June 15, 2026

The Hidden Mechanics Behind Asia's Coal Comeback

Energy markets rarely move in straight lines. They lurch, pivot, and recalibrate in response to events that policymakers and forecasters consistently underestimate. The closure of the Strait of Hormuz in early March 2026 represents exactly this kind of rupture — an event so structurally consequential that its ripple effects are now reshaping fuel procurement strategies across an entire continent. Understanding why the Asian energy squeeze drives coal demand surge requires looking past the surface-level narrative of a simple fuel switch and examining the deeper mechanics of how power systems, freight markets, and industrial supply chains respond when a critical energy artery is severed.

When big ASX news breaks, our subscribers know first

The Geopolitical Fault Line That Rewired Asian Energy Flows

The Strait of Hormuz is not merely a shipping lane. Roughly 20% of the world's total oil supply and a substantial portion of global LNG shipments transit this narrow channel annually. When access was effectively cut off in early 2026, the consequences for Persian Gulf-dependent energy importers across Asia were immediate and severe.

Asian buyers that had structured their energy procurement around relatively predictable Gulf supply chains suddenly found themselves competing for alternative cargoes in a market where optionality was thin and spot pricing was moving sharply higher. Furthermore, the disruption compounded an already fragile LNG supply outlook by removing a major processing hub from the equation.

The damage sustained by the Ras Laffan LNG facility in Qatar arguably represents the single most consequential supply shock of 2026. Ras Laffan is among the largest LNG processing complexes on earth, and any meaningful reduction in its operational capacity creates a hole in global LNG availability that cannot be patched quickly. New LNG liquefaction capacity takes years to permit, finance, and construct, meaning the shortfall created by this disruption cannot be remedied through rapid supply-side responses.

Quantifying the LNG Gap and Its Downstream Power Market Effects

The scale of the supply disruption becomes clearer when the numbers are laid out directly.

| Metric | Estimated Figure |

|---|---|

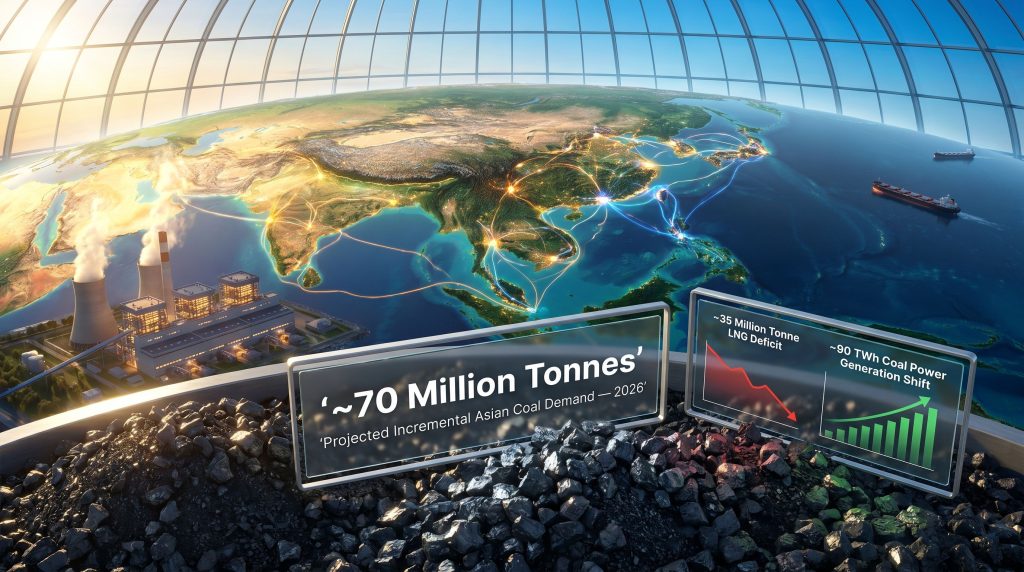

| Total LNG shortfall across Asia (2026) | ~35 million tonnes |

| LNG capacity removed by Ras Laffan damage | ~10.2 Mtpa |

| Power generation shift from gas to coal | ~90 TWh |

| Projected incremental Asian coal demand (2026) | Up to 70 million tonnes |

| Cumulative coal demand uplift by 2030 (sustained scenario) | ~150 million tonnes |

Spot LNG prices moved close to three-year highs in the wake of the disruption, creating a powerful economic incentive for utilities to reduce gas burn wherever an operational alternative existed. Coal-fired power plants, many of which had been running at reduced utilisation rates as utilities prioritised gas and renewables, became the most immediately available backstop.

