July 26, 2026

The Investment Architecture Reshaping Latin America's Critical Minerals Race

Across the global mining industry, the fundamental challenge has never been geological. The world's remaining copper and lithium endowments are well understood, reasonably mapped, and largely accessible. What separates a resource in the ground from a mine in production is the regulatory and fiscal environment surrounding it. Jurisdictional risk, not resource scarcity, has historically been the primary constraint on critical minerals supply growth. Argentina RIGI mining projects represent a direct, structural attempt to solve that problem at scale.

The timing is significant. Global copper demand tied to grid infrastructure buildout, electrification, and EV manufacturing is widely expected to outpace new mine supply through the late 2020s. Lithium markets, while more volatile, face long-term structural demand growth from battery storage deployment. Against this backdrop, any jurisdiction capable of credibly de-risking large-scale mining investment becomes a focal point for global capital. Argentina, for the first time in a generation, is positioning itself as exactly that jurisdiction.

When big ASX news breaks, our subscribers know first

What Is Argentina's RIGI Scheme and Why Does It Matter for Global Mining?

The Regulatory Architecture Behind RIGI

The Régimen de Incentivo para Grandes Inversiones, known by its acronym RIGI, was established under Argentina's 2024 Ley de Bases as a dedicated framework for large-scale capital deployment across strategic sectors. Its design reflects a deliberate departure from the policy instability that has historically inflated Argentina's sovereign risk premium and discouraged multi-decade infrastructure commitments.

The scheme sets a minimum qualifying threshold of US$200 million per project, explicitly targeting export-oriented, capital-intensive investments rather than small or medium-scale operations. Eligible sectors span mining, energy, oil and gas, infrastructure, and technology, with a deliberate focus on industries where long investment horizons make policy uncertainty particularly damaging to capital allocation decisions.

The Core Incentive Stack: What Investors Actually Receive

The incentive structure RIGI offers is meaningfully different from prior Argentine investment promotion schemes, primarily because it combines fiscal benefits with contractual durability.

| Incentive Category | Specific Benefit |

|---|---|

| Tax Stability | Fixed corporate tax rates for 30 years |

| Customs Exemptions | Import duty waivers on capital equipment |

| FX Flexibility | Rights to retain and repatriate foreign currency earnings |

| Regulatory Certainty | Protection against future legislative changes |

| Local Content Requirement | Minimum 20% local supplier participation |

The foreign exchange component deserves particular attention. Historically, Argentina's currency controls and capital repatriation restrictions have been the single most cited deterrent for international mining investors. RIGI directly addresses this by granting approved projects the legal right to retain foreign currency earnings and repatriate capital outside the standard exchange control framework. For a country with Argentina's monetary history, this is a substantive structural commitment, not merely a promotional gesture.

The contractual architecture of RIGI is designed to provide protections that survive government transitions, meaning changes in future administrations cannot unilaterally alter the terms granted at the point of approval. This directly targets the sovereign risk premium that has historically made Argentine assets trade at a discount to comparable geological opportunities elsewhere.

President Milei's Pro-Market Reform Context

RIGI sits at the centre of President Javier Milei's economic liberalisation agenda, representing a calculated pivot away from the resource nationalism that characterised earlier Argentine administrations. The scheme targets Argentina's position within the lithium triangle, the contiguous zone across Salta, Jujuy, and Catamarca provinces that collectively holds some of the world's most significant brine-based lithium concentrations. Simultaneously, it aims to develop an emerging copper belt centred on San Juan and Mendoza.

Submission deadlines have been progressively extended, with current windows running through July 2026 to 2027, a signal that the government is actively managing pipeline development rather than treating RIGI as a one-time reform measure. Furthermore, the large investment incentive scheme provides detailed guidance for prospective investors navigating the approval process.

How Large Is Argentina's RIGI Mining Investment Pipeline?

