May 12, 2026

Europe's Aluminum Supply Crisis Is Three Decades in the Making

The global metals industry operates on long cycles, and few structural imbalances illustrate this better than Europe's primary aluminum deficit. While demand for the metal has grown steadily across electric vehicles, renewable energy hardware, and advanced manufacturing, the supply side of the European equation has quietly hollowed out. Energy cost pressures, carbon pricing mechanisms, and the absence of new greenfield investment have collectively removed productive capacity faster than it has been replaced. The result is a continent that consumes aluminum at scale but increasingly relies on imports to fill the gap left by decades of underinvestment.

It is within this context that the Arctial aluminum plant in Finland has emerged as one of the most strategically significant industrial proposals in European metals in a generation. The project is not simply a new smelter. It represents a test of whether large-scale, low-carbon primary aluminum production is commercially viable in Europe at a moment when the economic and political arguments for domestic supply have rarely been stronger.

When big ASX news breaks, our subscribers know first

What Is the Arctial Project and Why Is Scale Important?

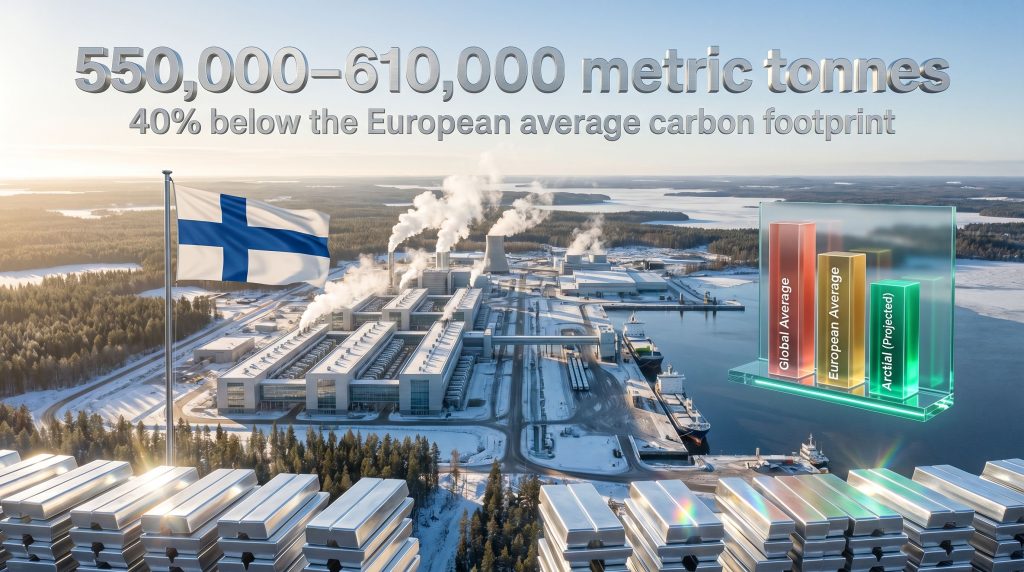

The Arctial facility is a proposed primary aluminum smelter planned for the municipalities of Kokkola and Kronoby in northern Finland. At a planned annual production capacity of 610,000 metric tonnes, confirmed by Arctial's chief commercial officer Maxime Vandersmissen at the CRU World Aluminium Conference in London in May 2026, the project would rank among the largest greenfield aluminum investments in European history.

Continental Europe has not seen a new primary aluminum smelter commissioned in over three decades. This is not a minor footnote. Smelting capacity represents the foundation of the aluminum supply chain, converting alumina into metal that downstream manufacturers can actually use. Without primary production, furthermore, European industry becomes dependent on imported metal, exposing manufacturers to currency risk, geopolitical disruption, and carbon-intensive supply chains that increasingly conflict with regulatory obligations.

The Arctial project is structured as a direct response to this structural vulnerability. Key project parameters include:

- Production capacity: 610,000 metric tonnes per year

- Location: Kokkola and Kronoby, northern Finland

- Target first production: Second half of 2029

- FID assumption: Final Investment Decision in 2027

- Current phase: Feasibility study covering social, technical, environmental, and commercial dimensions (commenced early 2025)

Why Primary Aluminum Matters Differently from Secondary

A critical distinction often overlooked in industry commentary is the difference between primary and secondary (recycled) aluminum. Secondary aluminum, produced by remelting scrap, requires only around 5% of the energy needed for primary production. However, recycled content cannot meet the full specification requirements of high-performance applications, particularly in aerospace, certain automotive structural components, and high-purity electrical conductors.

Primary production is irreplaceable for these end uses, which means Europe's primary capacity deficit is not simply addressable through recycling expansion. In this context, Europe's supply chain challenge becomes especially acute, and the Arctial project specifically targets this structural gap.

