May 21, 2026

The Supply Chain Problem That Rare Earth Markets Have Never Solved

For decades, Western manufacturers of electric motors, wind turbines, and precision defence systems have operated with a structural vulnerability hidden in plain sight. The magnets that make their most advanced products work depend on a single oxide compound processed almost entirely within one country. Every EV drivetrain, every offshore wind generator, every guided weapons system using rare earth permanent magnets traces its most critical input back to Chinese separation infrastructure. That is not a political observation — it is a supply chain architecture fact that has persisted across multiple technology cycles, trade disputes, and strategic reviews.

The Arafura Nolans rare earths project FID, confirmed in May 2026, represents the most advanced attempt yet to structurally alter that reality at commercial scale outside of China.

When big ASX news breaks, our subscribers know first

Why NdPr Oxide Sits at the Centre of Every Clean Energy and Defence Supply Chain

The Irreplaceable Input Inside High-Performance Magnets

Neodymium-praseodymium oxide, universally abbreviated to NdPr, is the feedstock from which rare earth permanent magnets (REPMs) are manufactured. Specifically, the dominant magnet type — neodymium-iron-boron (NdFeB) — requires NdPr as its primary functional element. These magnets generate the powerful, compact magnetic fields that make high-torque electric motors and direct-drive wind turbine generators both technically feasible and economically viable at scale.

What makes NdPr strategically irreplaceable is the absence of a commercially viable substitute at equivalent performance and cost. Ferrite magnets, the most common alternative, deliver significantly lower energy density, which means heavier motors, lower efficiency, and reduced range in EV applications. For automotive engineers targeting power density targets in constrained packaging spaces, the performance trade-off of switching away from NdFeB is not a rounding error — it is a fundamental engineering constraint.

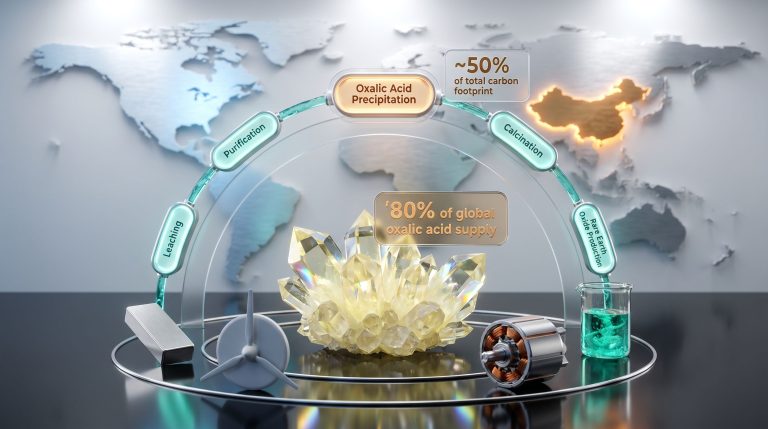

China's Refining Chokehold: A Structural Risk, Not Just a Trade Story

The widely cited statistic that China controls roughly 85 to 90 percent of global rare earth separation and refining capacity understates the true nature of the dependency. Western miners can extract rare earth-bearing ore. The problem has always been what happens next.

Most non-Chinese rare earth mining operations, when they reach the processing stage, must either ship concentrate to Chinese separation facilities or rely on the very limited number of non-Chinese hydrometallurgical plants — most of which themselves depend on Chinese-sourced reagents or technical expertise. This creates a structural chokehold not at the mining stage but at the oxide separation stage, which is the step that produces the NdPr oxide that magnet manufacturers actually need to buy.

China has demonstrated its willingness to restrict rare earth supply chain exports as a trade policy instrument on multiple occasions, most recently through controls on rare earth processing technology and equipment exports introduced in 2023. Each restriction event accelerates the urgency felt by Western governments and manufacturers to find alternative separation capacity, but building that capacity takes years and requires overcoming project finance barriers that have historically proven extremely difficult to clear without Chinese participation.

What the Nolans Project Actually Produces: A Full Output Breakdown

Integrated Mine-to-Oxide Processing: Why Location Matters

The Nolans project is located approximately 135 kilometres north of Alice Springs in Australia's Northern Territory. Its defining technical characteristic is vertical integration across the entire value chain from ore extraction through to separated rare earth oxide, all within a single Northern Territory facility. This is not merely a logistical efficiency — it eliminates the structural dependency on third-party, often Chinese, separation infrastructure that undermines the supply chain sovereignty claims of many competing rare earth projects.

