July 21, 2026

Arctic Resource Development: Why Greenland's Rare Earth Potential Remains Locked

Arctic mining ventures face extraordinary operational hurdles that extend far beyond conventional mineral extraction challenges. Despite possessing vast rare earth deposits, Greenland represents a case study in how geographic isolation, extreme climate conditions, and infrastructure deficits can render substantial mineral wealth economically inaccessible for decades.

When big ASX news breaks, our subscribers know first

Geographic Isolation Creates Fundamental Development Barriers

Greenland's geographic constraints create unprecedented logistical challenges for rare earth mining operations. Only southwestern ports operate year-round, with Nuuk serving as the sole facility equipped with modern port infrastructure capable of supporting large-scale mineral transport operations.

This geographic reality forces mining companies into a self-sufficiency model unknown in established mining jurisdictions. Unlike Australia, Canada, or the United States, where existing transport networks connect mining sites to global markets, Greenland projects must construct proprietary logistics systems from inception.

The island's vast distances between potential mining sites and port facilities compound transportation costs significantly. Mining operations must establish dedicated transport corridors across terrain that remains inaccessible for substantial portions of each year due to weather conditions.

Climate-Driven Operational Constraints in Polar Mining

Greenland rare earth mining challenges intensify due to extreme Arctic conditions that create operational windows unknown in temperate mining regions. High snowfall, sub-zero temperatures, and dramatically shortened daylight hours during winter months reduce the effective mining season and increase equipment maintenance requirements.

Regular weather disruptions limit site access unpredictably, creating production scheduling uncertainties that complicate project financing and operational planning. Equipment failure rates increase substantially in polar conditions, requiring specialized cold-weather adaptations and redundant systems that multiply capital expenditure requirements.

The shortened daylight period during Arctic winters reduces productive surface mining hours, affecting annual production capacity calculations. Surface operations become particularly challenging when daylight availability drops to minimal levels, forcing operations to rely heavily on artificial lighting systems that increase energy consumption.

Infrastructure Investment Requirements vs. Global Alternatives

Greenland's critical minerals infrastructure deficit creates capital requirement multipliers that fundamentally alter project economics compared to established mining jurisdictions. Projects must develop proprietary energy generation, as grid connectivity remains unavailable across potential mining regions.

Energy infrastructure development requires complete self-sufficiency through renewable or conventional generation systems designed to operate reliably in Arctic conditions. This necessity adds hundreds of millions of dollars to project development costs before mineral extraction commences.

As David Riley, Senior Research Analyst at Wood Mackenzie, noted in January 2026, Greenland projects face significant infrastructure challenges that must compete for investment with countries such as Canada, Australia, and the US that have more developed infrastructure and established mining sectors. The lack of infrastructure, low labor pool, and high capital requirements represent the main barriers to development, expected to remain major limiting factors regardless of Greenland's political status.

What Makes Greenland's Rare Earth Deposits Strategically Significant?

Strategic mineral security has become a critical concern for Western economies seeking to reduce dependency on concentrated supply chains. Greenland's undeveloped rare earth potential represents a significant opportunity for supply diversification, despite the substantial development challenges that have prevented commercial production to date.

Critical Mineral Reserves Ranking in Global Context

The European Commission estimates that Greenland possesses the geological capacity to produce 27 of the 34 minerals classified as critical under the EU's Critical Raw Materials Act. This classification positions Greenland as potentially one of the world's most comprehensive critical mineral provinces, rivaling established producers in terms of resource diversity.

Current global rare earth production remains heavily concentrated, with China controlling approximately 61% of global rare earth element production and 90% of global processing capacity. This concentration creates strategic vulnerabilities for economies dependent on rare earth supply chains, particularly in high-technology manufacturing sectors.

Greenland's resource base offers potential strategic value through geographic diversification from Asian supply sources. However, the absence of operational mines means this potential remains theoretical until infrastructure and regulatory barriers can be overcome.

Heavy Rare Earth Concentration Advantages

While specific heavy rare earth percentages within Greenland's deposits require further geological assessment, the strategic importance of heavy rare earth elements (HREEs) in advanced technology applications makes any significant HREE concentration valuable for supply chain diversification efforts.

