention than it has received in mainstream industry commentary.

Three Scenarios for Global Rough Diamond Prices

Angola's supply intervention creates a branching set of potential outcomes for the global rough diamond market. The following scenario framework outlines the most likely trajectories and the conditions that would drive each.

Scenario A: Restriction Holds and Prices Stabilise

If Endiama maintains the small-rough volume reduction for the full three-month period and extends it conditionally, the under-one-carat polished segment could recover meaningfully. Other producers under comparable inventory pressure would likely follow Angola's lead, creating a de facto coordinated supply response without requiring formal coordination agreements. Price recovery estimates for this scenario range from 5% to 12% in the small polished category, which would materially improve cutting and polishing margins in Surat particularly.

Scenario B: Restriction Reverses After the Initial Period

If downstream prices do not recover sufficiently within three months, Endiama faces a difficult commercial choice. Extending the restriction deepens short-term revenue sacrifice for the Angolan government, which is simultaneously targeting diamond sector growth as a fiscal objective. Releasing withheld inventory into a market that has not yet absorbed existing supply could amplify rather than correct the oversupply condition, creating a worse outcome than no intervention at all.

Scenario C: LGD Competition Renders Supply Cuts Structurally Insufficient

This scenario represents the most consequential long-term risk. If laboratory-grown diamond penetration in the sub-one-carat segment continues accelerating, no level of natural rough supply restriction can restore price levels in that category. The market bifurcates permanently, with natural diamonds commanding premiums only at larger carat weights and in specific provenance-driven segments. In this scenario, Angola's optimal strategy shifts from supply restriction toward geological and capital reallocation toward larger-stone operations.

Disclaimer: The scenario projections above represent analytical frameworks and should not be interpreted as financial forecasts. Diamond market outcomes are subject to numerous variables including global consumer sentiment, currency fluctuations, geopolitical developments, and technological change in the LGD sector.

The Laboratory-Grown Diamond Disruption: A Permanent Structural Shift

The degree to which laboratory-grown diamonds have penetrated the small-carat natural diamond market in a relatively short timeframe is not widely appreciated outside specialist circles. The technology enabling gem-quality LGD production, primarily chemical vapour deposition (CVD) and high-pressure high-temperature (HPHT) synthesis, has improved dramatically in both quality and throughput efficiency since 2018.

What was initially a niche product targeting price-sensitive consumers has become the default choice in fashion jewellery and entry-level bridal segments in North American and Chinese markets. Several dynamics are driving this:

- LGD retail prices in the sub-one-carat polished category have fallen by an estimated 70-80% since 2020 as manufacturing scale increased

- Grading laboratories such as the GIA now issue full grading reports for laboratory-grown diamonds, removing the information asymmetry that previously deterred some consumers

- Major retail chains have allocated significant shelf space and marketing budgets to LGD collections, normalising the product in mainstream consumer environments

- The environmental positioning of LGDs, irrespective of its scientific accuracy in terms of energy consumption, resonates strongly with younger consumer demographics

The implication for natural small rough producers is severe. Competing on price in this environment is not viable. The only credible long-term strategy is differentiation, through provenance, certification, and the unique geological narrative that only natural diamonds possess. This is a marketing and positioning challenge that Angola rough diamond production cuts do not, and cannot, address on their own.

The next major ASX story will hit our subscribers first

Angola's Diamond Sector at a Glance: Key Data

| Metric | Figure | Context |

|---|---|---|

| 2025 rough diamond exports | 17.7 million carats | +70% year-on-year |

| 2025 total production | 15.2 million carats | Among Africa's highest |

| 2027 production target | 17 million carats | Government growth objective |

| Luele mine commercial start | 2023 | One of the largest recent kimberlite discoveries globally |

| Key operations affected | Catoca and Luele | Both subject to the new small-rough restriction |

| Restriction duration (initial) | Three months | Extendable subject to market conditions |

Angola ranks among the world's top five diamond-producing nations by volume alongside Russia, Botswana, Canada, and the Democratic Republic of Congo. Its rapid rise in production since 2023 has made it a swing factor in global rough supply, a role that carries both the power to influence market conditions and the responsibility to do so strategically. However, the broader mining geopolitical landscape reminds us that resource decisions are rarely made in isolation from wider geopolitical pressures.

What Endiama's Strategic Shift Signals for the Future of African Diamond Production

Perhaps the most consequential dimension of Angola's move is what it signals about the evolving commercial philosophy of African state-owned diamond companies. Endiama's announcement represents a departure from the volume-growth mandate that has characterised Angola's diamond sector since the post-conflict liberalisation of its mining industry in the early 2000s.

The shift toward a value-per-carat framework, where the quality and pricing of each carat produced matters more than aggregate tonnage, aligns Angola more closely with the supply-discipline traditions historically practised by Botswana's Debswana joint venture and De Beers' long-standing rough market management approach. De Beers built and sustained its market dominance for decades not through geological advantage alone, but through meticulous control of rough supply volumes and release timing. Understanding how commodity prices and miners interact further underscores why this strategic pivot carries such weight.

Whether Endiama has the institutional capacity and political support to sustain this approach through a multi-year price recovery cycle remains an open question. Angola's government has invested heavily in diamond sector infrastructure, particularly at Luele, and will face fiscal pressure to monetise that investment through volume. Balancing revenue objectives against price discipline is precisely the tension that has undermined supply coordination efforts in virtually every commodity market over time.

The fundamental test for Angola's supply discipline strategy is not whether it can hold for three months. It is whether Endiama can maintain the restriction long enough, and attract sufficient follow-through from other producers, to shift the market's expectations about future rough availability. Expectation management, not carat management, is the ultimate lever.

Frequently Asked Questions: Angola Rough Diamond Production Cuts

What mines are affected by Angola's rough diamond supply restriction?

The restriction applies to both the Catoca and Luele mines, Angola's two largest diamond-producing operations. Both generate substantial volumes of smaller-size rough diamonds, which are the specific categories targeted by the volume reduction initiative.

How long will the Angola rough diamond production cuts remain in effect?

The initial period is three months from the announcement, which was confirmed at the JCK Las Vegas industry meetings. Endiama has indicated the measure may be extended if small-rough prices and downstream demand conditions do not show adequate recovery within that timeframe.

Why are small rough diamonds the specific target of the restriction?

Small rough diamonds feed the under-one-carat polished segment, which faces the most intense competition from laboratory-grown diamonds. LGDs have achieved near-price parity with natural diamonds in this category, reducing consumer willingness to pay a natural premium and consequently compressing per-carat realisations for producers.

Is Angola physically reducing mining output or simply withholding sales?

Endiama has not confirmed which operational mechanism it will use. The distinction is commercially critical: deferred sales accumulate inventory that can flood the market if released suddenly, while actual production cuts provide more durable price support. Furthermore, additional operational details from Endiama are expected in coming weeks.

How does Angola's action compare to other major diamond producers?

Botswana, Russia, and Canada have all faced output reductions due to a combination of demand weakness, sanctions, and geological depletion respectively. Angola is unique in being the only major producer that has been actively expanding output while simultaneously choosing to impose voluntary supply discipline, making its intervention particularly significant for market sentiment.

Want to Know Which ASX Mining Companies Are Uncovering the Next Major Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the noise across 30+ commodities to surface actionable opportunities the moment they're announced. Explore historic discoveries and their returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.