June 9, 2026

The Capital Efficiency Question Reshaping Junior Lithium Development

Not every lithium project needs to cost half a billion dollars to matter. As the battery supply chain buildout accelerates globally, a quiet but important realisation has taken hold among institutional capital allocators: the most strategically valuable lithium assets are not always the largest. Sometimes, they are the ones closest to production, with the lowest execution risk and the most defensible capital structure. That calculus is precisely what makes the Atlas Lithium Brazilian US$60 million project in the United States investor circuit an inflection point worth examining in detail.

The Neves Project, located in Brazil's Minas Gerais state, sits at an unusual intersection of geological merit, regulatory readiness, and capital efficiency. With a completed Definitive Feasibility Study, secured operational permits, and a Dense Media Separation plant already delivered to site, it occupies a category that relatively few junior lithium assets worldwide can legitimately claim: genuinely construction-ready.

When big ASX news breaks, our subscribers know first

Why Minas Gerais Is Not the Same as the Lithium Triangle

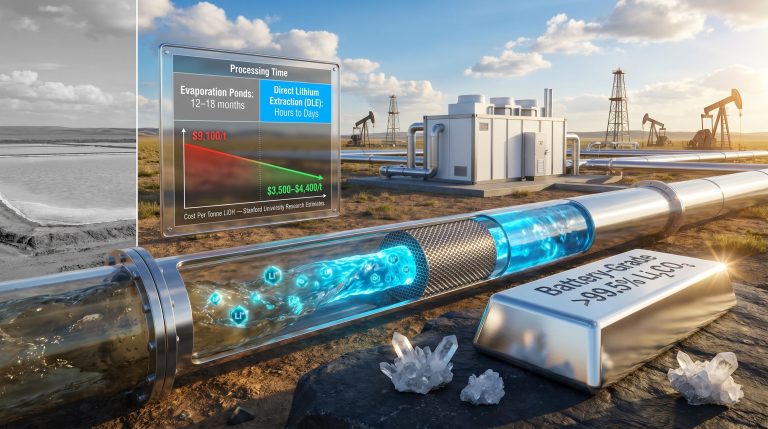

Most mainstream coverage of South American lithium focuses almost exclusively on the brine-rich Atacama and Puna plateau regions spanning Chile, Argentina, and Bolivia. That framing overlooks something geologically and commercially significant: Brazil's Minas Gerais state hosts a distinct and historically productive pegmatite belt that produces hard-rock spodumene deposits, not brines.

The distinction matters enormously from a processing and supply chain perspective. Lithium brine operations require vast evaporation ponds, multi-year processing timelines, and produce lithium carbonate as a primary output. Hard-rock pegmatite operations, by contrast, use established crushing and separation technologies to produce spodumene concentrate (typically graded at 5.5% to 6% Li₂O) within months of commissioning, with that concentrate then shipped to converters who produce battery-grade lithium hydroxide or carbonate.

This geological difference translates into a fundamentally different risk and financing profile:

| Region | Deposit Type | Primary Product | Processing Complexity | Geopolitical Risk |

|---|---|---|---|---|

| Minas Gerais, Brazil | Hard-rock (spodumene/pegmatite) | Lithium concentrate | Moderate | Low–Medium |

| Atacama, Chile | Brine | Lithium carbonate/hydroxide | High (evaporation) | Medium |

| Pilbara, Australia | Hard-rock (spodumene) | Lithium concentrate | Moderate | Low |

| Sichuan, China | Mixed | Carbonate/hydroxide | High | High (sovereign) |

| Nevada, USA | Sedimentary/clay | Carbonate | Very High | Low |

Minas Gerais also benefits from Brazil's most developed mining infrastructure corridor, including rail connections to deep-water Atlantic export ports such as Tubarão and Açu, an established power grid, and a deep regional labour pool with hard-rock mining expertise built over decades of iron ore and gold production. These structural advantages meaningfully reduce greenfield development costs compared to more remote Brazilian states.

Dense Media Separation: Understanding the Technology Behind the Neves Project

One element of the Neves Project that deserves more analytical attention than it typically receives is the processing technology choice. The project uses Dense Media Separation (DMS), and the plant has already been physically delivered to Brazil — a milestone that distinguishes paper-based feasibility from tangible infrastructure deployment.