This is a critical distinction that is often lost in the broader narrative. The current coal demand surge is not being driven by new coal plant construction. It reflects a sharp acceleration in the utilisation rates of existing coal capacity — a response pathway that is faster, cheaper, and more logistically straightforward than any supply-side alternative. Restarting or increasing output at an existing coal plant can be achieved in days or weeks. Building new generation infrastructure requires years.

According to Rystad Energy's analysis of Asia's coal demand, the region's appetite for thermal coal is set to rise materially as LNG substitution accelerates across multiple markets simultaneously.

Country-by-Country Exposure Across the Region

The fuel-switching response has not been uniform across Asia. Different countries face different structural constraints, and their coal demand responses reflect those differences.

| Country | Demand Driver | Coal Response |

|---|---|---|

| Japan | LNG supply disruption, nuclear constraints | Higher coal plant utilisation |

| South Korea | Spot LNG price spike | Temporary coal burn increase |

| Taiwan | Gas import dependency | Accelerated coal restocking |

| Vietnam | Power generation shortfall | Expanded coal plant operations |

| Thailand | Gas-to-power gap | Fuel switching to coal |

| Philippines | LNG infrastructure limits | Coal as baseload backup |

| China | Oil supply disruption, chemical feedstock shift | Coal-to-chemicals pivot plus strategic restocking |

Japan and South Korea are particularly exposed because both nations rely heavily on imported LNG for gas-fired power generation and lack meaningful domestic fossil fuel resources. Taiwan faces a structurally similar challenge, with high gas import dependency and limited grid flexibility. Across Southeast Asia, Vietnam, Thailand, and the Philippines are responding with operational increases at existing coal plants rather than long-term policy reversals.

However, broader coal supply challenges in the global market mean that sourcing the additional volumes required to satisfy this demand will not be straightforward for all buyers.

China's Response: A Different Animal Entirely

China's reaction to the Hormuz disruption deserves separate treatment because it operates across two distinct dimensions simultaneously.

First, China has been restocking coal in very large volumes as a direct energy security response. According to Stamatis Tsantanis, CEO of Capesize shipping operator Seanergy Maritime Holdings, China's coal restocking activity in recent months has been substantial — a signal that Beijing is treating coal not merely as a power generation input but as a strategic buffer against prolonged geopolitical instability affecting energy supply chains.

Second, and perhaps more strategically significant, China is accelerating its coal-to-chemicals production pathway. Chinese petrochemical facilities and refineries that would typically use crude oil as a feedstock are increasingly substituting domestic coal through established chemical conversion processes. This is not a new technology in China — coal gasification and liquefaction infrastructure has existed for decades — but the current geopolitical environment has meaningfully expanded its economic attractiveness relative to crude oil imports routed through contested maritime corridors.

In addition, China commodity demand trends across steel and iron ore markets are compounding the broader pressure on bulk freight capacity, further tightening shipping availability for coal cargoes. Tsantanis has also highlighted that coal is increasingly being treated as a strategic commodity by the United States, which has emerged as a supplier of last resort for some Asian buyers who can no longer source affordably from Gulf producers.

The Rystad Demand Projections and What They Mean for Trade

Energy consultancy Rystad Energy has projected that Asia could require up to 70 million additional tonnes of coal in 2026 relative to baseline consumption levels. Under a scenario where LNG supply tightness persists across multiple years, cumulative additional coal consumption could reach 150 million tonnes by 2030.

These are not trivial figures. To contextualise the scale, the global seaborne thermal coal trade typically runs at roughly 1 billion tonnes per year. A sustained uplift of 70 to 150 million tonnes represents a meaningful percentage shift in global trade volumes, with significant implications for:

- Port infrastructure utilisation across major coal export hubs in Australia, Indonesia, and South Africa

- Vessel availability in the Capesize and Panamax bulk carrier segments

- Coal price benchmarks at Newcastle, Richard's Bay, and API 2

Furthermore, the eco-business analysis of Asia's coal outlook suggests that the 150 million tonne cumulative demand figure could prove conservative if Southeast Asian LNG infrastructure constraints remain unresolved beyond 2027.

The next major ASX story will hit our subscribers first

Freight Markets: The Secondary Consequence Nobody Is Pricing Correctly

One of the less-discussed consequences of the current supply disruption is its effect on bulk freight markets. Vessels that would ordinarily transit the Strait of Hormuz or the Red Sea are now routing around these corridors, significantly extending voyage distances and increasing fuel consumption per trip.

