May 21, 2026

The Permanent Magnet Supply Chain Problem Western Industry Can No Longer Ignore

Every electric vehicle motor, every offshore wind turbine nacelle, and every industrial servo system that powers modern manufacturing shares a common dependency: neodymium-praseodymium oxide, better known as NdPr. This refined rare earth compound sits at the heart of sintered permanent magnets, the most energy-dense magnetic technology available at commercial scale. Without it, the physical hardware of the clean energy transition simply does not function.

For decades, the processing and refining of rare earth elements has been concentrated within a single national jurisdiction, creating a structural vulnerability that Western governments and industrial manufacturers have only recently begun to address with genuine urgency. The challenge is not merely one of mine supply; it is a processing dependency problem, and understanding the rare earth supply chain importance helps clarify why this matters so deeply to allied nations.

Ore can be dug from the ground across multiple continents, but transforming it into the refined oxide compounds that magnet manufacturers actually purchase requires chemical processing infrastructure that has, until recently, existed almost exclusively in China. This is the structural backdrop against which the Arafura Rare Earths Nolans project FID must be understood — not as a single company announcement, but as a data point in a much larger reconfiguration of how the world's most technology-critical supply chains are being rebuilt from first principles.

When big ASX news breaks, our subscribers know first

What Makes the Nolans Project Structurally Different From Other Rare Earth Developments

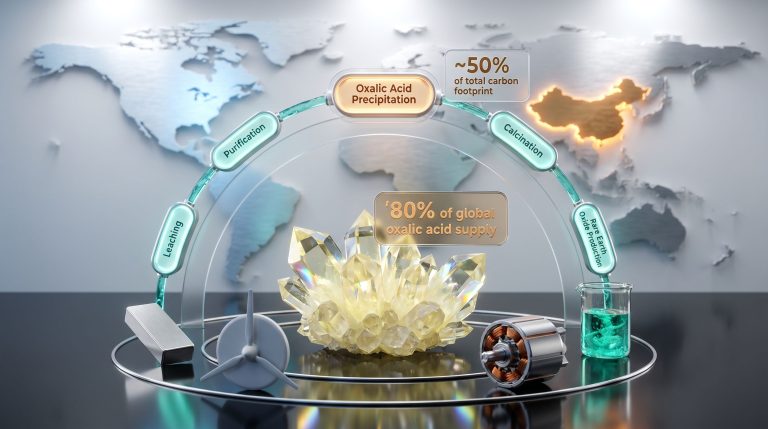

The Ore-to-Oxide Distinction and Why It Changes Everything

Most rare earth projects in development outside China operate on a concentrate-export model. Ore is mined, processed into an intermediate concentrate, and then shipped to a refinery, often in Asia, for the final chemical separation steps that produce saleable oxide. This model is commercially simpler to finance and build, but it perpetuates the processing dependency that Western supply chain strategists are trying to eliminate.

The Nolans project takes a fundamentally different approach. Positioned in Australia's Northern Territory, it is designed as a fully integrated ore-to-oxide operation, capturing every stage of the value chain from mine extraction through to finished NdPr oxide within a single site and a single jurisdiction. This is not merely a technical distinction; it is a geopolitical one. Furthermore, the rare earth processing challenges involved in achieving this within a single jurisdiction make the project's design all the more remarkable.

A fully integrated ore-to-oxide facility captures margin at every processing stage while simultaneously eliminating the geopolitical exposure that comes with sending intermediate products through foreign refining infrastructure. For Western governments prioritising supply chain sovereignty, this single-site integration model represents the gold standard of rare earth project design.

The competitive implications of this model are significant when compared to concentrate-export peers:

| Project Model | Processing Jurisdiction | Geopolitical Exposure | Value Capture |

|---|---|---|---|

| Ore-to-oxide (Nolans) | Single site, Australia | Low | Full chain |

| Concentrate export | Mine in West, refinery in Asia | High | Partial |

| Toll refining arrangements | Variable | Moderate to high | Partial |

The Nolans Deposit: Geology and Grade Profile

The Nolans Bore deposit in the Northern Territory is not a conventional rare earth deposit. It hosts a phosphate-uranium-rare earth mineralisation style that is mineralogically distinct from the laterite and carbonatite deposits more commonly associated with global rare earth production. The deposit's rare earth mineralisation is hosted primarily in apatite, a calcium phosphate mineral, which has implications for both the metallurgical processing route and the extraction chemistry required.

This apatite-hosted mineralogy means the Nolans processing flowsheet must handle phosphate and uranium as co-products or by-products of the rare earth extraction process, adding complexity to the plant design but also potentially creating additional revenue streams. The deposit's grade profile includes a meaningful concentration of NdPr within the total rare earth oxide basket, which is the critical metric for permanent magnet market relevance.

