June 24, 2026

The Hidden Economics of Antimony: Why Byproduct Mineralogy Is Reshaping US Critical Mineral Supply Chains

Most investors evaluating silver mining companies focus almost exclusively on silver grades, ounce estimates, and all-in sustaining costs. What frequently escapes scrutiny is the mineralogical architecture of the ore body itself, specifically whether the host mineral assemblage contains co-occurring metals that can be extracted at zero incremental mining cost. In a period where antimony critical mineral supply chain security has become a policy priority across Western economies, this distinction is evolving from a technical footnote into a genuine strategic differentiator.

Antimony is the clearest current example of this dynamic. The US Geological Survey classifies antimony as a critical mineral due to its antimony defence applications, its concentrated global supply profile, and the absence of near-term substitutes in key end uses. Yet most investors remain unfamiliar with where domestic antimony production actually comes from, or how geology determines which silver mines can produce it without additional capital expenditure.

When big ASX news breaks, our subscribers know first

Why Antimony's Supply Concentration Creates Strategic Vulnerability

China accounts for an estimated 70 to 80 percent of global refined antimony output, a concentration that has drawn increasing attention from policymakers in the United States and allied nations. Unlike many critical minerals where supply diversification is a medium-term aspiration, antimony's end-use profile makes near-term domestic production capacity a more pressing concern.

Antimony's applications span several strategically sensitive categories:

- Flame retardants in electronics, textiles, and building materials, where antimony trioxide is a primary additive

- Military ammunition and armour-piercing components, where hardened lead-antimony alloys remain the standard

- Semiconductor manufacturing, where antimony is used in certain compound semiconductors and diodes

- Lead-acid batteries, where antimony improves grid strength and charge retention

- Night-vision optics and infrared detector arrays, where antimony compounds serve as active sensing materials

The combination of military-grade applications, no near-term substitutes, and a single-nation supply concentration creates a vulnerability profile that has intensified US interest in domestic production alternatives. Furthermore, the antimony shortage risks have become particularly prominent since 2024, when supply chain security in critical minerals became a more pressing policy focus.

The Tetrahedrite Connection: Geology as Strategy

What most general investors do not know is that antimony does not typically occur as a standalone mineral in most ore systems. In silver-bearing tetrahedrite deposits, antimony is structurally incorporated into the mineral lattice itself. Tetrahedrite is a copper-antimony sulfosalt mineral with the chemical formula Cu10(Fe,Zn)2Sb4S13, meaning antimony is chemically bonded within the crystal structure alongside copper and silver.

This has a profound practical consequence: every tonne of tetrahedrite ore mined for silver automatically contains antimony and copper at fixed mineralogical ratios. At the Galena Complex in Idaho's Silver Valley, antimony occurs at approximately a 0.7:1 ratio relative to copper within this tetrahedrite mineralisation. This means antimony production is not a choice — it is a geological inevitability that scales in direct proportion to silver mining rates.

The implications are significant: unlike standalone antimony projects that require dedicated permitting, purpose-built mining infrastructure, and separate capital allocation, tetrahedrite-hosted silver operations produce antimony as an unavoidable consequence of extracting their primary metal. The question is not whether to mine antimony, but whether to capture its value.

The Americas Gold & Silver Antimony Strategy: From Byproduct Credit to Vertical Integration

For much of Galena's operating history, the antimony content in shipped concentrate was either unpaid or received a heavily discounted credit relative to prevailing market prices. This is a common structural inefficiency in the mining industry: concentrate buyers, typically smelters and traders, capture the processing spread between the value of metals in concentrate and the cost of refining them into finished products.

The Americas Gold & Silver antimony strategy represents a deliberate effort to move up the value chain and recapture that processing spread domestically. This pivot has unfolded across three sequential steps:

-

Contract renegotiation: The January 2026 revised concentrate sales agreement with Teck Resources formally recognised both copper and antimony as reportable, payable metals in shipped concentrate. This converted antimony from an accounting credit into an active cash flow line item.

