June 3, 2026

How Nuclear Utility Procurement Cycles Are Reshaping the Junior Uranium Development Landscape

The uranium market operates on procurement timelines that most commodity sectors would find extraordinary. Nuclear utilities typically plan fuel purchases five to ten years in advance, creating a procurement environment where early-stage developers who can demonstrate commercial credibility gain disproportionate advantages over peers still chasing resource milestones. This structural dynamic has intensified considerably since 2022, when the geopolitical fracturing of established uranium supply chains accelerated utility procurement urgency to a degree not seen since the post-Fukushima restocking cycle of the mid-2010s.

Against this backdrop, the Aura Energy Tiris uranium project nuclear utility deal represents something more analytically interesting than a standard junior developer announcement. It reflects a convergence of commercial, technical, and financing milestones that, taken together, suggest the project has crossed a threshold separating aspirational development assets from commercially validated pre-production opportunities.

When big ASX news breaks, our subscribers know first

What Makes a Nuclear Utility Offtake Agreement Different From Other Commodity Deals

The Structural Logic of Uranium Term Contracts

Uranium offtake agreements are not simply sales contracts. They are, in practice, creditworthiness certificates issued by the buyer to the seller. When a Fortune 500, investment-grade nuclear utility signs even a non-binding memorandum of understanding with a junior developer, it signals that the utility's procurement team has conducted sufficient due diligence to consider the project a credible future supplier.

This matters because uranium project financing is notoriously difficult to assemble without demonstrated demand. Unlike base metals, where spot market liquidity provides a financing backstop, the uranium supply deficit and thin spot market mean that lenders require term contract visibility before committing senior debt. The offtake agreement effectively unlocks the financing conversation.

"In uranium project development, a signed offtake arrangement with a creditworthy nuclear utility carries more de-risking weight than a resource upgrade or a completed feasibility study, because it validates that real demand exists at the price level required to underpin project economics."

Collar Pricing: A Mechanism Worth Understanding

One feature of the Aura Energy Tiris nuclear utility deal that deserves careful attention is the collar pricing structure attached to the offtake terms. A collar arrangement in uranium contracting sets both a price floor and a price ceiling for deliveries over the contract term.

For producers, the floor is critical: it must sit above projected all-in production costs to ensure the contract is economically accretive rather than destructive. For buyers, the ceiling provides budget certainty in a commodity known for episodic price volatility. The collar therefore performs a dual risk-management function that aligns the economic interests of both parties.

Importantly, the price floor in the Aura Energy arrangement has been disclosed as sitting above forecast production costs, which is a prerequisite condition for any bankable feasibility study to present a viable project economics case. Lenders will model downside scenarios against the floor price, not against spot prices, making the floor level arguably the single most important commercial number in the entire financing structure.

The Tiris Uranium Project: Scale, Structure, and Strategic Context

Project Fundamentals

The Tiris uranium project is located in the Tiris region of northeastern Mauritania, an area geologically characterised by surficial uranium mineralisation hosted within sandstone and calcrete-type deposits. This deposit style is operationally significant: surficial uranium systems are typically amenable to low-strip-ratio open-pit mining and relatively straightforward processing, which supports the capital intensity profile that makes Tiris competitive on a global cost curve basis.