Heavy rare earth elements command premium pricing due to their critical applications in high-performance permanent magnets, advanced electronics, and renewable energy systems. Projects capable of producing meaningful HREE quantities gain economic advantages over light rare earth-focused operations.

Geological surveys of Greenland's major deposits suggest varying rare earth concentrations, with the Gronnedal deposit showing 0.63% REO concentration and the Motzfeldt deposit containing 0.260% total rare earth oxides (TREO). These grade levels require detailed metallurgical assessment to determine HREE content and extraction feasibility.

Geopolitical Supply Chain Diversification Value

Rare earth elements serve as critical inputs across modern manufacturing value chains, particularly in smartphone production, solar panel manufacturing, and high-powered magnet applications. Any significant disruption to rare earth supply chains creates cascading impacts across multiple industries simultaneously.

Rising geopolitical tensions have accelerated Western efforts to establish alternative supply sources outside Chinese control. Memoranda of Understanding established between Greenland and the United States in 2019, alongside the 2023 partnership on sustainable raw materials with the European Union, demonstrate strategic interest in Greenland's mineral potential.

However, Chinese capital participation in Greenland projects creates strategic complexity. Energy Transition Minerals, operator of the Kvanefjeld project, maintains 6.5% Chinese ownership through Shenghe Resources Holding Co., illustrating how global supply diversification efforts encounter Chinese investment presence even in alternative supply development projects.

How Do Regulatory Frameworks Impact Mining Development Timelines?

Regulatory uncertainty represents a primary impediment to Greenland rare earth mining development, creating investment hesitation across projects spanning multiple political cycles. Policy shifts, uranium content restrictions, and evolving environmental standards generate project timeline extensions that compound capital cost requirements.

Uranium Co-occurrence Restrictions and Policy Evolution

Greenland established a 100 parts per million (ppm) uranium limit for mining operations in 2021, creating immediate regulatory compliance challenges for existing projects. The Kvanefjeld project, containing uranium concentrations exceeding 300 ppm, faces regulatory barriers that prevent operational advancement under current policy frameworks.

December 2021 marked a significant policy shift when Greenland's Parliament formally banned uranium exploration and exploitation activities. This prohibition affects multiple rare earth projects where uranium occurs as a natural co-product within rare earth-bearing ore bodies.

The uranium regulatory threshold operates as a strict compliance boundary requiring technical solutions or policy modifications for affected projects. Potential resolution pathways include:

• Uranium extraction and separate processing protocols

• Specialised waste management systems for uranium-bearing materials

• Policy threshold modifications through legislative processes

• Alternative deposit development focusing on low-uranium ore bodies

Environmental Standards Under the Mineral Resources Strategy 2025-2029

Greenland's current Mineral Resources Strategy emphasises sustainability and high environmental standards as foundational requirements for mining project approval. This policy orientation prioritises environmental protection over rapid resource extraction, potentially extending permitting timelines and operational compliance requirements.

The strategy framework requires comprehensive environmental impact assessments that address Arctic ecosystem protection, marine environment preservation, and long-term environmental monitoring protocols. These requirements add regulatory complexity but align with international best practices for Arctic resource development.

Environmental standard implementation creates additional compliance costs and timeline extensions compared to jurisdictions with established regulatory frameworks. However, these standards may provide greater long-term project security through reduced environmental opposition and improved community acceptance.

Indigenous Rights and Community Consultation Requirements

Political developments reflect Indigenous community influence on Greenland's mining policy direction. The Inuit Ataqatigiit party won the highest number of legislative seats in 2021 on a platform opposing the Kvanefjeld project, demonstrating community scepticism toward large-scale mining development.

While the Democrats became the largest political party in 2025 supporting private-sector resource use, the current Minister of Industry, Raw Materials, Mining and Energy maintains connections to Inuit Ataqatigiit, creating ongoing policy uncertainty for mining project advancement.

This political dynamic suggests that community consultation requirements likely extend beyond standard regulatory processes, requiring sustained engagement and community benefit agreement negotiations that can span multiple years before project approval.