The term mine-to-oxide carries specific commercial significance. Producing separated NdPr oxide rather than a mixed rare earth concentrate means Nolans output is drop-in ready for magnet alloy manufacturers in Japan, South Korea, Europe, and North America. These manufacturers buy oxide, not concentrate, and they currently source the overwhelming majority of that oxide from Chinese suppliers. A non-Chinese separated oxide producer changes the purchasing equation in a way that a concentrate supplier does not.

Full Production Profile at Nameplate Capacity

| Product | Annual Output | Specification |

|---|---|---|

| NdPr Oxide | 4,440 t/yr | Separated light rare earth oxide |

| Mixed Medium-Heavy Rare Earth Oxide | 470 t/yr | Includes Dy, Tb, Ho, Er fractions |

| Phosphoric Acid | 144,000 t/yr | 54% P₂O₅, fertilizer-grade |

| Total Rare Earth Output | 4,870 t/yr | Across all rare earth product streams |

Source: Arafura Resources

The medium-heavy rare earth fraction deserves particular attention. While modest in volume at 470 tonnes per year, it contains dysprosium and terbium — elements critical for high-temperature magnet performance in automotive traction motors where heat management is a primary engineering challenge. Global separated supply of these heavy rare earths outside China is extremely limited, giving this fraction strategic value disproportionate to its tonnage.

The phosphoric acid co-product adds a meaningful economic dimension that many commentators overlook. At 144,000 tonnes per year of fertilizer-grade phosphoric acid, Nolans generates a secondary commodity revenue stream with its own independent market pricing. This co-product revenue partially hedges project economics against NdPr price volatility — a structurally important feature when rare earth prices have demonstrated significant cyclical swings over the past decade.

Lesser-Known Technical Detail: The phosphate mineralisation at Nolans is integral to the deposit's geology, not incidental. The ore body contains apatite-hosted rare earths, meaning the phosphate and rare earth elements are co-located within the same mineral phase. The hydrometallurgical process extracts both simultaneously, making the phosphoric acid co-product a natural output of the rare earth circuit rather than a separate operation. This co-processing efficiency is a genuine cost advantage that purely rare earth-focused operations cannot replicate.

How the Nolans Capital Stack Was Assembled

Debt Architecture: Tiered Facilities Addressing Different Risk Layers

Securing project finance for a first-of-kind integrated rare earth processing facility requires lenders to accept risks they have rarely evaluated in a Western context. The debt structure assembled for Nolans addresses this through layered facilities, each targeting a specific risk category:

- US$775 million senior debt facilities covering the primary construction capital requirement

- US$80 million cost overrun facility providing a dedicated buffer against construction cost escalation in a remote Northern Territory environment

- US$200 million subordinated standby liquidity facility designed to support construction-phase cash flow and production ramp-up, protecting against the scenario where commissioning delays create a revenue gap before debt service obligations begin

The total debt-side capital commitment across all facility types approaches approximately US$1.055 billion, indicating a total project capital requirement well above the US$1 billion threshold when equity contributions are incorporated.

Equity and Sovereign Co-Investment

Australia's National Reconstruction Fund committed A$200 million (approximately US$144 million) to the Nolans project on 12 May 2025. This commitment from a government co-investment vehicle provided a catalytic anchor that signalled federal confidence in the project's commercial and strategic viability at a critical moment in the financing process. Furthermore, the critical minerals demand surge across Western economies has made sovereign co-investment instruments of this kind increasingly common as governments seek to reduce strategic exposure.

The EFA Offtake Mechanism: The Instrument That Triggered FID

The precise catalyst for the board's Final Investment Decision was a non-binding letter of support from Export Finance Australia (EFA) covering 500 tonnes per year of NdPr oxide under Australia's Critical Minerals Strategic Reserve framework. This commitment pushed Arafura's contracted offtake from below the board-mandated threshold to 80.4% of nameplate capacity, crossing the internal gate condition that the board had established as a precondition for FID approval.