The Full Scale of Capital Mobilised

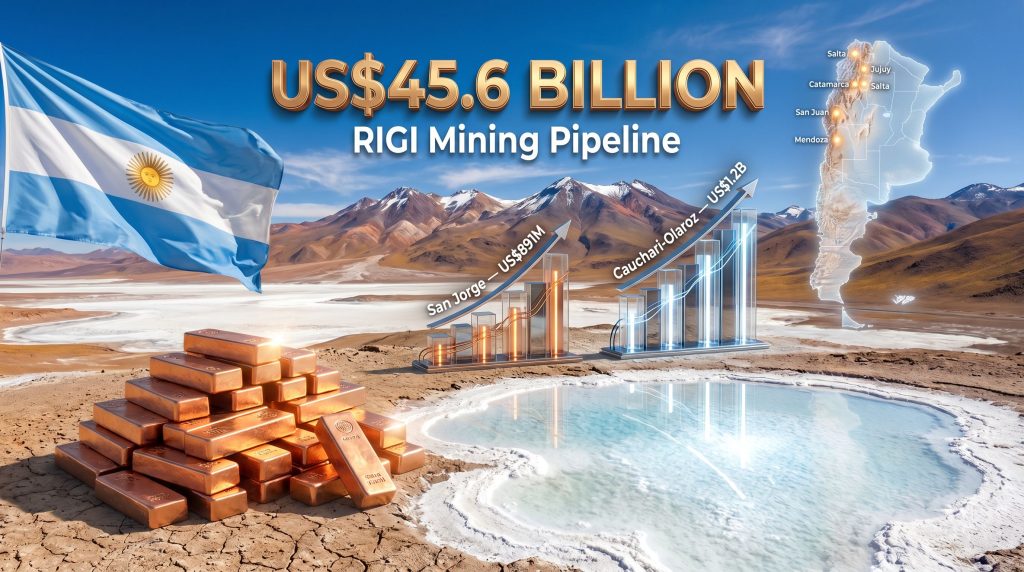

The scale of capital attracted to Argentina RIGI mining projects has exceeded most early projections for the scheme. Across all sectors, proposed investments range between US$33.9 billion and US$69.2 billion across 32 identified projects. Within this broader pipeline, mining accounts for approximately US$45.6 billion spread across 18 projects, making it the dominant sector by capital value.

| Pipeline Category | Estimated Value | Number of Projects |

|---|---|---|

| Total Proposed (All Sectors) | US$33.9B to US$69.2B | 32 projects |

| Mining-Specific Pipeline | US$45.6B | 18 mining projects |

| Approved (All Sectors) | US$8B to US$26.6B | 8 to 12 projects |

| Under Review | US$17B to US$30B | 12+ projects |

| Rejected | US$273M | 1 project |

Copper dominates the mining pipeline by capital value, representing roughly 73% of mining-specific investment commitments. This weighting reflects both the scale of capital required for large porphyry copper developments and the geological prospectivity of Argentina's western provinces.

Commodity Breakdown Within the Mining Pipeline

-

Copper: The largest category by value; projects concentrated in San Juan and Mendoza provinces; includes assets at feasibility and construction-ready stages

-

Lithium: Primarily brine-based operations across the northern provinces; early RIGI approvals weighted toward brownfield expansions before greenfield projects progressed through the review process

-

Silver and Gold: An emerging presence in the pipeline, including polymetallic assets in Salta province

-

Strategic Alignment: The commodity mix directly corresponds to energy transition demand, copper for grid infrastructure and electrification, lithium for battery storage and electric vehicles

What Are the Two Newly Approved RIGI Mining Projects Worth $2.1 Billion?

Argentina's Economy Minister Luis Caputo confirmed on May 14, 2026 that two new mining projects had received RIGI approval, bringing combined investment to US$2.1 billion and projected employment to more than 8,000 direct and indirect jobs.

Project 1: San Jorge Copper Project, Mendoza Province

The San Jorge copper project in Mendoza received RIGI approval with a committed investment of US$891 million. The project adds Mendoza to the map of provinces actively attracting large-scale mining capital under the scheme, complementing the copper and lithium development activity already underway in San Juan, Jujuy, and Catamarca.

The approval is particularly notable from a timing perspective. The ongoing copper supply crunch is creating a structural tension between rising demand from electrification and constrained new supply pipelines, with major projects facing permitting delays, cost overruns, and social licence challenges across multiple jurisdictions. Argentina's ability to advance a near-US$900 million copper project through a formal regulatory approval framework in this environment is precisely the kind of jurisdictional signal that shifts capital allocation decisions.

Project 2: Cauchari-Olaroz Lithium Project Expansion, Jujuy Province

The expansion of the Cauchari-Olaroz lithium project received RIGI approval for a US$1.2 billion investment in Jujuy Province. Cauchari-Olaroz is a brine-based lithium operation situated within the lithium triangle, and the RIGI-approved component represents a capacity expansion of an already-producing asset. This brownfield profile reduces the ramp-up risk and timeline uncertainty that accompanies greenfield lithium developments, making it a lower-execution-risk vehicle for expanding Argentine lithium output.

Ganfeng Lithium, one of the world's largest lithium producers, holds involvement in the Cauchari-Olaroz project, representing a significant commitment from a tier-one participant in global battery supply chains. In addition, the Argentina lithium brines sector continues to attract increasing attention from international capital as brine-based cost economics demonstrate resilience across varied lithium price environments.