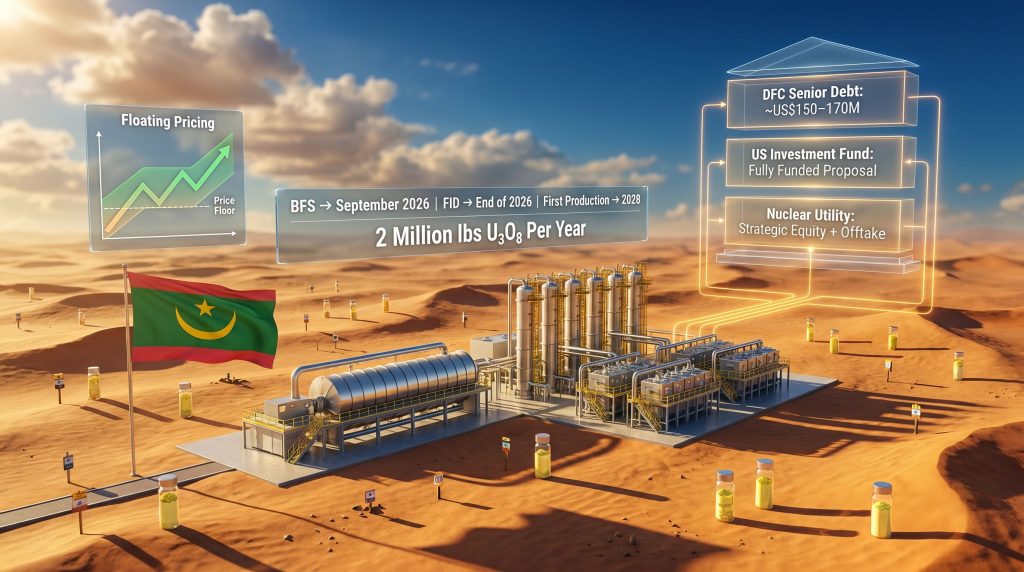

The project's base-case design targets annual production of 2 million pounds of uranium oxide (U₃O₈), with an evaluated expansion pathway to 3.5 to 4 million pounds per year. Over a projected 25-year mine life, cumulative production under the base case would approach 50 million pounds of uranium oxide equivalent, positioning Tiris as a material contributor to global primary supply if it reaches production.

Ownership and Government Partnership

| Stakeholder | Ownership Interest |

|---|---|

| Aura Energy (via Tiris Resources SA) | 85% |

| Mauritanian Government | 15% |

The 15% government equity position is a standard feature of mining investment frameworks across West Africa, designed to align sovereign interests with project development. From a financing perspective, government co-ownership can function as a political risk mitigant by giving the host state a direct economic stake in project success. It also introduces a governance layer that project debt providers typically evaluate carefully during due diligence.

Tiris would become Mauritania's first uranium mine and the country's first new mining project of any material scale in approximately 20 years, a distinction that carries both political significance and infrastructure development implications for the region.

Why West African Uranium Supply Is Attracting Renewed Attention

The post-2022 restructuring of Western uranium procurement strategies has elevated non-Russian, non-Central Asian supply sources considerably in utility procurement rankings. Historically, Kazakhstan, Russia, and Uzbekistan collectively supplied a substantial portion of Western utility uranium requirements, either directly or through conversion and enrichment services. Furthermore, the US ban on Russian uranium introduced in 2024 has altered that calculus materially, creating a structural preference among US utilities for supply originating from jurisdictions outside the Russian supply chain ecosystem.

Mauritania's location in West Africa, combined with its comparatively stable investment environment relative to Sahel neighbours, positions Tiris as a geographically diversified supply option at a moment when such diversification carries a genuine procurement premium.

Dissecting the Commercial Architecture: Term Offtake Plus Spot Access

The Nuclear Utility MOU: Key Commercial Parameters

| Term | Detail |

|---|---|

| Counterparty Classification | Major US nuclear utility (Fortune 500, investment-grade) |

| Volume Coverage | Approximately 10% of projected annual base-case output |

| Contract Duration | Four-year term: 2028 to 2031 |

| Pricing Mechanism | Market-related within a collar structure |

| Price Floor | Above forecast production costs |

| Condition Precedent | Subject to financing completion and FID |

The counterparty's identity has been withheld at the nuclear company's request, a practice that is not unusual in uranium contracting given the commercially sensitive nature of utility procurement strategies. The MOU signed with the nuclear utility encompasses potential strategic equity investment, uranium offtake arrangements, technical collaboration, and funding support, reflecting a multi-dimensional relationship rather than a simple purchase agreement.

The Master Spot Sales Agreement: A Second Commercial Layer

Alongside the utility MOU, Aura Energy has established a master spot sales agreement with a global uranium trading group. This agreement provides access to spot market sales and conversion facilities across the United States, Europe, France, and Canada, preserving optionality to sell volumes not committed under the term contract at prevailing market prices.

