June 15, 2026

Argentina lithium adds Chinese partner arrangements are fundamentally reshaping South America's critical minerals landscape, as international collaboration becomes essential for navigating complex supply chain demands and capital-intensive development requirements. These partnerships demonstrate how strategic alliances can accelerate project timelines while distributing technical and financial risks across complementary capabilities. Furthermore, the success of these collaborative models signals a broader transformation in global mining operations, where technological expertise and market access often matter more than traditional resource ownership structures.

How Are Chinese Investment Patterns Reshaping Argentina's Critical Minerals Landscape?

Chinese enterprises have fundamentally altered the investment architecture within Argentina's lithium sector through systematic capital deployment strategies that prioritise vertical integration over speculative resource plays. This approach reflects broader supply chain security objectives rather than purely financial returns, creating unique partnership structures that differ markedly from traditional Western mining investment models.

Capital Deployment Strategies in Emerging Lithium Markets

The investment patterns emerging across northwestern Argentina demonstrate sophisticated risk allocation mechanisms between international partners and local operators. Chinese companies typically structure their participation through staged equity arrangements that begin with technical partnerships and evolve into majority ownership positions based on development milestones.

Key investment characteristics include:

• Long-term offtake commitments spanning 10-15 years, providing revenue certainty for project developers

• Technology transfer provisions that accelerate processing capabilities in remote locations

• Infrastructure co-investment in roads, power generation, and water treatment facilities

• Local employment requirements that mandate workforce development programs

Argentina lithium adds Chinese partner arrangements have become increasingly common as foreign direct investment flows into the region reached approximately USD $2.3 billion during 2024-2025, with Chinese entities accounting for roughly 60% of total committed capital. This concentration reflects strategic positioning within global battery supply chains rather than opportunistic resource speculation.

The Salta Province mining corridor has emerged as a focal point for these partnerships, with lithium concentrations in local brines typically ranging from 1,200-1,800 mg/L and favourable magnesium-to-lithium ratios that reduce processing complexity. These geological advantages, combined with Argentina's liberal foreign ownership frameworks, create attractive investment conditions for international partners seeking supply chain diversification.

Regulatory Framework Impact on Cross-Border Mining Ventures

Argentina's mining investment regulations permit up to 100% foreign ownership of mineral concessions, though provincial governments retain authority over specific operational requirements and revenue-sharing arrangements. This regulatory structure enables flexible partnership configurations while maintaining local economic participation.

Provincial jurisdiction dynamics create varying investment conditions across the lithium triangle region:

| Province | Foreign Ownership Limit | Local Partnership Requirement | Revenue Sharing Rate |

|---|---|---|---|

| Salta | 100% permitted | None mandatory | 3-5% provincial royalty |

| Catamarca | 100% permitted | Technical partnerships encouraged | 3-8% graduated royalty |

| Jujuy | 100% permitted | Local employment quotas | 5% provincial royalty |

These frameworks facilitate joint venture formations that typically involve Chinese partners providing capital and technology while Argentine entities contribute local expertise and regulatory navigation. The resulting structures often feature governance arrangements that balance international technical standards with local operational requirements.

However, the US-China trade impact continues to influence investment decisions, with some projects incorporating risk mitigation strategies to address potential supply chain disruptions.

When big ASX news breaks, our subscribers know first

What Financial Models Drive Large-Scale Lithium Project Development?

Contemporary lithium project financing relies on multi-tranche capital structures that distribute risk across development phases while maintaining flexibility for technology adaptation and market volatility. These models have evolved significantly from traditional mining finance approaches, incorporating elements specific to battery material supply chains and processing technology risks.

Staged Investment Architecture Analysis

The capital requirements for lithium project development follow predictable patterns, though specific amounts vary based on deposit characteristics, processing technology selection, and infrastructure availability. Industry data indicates consistent ranges across major development phases:

| Development Stage | Capital Range (USD) | Risk Profile | Timeline | Key Activities |

|---|---|---|---|---|

| Pilot Testing | $8-22 million | High | 15-24 months | Technology validation, permitting |

| Feasibility Studies | $18-40 million | Medium-High | 18-30 months | Resource definition, engineering design |

| Commercial Construction | $120-280 million | Medium | 30-48 months | Plant construction, infrastructure |

| Working Capital | $15-35 million | Low-Medium | Ongoing | Inventory, operations funding |

Risk-adjusted financing mechanisms within these structures typically combine:

• Senior debt facilities (45-65% of project capital) with 7-12 year tenors

• Mezzanine financing providing equity-like returns with debt-level security

• Development equity from project sponsors and strategic partners

• Contingent consideration tied to production milestones and commodity pricing

The Argentina lithium adds Chinese partner financing model demonstrates how international partnerships can optimise capital efficiency through complementary strengths. Chinese entities often provide construction financing and equipment procurement capabilities, while local partners contribute regulatory expertise and operational infrastructure.