DMS works by suspending crushed ore in a liquid medium of calibrated density. Lithium-bearing spodumene minerals, being less dense than most associated waste minerals, float to the surface and are separated mechanically. Furthermore, the process is closely related to spodumene extraction methods proven across multiple operating mines globally. The process is:

- Proven at commercial scale across multiple operating spodumene mines in Australia and Africa

- Lower capital intensity than flotation or hydrometallurgical alternatives

- Operationally simpler, reducing the technical risk associated with first-time commissioning

- Well-understood by offtake buyers, meaning the concentrate quality profile is predictable and bankable

The choice of DMS over more complex processing routes is a deliberate capital efficiency decision. It keeps the ~US$60 million capex figure credible and positions the project for faster commissioning once full funding is confirmed.

A DMS plant delivered to site is not a trivial milestone. In the junior mining world, equipment procurement and delivery represents a meaningful portion of total project risk. Its arrival in Brazil signals that the Neves Project has moved from the study phase into the physical construction pipeline.

Benchmarking the US$60 Million Capex Against the Brazilian Lithium Peer Group

Context matters when evaluating capital expenditure figures. The ~US$60 million estimate for the Neves Project positions it at the capital-efficient end of the hard-rock lithium development spectrum, particularly when benchmarked against other Minas Gerais operations. In addition, Atlas Lithium has hired four engineering and construction companies to support this development, further validating its construction-ready status:

| Project | Company | Stage | Est. Capex | Technology |

|---|---|---|---|---|

| Neves Project | Atlas Lithium | Construction-ready (DFS complete) | ~US$60M | Dense Media Separation |

| Grota do Cirilo | Sigma Lithium | Operating | ~US$120M+ | Proprietary "Greentech" |

| Salinas Project | Latin Resources | Advanced exploration | TBD | TBD |

| Bandeira Project | Lithium Ionic | PFS stage | TBD | Hard-rock processing |

At US$60 million, the Neves Project sits in what capital markets practitioners sometimes describe as the financing sweet spot for junior resource development: large enough to be commercially meaningful, but small enough to be financed without requiring a Tier 1 mining house as a cornerstone partner. Projects at this scale can realistically access a combination of equity raises, royalty streaming arrangements, or project-level debt facilities without surrendering operational control.

It is worth noting that Sigma Lithium's Grota do Cirilo, the benchmark operating asset in the same state, required more than double the capital to reach production. The Neves Project's leaner footprint reflects either a more modest initial production scale, a modular development philosophy, or both — each of which has distinct implications for ramp-up timelines and revenue forecasting.

Three Development Scenarios and Their Probability Weightings

Sophisticated investors rarely evaluate a junior mining asset against a single outcome. Scenario modelling across multiple capital and partnership pathways provides a more realistic picture of how value could be realised:

Scenario 1: Independent Construction and Operation

Atlas Lithium raises equity and secures project-level debt to self-fund construction. The DMS plant is commissioned within 12 to 18 months of full funding confirmation. Spodumene concentrate is sold to Asian or European converters. Revenue is directly exposed to spot market pricing, which has ranged from approximately US$400 per tonne to over US$8,000 per tonne between 2020 and 2023 — a volatility range that demands careful hedging strategy.

Scenario 2: Offtake-Backed Strategic Financing

A major battery manufacturer, Japanese trading house, or European automaker provides advance financing in exchange for long-term concentrate supply rights. This model, successfully employed by multiple Australian and African spodumene producers, reduces equity dilution while compressing construction timelines. South Korean and Japanese battery supply chain participants have been particularly active in securing upstream spodumene offtake as a hedge against Chinese processing dependency.

Scenario 3: Acquisition or Joint Venture by a Major Mining House

A Tier 1 diversified miner acquires a controlling stake or establishes a joint venture. The completed DFS and permitting position Neves as an attractive bolt-on for any large-cap miner seeking near-term production growth without bearing exploration-stage risk. Precedent activity within Minas Gerais, including strategic partnership structures executed by Sigma Lithium, supports the plausibility of this pathway.

The IRA Policy Gap and What It Means for Brazilian Lithium Investors

Presenting the Atlas Lithium Brazilian US$60 million project in the United States is not simply a capital-raising exercise. It reflects a deliberate positioning strategy aimed at a North American investor base that has been significantly reshaped by the Inflation Reduction Act (IRA) and its critical minerals provisions.

The IRA's clean vehicle tax credit framework requires that qualifying percentages of battery materials originate either domestically or from countries holding free-trade agreements with the United States. Brazil does not currently hold such an agreement, which creates a structural policy gap that limits direct IRA qualification for Brazilian-sourced spodumene.