This dual-channel structure, combining a term offtake with a Fortune 500 utility and a separate spot market access facility, is a relatively sophisticated commercial arrangement for a project that has not yet reached final investment decision. It reflects deliberate portfolio risk management: the term contract provides revenue floor certainty while the spot channel captures upside in a rising price environment.

"The combination of a structured term offtake and an active spot market sales agreement gives Tiris a commercial architecture that mirrors the approach used by established mid-tier uranium producers, not a project still assembling its financing package."

Processing Technology: Why the Flowsheet Decision Matters More Than It Appears

The Selected Processing Design

The confirmation of Tiris's processing flowsheet has been described as the project's most important technical milestone to date. The selected design incorporates three core components:

- Pre-leach centrifuge separation for ore preparation and gangue material rejection ahead of the leach circuit, reducing the volume of material requiring chemical processing

- Polymer-based dewatering technology for efficient solid-liquid separation following leaching, with direct implications for reagent consumption and tailings management

- Horizontal vacuum belt filtration as the final dewatering stage, an industry-standard technology with well-established capital and operating cost benchmarks

Each of these components is drawn from commercially proven process technology with established vendor supply chains and documented performance records at operating uranium facilities. This is not a trivial distinction. Projects that incorporate novel or unproven processing elements face substantially higher technical risk assessments from project debt providers, which can translate directly into higher financing costs or reduced debt capacity.

By anchoring the flowsheet to proven technology, Tiris's bankable feasibility study can reference real-world operating data rather than laboratory projections. This strengthens the credibility of capital and operating cost estimates with lenders and equity investors alike.

The Capital Stack: Three Funding Pillars and What Each Means

Financing Structure Overview

| Funding Source | Type | Amount / Status |

|---|---|---|

| US International Development Finance Corporation (DFC) | Senior Project Debt | Approximately US$150-170 million (advanced discussions) |

| Major US Investment Fund | Equity / Debt Proposal | Non-binding; fully funded proposal received |

| Nuclear Utility MOU | Strategic Equity + Offtake | Under negotiation |

The DFC Engagement: Strategic Dimension Beyond the Dollar Amount

The US International Development Finance Corporation is the United States government's development finance institution, with a mandate that includes supporting supply chain resilience for critical minerals. DFC engagement in a project of this nature reflects the institution's assessment that the asset meets its investment criteria, which include development impact, financial viability, and strategic alignment with US interests.

It is important to note that discussions with the DFC remain advanced but not concluded. No binding commitment has been announced. However, DFC engagement at the level of discussing a US$150 to $170 million senior debt facility is a commercially significant signal, as the institution conducts substantial due diligence before advancing to this stage of discussions with any project counterparty.

The Fully Funded Equity Proposal: Reading Between the Lines

The receipt of a non-binding fully funded proposal from a major US investment fund indicates that at least one institutional equity party has assessed the total project capital requirement and indicated willingness to provide a comprehensive funding solution. Non-binding status means the economic terms, governance arrangements, and equity dilution parameters remain subject to negotiation.

Investors should note that the gap between a non-binding proposal and a signed funding agreement can be significant, particularly where complex equity structures and project finance covenants intersect. For context, comparable situations such as the Alta Mesa uranium project illustrate how nuanced these financing negotiations can become before a final commitment is reached.

The next major ASX story will hit our subscribers first

Critical Path: From Feasibility Study to First Production

The Development Timeline

Bankable Feasibility Study Completion → September 2026

Final Investment Decision Target → End of 2026

Construction Commencement → H1 2027 (implied)

First Production / Offtake Commencement → 2028

Five Conditions That Must Be Met Before FID

- Completion and independent acceptance of the bankable feasibility study

- Finalisation and signing of the DFC senior debt facility

- Conversion of the nuclear utility MOU into a binding offtake agreement

- Resolution of the equity and co-funding package with the US investment fund

- Satisfaction of all regulatory and environmental approvals in Mauritania, including the environmental and social impact assessment update

Each of these conditions carries its own execution timeline and risk profile. The binary nature of the FID deadline is particularly important: if the offtake MOU includes a condition requiring FID to be achieved by a specified date, timeline slippage in any of the five workstreams above could trigger a renegotiation obligation with the utility counterparty.