The next major ASX story will hit our subscribers first

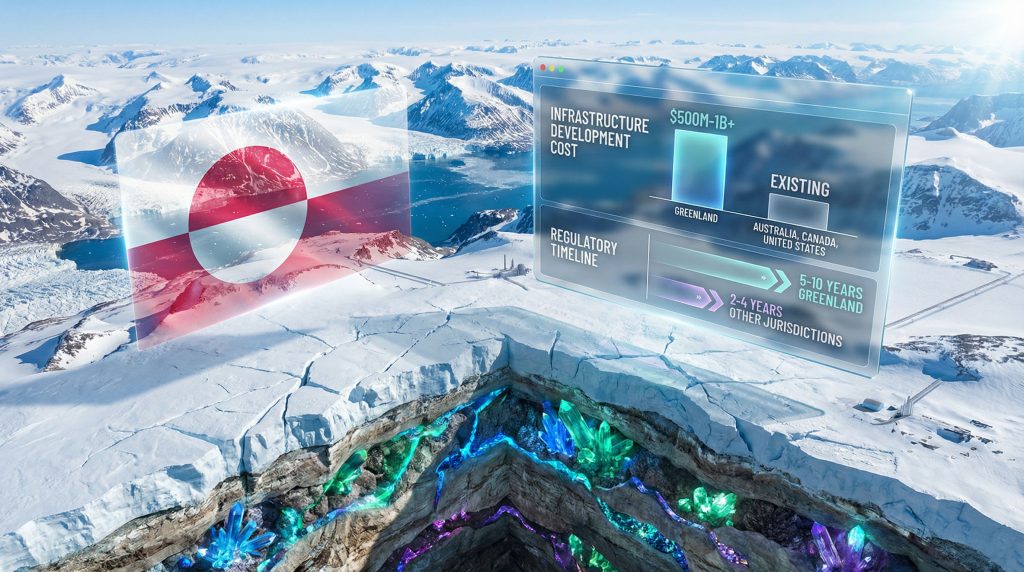

Capital Investment Scenarios: Comparing Development Pathways

Infrastructure-driven capital requirements fundamentally differentiate Greenland mining projects from established jurisdictions, creating investment scenarios that require complete foundational development before mineral extraction commences.

| Factor | Greenland | Australia | Canada | United States |

|---|---|---|---|---|

| Infrastructure Development | $500M-1B+ | Existing | Existing | Existing |

| Energy Generation | Self-sufficient required | Grid connected | Grid connected | Grid connected |

| Skilled Labour Pool | Import required | Domestic available | Domestic available | Domestic available |

| Regulatory Timeline | 5-10 years | 2-4 years | 3-5 years | 2-4 years |

| Transport Logistics | Year-round limitations | Established networks | Established networks | Established networks |

Energy Infrastructure Self-Sufficiency Requirements

Greenland mining operations must achieve complete energy independence through proprietary power generation systems designed for Arctic conditions. Grid connectivity remains unavailable across potential mining regions, forcing projects to construct dedicated power plants capable of supporting both mining operations and associated infrastructure.

Renewable energy integration offers potential cost advantages and environmental benefits but requires substantial initial investment in wind, solar, or hydroelectric systems adapted for Arctic performance. Energy storage systems become critical for maintaining operational continuity during extreme weather events or seasonal energy production variations.

Energy infrastructure costs represent a significant portion of total project capital requirements, potentially adding $200-400 million to development costs depending on operational scale and energy source selection. These costs occur before revenue generation begins, creating extended payback periods compared to grid-connected operations.

Skilled Labour Import Costs and Logistics

Greenland's limited domestic population and underdeveloped mining sector necessitate importing specialised mining professionals from established mining regions. Unlike jurisdictions with trained local workforces, all technical expertise must be recruited internationally, creating sustained employment cost premiums.

Worker rotation systems require accommodation facilities, transportation logistics, and premium compensation packages to attract qualified personnel to remote Arctic locations. These costs compound annually throughout project operational life, unlike one-time infrastructure investments.

International labour recruitment creates workforce management complexity through visa requirements, rotation scheduling, and cultural integration challenges. Projects must maintain redundant staffing levels to account for weather-related access disruptions and higher turnover rates typical in remote location assignments.

Port Development and Year-Round Access Challenges

Limited port infrastructure restricts mineral transport options and requires significant investment in specialised Arctic shipping facilities. Only Nuuk possesses modern port infrastructure, while other coastal locations require complete development from inception.