Combined Impact Summary

| Metric | Value |

|---|---|

| Total Combined Investment | US$2.1 billion |

| Jobs Created (Direct and Indirect) | 8,000+ |

| Provinces Activated | Mendoza (copper), Jujuy (lithium) |

| Commodity Diversification | Copper and lithium, dual energy transition metals |

The simultaneous approval of projects across two different provinces and two different commodities within a single announcement reflects the operational breadth RIGI has developed. The scheme is demonstrably capable of processing large, complex, multi-province approvals concurrently, a capacity that reduces the queue risk for projects still under review.

Which Major Global Mining Companies Are Betting on Argentina's RIGI?

Flagship Projects and Corporate Participants

The quality of corporate participation in Argentina RIGI mining projects is as analytically significant as the headline investment figures. Tier-one miners conduct exhaustive sovereign risk assessments before committing feasibility capital. Their presence functions as an implicit endorsement of the framework's credibility and durability.

Key participants include:

-

McEwen Copper: Los Azules copper project in San Juan; RIGI approval confirmed September 2025 with a committed investment of US$2.672 billion; the project incorporates renewable energy and low-water heap leaching technology, positioning it as a lower-carbon copper operation aligned with downstream buyer ESG requirements

-

Rio Tinto: Sal de Vida lithium project; under active review within the RIGI framework; signals tier-one miner confidence in Argentina's regulatory trajectory

-

Glencore: Active within the copper pipeline; presence reinforces institutional credibility of the scheme as a vehicle capable of attracting diversified major mining companies

-

Ganfeng Lithium: Involved in the Cauchari-Olaroz project receiving the newly announced US$1.2 billion expansion approval; Ganfeng's separate Mariana project was previously rejected for non-compliance, demonstrating both the scheme's accessibility and its enforcement standards

-

Lundin Group: Represented within the broader copper pipeline

-

Abra Silver: Diablillos silver-gold project in Salta Province; approximately US$500 million; currently under evaluation

The entry of Rio Tinto, Glencore, and Ganfeng Lithium into Argentina's RIGI pipeline carries analytical weight beyond headline dollar figures. These companies conduct exhaustive sovereign risk assessments before committing to feasibility expenditure. Their participation reduces the perceived risk premium for smaller and mid-tier investors considering Argentine exposure, creating a validation effect that extends well beyond the direct capital they represent.

Understanding Low-Water Heap Leaching: A Technical Differentiator

The low-water heap leaching technology referenced in connection with the Los Azules project warrants explanation for investors less familiar with copper processing methods. Traditional copper extraction in porphyry deposits typically requires significant water consumption, which creates both operational and social licence challenges in arid Andean environments. Heap leaching applies acidic solution to crushed ore stacked on impermeable pads, dissolving copper which is then recovered from the solution, and the low-water variant of this process is designed specifically to minimise freshwater drawdown in water-stressed high-altitude regions.

This technical choice is not incidental. It directly addresses one of the primary community and environmental objections to large-scale copper mining in Argentine Andean provinces, potentially smoothing the social licence pathway that has blocked comparable projects in Peru and Chile. Furthermore, the emerging Argentina copper system in San Juan continues to demonstrate geological prospectivity that reinforces the country's long-term copper production potential.

How Does RIGI Compare to Mining Investment Frameworks Across Latin America?

Competitive Positioning Against Regional Peers

Argentina's RIGI does not operate in a vacuum. It competes for a finite pool of global mining capital against established and emerging frameworks across the region.

| Country | Key Framework Feature | Investor Perception | Key Risk Factor |

|---|---|---|---|

| Argentina (RIGI) | 30-year tax stability, FX flexibility, contractual protections | Increasingly positive; tier-one miner entry | Environmental compliance, glacier law exposure |

| Chile | Established regime; royalty reform uncertainty | Cautious; royalty debate created hesitation | Lithium nationalisation risk; royalty rate increases |

| Peru | Large copper endowment; permitting challenges | Mixed; community conflict risk elevated | Social licence failures; permitting delays |

| Mexico | Historically permissive; recent nationalisation moves | Declining; resource nationalism concerns | Lithium nationalisation; regulatory reversals |

Chile's lithium strategy is instructive. The extended domestic debate over lithium nationalisation and copper royalty restructuring created a multi-year window of investment hesitation that materially slowed the advancement of several large projects. Argentina's RIGI is, in part, designed to capture capital that would historically have defaulted to Chile in the absence of a credible competitive framework.