Equity Participation Structures in Mining Partnerships

Earn-in mechanisms have become the predominant structure for international lithium partnerships, allowing technical partners to acquire equity positions through staged capital contributions rather than upfront payments. These arrangements align incentives around technical delivery while managing early-stage development risks.

Typical milestone-based ownership progression includes:

Phase 1: Exploration and Resource Definition (24-36 months)

• Partner earns 25-35% equity through $10-25 million investment

• Focus on drilling, resource estimation, and preliminary feasibility

• Performance targets include resource upgrade to indicated/measured categories

Phase 2: Development and Engineering (18-30 months)

• Partner earns additional 15-25% equity through $25-60 million investment

• Completion of bankable feasibility study and major permit approvals

• Technology selection and engineering design finalisation

Phase 3: Construction and Commissioning (30-42 months)

• Partner achieves target ownership of 51-65% through remaining capital contribution

• Project construction, equipment installation, and production startup

• Achievement of nameplate production capacity within specified timeframes

Performance guarantees within these structures typically include:

• Resource estimate accuracy within ±20% variance tolerances

• Processing recovery rates achieving 85-92% lithium extraction efficiency

• Timeline adherence with equity dilution penalties for excessive delays

• Product quality standards meeting battery-grade lithium specifications

Which Direct Lithium Extraction Technologies Are Gaining Commercial Traction?

Direct lithium extraction represents a transformative approach to brine processing that promises significant reductions in water consumption and production timelines compared to traditional evaporation methods. However, commercial deployment remains limited as operators balance technological promise against proven operational reliability.

Technical Innovation in Brine Processing Operations

DLE technology maturity varies significantly across different technical approaches, with most systems remaining in pilot or demonstration phases despite substantial development investment. Industry analysis indicates approximately 20-25 DLE projects globally in various development stages, though fewer than five operations have achieved sustained commercial production.

Water consumption comparisons reveal DLE's primary environmental advantage:

• Traditional evaporation ponds: 600,000-1,200,000 gallons per tonne lithium produced

• Optimised DLE systems: 80,000-250,000 gallons per tonne lithium produced

• Water savings potential: 70-85% reduction in freshwater requirements

Processing timeline advantages represent DLE's operational benefit:

• Traditional methods: 14-20 months from brine extraction to product

• DLE processing: 6-12 weeks from brine to battery-grade lithium

• Production flexibility: Ability to adjust output based on demand fluctuations

Recovery efficiency metrics demonstrate technology performance ranges:

| DLE Technology Type | Recovery Rate | Development Status | Key Advantages | Primary Challenges |

|---|---|---|---|---|

| Sorption-based | 75-85% | Pilot/Demo | High selectivity | Sorbent durability |

| Precipitation | 70-80% | Early commercial | Proven chemistry | Waste management |

| Membrane separation | 72-88% | Laboratory/Pilot | Low chemical use | Membrane fouling |

| Ion exchange | 78-86% | Demonstration | Established technology | Resin regeneration |

The Argentina lithium adds Chinese partner projects increasingly incorporate DLE technology evaluation as standard development protocol, though most operators maintain traditional processing as the primary production method while testing DLE systems in parallel operations.

Furthermore, these partnerships often align with broader critical minerals strategy initiatives that prioritise technological advancement and supply chain security.

Technology Transfer Dynamics in Sino-Argentine Ventures

Intellectual property arrangements within international partnerships create complex frameworks for technology sharing while protecting proprietary innovations. Chinese partners typically provide process equipment and engineering expertise, while Argentine entities contribute geological knowledge and regulatory navigation capabilities.