Year-round shipping access remains challenging even from developed ports due to sea ice conditions and extreme weather events that can prevent ship access for extended periods. This limitation affects both inbound supply deliveries and outbound mineral concentrate shipments.

Port development costs vary substantially based on location selection, water depth requirements, and ice-breaking facility needs. Dedicated mineral loading facilities add additional costs but provide operational efficiency advantages for large-scale production operations.

Current Project Status Analysis: From Exploration to Production Delays

Greenland's rare earth projects demonstrate how regulatory barriers, financing constraints, and infrastructure requirements create development timelines spanning decades rather than years typical in established mining jurisdictions.

The Kvanefjeld project, initiated in 2007, exemplifies the extended development cycles facing Greenland's rare earth sector. Despite nearly two decades of planning, regulatory challenges and uranium content restrictions have prevented operational status.

Tanbreez Project Development Trajectory and US Export-Import Bank Financing

Critical Metals' Tanbreez project received a US$120 million Letter of Interest from the US Export-Import Bank, representing significant government-backed financing for Greenland rare earth development. This financing mechanism indicates US strategic interest in supply chain diversification through government-supported development programmes.

The mid-2026 pilot facility timeline reflects extended development cycles characteristic of Greenland projects. Pilot facilities typically precede full-scale commercial production by several additional years, suggesting commercial production timelines extending well into the 2030s.

US Export-Import Bank financing provides competitive advantages through government backing, but project success remains dependent on resolving infrastructure challenges and regulatory compliance requirements that affect all Greenland mining ventures.

Kvanefjeld Legal Challenges and Uranium Content Resolution Strategies

Energy Transition Minerals' Kvanefjeld project faced legal challenges beginning in early 2022, centred on uranium content exceeding regulatory thresholds established in 2021. The project's 300+ ppm uranium concentration violates the 100 ppm regulatory limit, creating fundamental compliance barriers.

Original project planning targeted 30 kilotonnes of rare earth oxide (REO) production annually, representing substantial production capacity if regulatory and infrastructure barriers can be resolved. However, the 19-year development timeline from 2007 initiation illustrates systemic challenges affecting Greenland mining development.

Chinese investment through Shenghe Resources Holding Co.'s 6.5% ownership stake adds geopolitical complexity to resolution strategies. While Western nations pursue supply diversification from China, Chinese capital participation in Greenland projects creates strategic ambiguity regarding ultimate project control and benefit distribution.

Early-Stage Exploration Projects: Sarfartoq and Motzfeldt Prospects

Neo Performance Materials' Sarfartoq project remains in early-stage exploration, representing the earliest development phase among Greenland's rare earth pipeline. Early-stage status indicates potential commercial production timelines extending beyond 2035, assuming successful development progression.

Stallion Resources' Motzfeldt project completed exploratory drilling, revealing 0.260% total rare earth oxides (TREO) concentration. While this grade level requires detailed metallurgical assessment for economic viability, it demonstrates additional resource potential beyond the more advanced Kvanefjeld and Tanbreez projects.

The Gronnedal deposit shows 0.63% REO concentration, indicating higher grade potential but uncertain development status. Multiple early-stage projects suggest substantial resource potential but highlight the extended timelines required for project advancement in Greenland's challenging development environment.

Environmental Risk Assessment in Arctic Mining Operations

Arctic mining operations face unique environmental challenges that require specialised risk management approaches unknown in temperate mining regions. Permafrost interactions, marine ecosystem protection, and radioactive material management create complex environmental compliance requirements.

Permafrost Stability and Mining Infrastructure Interactions

Permafrost degradation poses significant risks to mining infrastructure stability in Arctic regions. Underground mining operations and surface processing facilities must account for permafrost behaviour changes resulting from thermal disturbance and climate warming trends.

Foundation systems require specialised engineering to maintain structural integrity across freeze-thaw cycles and potential permafrost degradation. Infrastructure failure risks increase substantially when permafrost stability becomes compromised through mining activities or climate change impacts.

Tailings storage facilities face particular challenges in permafrost environments, where containment system integrity depends on maintaining frozen ground conditions. Long-term environmental liability concerns increase when permafrost stability cannot be guaranteed across mine operational lifecycles.