Seanergy Maritime Holdings, which operates Capesize vessels carrying coal, iron ore, and bauxite, has no ships currently transiting the Strait of Hormuz. However, the company has flagged that higher bunker fuel costs and longer trade routes are inflating operating costs across the fleet. These elevated freight costs are not contained within energy markets.

Elevated transport costs for bulk raw materials directly affect the economics of major global infrastructure programmes, including data centre construction and large-scale civil engineering projects, which depend on reliable and cost-efficient movement of steel, cement inputs, and other bulk commodities.

This freight cost inflation represents a secondary transmission mechanism through which the Middle East supply disruption reaches industries with no direct exposure to energy markets. Consequently, the oil market disruption stemming from contested waterways is creating knock-on effects that extend well beyond traditional energy sector boundaries.

Is This a Structural Shift or Emergency Substitution?

The honest analytical answer is that the current demand surge reflects emergency fuel substitution rather than a fundamental abandonment of Asia's longer-term energy transition commitments. Most regional governments have not revised their decarbonisation targets, and regulatory frameworks governing coal plant closures remain broadly intact.

However, the risk of temporary dependency becoming structurally embedded should not be dismissed. Utility procurement teams that rebuild coal supply chains, renegotiate long-term contracts, and recommission idled capacity are making decisions that have operational inertia. The longer the LNG shortfall persists, the greater the probability that coal consumption levels in 2027 and 2028 remain elevated above pre-crisis trajectories even after some LNG supply is restored.

An additional wildcard is the El Niño weather pattern. Tsantanis has specifically flagged the risk of a strong El Niño event amplifying fuel demand across parts of Asia, particularly in regions where hydropower generation collapses during drought conditions and thermal power plants must compensate. Countries like Vietnam, Thailand, and the Philippines have historical vulnerability to exactly this dynamic.

Investor note: Markets that price coal equities or coal-linked freight assets purely on the basis of short-term demand metrics risk misjudging the structural ceiling. The current Asian energy squeeze drives coal demand surge in ways that are crisis-driven. Any easing of Hormuz access or restoration of Ras Laffan output could materially reduce the demand impulse within a relatively short timeframe.

Mining Majors Best Positioned to Capitalise

Among the largest beneficiaries of redirected Asian coal demand are miners with established export positions in markets perceived as geopolitically stable and outside the zones of maritime contestation. BHP and Glencore both operate significant thermal and metallurgical coal assets with Pacific Basin export exposure, positioning them to supply markets that are actively diversifying away from Russian and Middle Eastern supply chains.

The diversification imperative is itself a structural demand driver that sits on top of the cyclical fuel-switching response. Understanding the broader commodity price impacts on mining company earnings is therefore essential context for evaluating which producers stand to benefit most from sustained Asian demand. Asian utilities and governments that have experienced the vulnerability of concentrated supply chains are likely to build strategic stock diversification requirements into future procurement policies, even after the immediate crisis passes.

Frequently Asked Questions: Asia's Coal Demand Surge Explained

Why is Asia turning to coal instead of renewables or nuclear during this crisis?

Renewables and nuclear cannot be rapidly scaled to fill an acute supply gap. Solar and wind output cannot be scheduled on demand, and nuclear capacity additions require long lead times. Coal plants already exist across the region and can increase output within days, making them the only realistic short-term bridge fuel.

Which Asian nations face the greatest exposure to the LNG shortfall?

Japan, South Korea, and Taiwan face the highest structural exposure due to their heavy reliance on imported LNG and limited domestic energy alternatives. Southeast Asian markets including Vietnam and the Philippines are also significantly affected.

Could the coal demand surge persist beyond 2026?

Under Rystad Energy's sustained tightness scenario, cumulative additional coal consumption could extend to 150 million tonnes by 2030. Whether this materialises depends on how quickly LNG supply is restored and whether regional governments embed coal procurement flexibility into long-term energy policy.

How does the Hormuz closure affect coal specifically, given that coal does not transit the strait?

The connection is indirect but significant. Hormuz's closure reduces oil and LNG availability, forcing fuel switching to coal. Simultaneously, vessels routing around contested waterways face higher operating costs, which flows into freight rates for all bulk commodities including coal.

What role could El Niño play in amplifying Asian energy demand?

A strong El Niño event typically reduces hydropower output across Southeast and East Asia by depressing rainfall and reservoir levels. Countries that rely materially on hydropower, including Vietnam and parts of southern China, would face amplified power deficits, pushing coal plant utilisation even higher. The Asian energy squeeze drives coal demand surge even harder under this scenario, making it one of the key risk variables for energy market participants to monitor through the remainder of the decade.

Want to Capitalise on the Next Major Commodity Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.