Technology transfer mechanisms commonly include:

• Joint research and development programmes focusing on high-altitude processing optimisation

• Equipment manufacturing partnerships with technology localisation requirements

• Technical training programmes for local workforce development

• Shared patent portfolios covering process improvements and equipment modifications

High-altitude processing considerations specific to northwestern Argentina include:

• Atmospheric pressure variations (60% of sea level) affecting evaporation rates

• Temperature fluctuations (-15°C to +40°C) impacting brine chemistry stability

• Equipment durability requirements for harsh environmental conditions

• Remote location logistics for maintenance and technical support

Additionally, these arrangements often incorporate lithium industry innovations that can be adapted to local operating conditions.

How Do Geopolitical Factors Influence Lithium Supply Chain Strategies?

Global lithium supply chains face unprecedented concentration risks as three countries (Australia, Chile, and China) control approximately 75% of global production capacity. This concentration creates strategic vulnerabilities that drive diversification initiatives and alternative supply source development across multiple continents.

Strategic Resource Competition in the Lithium Triangle

The South American lithium triangle encompasses world-class brine deposits across Argentina, Chile, and Bolivia, collectively containing an estimated 58% of global lithium reserves. Regional production capacity expansion targets indicate potential output of 600,000+ tonnes lithium carbonate equivalent annually by 2030, representing the majority of projected global supply growth.

Regional governments have established lithium as a strategic resource, with Argentina targeting 150,000 tonnes annual production capacity, Chile maintaining current leadership at 300,000+ tonnes, and Bolivia developing pilot commercial operations targeting 50,000 tonnes annually by 2028.

Production capacity distribution across the triangle reveals varying development strategies:

| Country | Current Production (2025) | Target Capacity (2030) | Key Advantages | Development Challenges |

|---|---|---|---|---|

| Chile | 285,000 tonnes LCE | 350,000 tonnes LCE | Established operations | Water scarcity concerns |

| Argentina | 12,500 tonnes LCE | 150,000 tonnes LCE | High-grade deposits | Infrastructure development |

| Bolivia | 8,000 tonnes LCE | 50,000 tonnes LCE | Massive reserves | Political stability |

Infrastructure development requirements across the region include:

• Transportation networks connecting remote mining areas to export terminals

• Power generation capacity for energy-intensive processing operations

• Water treatment facilities for sustainable brine processing

• Port facilities capable of handling specialised lithium product shipments

These regional developments often complement detailed Argentina lithium insights that highlight specific competitive advantages and market positioning opportunities.

Market Access and Trade Route Optimisation

Export logistics from northwestern Argentina present unique challenges due to the region's landlocked geography and high-altitude mining locations. Most lithium products require transportation across 1,200+ kilometres to reach Pacific coast shipping facilities in Chile or Atlantic ports in Argentina.

Primary export routes include:

• Pacific corridor: Salta to Chilean ports (Antofagasta, Iquique) via Route 52

• Atlantic corridor: Salta to Argentine ports (Buenos Aires, Rosario) via Routes 9/34

• Rail alternatives: Limited freight rail capacity requiring substantial infrastructure investment

Shipping logistics considerations affect market competitiveness:

• Transport costs: $200-400 per tonne lithium depending on route and logistics efficiency

• Transit times: 5-8 days to Pacific ports, 12-15 days to Atlantic ports

• Customs procedures: Cross-border documentation requirements for Chilean route

• Product handling: Specialised equipment for battery-grade lithium transport

The Argentina lithium adds Chinese partner strategy often incorporates logistics optimisation through coordinated shipping arrangements and shared infrastructure development to reduce per-tonne transportation costs.

What Market Dynamics Drive Lithium Project Valuations?

Lithium project valuations reflect complex interactions between long-term demand projections, supply chain security premiums, and technology risk assessments that extend beyond traditional mining asset evaluation methodologies. Current market dynamics indicate significant valuation premiums for projects offering verified processing capabilities and established offtake arrangements.

Demand Forecasting for Electric Vehicle Battery Supply Chains

Global electric vehicle adoption continues accelerating with 18.2 million EVs sold in 2024, representing 16.8% of total vehicle sales. Industry projections indicate potential 45-60 million annual EV sales by 2030, creating lithium demand of approximately 1.4-1.7 million tonnes lithium carbonate equivalent annually.

