June 17, 2026

The Hidden Battery Beneath America's Oldest Mountain Range

Geologists have understood for decades that the ancient rock formations running down America's eastern spine hold unusual concentrations of lithium-bearing minerals. Yet the scale of what sits beneath the Appalachian corridor has only recently come into sharper focus. The Appalachian lithium cache enough to power 130 million EVs has emerged as one of the most consequential mineral discoveries in modern US history, with implications extending well beyond academic geology into the heart of the global energy transition.

The United States finds itself in an increasingly uncomfortable position: simultaneously the world's largest consumer of advanced battery technology and one of its most import-dependent nations when it comes to the raw materials that make those batteries possible. More than half of all lithium consumed domestically arrives from overseas. Furthermore, these supply chains thread through South America's salt flats and, critically, through Chinese processing facilities that handle an estimated 60 to 70 percent of the world's refined lithium output.

When big ASX news breaks, our subscribers know first

What the USGS Study Actually Found

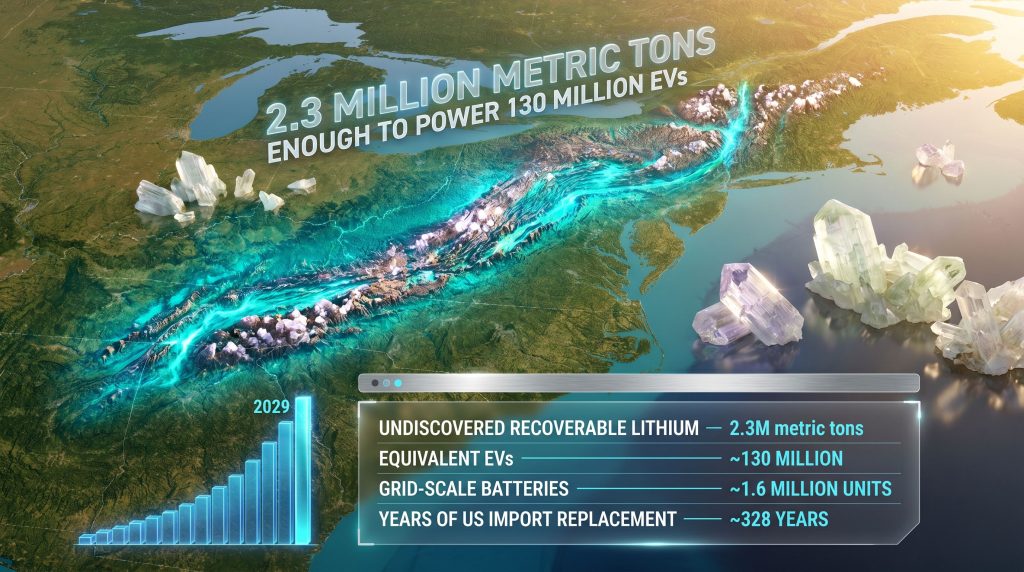

A USGS assessment published in April 2026 identified approximately 2.3 million metric tons of undiscovered, economically recoverable lithium spread across a geological corridor encompassing Maine, New Hampshire, and the Carolinas. The agency's own calculations translate that figure into the equivalent of battery material sufficient to supply roughly 130 million electric vehicles or approximately 1.6 million grid-scale battery systems.

Perhaps the most striking metric offered was the import replacement equivalency: at 2025 US import volumes, this resource could theoretically substitute for foreign lithium supply for around 328 years. USGS Director Ned Mamula characterised the findings as a meaningful contribution to US mineral security at a time when global lithium demand is accelerating rapidly. According to reporting from Mining.com, the scale of this find has prompted fresh debate about America's long-term energy independence strategy.

The figures below place the Appalachian estimate in context:

| Metric | Estimated Figure |

|---|---|

| Undiscovered recoverable lithium | 2.3 million metric tons |

| EV battery equivalent | ~130 million vehicles |

| Grid-scale battery equivalent | ~1.6 million systems |

| Years of import replacement (2025 volumes) | ~328 years |

| Approximate US EV fleet size (2025) | 4 to 5 million vehicles |

One figure rarely emphasised: the 130 million EV equivalent represents approximately 26 to 32 times the size of the entire current US electric vehicle fleet. That scale is transformative on paper, but the practical path from geological potential to road-ready battery material is long, capital-intensive, and far from guaranteed.

Understanding the Distinction Between Resource and Reserve

A recurring source of misunderstanding in critical minerals coverage involves the conflation of resource estimates with production-ready reserves. The USGS methodology for "undiscovered economically recoverable resources" relies on probabilistic modelling, geological mapping, and geochemical sampling to assess what may exist within a defined geological setting under specified economic conditions.

This classification does not mean a mine is ready to operate, nor that the lithium is confirmed through drilling. It means the underlying geology is consistent with the potential for extraction at assumed price and cost parameters. Investors and policymakers should interpret the Appalachian findings within this probabilistic framework.