The Low-Carbon Architecture Behind the Proposal

The aluminum smelting industry faces a carbon intensity problem that is fundamental rather than incidental. The dominant production process, the Hall-Heroult electrolytic reduction method, is inherently electricity-intensive, consuming roughly 13 to 15 megawatt-hours of electricity per metric tonne of aluminum produced depending on technology generation and operational efficiency. When that electricity comes from fossil fuel grids, the carbon consequences are severe. Industry estimates suggest primary aluminum production contributes approximately 2% of global CO₂ emissions, a figure that sits disproportionately high relative to the metal's share of industrial output.

Arctial's proposed emissions performance targets a carbon footprint approximately 40% below the European average for primary aluminum production and potentially up to 75% below the global average, according to the project's published parameters. These figures depend on two interconnected factors:

-

Electricity source: Finland's grid is characterised by a high proportion of nuclear and renewable generation, providing a structurally low carbon intensity that most European locations cannot replicate. This grid profile, rather than any project-specific arrangement, is what makes the low-carbon production claim credible from a foundational standpoint.

-

Smelting technology: The facility will deploy Rio Tinto's AP60 technology, a next-generation electrolytic reduction process designed to deliver higher energy efficiency per tonne of aluminum compared to older Hall-Heroult cell designs.

Investors and industry observers should note that the carbon intensity figures cited by Arctial are forward-looking projections based on proposed technology and grid assumptions. Independent verification of these figures against standardised measurement frameworks, including scope boundaries and allocation methodologies, has not been publicly confirmed in the materials available at the time of writing.

AP60 Technology: What Sets It Apart?

Rio Tinto's AP60 smelting technology represents the company's most advanced commercial deployment of the Hall-Heroult process. The AP60 designation refers to a cell amperage class, with higher amperage enabling greater productivity per cell while simultaneously achieving better energy efficiency ratios when operating conditions are optimised.

The practical implications for the Arctial aluminum plant in Finland include:

- Higher throughput per cell: Reducing the number of cells required for a given production target, which affects capital cost and facility footprint

- Lower kWh per tonne: Improving the operational carbon intensity calculation relative to older cell technology

- Operational maturity: AP60 technology has been deployed in Rio Tinto's own operations, providing verified performance data rather than theoretical projections based on pilot-scale testing

- Reduced process variability: More consistent cell performance reduces off-spec production and improves metal quality consistency

Critically, the combination of AP60 technology and Finland's clean electricity grid is what gives Arctial's low-carbon claims structural credibility. Either factor in isolation would be insufficient. AP60 running on a coal-heavy grid would still produce relatively high-carbon aluminum. Conversely, even older cell technology powered by clean Finnish electricity would outperform the European average. The two factors working together is what places Arctial's projected output in the same carbon intensity tier as Scandinavian hydropower-based producers, currently the global benchmark for low-carbon primary aluminum.

The Consortium Structure and What Each Partner Contributes

The project's industrial partnership structure is unusually broad for a greenfield smelter, spanning technology, energy, automation, logistics, and financial structuring. This breadth signals that the feasibility study is being conducted with institutional rigour across multiple dimensions simultaneously. ABB's involvement in the project, for instance, underscores the level of industrial credibility behind this proposal.

| Partner | Primary Contribution |

|---|---|

| Rio Tinto | AP60 smelting technology and process know-how |

| Fortum | Long-term clean electricity sourcing and energy partnership |

| ABB | Electrification and automation feasibility assessment |

| Mitsubishi Corporation | Feasibility study support and global commodity expertise |

| Siemens Financial Services | Financial structuring for pre-FID phase |

| Tesi | Investment support and financial structuring |

| Vargas | Financial structuring participation |

Fortum's role as the energy partner is particularly consequential. Aluminum smelters are among the largest single industrial electricity consumers in any grid they connect to. The Arctial facility is expected to require approximately 7 terawatt-hours of electricity annually, a load that represents a significant share of Finnish industrial electricity consumption. Structuring long-term power purchase agreements that lock in both price stability and renewable energy certification is therefore not a peripheral task. It is central to whether the project's economic model holds together across its operational life.

Fingrid, Finland's national transmission system operator, has signed a Letter of Intent confirming the technical feasibility of a grid connection capable of supporting this energy demand. This confirmation is a necessary precondition for the feasibility study to proceed meaningfully, as grid connection failure would represent an insurmountable obstacle at any stage.

Finland's Locational Advantages Are Not Coincidental

The choice of Kokkola and Kronoby is not arbitrary. The location combines several structural advantages that are difficult to replicate elsewhere in Europe:

- Electricity grid quality: Finland's electricity mix provides a foundational carbon advantage for any large industrial consumer

- Port infrastructure: The Kokkola port provides established export logistics capability, which is essential for a facility producing at 610,000 tonnes per year

- Industrial heritage: The Kokkola region hosts an established industrial base with relevant chemical, metallurgical, and energy sector experience, reducing workforce development risk

- Grid connection feasibility: The Fingrid LOI provides documented confirmation that the energy infrastructure requirement is technically addressable

- European logistics positioning: Northern Finland offers reasonable connectivity to Central European manufacturing hubs that would be the primary consumers of domestically produced aluminum

In addition, the broader context of European raw materials supply reinforces why Finland's attributes make it a compelling host for this type of strategic industrial investment.