Marine Ecosystem Protection During Mineral Processing

Greenland's coastal mining operations require stringent marine environment protection protocols due to sensitive Arctic marine ecosystems and indigenous community dependence on marine resources. Processing waste management becomes critical when operations locate near coastal waters.

Marine discharge regulations likely exceed standards in temperate regions, requiring advanced water treatment systems and monitoring protocols. Arctic marine environments show reduced capacity for contaminant dilution and slower ecosystem recovery rates compared to temperate marine systems.

Seasonal sea ice coverage affects waste management strategies and emergency response capabilities. Operations must maintain environmental compliance across varying seasonal conditions that affect marine ecosystem vulnerability periods.

Radioactive Waste Management in Polar Environments

Uranium-bearing rare earth deposits require specialised radioactive waste management protocols adapted for Arctic conditions. Traditional waste management approaches may require modification for permafrost environments and limited transport infrastructure.

Long-term storage solutions must account for permafrost stability, seismic activity, and potential climate change impacts on storage system integrity. Radioactive waste transport faces additional challenges due to limited infrastructure and weather-dependent access conditions.

Regulatory frameworks for radioactive waste management in Arctic environments remain underdeveloped compared to established nuclear industry protocols, creating compliance uncertainty for projects containing uranium co-products.

Market Dynamics: China Dependency vs. Alternative Supply Development

Global rare earth market dynamics create both opportunities and challenges for Greenland's potential rare earth production. Chinese market dominance generates demand for alternative supplies while creating competitive pressures that affect project economics and strategic positioning.

Global Supply Chain Concentration Risks

Current rare earth supply chain concentration in China creates strategic vulnerabilities for technology-dependent economies. Manufacturing disruptions in smartphones, electric vehicles, and renewable energy systems could result from supply chain interruptions affecting rare earth availability.

Supply diversification efforts face economic challenges when alternative sources require substantially higher development costs than established Chinese operations. Greenland projects must compete economically while providing strategic supply security benefits that justify higher production costs.

Furthermore, uranium market trends demonstrate cyclical behaviour influenced by Chinese production policies, technology demand changes, and geopolitical tensions affecting trade relationships.

Processing Capability Development Requirements

Rare earth mining represents only the initial stage in complex processing value chains required for end-user applications. Raw rare earth concentrates require sophisticated separation and refining processes currently concentrated in Chinese facilities.

Alternative processing capacity development faces substantial capital requirements and technical expertise constraints. Processing facility construction requires specialised knowledge and equipment primarily available through Chinese suppliers, creating strategic dependencies even in alternative supply development efforts.

Integrated mining and processing operations offer strategic advantages but multiply capital requirements and technical complexity. Greenland projects must evaluate whether to focus on concentrate production or pursue vertical integration through processing capability development.

Strategic Mineral Security Implications for Western Economies

National security considerations increasingly influence rare earth supply development policies across Western nations. Government financing support, trade policy measures, and strategic stockpiling programmes reflect growing recognition of rare earth supply security importance.

Military and aerospace applications of rare earth elements create particular security concerns when supply sources remain concentrated in geopolitically unstable regions. Defense supply chain requirements may justify higher costs for secure supply sources.

Additionally, critical minerals policies including the 2019 US-Greenland MoU and 2023 EU partnership, demonstrate coordinated efforts to support alternative supply development through government backing and policy coordination mechanisms.

Technology Solutions for Extreme Environment Mining

Advanced mining technologies offer potential solutions for overcoming Greenland's operational challenges, though implementation requires adaptation for Arctic conditions and higher capital investment than conventional mining approaches.

Cold Weather Equipment Adaptations and Maintenance Protocols

Mining equipment requires extensive cold weather modifications to maintain operational reliability in Arctic conditions. Standard mining machinery faces component failure risks, reduced efficiency, and shortened operational life when exposed to extreme cold without proper adaptation.

Hydraulic systems, electronic components, and mechanical systems require specialised cold-weather formulations and protection systems. Equipment heating systems add energy consumption costs while preventing operational failures during extreme cold periods.