The Critical Minerals Strategic Reserve mechanism functions as a government-as-offtake-counterparty instrument. Rather than simply funding exploration or offering loan guarantees, the sovereign acts as a committed buyer of physical product at commercial terms. This structure directly solves the project finance problem: lenders require demonstrated revenue certainty before committing capital, and offtake contracts provide that certainty. By making the government a volume-contracted purchaser, the mechanism converts a policy aspiration into bankable revenue — a materially different intervention than most critical minerals policy tools previously deployed in Western jurisdictions.

The Offtake Architecture: Contracted Demand from Four Continents

Full Contracted Offtake Breakdown

| Counterparty | Domicile | Agreement Date | NdPr Oxide (t/yr) | % of Nameplate |

|---|---|---|---|---|

| Hyundai & Kia | South Korea | November 2022 | 1,500 | 33.8% |

| Siemens Gamesa RE | Germany | April 2023 | 520 | 11.7% |

| Traxys Europe | Luxembourg | March 2025 | 300 | 6.8% |

| Traxys North America | United States | May 2025 | 500 | 11.3% |

| Export Finance Australia | Australia | May 2025 | 500 | 11.3% |

| Unspecified OEM | Germany/Europe | Undisclosed | 250 | 5.6% |

| Total Contracted | 3,570 | 80.4% | ||

| Uncontracted (spot market) | — | — | 870 | 19.6% |

Source: Arafura Resources

Reading the Counterparty Mix as a Market Intelligence Signal

The composition of Arafura's offtake book reveals which industry sectors feel the most acute pressure to secure non-Chinese NdPr supply and have translated that pressure into contractual commitments. The Arafura-Traxys rare earth deal is a particularly notable component of this book, demonstrating how commodity trading intermediaries are positioning themselves within the emerging non-Chinese supply ecosystem:

-

Hyundai and Kia's 33.8% anchor position reflects South Korea's acute structural exposure. Korean automakers are scaling EV production aggressively across multiple model platforms, and their procurement teams understand that NdPr sourced entirely from Chinese supply chains creates a single-point-of-failure risk in their manufacturing operations.

-

Siemens Gamesa's 11.7% commitment connects Nolans directly to European offshore wind turbine manufacturing. Under the EU Critical Raw Materials Act, European industrial manufacturers face increasing regulatory and reputational pressure to demonstrate supply chain provenance for critical minerals. An offtake agreement with a fully integrated Australian producer directly addresses that requirement.

-

Dual Traxys offtake agreement structures across European and North American entities introduce commodity trading intermediaries capable of redistributing volumes across multiple downstream magnet manufacturers. This broadens the effective end-customer base significantly beyond the six named counterparties.

-

The undisclosed German/European OEM holding 250 t/yr is a notable signal. The fact that a major industrial manufacturer has secured volume but not yet disclosed the relationship publicly suggests commercial sensitivity around supply chain strategy — consistent with the behaviour of a large automotive or industrial OEM managing competitive disclosure risk.

Why 80.4% Is the Structurally Significant Number

Project finance lenders to long-duration mining and processing assets apply rigorous offtake coverage analysis before committing capital. The logic is straightforward: contracted revenue streams directly support debt service coverage ratio calculations, and insufficient offtake coverage creates scenarios where price weakness could impair repayment capacity.

Arafura's board established an 80% contracted nameplate threshold as its internal FID precondition. Achieving exactly 80.4% is therefore not a coincidence — it reflects deliberate sequencing of offtake negotiations to reach the minimum bankable threshold without overly concentrating contracted volume at terms that might not reflect prevailing market conditions at the time of production commencement.

The remaining 870 t/yr uncontracted volume (19.6% of nameplate) provides exposure to NdPr spot market upside during the project's operating life, functioning as a built-in revenue optionality mechanism within an otherwise conservatively structured project finance framework.

Construction Timeline and Technical Execution Risk

From FID to First Production: The Critical Path

- Construction commencement: September 2025

- EPCM contractor: Hatch (global mining and metallurgical engineering firm with significant hydrometallurgical project experience)

- Estimated construction duration: 30 months

- Targeted first production: early-to-mid 2029

- Mine life underpinning long-term production: 38 years

What Are the Execution Risks Specific to This Project Type?