Not all rare earth deposits are created equal; projects with low NdPr fractions within their total rare earth mix generate far less value per tonne of ore processed, regardless of headline grade figures. Nolans' NdPr composition within its ore basket is considered commercially competitive for the permanent magnet supply chain. At nameplate capacity, the project is projected to contribute approximately 4% of global NdPr oxide supply — a figure that sounds modest in isolation but takes on strategic significance when considered against the near-total Western dependency on Chinese processing that currently exists.

The Financing Architecture: A Multi-Sovereign Capital Stack

How the Nolans Funding Structure Was Assembled

The capital structure assembled to finance the Nolans project is arguably as significant as the project itself. It represents a template for how Western governments can deploy financial instruments to shift large-scale critical mineral projects from development-stage assets to construction-ready infrastructure. Consequently, the critical minerals demand surge has accelerated the urgency with which allied governments are deploying such instruments.

| Facility Type | Amount | Provider |

|---|---|---|

| Senior Debt Facilities | US$775 million | Conditional approval secured |

| Cost Overrun Facility | US$80 million | Supplementary debt layer |

| Subordinated Standby Liquidity | Up to US$200 million | Export Finance Australia (EFA) |

| Enabling Infrastructure Support | Up to A$200 million | Northern Australia Infrastructure Facility (NAIF) |

| Cornerstone Equity Subscriptions | Binding commitments | EFA, National Reconstruction Fund Corp, German Raw Materials Fund |

The participation of sovereign-backed institutions from Australia, Germany, South Korea, Canada, and the United States in the financing structure reflects a deliberate strategy of anchoring the project within the allied critical minerals security framework. Export Finance Australia has issued a non-binding letter of support, while the National Reconstruction Fund Corporation has made binding cornerstone equity commitments.

The German Raw Materials Fund's participation signals European industrial policy alignment, as Germany's manufacturing sector, particularly its automotive industry, faces acute exposure to rare earth supply disruption. The Australian Government's strategic backing of this project further underscores the national significance attached to the Nolans development.

Understanding the Gap Between FID and Financial Close

A critical distinction that investors in ASX-listed critical mineral companies often underappreciate is the difference between a Final Investment Decision and financial close. The FID represents the board's authorisation to proceed with the project and begin mobilising contractors and resources. Financial close, by contrast, is the point at which all funding commitments are legally locked, drawn, and the full capital stack is in place.

For the Arafura Rare Earths Nolans project FID achieved in May 2026, the remaining equity funding gap must be closed before the September 2026 construction commencement target becomes executable. The cornerstone equity strategy — using anchor commitments from sovereign-backed institutions to de-risk the broader equity placement — is the mechanism through which this gap is being addressed.

The speed of equity close-out between now and September 2026 is the single most consequential execution variable for the Nolans timeline. Binding offtake agreements provide lenders and equity investors with revenue certainty, but anchor commitments must translate into full financial close for ground-breaking to proceed on schedule.

Offtake Partners and the Strategic Logic of Demand Diversification

A Four-Continent Customer Base

The binding offtake agreements secured prior to the Nolans FID are not standard commodity sales contracts. They represent strategic procurement decisions by tier-one industrial manufacturers who have identified upstream NdPr supply security as a business-critical priority. The Arafura Traxys offtake agreement is one such example, demonstrating how these partnerships extend well beyond conventional commercial arrangements:

- Hyundai and Kia provide exposure to South Korea's EV manufacturing sector, one of the world's most technologically advanced, and create a direct link between the Nolans supply chain and the permanent magnets used in traction motors for mass-market electric vehicles.

- Siemens Gamesa connects Nolans to the European wind energy manufacturing ecosystem, where permanent magnet direct-drive turbine designs are becoming the dominant offshore wind technology, significantly increasing per-turbine NdPr demand relative to older geared designs.

- Traxys provides a commodity trading intermediary structure that offers flexibility in volumes and pricing mechanisms, useful for managing the ramp-up phase of production.

The geographic diversity of this customer base across Europe, East Asia, and potentially North American markets creates a natural hedge against single-region demand cycles. A slowdown in European wind installations, for example, does not eliminate offtake if Korean EV production remains robust.

Why Binding Offtake Is a Bankability Requirement, Not Just a Commercial Milestone

Project finance lenders providing the US$775 million senior debt facility require revenue certainty as a condition of lending. Binding offtake agreements, particularly from investment-grade counterparties such as Hyundai, Kia, and Siemens Gamesa, directly satisfy this requirement by demonstrating that the project has creditworthy buyers for its output.

This is why the sequence of offtake signings preceding the FID was not merely commercial news; it was a necessary precondition for the financing structure to hold together. Furthermore, the Arafura rare earth supply deal with Traxys illustrated how strategically these agreements were sequenced to build lender confidence ahead of the formal FID.