The next major ASX story will hit our subscribers first

Timeline, Critical Path, and the FID Decision

The production timeline is straightforward in structure but demanding in execution. With a 2027 FID assumption and an H2 2029 first production target, the implied construction period is approximately 24 months. For context, large-scale greenfield smelter construction typically requires between 24 and 36 months from financial close to first hot metal, depending on site preparation complexity, equipment procurement lead times, and the parallelisation of permitting, procurement, and civil works.

The 24-month window is achievable but leaves limited contingency. Key dependencies include:

- Completion of the feasibility study to a standard sufficient to support FID

- Resolution of permitting and environmental assessment requirements within Finnish regulatory frameworks

- Financing close across the consortium and any project finance structures

- Major equipment procurement, particularly electrolytic cell components with long lead times

- Civil construction and infrastructure completion

- Commissioning and pre-production testing phases

Any delay to the FID beyond 2027 would mathematically push first production beyond H2 2029, likely into 2030. The current timeline is achievable but requires concurrent execution across multiple workstreams with minimal slippage.

Carbon Border Adjustment Mechanisms and the Competitive Premium

One dimension of the Arctial aluminum plant in Finland that receives insufficient attention is the emerging premium attached to low-carbon aluminum under evolving European trade policy. The EU's Carbon Border Adjustment Mechanism imposes a carbon cost on high-carbon imports, effectively levelling the playing field between domestically produced low-carbon material and cheaper but more emissions-intensive imports.

For Arctial, the projected carbon intensity of its output could qualify for a meaningful pricing premium relative to aluminum imported from regions with coal-heavy electricity grids. This is not a speculative benefit. It is a direct consequence of how CBAM is structured, and it strengthens the commercial case for the investment in ways that go beyond simple production cost comparisons. As CBAM coverage expands and carbon prices evolve, the value of a verified low-carbon origin certificate on primary aluminum is expected to grow. Furthermore, the recent debate over aluminum and steel tariffs adds another layer of urgency to securing reliable, low-carbon domestic supply.

The Broader Market Signal

The Arctial project's significance extends beyond the facility itself. European aluminum smelter capacity has contracted meaningfully over the past decade, driven primarily by high electricity costs and the structural disadvantage facing conventional smelters under carbon pricing regimes. A successful Arctial project would represent empirical proof that greenfield, low-carbon primary aluminum production is commercially viable in Europe at scale.

This proof-of-concept value could catalyse further investment in European metals infrastructure, including wire rod and casthouse investment, particularly as CBAM creates lasting structural differentiation between low and high-carbon supply sources. Consequently, the ripple effects across the broader aluminium value chain could be considerable.

Economic and Employment Dimensions for Finland

A facility of this scale carries substantial regional economic consequences. While specific employment projections from the feasibility study have not been publicly quantified at the time of writing, primary aluminum smelters of comparable scale typically generate significant direct employment during both construction and operations phases, with multiplier effects extending through supply chain, maintenance, and supporting services.

For Finland, the broader implications extend to export revenues, municipal and national tax contributions, and the positioning of the country as the leading low-carbon aluminum producer in continental Europe. The downstream benefit for European manufacturers, particularly those in automotive and clean energy sectors seeking to reduce the embedded carbon in their own supply chains, is also material. Proximate access to verified low-carbon primary aluminum eliminates both the logistics cost and the carbon accounting burden associated with long-distance imports.

Key Risk Factors for the Project's Commercial Case

No pre-FID project of this scale is without material execution risk. Investors and industry participants tracking the Arctial aluminum plant in Finland should monitor the following variables closely, as even experienced global aluminium producers face comparable challenges on projects of this magnitude:

- FID timing: A 2027 decision remains an assumption, not a confirmed outcome. The feasibility study must support an affirmative decision across all dimensions

- Energy cost structure: Long-term electricity pricing stability in Finland is essential to the operational economic model

- Aluminum market conditions: The project's returns are sensitive to global primary aluminum prices, which are influenced by Chinese production levels, energy costs globally, and demand growth in key end markets

- CBAM implementation pace: The commercial premium from low-carbon credentials depends on the robustness and expansion of carbon border adjustment mechanisms over time

- Permitting and community engagement: Finnish environmental and social permitting processes must be completed within timeframes compatible with the construction schedule

- Equipment procurement: Long lead times for key electrolytic components could create critical path risks if procurement is not initiated well in advance of FID

This article contains forward-looking statements based on publicly announced project parameters and industry analysis. The Arctial project remains in the feasibility study phase as of May 2026. FID has not been taken, and production outcomes are contingent on multiple factors that remain subject to change. This content does not constitute financial or investment advice.

Want To Stay Ahead of Europe's Next Major Metals Opportunity?

As structural deficits reshape European aluminium supply and low-carbon production premiums grow, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — from aluminium to critical metals — so subscribers can act on actionable opportunities before the broader market. Explore how historic discoveries have generated exceptional returns on Discovery Alert's discoveries page, then start your 14-day free trial to secure your market-leading edge.