-

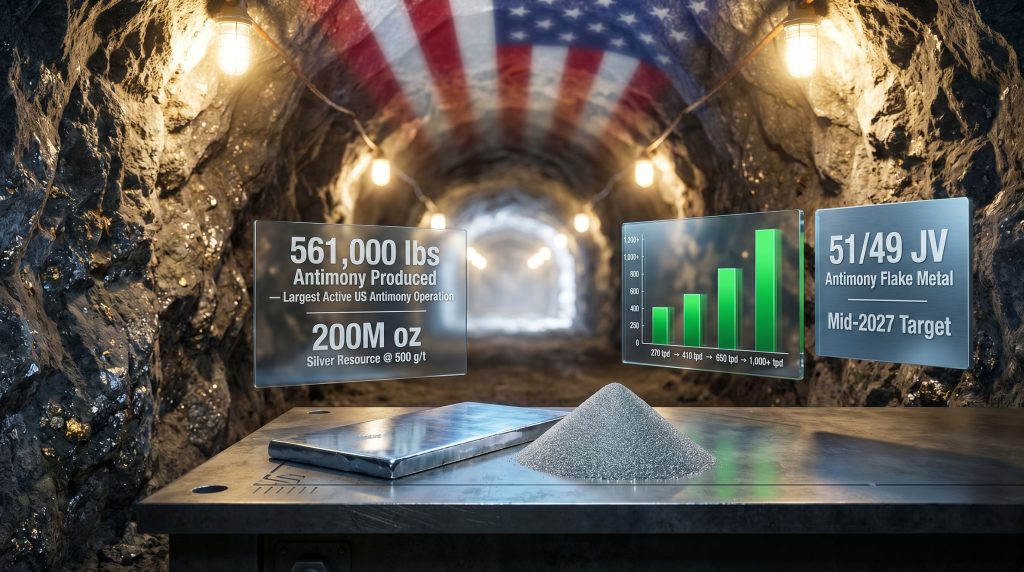

Joint venture formation: The February 2026 announcement of a 51/49 joint venture with US Antimony Corporation to construct an on-site processing facility at Galena, targeting mid-2027 commissioning, moves the company from selling antimony in concentrate to producing finished antimony flake metal.

-

Balance sheet restructuring: The May 22, 2026 equity conversion transaction with Sprott Mining eliminated the remaining silver delivery obligations, freeing cash flow for operational reinvestment into both the throughput scaling programme and the antimony processing infrastructure.

How the 51/49 Joint Venture Actually Works

The division of responsibilities between the two parties reflects complementary operational capabilities rather than a generic financial partnership. Americas brings site access, existing ore feed, and operational infrastructure at the Galena Complex antimony production. US Antimony Corporation, however, contributes the processing expertise, existing antimony marketing relationships, and the technical knowledge required to operate an on-site leaching facility.

The processing method involves leaching antimony directly from the silver-copper concentrate on site, then converting the extracted antimony into flake metal product. This captures the refining margin that currently flows to third-party concentrate buyers, increasing the realised revenue per pound of antimony produced. Metallurgical test results have demonstrated antimony recovery rates exceeding 99 percent from copper concentrate, a figure that substantially de-risks the processing economics.

High recovery efficiency means minimal feed loss, which directly improves per-unit profitability and strengthens the investment case for the facility. The company has also submitted a white paper to the US government regarding the joint venture's strategic significance, reflecting the alignment between Galena's domestic mine-to-finished-product model and broader supply chain objectives.

The Stream Termination: Mechanics, Motive, and Strategic Logic

Silver streaming agreements function as a form of project finance. A mining company sells the right to receive a fixed quantity of future silver production at a predetermined price, typically well below spot, in exchange for upfront capital. The streaming counterparty profits from the spread between the agreed delivery price and the market price over time.

From the mining company's perspective, streaming provides capital without equity dilution, but creates a structural drag on cash flow as ongoing delivery obligations divert production revenue away from operational reinvestment.

The May 22, 2026, transaction converted 592,000 ounces of remaining silver delivery obligations into equity at a deemed price of US$5.57 per share, resulting in the issuance of 7,956,696 common shares to Sprott Mining. The financial mechanics are summarised below:

| Transaction Parameter | Detail |

|---|---|

| Silver ounces retired | 592,000 oz |

| New shares issued | 7,956,696 common shares |

| Deemed conversion price | US$5.57 per share |

| Future debt obligations removed | More than US$45 million |

| Cash on hand (post-transaction) | US$122 million |

| Credit facility utilisation | US$50M drawn from US$100M available facility |

The transaction is subject to Toronto Stock Exchange approval and carries a four-month statutory hold period under applicable Canadian securities laws.