However, several nuances deserve attention. Consequently, investors navigating the global lithium market are actively repositioning around these policy uncertainties:

- Ongoing U.S.–Brazil bilateral trade discussions have elevated the strategic relevance of Brazilian critical minerals to Washington policymakers

- The broader "friend-shoring" policy framework specifically identifies Brazil as a preferred partner for supply chain diversification, even absent a formal FTA

- IRA implementation regulations have demonstrated flexibility in their interpretation of qualifying criteria, with amendments and guidance documents issued at irregular intervals

- Investors are actively positioning ahead of potential policy evolution, meaning Brazilian lithium assets may carry optionality value tied to a future FTA or equivalent bilateral agreement

The absence of a formal U.S.–Brazil free-trade agreement means Brazilian lithium currently sits outside direct IRA qualification pathways. However, ongoing bilateral dialogue and the friend-shoring framework suggest this gap may narrow — a development that could materially re-rate Brazilian lithium asset valuations if it materialises.

The next major ASX story will hit our subscribers first

Key Risk Factors Investors Should Quantify

No development-stage lithium asset is without material risk. For the Neves Project specifically, the following variables warrant rigorous independent assessment:

- Lithium price cyclicality: Spodumene concentrate experienced a collapse from peak pricing above US$8,000/t in late 2022 to below US$1,000/t by mid-2024, illustrating the severity of downside scenarios in an oversupply environment

- Currency exposure: The project carries a U.S.-dollar-denominated capex against Brazilian real-denominated operating costs; BRL/USD movements can significantly affect the real-terms cost of production

- Construction execution risk: Delivering a US$60 million project on schedule in a developing market jurisdiction requires disciplined contractor management and contingency planning

- Offtake clarity: Without a confirmed long-term offtake agreement at the time of writing, post-commissioning revenue visibility remains a key outstanding variable

- Regulatory continuity: Brazilian environmental licensing frameworks have undergone periodic revision; sustained policy stability in Minas Gerais is an ongoing assumption embedded in project economics

Disclaimer: This article is intended for informational and educational purposes only. Nothing contained herein constitutes financial, investment, or legal advice. Readers should conduct independent due diligence and seek qualified professional advice before making any investment decisions. All forward-looking statements, scenario projections, and financial estimates referenced in this article involve inherent uncertainty and may not reflect actual outcomes.

Brazil's Industrial Policy Ambition: From Concentrate Exporter to Battery Value Chain Participant

A dimension of the Neves Project's long-term value that extends beyond the DFS and capex figure is the evolving industrial policy context within Brazil itself. The Brazilian federal government has publicly identified lithium as a priority critical mineral, with active policy discussions centred on incentivising downstream processing within Brazilian borders rather than exporting raw spodumene concentrate.

If Brazil successfully transitions from a concentrate-exporting jurisdiction to one capable of producing battery-grade lithium hydroxide domestically, the economics of assets like the Neves Project would change fundamentally. Lithium hydroxide commands a significant price premium over spodumene concentrate — typically in the range of three to five times the concentrate value on a per-tonne basis — and would position Brazilian producers much closer to the end-use battery manufacturing market. Technologies such as direct lithium extraction may also play a role in enabling this transition as the sector matures.

This policy trajectory is speculative at this stage, and execution risk is substantial. However, for long-horizon investors, the optionality embedded in a well-located Minas Gerais pegmatite asset extends well beyond its initial production scenario. Furthermore, S&P Global's lithium market intelligence consistently highlights Brazil's emerging role as a strategically significant supplier within the broader critical minerals landscape.

FAQ: Atlas Lithium and the Neves Project

What exactly is the Neves Project?

A hard-rock lithium development asset in Minas Gerais, Brazil, operated by Atlas Lithium. It has completed a DFS, secured operational permits, and received its DMS processing plant on site.

Why does the US$60 million capex matter?

It places the project in a capital-efficient development tier that can be financed without mandatory Tier 1 mining house involvement, while remaining commercially significant enough to attract institutional and strategic capital.

Is the project located in the United States?

No. The project is entirely in Brazil. The US$60 million figure refers to the estimated capital expenditure denominated in U.S. dollars. Atlas Lithium has been presenting this Brazilian asset to U.S.-based investors as part of its cross-border capital strategy.

What processing method does the project use?

Dense Media Separation, the industry-standard technology for hard-rock spodumene operations, which has been physically delivered to the project site in Brazil.

What is the primary risk to project economics?

Lithium price volatility represents the most immediate variable. Spodumene concentrate pricing history demonstrates the potential for severe and rapid price corrections, making revenue forecasting inherently uncertain for any pre-production lithium asset.

Want To Stay Ahead Of The Next Major Mineral Discovery On The ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex data across more than 30 commodities into clear, actionable insights for investors at every level. Start your 14-day free trial today and explore how historic discoveries have generated extraordinary returns.