Hydrometallurgical rare earth separation facilities are among the most technically complex processing plants in the mining industry. Unlike conventional mineral processing, rare earth separation circuits involve sequential solvent extraction stages where dozens of organic-aqueous extraction steps produce individual rare earth fractions with very high purity specifications. Commissioning these circuits consistently at nameplate throughput and product specification is a known industry challenge — even well-resourced projects have historically experienced 12 to 24 month commissioning delays.

Key execution risks for the Arafura Nolans rare earths project FID construction phase include:

- Remote logistics complexity — Supplying a large construction workforce and heavy equipment to a site 135 km from Alice Springs requires dedicated logistics infrastructure that is vulnerable to Northern Australian seasonal weather events

- Solvent extraction commissioning — Achieving stable, specification-grade NdPr oxide separation from a multi-element rare earth feed stream requires precise chemistry management that often takes months to optimise post-mechanical completion

- Reagent supply chain resilience — Hydrometallurgical processing requires sulphuric acid and other reagents in large volumes; Northern Territory supply chain logistics for these inputs represent a material operational planning requirement

- Skilled labour constraints — Northern Australia faces structural skilled workforce shortages for specialised hydrometallurgical and chemical engineering roles

The US$80 million cost overrun facility and US$200 million standby liquidity facility represent the financial mitigation architecture for these risks. Together they provide approximately US$280 million of contingency and liquidity headroom above the primary construction budget.

The next major ASX story will hit our subscribers first

Nolans in Global Context: Where It Sits in the NdPr Project Landscape

Comparative Project Overview

| Project | Developer | Country | Est. NdPr Output | Status |

|---|---|---|---|---|

| Nolans | Arafura Resources | Australia | ~4,440 t/yr | FID reached; construction commencing |

| MP Materials (Mountain Pass) | MP Materials | USA | ~6,000 t/yr (oxide equiv.) | Operating; expanding downstream |

| Lynas Rare Earths (Mt Weld) | Lynas | Australia/Malaysia | ~7,000+ t/yr NdPr | Operating |

| Pensana (Longonjo) | Pensana | Angola | ~4,500 t/yr | Pre-construction |

| Vital Metals (Nechalacho) | Vital Metals | Canada | Smaller scale | Early stage |

Lynas Rare Earths remains the world's dominant non-Chinese rare earth producer, processing concentrate from its Mt Weld mine in Western Australia through its Malaysian separation facility. Nolans is structurally complementary rather than competitive with Lynas — both produce NdPr oxide for the same growing non-Chinese supply market, and at projected combined output levels, the two operations together still represent a relatively small fraction of total global NdPr demand. The Western rare earth supply deficit is large enough to accommodate multiple commercial-scale producers without creating oversupply conditions.

The Nolans project's fully Australian processing model — specifically avoiding the concentrate-to-third-country-processing pathway that created regulatory risk for Lynas in Malaysia — reflects a deliberate design choice to maximise supply chain sovereignty credentials for downstream customers. However, the rare earth geopolitical risk landscape continues to evolve rapidly, and the strategic value of fully sovereign processing infrastructure is likely to increase rather than diminish over the project's 38-year mine life.

Scenario Analysis: Three Pathways to 2029

Bull Case: Aligned Execution

- NdPr spot prices recover materially above 2024–2025 levels as EV penetration accelerates beyond baseline forecasts

- Hatch delivers the EPCM contract within the 30-month construction window

- The 870 t/yr uncontracted volume attracts term agreements before first production, eliminating spot exposure

- Outcome: Nolans enters production in early 2029 as a fully contracted, cash-generative oxide producer

Base Case: Managed Execution Risk

- Construction encounters 3 to 6 month delays related to Northern Territory logistics or hydrometallurgical circuit commissioning

- NdPr prices remain range-bound; uncontracted volume sold into spot markets at prevailing rates

- Phosphoric acid co-product revenue provides meaningful support during ramp-up

- Outcome: First production mid-2029; full nameplate capacity achieved within 12 to 18 months

Stress Case: Price and Execution Headwinds

- Sustained NdPr price weakness compresses projected revenue, creating tension with debt service coverage ratios

- Construction cost overruns approach or exhaust the US$80 million contingency facility

- Geopolitical disruption creates downstream uncertainty among some offtake counterparties

- Outcome: Project timeline extends toward late 2029 or beyond; however, the 38-year mine life and multi-layered sovereign financial support provide structural resilience against short-term market stress

Disclaimer: Scenario projections are illustrative analytical frameworks only and do not represent financial forecasts or investment advice. Actual project outcomes will depend on factors including commodity price movements, construction execution, regulatory conditions, and broader macroeconomic variables that cannot be predicted with certainty.