What the Sprott Conversion Signals to the Market

From a market psychology perspective, the nature of what Sprott exchanged is arguably more informative than the transaction itself. A silver streaming agreement provides contractual certainty: a defined quantity of metal delivered at a known price, regardless of what the operating company does or does not achieve. Voluntarily converting that certainty into common equity at a price materially above his initial consolidation entry point represents a forward-looking bet on operational execution and equity upside.

Eric Sprott became Americas' largest shareholder following the December 2024 consolidation of 100% Galena Complex ownership. His characterisation of Galena as among the most prolific silver mines globally, combined with his expressed confidence in management's ability to scale production and drive productivity improvements, contextualises the stream conversion as a deliberate upgrade in risk profile rather than a financial default.

When a sophisticated resource sector investor with deep sector knowledge surrenders secured contractual metal delivery rights in exchange for unsecured equity, it sends a qualitatively different signal than a new equity purchase. It suggests the investor believes the probability-weighted equity upside materially exceeds the value of the certainty being relinquished.

Galena Complex: The Asset Architecture Underpinning the Entire Strategy

The Galena Complex's credentials as a world-class silver asset are not marketing language. The operation hosts more than 200 million ounces of silver resources at 500 grams per tonne, a grade profile that ranks it as the second-highest-grade silver mine globally. The vast majority of revenue exposure, approximately 75 to 80 percent, derives from silver, with antimony, copper, and lead providing byproduct credits that structurally reduce the all-in sustaining cost per silver ounce.

Throughput Scaling: The Operational Engine

The production trajectory at Galena under current management is the operational foundation on which the antimony strategy is built. As throughput grows, antimony output grows proportionally, because both metals occupy the same ore body. Consequently, US antimony production capacity gains at Galena directly reinforce the broader domestic supply objective.

| Production Milestone | Throughput (tonnes/day) | Timeline |

|---|---|---|

| Management entry baseline | 270 tpd | Pre-2024 |

| Current operating rate | 410 tpd | 2026 |

| Year-end 2026 target | 650 tpd | Q4 2026 |

| Medium-term projection | 1,000+ tpd | Within 2 years |

The annual silver production target of 5 million ounces represents approximately 30 percent growth over 2025 guidance. Antimony output in 2025 reached approximately 561,000 pounds, establishing Galena as the largest active antimony operation in the United States.

Why Mining Method Determines Everything

The transition from conventional underhand cut-and-fill mining to long-hole stoping is the technical mechanism driving the throughput ramp, and it deserves explanation for investors unfamiliar with underground mining methods.

Underhand cut-and-fill is a selective, labour-intensive method where miners work in horizontal slices, cutting ore from below and filling the void above with waste or paste before advancing. It is precise and safe in poor ground conditions but inherently slow, with each cycle requiring significant time before the next ore slice can be accessed.

Long-hole stoping drills a series of parallel holes from an upper level down through a larger ore block, then blasts the entire column in a single firing. This allows vastly more ore to be extracted per cycle, with management reporting more than 300 percent productivity improvement and 12 times faster cycling rates across 10 test panels at Galena.

Infrastructure enabling this transition includes a modernised Number 3 shaft hoisting system to handle increased ore movement and a paste backfill plant targeting mid-2027 commissioning. By year-end 2027, approximately 70 percent of mining activity is projected to utilise long-hole stoping, fundamentally transforming the cost and volume profile of the operation.