Battery chemistry evolution affects lithium intensity requirements:

• Current generation batteries: 8-12 kg lithium per vehicle

• Next generation chemistries: 10-15 kg lithium per vehicle (higher energy density)

• Commercial vehicles: 25-80 kg lithium per vehicle depending on battery size

• Stationary storage: 150-300 kg lithium per MWh storage capacity

Demand growth drivers beyond automotive applications include:

• Grid-scale energy storage: 280+ GWh annual installations projected by 2030

• Consumer electronics: Sustained 8-12% annual growth in lithium-ion battery demand

• Industrial applications: Power tools, aerospace, and specialty battery markets

• Emerging technologies: Solid-state batteries and next-generation energy storage

Competitive Positioning Analysis of Argentine Projects

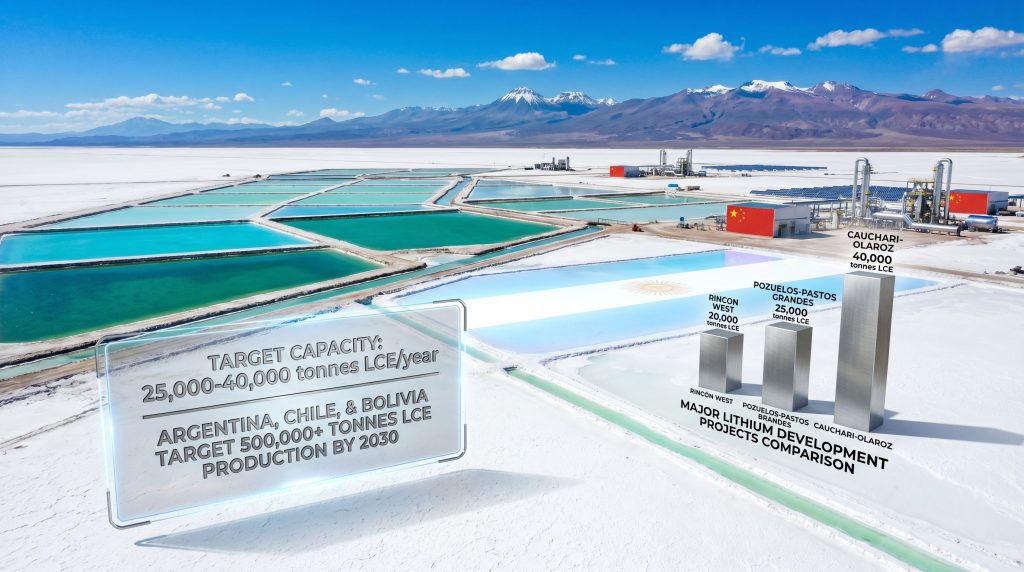

Argentine lithium development encompasses approximately 40+ projects in various development stages, with significant variation in resource quality, development timelines, and partnership structures. The Argentina lithium adds Chinese partner trend has accelerated project advancement through improved access to capital and technical expertise.

Major development projects comparison reveals competitive positioning:

| Project Name | Target Capacity (LCE/year) | Development Stage | Investment Partners | Estimated Timeline |

|---|---|---|---|---|

| Cauchari-Olaroz | 40,000 tonnes | Production | Ganfeng + Lithium Americas | Operating |

| Pozuelos-Pastos Grandes | 125,000 tonnes | Advanced Development | Multiple international | 2026-2027 |

| Rincón West | 35,000 tonnes | Early Development | Argentina Lithium + Chinese partner | 2027-2028 |

| Salar de Vida | 60,000 tonnes | Feasibility | Galaxy + POSCO | 2026-2027 |

Valuation metrics for comparative analysis include:

• Enterprise value per tonne capacity: $180,000-$420,000 depending on development stage

• Resource multiple: 2.5-8.5x net present value of measured/indicated resources

• Infrastructure premium: 15-35% valuation increase for projects with established logistics

• Partnership discount: 10-25% valuation reduction for projects requiring development partners

Quality differentiation factors affecting project valuations:

• Brine lithium concentration: Projects above 1,400 mg/L command valuation premiums

• Impurity ratios: Low magnesium/calcium ratios reduce processing costs and complexity

• Resource classification: Measured/indicated resources valued 2-3x higher than inferred

• Processing technology: DLE-capable projects receive 20-40% valuation premiums

Which Investment Risk Factors Should Stakeholders Monitor?

Lithium project investments face multi-dimensional risk exposures spanning technical, regulatory, market, and geopolitical factors that require sophisticated risk management approaches. Recent market volatility has highlighted the importance of comprehensive risk assessment frameworks that address both project-specific and systemic industry risks.

Operational Risk Assessment in High-Altitude Mining

High-altitude mining operations in northwestern Argentina present unique operational challenges that significantly impact project development timelines and capital requirements. Mining activities at 3,800-4,200 metres above sea level create specific risk factors not present in traditional mining environments.