Maintenance protocols must account for reduced component life cycles, increased failure rates, and limited equipment replacement availability. Redundant equipment systems become necessary to maintain production continuity when primary systems fail due to extreme weather conditions.

Remote Operation Technologies and Automation Potential

Remote mining technologies offer potential solutions for reducing on-site personnel requirements and improving operational safety in extreme Arctic conditions. However, automated mining technologies can maintain production during weather events that prevent human site access.

Satellite communication systems enable remote monitoring and control capabilities, though Arctic communication infrastructure requires specialised satellite coverage and backup systems. Remote operation centres can be located in temperate regions while controlling Arctic mining operations.

However, remote operation technologies require substantial initial investment and ongoing technical support that may not be economically justified for smaller-scale operations. Technology implementation must balance automation benefits against capital cost increases and technical complexity.

Renewable Energy Integration in Off-Grid Mining Operations

Renewable energy systems offer long-term operational cost advantages and environmental benefits for Greenland mining operations, though initial capital requirements exceed conventional power generation systems.

Wind energy systems designed for Arctic conditions can provide substantial power generation capacity, though ice formation and extreme weather events require robust system design and maintenance protocols. Wind energy consistency varies seasonally, requiring energy storage integration.

Hydroelectric potential exists in certain Greenland regions, offering reliable baseload power generation for mining operations. However, hydroelectric development requires substantial environmental assessment and infrastructure investment in dam construction and power transmission systems.

Solar energy integration faces challenges due to limited daylight hours during winter months, though summer solar resources can provide substantial power generation capacity. Battery storage systems become essential for maintaining power availability during extended periods of limited solar generation.

Economic Feasibility Models Under Different Scenarios

Economic modelling for Greenland rare earth projects requires scenario analysis accounting for commodity price volatility, infrastructure cost variations, and regulatory timeline uncertainties that affect project returns and financing requirements.

Commodity Price Thresholds for Project Viability

Greenland rare earth projects require higher commodity prices than established jurisdictions due to infrastructure development costs and operational challenges. Break-even analysis must account for capital cost recovery across extended development timelines.

Rare earth price volatility creates financing challenges when project economics depend on sustained high prices for economic viability. Long-term price forecasting becomes critical for project financing decisions but faces substantial uncertainty due to market manipulation potential and demand volatility.

Heavy rare earth elements command premium pricing that can improve project economics, though production forecasts require detailed metallurgical assessment to determine actual HREE recovery rates from Greenland deposits.

Government Incentive Programmes and International Partnerships

Government financing support through export credit agencies, development banks, and strategic partnership programmes can substantially improve project economics by reducing financing costs and providing political risk insurance.

The US Export-Import Bank's $120 million Letter of Interest for the Tanbreez project demonstrates government financing availability for strategic mineral projects. Similar programmes may become available through other Western nations pursuing supply diversification objectives.

International partnership agreements can provide market access guarantees, technical expertise sharing, and coordinated policy support that reduces project risks and improves financing availability. However, government support programmes often include policy requirements that may affect operational flexibility.

Break-Even Analysis for Infrastructure-Heavy Developments

Infrastructure-heavy developments require extended payback periods and higher production volumes to achieve acceptable returns on investment. Break-even analysis must account for infrastructure depreciation across project operational lifecycles.

Shared infrastructure development among multiple projects can reduce individual project costs but requires coordination among different operators and synchronised development timelines. Infrastructure sharing agreements create additional complexity but offer potential cost advantages.

Financing structures must account for extended development timelines and higher capital requirements compared to conventional mining projects. Project finance terms may require government backing or strategic partner participation to achieve acceptable risk-adjusted returns.

Future Outlook: Timeline Projections for Commercial Production

Commercial rare earth production in Greenland faces timeline projections extending well into the 2030s under optimistic scenarios, with realistic assessments suggesting potential delays extending into the 2040s for large-scale production capacity.

Political Stability Requirements for Long-Term Investment

Mining project development requires political stability across 10-20 year investment horizons, creating particular challenges in Greenland's evolving political landscape. Recent political shifts demonstrate how mining policy can change substantially across electoral cycles.

The transition from Inuit Ataqatigiit anti-mining positions to Democrats pro-development policies illustrates political volatility that affects investor confidence. However, the current Minister's continued Inuit Ataqatigiit connections suggest ongoing policy uncertainty.