Translating a USGS undiscovered resource estimate into a defined mineral resource under international reporting standards such as JORC or NI 43-101 requires systematic drilling, sampling, and economic analysis conducted by qualified mining companies. That process alone can take years before a preliminary economic assessment is even feasible.

The Geology Behind the Discovery

The Appalachian mountain belt is among the oldest geological features in North America, with its primary orogeny occurring across multiple phases spanning roughly 480 to 290 million years ago. The lithium mineralisation identified in the USGS study is primarily associated with pegmatite formations, coarse-grained igneous intrusions that form under specific pressure and temperature conditions and are known to concentrate incompatible elements, including lithium, into high-grade pockets.

Key lithium-bearing minerals found in Appalachian pegmatites include:

- Spodumene — a pyroxene mineral and the primary commercial lithium source in hard-rock mining; spodumene extraction processes are well-established globally but require significant capital investment

- Lepidolite — a lithium-rich mica with lower lithium grades but wide distribution

- Petalite — a lithium aluminium silicate found in some pegmatite systems

- Amblygonite — a phosphate mineral occasionally hosting significant lithium concentrations

The region has historical precedent for commercial mineral extraction. North Carolina's Spruce Pine pegmatite district has been actively mined for feldspar and mica for well over a century. That same geological province hosts lithium-bearing pegmatites, and North Carolina itself supported active lithium mining operations through the 1980s before market conditions led to cessation.

This history matters for two reasons. First, it demonstrates that the Appalachian region already has regulatory and operational precedent for industrial mineral extraction. Second, it means that geological characterisation of the lithium-bearing zones is not starting from zero, with historical drilling and sampling data potentially available to accelerate modern exploration programmes.

Hard-Rock Mining Versus Brine Extraction: A Technical Comparison

The Appalachian deposits are fundamentally different in character from the lithium brines explained in detail elsewhere, such as those found across South America's Lithium Triangle. Understanding this distinction matters for assessing both the opportunity and the complexity.

| Factor | Hard-Rock (Appalachian) | Brine Extraction (South America) |

|---|---|---|

| Lithium form | Spodumene, lepidolite minerals | Dissolved lithium salts in underground aquifers |

| Grade consistency | Generally higher and more uniform | Variable, dependent on aquifer chemistry |

| Water consumption | Lower during extraction | High, draws from water-scarce aquifers |

| Processing complexity | Higher (crushing, flotation, calcination, leaching) | Lower initial processing, but evaporation-dependent |

| Capital intensity | High | Moderate to high |

| Time to production | Typically longer | Variable |

| Environmental sensitivity | Tailings management, land disturbance | Aquifer depletion, ecosystem disruption |

Direct lithium extraction technologies, which EnergyX began commercialising at a Texas facility in early 2026, offer a potentially transformative processing pathway. While initially developed for brine applications, ongoing research into membrane-based and sorbent-based extraction methods may eventually find application in processing lithium-bearing solutions generated from hard-rock operations, though this remains largely developmental for pegmatite contexts.

The Supply Chain Vulnerability That Makes This Discovery Matter

The structural fragility of the US lithium supply chain is not a theoretical concern. It is a present-day reality with measurable financial and strategic consequences. Consider the layered dependency:

- Raw spodumene concentrate is mined predominantly in Australia (Greenbushes, Mt Marion, and other operations)

- That concentrate is shipped to China for conversion into lithium carbonate or lithium hydroxide

- Refined lithium compounds are then sold to battery cell manufacturers, many of which operate in China or in countries with supply agreements tied to Chinese processing infrastructure

- Battery cells eventually reach US EV manufacturers, who must navigate Inflation Reduction Act foreign entity of concern provisions affecting tax credit eligibility

A domestic Appalachian resource could, in theory, anchor an entirely US-controlled supply chain from pegmatite ore through to battery-grade lithium hydroxide. This would bypass both South American extraction geopolitics and Chinese processing dominance entirely. The Inflation Reduction Act, effective from August 2022 onward, created direct financial incentives to break this dependency through domestic content thresholds and restrictions on designated foreign entities.

How the Appalachian Find Compares to Other US Discoveries

The Appalachian estimate does not stand alone within the emerging map of domestic US lithium resources. Three distinct geological settings are now collectively reshaping assumptions about American supply chain independence. Countries holding the largest lithium reserves have long dominated global supply, however these domestic US finds are beginning to shift that balance.

| Resource | Location | Type | Scale |

|---|---|---|---|

| Appalachian Corridor | ME, NH, NC, SC | Hard-rock pegmatite | ~2.3M metric tons |

| Smackover Formation | SW Arkansas | Lithium brine | Estimated 5 to 19M metric tons |

| Thacker Pass | Nevada | Sedimentary clay | ~3.7M metric tons LCE |

The Smackover Formation in Arkansas represents the largest of these by estimated volume, with lithium brines associated with oilfield wastewater infrastructure. The Thacker Pass lithium mine in Nevada, being advanced by Lithium Americas Corp., is currently the most progressed large-scale project with a valid mining permit in place. Furthermore, Ioneer's Rhyolite Ridge project in Nevada adds a lithium-boron deposit to the western US project pipeline.