Frequently Asked Questions: Arafura Nolans Rare Earths Project FID

What Is the Arafura Nolans Rare Earths Project?

The Nolans project is a fully integrated mine-to-oxide rare earth development located approximately 135 km north of Alice Springs in Australia's Northern Territory. It is designed to produce 4,440 tonnes per year of separated NdPr oxide alongside 470 t/yr of mixed medium-heavy rare earth oxides and 144,000 t/yr of fertilizer-grade phosphoric acid, with a mine life of 38 years. For further detail on the project's technical scope, Arafura's official project update provides comprehensive current information.

What Does the Arafura Nolans FID Actually Mean?

A Final Investment Decision is the formal board-level commitment to deploy full project construction capital. For the Arafura Nolans rare earths project FID, this triggers a 30-month construction programme beginning September 2025, with first production targeted for early-to-mid 2029. It represents the transition from a development asset to an asset under active construction.

Why Is NdPr Oxide Strategically Critical?

NdPr oxide is the essential input for neodymium-iron-boron permanent magnets, which deliver the highest magnetic energy density of any commercially produced magnet type. These magnets power EV traction motors, direct-drive wind turbine generators, and high-performance defence systems. No commercially competitive substitute currently exists at equivalent performance and cost, making reliable non-Chinese NdPr supply a strategic priority for manufacturers and governments across Europe, North America, Japan, and South Korea.

Who Are the Major Offtake Partners?

Contracted counterparties include Hyundai and Kia (South Korea), Siemens Gamesa Renewable Energy (Germany), Traxys Europe (Luxembourg), Traxys North America (United States), Export Finance Australia, and an undisclosed European OEM. Combined contracted volumes represent 80.4% of nameplate NdPr oxide capacity, totalling 3,570 t/yr.

What Makes Nolans Different from Other Rare Earth Projects?

The single-site, fully integrated processing model that produces separated NdPr oxide rather than concentrate is the defining differentiator. This eliminates dependency on third-party, often Chinese, separation infrastructure and delivers a product that magnet alloy manufacturers can use directly without further processing. Very few non-Chinese rare earth projects in development are capable of replicating this end-to-end integration at comparable scale.

Key Takeaways for Investors and Supply Chain Strategists

The Arafura Nolans rare earths project FID carries implications that extend well beyond a single project announcement. It demonstrates several propositions that were genuinely uncertain as recently as three years ago. Furthermore, the Australian Government's project analysis provides additional context on how sovereign financial instruments have been deployed to enable this outcome:

- Integrated non-Chinese NdPr oxide production at commercial scale is now bankable through a combination of sovereign financial participation and commercial offtake agreements structured across multiple geographic regions

- The government-as-offtake-counterparty model deployed through Australia's Critical Minerals Strategic Reserve has now functioned as an active project enablement instrument, not merely a policy statement — establishing a template that other Western governments are likely to study closely

- The 80.4% contracted offtake coverage ratio, combined with a 38-year mine life and a multi-layered debt structure with US$280 million of contingency headroom, creates a structurally de-risked production profile that distinguishes Nolans from earlier-stage rare earth development projects

- A projected 4% contribution to global NdPr demand upon reaching nameplate capacity positions Nolans as a meaningful but not market-flooding supply addition, preserving price support while diversifying the supply base available to Western manufacturers

- The phosphoric acid co-product, often overlooked in strategic commentary focused on rare earths, represents a genuine revenue diversification mechanism that reduces the project's sensitivity to NdPr price cycles

The construction phase commencing in September 2025 will test whether the project's financial architecture is as resilient in execution as it is in design. The 30-month construction window to early-to-mid 2029 is the period during which the gap between capital formation success and operational delivery will either close or widen.

This article is for informational and analytical purposes only. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex mineral data into clear, actionable insights for investors at every level. Explore how historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.