Greenland's potential political status changes, whether toward independence or US territorial acquisition, create additional uncertainty affecting long-term investment decisions. Political stability requirements may favour smaller-scale development approaches over large capital-intensive projects.

Technology Advancement Impact on Development Economics

Advancing mining technologies, particularly in automation and remote operations, may improve Greenland project economics by reducing labour costs and operational complexity. However, technology adoption requires additional capital investment and technical expertise.

Climate change impacts on Arctic accessibility could improve transportation logistics and extend operational seasons, potentially improving project economics. However, climate change also increases environmental risks and regulatory complexity for Arctic operations.

Processing technology advancement may enable lower-grade deposit development or improve recovery rates from existing deposits, expanding the range of economically viable projects. However, processing technology development occurs primarily in China, creating strategic dependency concerns.

Global Rare Earth Demand Growth Projections Through 2035

Electric vehicle adoption, renewable energy expansion, and advanced electronics demand growth create substantial rare earth demand increases projected through 2035. Demand growth supports higher commodity prices that improve Greenland project economics.

However, recycling technology advancement and rare earth substitution research may reduce demand growth rates or alter specific rare earth element demand patterns. Demand projections face uncertainty from technology development and policy changes affecting end-use sectors.

Supply diversification pressures from Western nations create strategic demand for non-Chinese rare earth sources, potentially supporting premium pricing for alternative supply sources despite higher production costs.

What Environmental Challenges Could Prevent Mining Development?

Greenland rare earth mining challenges extend beyond technical and economic considerations to encompass environmental risks that could permanently restrict development in certain regions. Arctic climate vulnerability and protected ecosystem designations create regulatory barriers that could override economic considerations.

The potential for marine ecosystem disruption through processing waste discharge creates long-term liability risks, particularly when operations affect indigenous communities dependent on marine resources. Radioactive waste management requirements add complexity when uranium co-occurs with rare earth deposits.

Environmental opposition from international conservation organisations could create pressure for additional protected area designations that restrict mining access. Furthermore, energy transition minerals development faces scrutiny when environmental protection conflicts with supply security objectives.

Climate Change Adaptation Requirements for Arctic Operations

Arctic climate change accelerates infrastructure risks and creates operational uncertainties that affect long-term project viability. Permafrost degradation threatens foundation stability while sea ice reduction affects shipping logistics and coastal infrastructure.

Temperature increase projections for Greenland exceed global averages, creating unprecedented conditions for infrastructure design and environmental impact assessment. Additionally, Arctic environmental challenges require adaptive management strategies that add operational complexity and costs.

Climate adaptation costs represent additional capital requirements beyond standard Arctic construction specifications. Long-term operational planning must account for changing environmental conditions that could affect mine life economics and environmental compliance requirements.

Frequently Asked Questions:

Why hasn't Greenland developed any operational rare earth mines despite significant reserves?

Three interconnected factors prevent development: extreme Arctic conditions requiring complete infrastructure construction, regulatory restrictions on uranium-bearing deposits, and high capital requirements that make projects less competitive than alternatives in established mining jurisdictions.

How do Greenland's development costs compare to other rare earth mining regions?

Greenland projects require $500 million to $1 billion+ in infrastructure development before mining begins, compared to established jurisdictions where existing transport, energy, and port facilities significantly reduce initial capital requirements.

What role does uranium regulation play in Greenland's rare earth development delays?

Greenland's 100 parts per million uranium limit, established in 2021, affects major deposits like Kvanefjeld that contain 300+ ppm uranium, creating regulatory barriers that require waste management solutions or policy modifications for project advancement.

Disclaimer: This analysis involves forecasts and projections based on current market conditions and regulatory frameworks. Rare earth mining investments carry substantial risks including commodity price volatility, regulatory changes, and infrastructure development challenges. Investment decisions should consider comprehensive due diligence and professional financial advice.

Ready to Discover the Next Major Mining Opportunity?

While Arctic mining ventures face significant challenges, major discoveries can still emerge from more accessible jurisdictions across the ASX. Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant mineral discoveries, helping investors identify actionable opportunities before they gain widespread market attention and secure competitive advantages through rapid, data-driven insights.