The Appalachian discovery is geographically distinct and strategically significant for a different reason: its proximity to the US East Coast manufacturing corridor, existing port infrastructure, and the dense concentration of technology and automotive supply chain activity along the eastern seaboard.

The Realistic Pathway From Geology to Production

The gap between a USGS probabilistic estimate and a functioning lithium mine is substantial. Anyone assessing the strategic value of the Appalachian lithium cache enough to power 130 million EVs must understand this development pathway and its associated timelines.

- Exploration and drilling to convert probabilistic USGS estimates into defined resource categories under recognised reporting standards

- Preliminary economic assessment evaluating mining method, processing flowsheet, infrastructure requirements, and initial capital estimates

- Pre-feasibility and feasibility studies with detailed cost modelling, geotechnical analysis, and metallurgical test work

- Environmental impact assessment and permitting under federal regulations including the National Environmental Policy Act and Clean Water Act provisions

- Infrastructure development covering processing facilities, transportation corridors, water management systems, and grid connections

- Capital raising and project financing, which for greenfield hard-rock lithium projects typically requires significant institutional backing

- Construction and commissioning, followed by ramp-up to nameplate production capacity

Across these stages, a greenfield hard-rock lithium project in North America typically requires 10 to 20 years from initial discovery to sustained commercial production. The Appalachian corridor currently has no advanced-stage development projects of meaningful scale. Consequently, the USGS findings represent a long-horizon opportunity rather than a near-term supply solution.

The next major ASX story will hit our subscribers first

Global Demand Growth and Why the Timeline Pressure Is Real

The USGS projects that global lithium production capacity will approximately double by 2029, driven by aggressive EV manufacturing expansion across the US, Europe, and China. This trajectory creates a narrowing window for new supply to enter the market before demand growth begins to stress available capacity.

BloombergNEF and the International Energy Agency have both modelled scenarios in which lithium supply deficits emerge in the late 2020s without significant new project development. In addition, battery manufacturers are increasingly seeking long-term offtake agreements with geopolitically stable suppliers. According to analysis from the USC Energy Research Institute, these supply pressures are creating potential first-mover advantages for any domestic project that can demonstrate a credible development path.

The 328-year import replacement figure assumes static demand, which is a deliberately conservative baseline. Under realistic demand growth scenarios incorporating EV adoption acceleration and grid storage expansion, the actual supply buffer would compress substantially, but would still represent multiple decades of meaningful contribution to US battery material needs.

Disclaimer: The analysis and projections presented in this article, including demand forecasts, supply timelines, and economic modelling references, are based on publicly available information and third-party assessments. They do not constitute financial or investment advice. Mineral resource estimates carry inherent uncertainty and should not be interpreted as guarantees of economic viability or production outcomes.

Frequently Asked Questions

How much lithium has been found in the Appalachian region?

The USGS assessment identified approximately 2.3 million metric tons of undiscovered, economically recoverable lithium across a corridor spanning Maine, New Hampshire, and the Carolinas. This is a probabilistic estimate derived from geological modelling, not a confirmed drilled resource.

Can this cache genuinely power 130 million electric vehicles?

Based on USGS calculations, the theoretical battery material yield from 2.3 million metric tons would be sufficient to supply approximately 130 million electric vehicles, or around 1.6 million grid-scale battery systems. This assumes full economic recovery of the estimated resource, which would require decades of extraction activity.

Is lithium being mined in the Appalachian region today?

There is no active large-scale commercial lithium mining in the Appalachian corridor. Historical operations in North Carolina ceased in the 1980s. The USGS findings identify future geological potential, not current production capacity.

Who is the only current US domestic lithium producer?

Albemarle Corporation currently operates the only producing lithium mine in the United States, the Silver Peak operation in Nevada. Canada's Lithium Americas Corp. and Australia's Ioneer Ltd. are both seeking to develop new mines in Nevada, representing the most advanced additions to the US production pipeline.

How does the Appalachian discovery compare to the Arkansas lithium formation?

The Smackover Formation in southwestern Arkansas is estimated to contain between 5 and 19 million metric tons of lithium within subsurface brines, making it substantially larger by volume. However, the two deposits are geologically and operationally distinct. Appalachian lithium occurs in solid pegmatite rock, while Smackover lithium is dissolved in deep subsurface brines associated with historic oil and gas infrastructure.

What lithium price assumptions underpin the USGS economic recoverability estimate?

The USGS's definition of economically recoverable resources incorporates assumptions about extraction costs, processing efficiency, and commodity prices. These parameters influence which portions of a deposit are classified as recoverable and should be revisited as lithium market conditions evolve. Investors should note that changes in lithium pricing can materially affect the economically recoverable portion of any resource estimate.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex geological data into actionable investment insights for both short-term traders and long-term investors — explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.