Environmental and operational risks include:

• Atmospheric conditions: Reduced oxygen levels affecting equipment performance and worker productivity

• Temperature extremes: Daily variations of 40-50°C impacting equipment reliability

• Remote locations: Limited access to specialised maintenance and emergency services

• Water scarcity: Competition for limited freshwater resources with local communities

Infrastructure development challenges specific to the region:

• Power generation: Limited grid connectivity requiring on-site power generation facilities

• Transportation access: Seasonal weather patterns affecting road accessibility

• Communication systems: Satellite-dependent communications due to geographic isolation

• Labour availability: Limited local skilled workforce requiring extensive training programmes

Risk mitigation strategies employed by successful operators:

• Redundant equipment systems to maintain operations during equipment failures

• Local partnership development for community relations and workforce development

• Seasonal operation planning to optimise productivity during favourable weather periods

• Supply chain diversification to reduce dependence on single-source critical components

Currency and Political Risk Management Strategies

Argentine peso volatility presents ongoing challenges for project economics, with currency devaluation exceeding 40% annually in recent years. The Argentina lithium adds Chinese partner structures often incorporate currency hedging mechanisms to protect against peso depreciation while maintaining local operational flexibility.

Political risk factors affecting mining investments:

• Regulatory stability: Provincial mining code modifications affecting royalty rates and environmental requirements

• Export restrictions: Potential limitations on lithium exports to protect domestic battery industry development

• Tax policy changes: Federal and provincial tax modifications affecting project economics

• Infrastructure investment: Government commitment to transportation and power infrastructure development

Risk management mechanisms commonly employed:

| Risk Type | Management Strategy | Implementation Method | Effectiveness |

|---|---|---|---|

| Currency volatility | USD revenue contracts | Long-term offtake agreements | High |

| Political instability | Government partnerships | Local joint ventures | Medium |

| Regulatory changes | Legal compliance monitoring | Specialised legal counsel | Medium-High |

| Infrastructure delays | Self-development | Integrated project development | High |

Insurance and financial protection strategies:

• Political risk insurance covering expropriation and regulatory changes

• Currency hedging contracts protecting against peso devaluation

• Construction delay insurance covering timeline extensions and cost overruns

• Environmental liability coverage for potential ecological damage claims

In addition, the broader context of Chinese global expansion strategies influences risk assessment frameworks as investors evaluate long-term partnership stability and technological capabilities.

The next major ASX story will hit our subscribers first

How Are Production Timelines Accelerating Through Strategic Partnerships?

Strategic partnerships between international technology providers and local operators have demonstrated capability to reduce lithium project development timelines by 25-40% compared to traditional single-operator approaches. These partnerships leverage complementary expertise and shared risk allocation to accelerate critical development phases.

Fast-Track Development Models in Lithium Mining

Integrated development approaches combine engineering, procurement, and construction (EPC) methodologies with parallel processing system development to optimise project schedules. The Argentina lithium adds Chinese partner model exemplifies these accelerated development strategies through coordinated technical and financial resources.

Timeline optimisation strategies include:

• Parallel development phases: Conducting feasibility studies simultaneously with pilot plant operations

• Modular construction: Pre-fabricating processing equipment off-site for rapid installation

• Integrated permitting: Coordinating environmental and operational approvals across jurisdictions

• Technology validation: Concurrent testing of multiple processing approaches to reduce technical risk

Development phase compression achievable through partnerships:

| Development Activity | Traditional Timeline | Partnership Timeline | Time Savings |

|---|---|---|---|

| Feasibility study completion | 24-30 months | 15-20 months | 9-10 months |

| Environmental permitting | 18-24 months | 12-16 months | 6-8 months |

| Engineering and design | 12-18 months | 8-12 months | 4-6 months |

| Construction and commissioning | 36-48 months | 24-36 months | 12 months |

Resource sharing benefits in partnership structures:

• Technical expertise: Access to proven processing technologies and operational experience

• Equipment procurement: Leveraged purchasing power and established supplier relationships

• Construction management: Experienced project management teams and construction methodologies

• Quality assurance: Established testing and validation protocols for product certification

Technology Validation and Scale-Up Methodologies

Pilot plant operations serve as critical validation steps for commercial-scale processing systems, with successful partnerships utilising staged scale-up approaches that minimise technical and financial risks. These methodologies enable iterative optimisation while maintaining development momentum.