Scenario Analysis: Three Pathways for the Americas Gold & Silver Antimony Strategy

Bull Case: Vertical Integration Delivers Premium Realisation

- The mid-2027 processing facility commissions on schedule

- Antimony spot prices remain elevated relative to historical averages

- Americas captures downstream refining margins currently paid to third-party buyers

- Realised value per pound of antimony increases materially above prior concentrate terms

- Throughput reaches 1,000+ tpd within 24 months, driving silver and antimony output to targeted levels

- Current trading at approximately 0.6x NAV re-rates toward the 2x NAV multiple observed in recent primary silver producer acquisitions, implying substantial upside from current levels

Bear Case: Execution Risk and Price Sensitivity

- Construction delays push commissioning beyond mid-2027

- Antimony prices correct from elevated levels, reducing the margin advantage of on-site processing

- US Antimony Corporation's execution of processing operations represents a critical path variable outside Americas' direct control

- Silver price weakness pressures the 75 to 80 percent revenue exposure, constraining reinvestment capital

- The stream termination share issuance adds approximately 7.96 million shares to the float, with potential selling pressure when the four-month statutory hold period expires

Base Case: Incremental Value Accretion Through Execution

- Processing facility achieves commissioning on a 6 to 12 month delay from the mid-2027 target

- Throughput reaches 650 tpd by year-end 2026, advancing toward 1,000 tpd within 24 months

- Antimony revenue grows from a byproduct credit into a standalone revenue contributor

- Valuation gradually compresses from 0.6x toward 1.0 to 1.2x NAV as operational milestones are delivered and execution risk is reduced

The next major ASX story will hit our subscribers first

Valuation Context and Market Positioning

The NAV discount at which Americas currently trades reflects the market's aggregate risk premium on execution. At approximately 0.6x NAV on street consensus estimates, compared to recent primary silver producer acquisitions at approximately 2x NAV, the implied gap represents either deep undervaluation or a market that requires further proof of operational delivery before re-rating the asset.

The growth in daily trading volume from US$400,000 to US$500,000 at management entry to US$70 to US$75 million currently is a meaningful secondary signal. This scale of volume increase typically reflects institutional participation rather than retail-driven activity. Furthermore, strategic antimony supply considerations have brought additional institutional attention to domestic producers capable of meeting defence and industrial demand. Whether that translates into multiple expansion depends on throughput milestones, antimony processing facility progress, and silver price trajectory. For a broader assessment of how this positions Americas competitively, Crux Investor's analysis of antimony as a new margin driver offers useful context.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The scenario analysis, valuation comparisons, and forward-looking statements contained herein involve assumptions and uncertainties that may not materialise as described. Investors should conduct their own due diligence and consult a qualified financial adviser before making investment decisions. Past performance of comparable transactions does not guarantee future outcomes.

Frequently Asked Questions: Americas Gold & Silver Antimony Strategy

What is the Americas Gold & Silver antimony strategy in simple terms?

The company is transitioning from selling antimony as a discounted component of silver-copper concentrate to producing finished antimony flake metal on-site through a 51/49 joint venture processing facility at the Galena Complex. The facility targets mid-2027 commissioning and is designed to capture the downstream refining margin currently paid to third-party buyers.

Why does Galena naturally produce antimony alongside silver?

Galena's ore body is hosted in tetrahedrite mineralisation, a copper-antimony sulfosalt mineral where antimony is chemically incorporated into the crystal structure. This means every tonne of ore mined for silver automatically yields antimony and copper at fixed geological ratios, with no dedicated mining capital required to produce them.

How does removing the silver stream obligation benefit the antimony strategy?

Eliminating mandatory silver delivery obligations means 100 percent of silver production revenue flows directly to Americas' balance sheet rather than being diverted to the streaming counterparty. This frees capital for reinvestment into both the throughput scaling programme and the antimony processing joint venture infrastructure.

What is the significance of the greater than 99 percent antimony recovery rate?

Metallurgical test results demonstrating this recovery efficiency confirm that the proposed processing technology performs at a very high level with minimal feed loss. This reduces the financial risk of the processing investment and strengthens the per-unit economics of on-site antimony production.

How does Galena compare to other US antimony producers?

At approximately 561,000 pounds produced in 2025, Galena is currently the largest active antimony operation in the United States. Critically, its antimony production carries near-zero incremental mining cost because it is extracted as a natural byproduct of high-grade silver operations, giving it a structural cost advantage over standalone antimony projects. In addition, junior mining network reporting on recent high-grade discoveries at Galena further underscores the depth of mineralisation supporting the long-term antimony production outlook.

Want to Track the Next Major ASX Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across more than 30 commodities — turning complex geological data into clear, actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.