"Investors should treat the bankable feasibility study completion date as the primary leading indicator of whether the December 2026 FID target remains achievable. Any delay to the BFS will cascade through the remaining milestones."

Risk Framework: What Remains Unresolved

Project-Level Risks

| Risk Category | Description |

|---|---|

| Financing completion risk | Senior debt and equity package not yet fully committed or signed |

| FID timing risk | December 2026 target depends on multiple parallel workstreams closing simultaneously |

| Offtake conditionality | Utility MOU remains conditional on financing and FID achievement |

| Permitting and regulatory risk | Mauritanian ESIA update and approvals process |

| Geopolitical and sovereign risk | Regional security environment and host government relations |

Capital Cost Reference Points

The base-case capital cost estimate for Tiris sits at approximately US$230 million, covering construction of a facility designed to produce a life-of-mine average of approximately 1.8 million pounds of uranium oxide equivalent per year. This reflects ramp-up and end-of-mine-life production profiles against the nominal 2 million pound design capacity. An expansion to 3.5 to 4 million pounds per year would require additional capital, the quantum of which is subject to the ongoing expansion evaluation.

These figures remain pre-BFS estimates and should be treated with appropriate caution. A definitive feasibility study frequently revises capital cost estimates relative to earlier scoping or pre-feasibility work, particularly for projects in frontier jurisdictions where infrastructure costs and logistics variables are more difficult to pin down at earlier study stages.

This article is intended for informational purposes only and does not constitute financial or investment advice. All forward-looking statements and projections are subject to material risks and uncertainties. Readers should conduct their own independent research and seek qualified financial advice before making any investment decision.

Three Scenarios for the Tiris Development Trajectory

Scenario 1: Base Case Execution

The financing package closes on schedule through 2026. The DFC senior debt facility is formalised, the US investment fund proposal converts to a binding commitment, and the utility MOU transitions to a signed offtake agreement following BFS completion in September. FID is confirmed in December 2026, construction commences in the first half of 2027, and first production is achieved in 2028 as targeted under the offtake arrangement.

Scenario 2: Accelerated Expansion Integration

The BFS incorporates the expanded 3.5 to 4 million pound per year capacity scenario, supported by additional offtake agreements with European or Asian utilities seeking non-Russian supply. The DFC debt facility is upsized to accommodate higher capital requirements, and a second utility relationship is formalised. This scenario would likely push first production into late 2028 or 2029 but significantly improves the project's long-term economics and financing leverage.

Scenario 3: Financing Delay and Renegotiation

One or more financing workstreams encounters execution complexity, pushing the BFS or funding package beyond the December 2026 deadline. The utility MOU's conditionality provisions are triggered, requiring commercial renegotiation. First production shifts toward 2029 to 2030. This scenario does not necessarily indicate project failure, but it resets the commercial terms negotiated under more favourable market conditions.

From Exploration Asset to Commercially Validated Development Project

The Aura Energy Tiris uranium project nuclear utility deal, considered alongside the DFC financing discussions, the settled processing flowsheet, and the master spot sales agreement, represents a qualitative shift in project status that goes beyond what any single milestone could achieve in isolation. The combination of a Fortune 500 utility counterparty, a dual-channel commercial structure, and a commercially proven processing design addresses three of the most common failure modes for junior uranium developers simultaneously: demand uncertainty, revenue concentration risk, and technical execution risk.

What the next six months will determine is whether the financing architecture can be assembled completely enough to support a credible FID. The bankable feasibility study completion in September 2026 will be the pivotal moment, providing the foundational document against which every remaining financing and commercial decision will be assessed. Until that document is in the hands of lenders, utility counterparties, and equity investors, the project remains a well-structured development opportunity rather than a financed construction project.

For those tracking the uranium market dynamics and the global uranium development pipeline, Tiris deserves attention not merely as a single-company story, but as a case study in how the convergence of supply chain politics, utility procurement urgency, and development finance institution mandates is reshaping the economics of new uranium mine development outside the traditional producing regions.

Want to Track the Next Major Uranium Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex commodity data to surface actionable opportunities the moment they're announced. Explore historic discoveries and their market-moving returns, then begin your 14-day free trial to position yourself ahead of the broader market.