Scale-up validation protocols include:

• Bench-scale testing: Laboratory validation of processing chemistry and recovery rates

• Pilot plant operation: Continuous processing at 0.1-1.0 tonnes per day capacity

• Demonstration scale: Semi-commercial operations at 5-20 tonnes per day capacity

• Commercial validation: Full-scale operations achieving nameplate capacity targets

Performance validation metrics tracked throughout scale-up:

• Recovery efficiency: Maintaining 85%+ lithium extraction rates across scale levels

• Product quality: Achieving battery-grade specifications (99.5%+ purity) consistently

• Process stability: Operating at design capacity for extended periods without interruption

• Cost performance: Meeting target production costs within ±15% variance

Quality control standards for battery-grade production:

| Specification | Battery-Grade Requirement | Testing Frequency | Compliance Method |

|---|---|---|---|

| Lithium content | 99.5% minimum | Every batch | X-ray fluorescence |

| Heavy metals | <10 ppm total | Weekly | ICP-MS analysis |

| Moisture content | <0.5% maximum | Daily | Karl Fischer titration |

| Particle size | 5-25 microns | Every batch | Laser diffraction |

What Long-Term Industry Implications Emerge from These Partnerships?

Cross-border lithium partnerships are fundamentally reshaping global supply chain architecture by creating integrated value chains that span multiple countries and technological capabilities. These developments suggest a structural evolution toward more collaborative and technologically sophisticated mining operations.

Supply Chain Diversification Strategies

Geographic risk distribution through international partnerships reduces dependence on single-country supply sources while creating resilient supply networks capable of adapting to geopolitical disruptions or natural disasters. The Argentina lithium adds Chinese partner trend represents broader industry movement toward supply chain redundancy.

Diversification benefits achieved through strategic partnerships:

• Production flexibility: Ability to shift output between facilities based on market conditions

• Technology sharing: Cross-pollination of technical innovations and operational improvements

• Risk mitigation: Reduced exposure to country-specific political or economic disruptions

• Market access: Combined partner networks providing broader customer reach

Vertical integration opportunities emerging from partnerships:

• Battery manufacturing: Lithium producers partnering with cell manufacturers

• Recycling capabilities: Closed-loop systems recovering lithium from used batteries

• Technology development: Joint research programmes advancing processing efficiency

• Infrastructure sharing: Coordinated development of transportation and processing facilities

Future Investment Patterns in Critical Minerals Sector

Investment flow analysis indicates increasing preference for partnership-based development models over traditional single-operator approaches. This trend reflects recognition that modern lithium operations require diverse technical capabilities and substantial capital resources that favour collaborative structures.

Emerging investment characteristics include:

• Technology-focused partnerships: Alliances prioritising technical innovation over pure financial returns

• Sustainability requirements: Environmental performance standards becoming standard investment criteria

• Local community integration: Mandatory stakeholder engagement and benefit-sharing arrangements

• Regulatory coordination: Multi-jurisdictional compliance management through specialised partnerships

Long-term industry evolution trends suggest:

• Consolidation pressure: Smaller operators seeking partnership structures to achieve scale

• Technology standardisation: Convergence around proven processing technologies and quality standards

• Supply chain integration: Vertical partnerships extending from mining through battery production

• Sustainability focus: Environmental performance becoming competitive differentiator

The transformation of South American lithium development through strategic international partnerships represents more than capital deployment optimisation. These collaborations are creating new operational paradigms that combine technological innovation with risk distribution and market access strategies. As battery demand continues expanding, the partnership model pioneered in Argentina's lithium sector may become the template for critical mineral development globally.

Investment professionals monitoring this sector should focus on partnership quality, technology validation progress, and infrastructure development timelines rather than traditional mining metrics alone. The most successful projects will likely be those that effectively combine local expertise with international technical capabilities and capital resources.

According to BN Americas analysis, these partnerships are increasingly structured around specific project development milestones that align technical delivery with financial contributions. Moreover, Argentina Lithium's official announcement demonstrates how these agreements typically incorporate technology transfer provisions alongside capital deployment commitments.

This analysis is based on publicly available information and industry research. Investors should conduct independent due diligence before making investment decisions. Lithium market conditions and regulatory frameworks may change, affecting project viability and investment returns.

Considering Investing in Argentina's Emerging Lithium Sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant lithium and critical minerals discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market at discoveryalert.com.au.