Peru's challenges are primarily operational rather than legislative, but the effect on capital allocation is similar. Community conflict, permitting gridlock, and social licence failures have delayed projects representing tens of billions of dollars in committed investment. Argentina's less congested project queue and structured approvals process offer a comparative advantage that is difficult to replicate through geological endowment alone.

Argentina's Structural Competitive Advantages

Several features of Argentina's position within the regional landscape are worth distinguishing from policy-specific factors:

-

Lithium Triangle Access: Argentina controls a disproportionate share of high-quality lithium brine resources, characterised by high lithium concentrations, manageable impurity profiles, and relatively shallow depths that reduce extraction costs relative to hard-rock spodumene operations in Australia

-

Brine vs. Hard-Rock Cost Economics: Lithium brine operations generally carry lower capital intensity and operating costs per tonne of lithium carbonate equivalent than hard-rock mining and processing, making Argentine assets economically competitive across a wide range of lithium price scenarios

-

Copper Belt Emergence: San Juan and Mendoza provinces are demonstrating geological prospectivity that positions Argentina as a potentially significant copper producer by the early 2030s

-

Currency Repatriation Rights: The FX flexibility embedded in RIGI directly resolves what has historically been the most cited deterrent for international investors considering Argentine exposure

The next major ASX story will hit our subscribers first

What Are the Environmental and Regulatory Risks Facing RIGI Mining Projects?

The Glacier Law Tension

No analysis of Argentina RIGI mining projects is complete without addressing the environmental overlay that constrains several high-value candidates. Argentina's Glacier Protection Law restricts mining and industrial activity in periglacial zones, creating a compliance layer that affects a number of large copper assets in the Andean provinces.

Projects including Josemaría and MARA, both copper developments, have attracted scrutiny regarding potential impacts on periglacial environments. A revised glacier regulatory framework enacted in February 2026 has been interpreted by some industry observers as potentially clarifying the permitting pathway for certain project types, though this does not eliminate the underlying compliance requirement. The distinction matters: brine lithium operations in the northern Puna region generally carry a different environmental profile than hard-rock copper mining in the central Andes, meaning the glacier law exposure is not uniform across the RIGI mining pipeline.

Key Environmental Risk Categories

-

Water Usage: Lithium brine extraction in the Puna region raises legitimate concerns about aquifer depletion and the water security of indigenous and rural communities dependent on shared freshwater systems

-

Wetland Impacts: Historical enforcement actions in Argentine mining have established a regulatory precedent that RIGI applicants must actively navigate, not merely acknowledge

-

Revenue Compliance: Past instances of export under-invoicing in Argentine mining have informed stricter revenue reporting requirements within RIGI's approval and monitoring framework

-

Community Consent: Free, prior, and informed consent requirements for indigenous communities in Jujuy and Salta add procedural complexity and timeline uncertainty to project development, particularly for greenfield lithium operations

The Mariana project rejection, a US$273 million proposal involving Ganfeng Lithium that was denied RIGI status for non-compliance, demonstrates that Argentina's government is prepared to decline approvals regardless of applicant scale. This enforcement precedent is analytically important: it signals that RIGI's protections apply post-approval, not as a guarantee during the review process, and that compliance standards are substantive rather than procedural.

What Does Argentina's RIGI Mean for the Global Copper and Lithium Supply Chain?

Copper Supply Gap and Argentina's Strategic Role

The structural context for Argentina's copper ambitions is well established in commodity market research. Global copper demand tied to grid infrastructure expansion, EV adoption, and industrial electrification is expected to grow materially through the late 2020s, while the pipeline of new mine supply faces delays, grade declines at operating mines, and permitting challenges across multiple major producing jurisdictions.

Argentina's RIGI copper pipeline, representing approximately 73% of mining investment value within the scheme, positions the country to contribute to closing this gap through large-scale porphyry copper development. The Los Azules project alone, approved in September 2025 at US$2.672 billion, is designed as a low-carbon operation with renewable energy integration, differentiating it in a market where downstream buyers are increasingly applying ESG criteria to supply chain qualification.

Lithium Supply Chain Implications

Argentina's lithium brine resources carry a cost advantage that is structural rather than cyclical. The combination of high-grade brines, established evaporation pond technology, and lower capital requirements relative to hard-rock alternatives means that RIGI-approved expansions like Cauchari-Olaroz can remain economically viable across a wider range of lithium price scenarios than comparable assets in higher-cost jurisdictions.