Project Timeline and Construction Execution Risk

Key Milestones from Development to First Production

| Milestone | Status / Target Date |

|---|---|

| Full project permitting | Completed |

| Senior debt conditional approval (US$775M + US$80M) | Secured |

| Binding offtake (Hyundai, Kia, Siemens Gamesa, Traxys) | Executed |

| Cornerstone equity (EFA, NRFC, German Raw Materials Fund) | Binding commitments secured |

| Final Investment Decision | Achieved, May 2026 |

| EPCM contractor engagement (Hatch) | Early engagement initiated |

| Construction commencement target | September 2026 |

| Construction period | 37 months |

| Operating activities commencement | Approximately 4 months pre-completion (~mid-2029) |

| Construction completion | Approximately October 2029 |

| Ramp-up to nameplate NdPr oxide capacity | Post first production |

Construction Risk Variables for a Remote Ore-to-Oxide Facility

Constructing a greenfield ore-to-oxide rare earth processing facility in a remote Northern Territory location introduces execution risk variables that are materially different from standard open-pit mining projects. The processing plant component of the Nolans facility requires hydrometallurgical circuits, solvent extraction infrastructure, and chemical reagent handling systems that demand specialised engineering and construction expertise.

The engagement of Hatch as the EPCM contractor is significant in this context. Hatch is a global engineering firm with a specific track record in complex hydrometallurgical and chemical processing plant design and construction, making them a technically credible choice for a project of this nature. The US$80 million cost overrun facility built into the capital structure acknowledges that greenfield processing plant construction in remote locations carries inherent budget variance risk, and structures a financial buffer to absorb it without jeopardising project completion.

The 38-Year Mine Life: Long-Duration Economics in Critical Minerals

Why Asset Longevity Changes the Investment Return Profile

A 38-year operating mine life is exceptional by any measure in the resources sector. For context, most base metal mining projects are designed and financed on the basis of 15 to 25 year mine lives, with resource extensions expected but not guaranteed. A 38-year horizon fundamentally alters the capital amortisation logic: the large upfront construction cost is spread across a much longer production life, improving the long-run average cost per unit of NdPr oxide produced.

This extended duration also provides strategic optionality. As permanent magnet demand grows through the 2030s and 2040s, driven by accelerating EV penetration and offshore wind build-out, a project with a four-decade operating life is structurally positioned to capture multiple demand growth cycles rather than a single wave.

Industry forecasters have modelled NdPr oxide demand growth as one of the most robust long-term trajectories in the critical minerals space, with some projections suggesting demand could increase several-fold between now and 2040. Investors should note that demand forecasts of this nature involve significant uncertainty and should not be treated as guaranteed outcomes.

The next major ASX story will hit our subscribers first

What the FID Signals for the Broader Critical Minerals Investment Landscape

From Development Asset to Construction-Stage Infrastructure

The Arafura Rare Earths Nolans project FID achievement is not simply a company-specific event. It represents a valuation inflection point that institutional investors in critical mineral equities monitor closely. Development-stage assets, where a project exists on paper with geological resources and feasibility studies but no committed funding, trade on a fundamentally different risk basis to construction-stage assets where capital is committed and contractors are being mobilised.

The market's response was instructive: ARU shares rose +6.78% to 31.5 cents on the announcement, against a market capitalisation of approximately A$1.38 billion, reflecting the market's recognition that a meaningful de-risking event had occurred.

The Demonstration Effect for Australian Critical Mineral Development

Perhaps the most underappreciated dimension of the Nolans FID is its potential role as a proof-of-concept for the broader Australian critical mineral development pipeline. The multi-sovereign financing architecture assembled for Nolans — combining domestic government financial institutions, allied nation sovereign funds, and private sector offtake partners — has not previously been deployed at this scale for an Australian rare earth project.

If this model is executed successfully through to first production, it creates a replicable template. Other advanced-stage Australian critical mineral projects seeking to build similar financing structures now have a working precedent to reference, potentially lowering the institutional friction involved in assembling comparable capital stacks for future projects.

The patient, multi-year partnership-building strategy that preceded the Nolans FID — described by the company's board as deliberate and disciplined — reflects a broader strategic reality in large-scale critical mineral development: the relationships that underpin a viable financing structure take years to build, and cannot be shortcut by technical excellence alone.

This article is intended for informational purposes only and does not constitute financial advice. All forecasts, timelines, and demand projections referenced involve inherent uncertainty. Readers are encouraged to conduct independent research and consult a qualified financial adviser before making investment decisions. Past share price performance is not indicative of future results.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths and over 30 other commodities — turning complex data into clear, actionable opportunities for both traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.