Advances in direct lithium extraction technology are also increasingly relevant to Argentina's brine-based operations, offering the potential to improve recovery rates and reduce environmental footprint compared to conventional evaporation pond methods. The government has, furthermore, identified a US$4.2 billion investment target specifically for the lithium sector, with RIGI as the primary mobilisation mechanism.

Long-Term Economic Projections

| Metric | Projection | Timeframe |

|---|---|---|

| Mining Trade Surplus | US$15B to US$31B | By 2030 to 2035 |

| Total Energy and Mining Surplus | US$75B | By 2035 |

| Direct and Indirect Jobs (RIGI Mining) | 35,600+ | Cumulative |

| Lithium Sector Investment Target | US$4.2B | Medium-term |

Disclaimer: The projections above represent government and industry estimates. Actual outcomes will depend on commodity price trajectories, project execution timelines, financing conditions, and macroeconomic factors. These figures should not be interpreted as guaranteed outcomes or investment advice.

Frequently Asked Questions: Argentina RIGI Mining Projects

What is the minimum investment required to qualify for RIGI?

Projects must commit a minimum of US$200 million in capital expenditure to be eligible. The scheme is explicitly designed for large-scale, export-oriented investments.

How many mining projects have been approved under RIGI so far?

As of mid-2026, between 8 and 12 projects across all sectors have received RIGI approval, with mining representing the largest single category by both project count and capital value. Total approved investment ranges from US$8 billion to US$26.6 billion depending on the measurement methodology applied.

Can a RIGI approval be revoked?

The contractual structure is designed to provide protections that survive legislative changes post-approval. However, the Mariana project rejection demonstrates that projects can be denied RIGI status during the application review stage for non-compliance.

Which provinces have the highest concentration of RIGI mining projects?

San Juan (copper), Catamarca (copper and lithium), Salta (lithium, silver-gold), and Jujuy (lithium) account for the majority of RIGI mining investment proposals. Mendoza was added to this group with the San Jorge copper project approval confirmed in May 2026.

What is the current RIGI submission deadline?

Submission windows currently run through July 2026 to July 2027 depending on project category, reflecting the government's ongoing commitment to pipeline development beyond the initial reform announcement.

The Road Ahead: Can Argentina Sustain RIGI's Investment Momentum?

Critical Success Factors

The conversion of RIGI proposals into operating mines will ultimately be determined by factors that sit outside the federal framework itself:

-

Provincial alignment: Mining permits and environmental approvals remain provincial responsibilities. RIGI provides federal-level contractual certainty but cannot bypass provincial permitting processes, creating a dual-approval pathway that introduces execution risk even for federally approved projects

-

Project financing conditions: Several approved projects remain contingent on securing project finance arrangements. Global credit conditions, commodity price trajectories, and lender ESG requirements will all influence the pace of construction commencement

-

Environmental compliance capacity: The government's ability to build credible, well-resourced environmental review capacity will determine whether RIGI approvals translate into operational mines or accumulate as approved-but-stalled assets

-

Electoral cycle durability: RIGI's 30-year protections are architecturally designed to survive government transitions, but investor confidence in that durability will face its first real test at Argentina's next electoral cycle

The 2026 to 2027 Approval Window

Approximately seven months of submission eligibility remain in the current RIGI window as of mid-2026. Projects under active evaluation include major copper assets such as Vicuña, MARA, and El Pachón, alongside lithium operations including Sal de Vida (Rio Tinto), Sal de Oro (Posco), and Rinconada (Tenaris). The inclusion of upstream hydrocarbon projects within RIGI's scope, notably Vaca Muerta LNG and associated pipeline infrastructure, provides a diversified approval base that reduces the scheme's dependence on mining-specific commodity price conditions.

Argentina's RIGI pipeline, if fully converted from proposals to operating assets, would represent one of the most significant single-country mining investment cycles in Latin American history. The US$45.6 billion mining component alone exceeds the total annual mining capital expenditure of most mid-tier producing nations. Whether that potential is realised depends less on geological endowment, which is demonstrably world-class, and more on the institutional execution capacity of both federal and provincial governments.

The announcement of the San Jorge copper project and the Cauchari-Olaroz expansion in a single May 2026 announcement is, in this context, a data point rather than a destination. It confirms that the approval machinery is functioning and that capital is moving. The harder question, how much of that capital ultimately reaches the ground, will take the better part of a decade to answer.

This article is intended for informational purposes only and does not constitute financial or investment advice. Mining project timelines, investment figures, and economic projections are subject to change based on commodity markets, regulatory developments, and project-specific factors. Readers should conduct their own due diligence before making investment decisions.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors. Explore why historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.