June 2, 2026

The Infrastructure Deficit Shaping America's Nuclear Future

The global uranium enrichment industry operates on a fundamental tension between the long lead times required to build physical infrastructure and the unpredictable geopolitical shocks that can reshape demand almost overnight. Centrifuge cascades take years to design, license, manufacture, and commission. Reactors, once built, operate for decades. When a political decision disrupts an established supply chain, the gap between policy intent and physical reality can stretch years into the future. That structural reality sits at the heart of the current transformation underway at the only commercial-scale uranium enrichment facility in the United States.

Understanding what the Urenco USA uranium enrichment expansion actually means requires more than tracking megawatts or SWU figures. It requires appreciating just how concentrated, fragile, and historically overlooked the upstream nuclear fuel cycle has been.

When big ASX news breaks, our subscribers know first

The Hidden Fragility of the US Uranium Fuel Cycle

Most discussion of nuclear energy focuses on reactors, megawatt capacity, and carbon emissions. Far less attention has historically been paid to the industrial processes that convert raw uranium ore into the precise, specification-grade enriched fuel that reactors actually consume. Enrichment sits at the middle of this chain, sandwiched between uranium mining and conversion on one side and fuel fabrication on the other.

The degree to which the US allowed its domestic enrichment capacity to atrophy is striking in retrospect. The country that pioneered nuclear technology, primarily through gaseous diffusion enrichment plants during the Cold War era, entered the 2020s with a single operating commercial enrichment facility. That facility, the National Enrichment Facility (NEF) in Eunice, New Mexico, operated by Urenco USA, has been running since 2010 and has attracted reported cumulative investment exceeding $5 billion in US manufacturing infrastructure since its development.

The NEF currently produces 4.3 million separative work units (SWU) per year, which covers roughly one-third of total US commercial reactor enrichment requirements. The remaining two-thirds has historically been sourced from international suppliers, with Russia's state-backed Rosatom subsidiary TENEX accounting for approximately one-fifth of US enrichment demand as recently as two years before the 2024 import ban was enacted. Furthermore, the uranium supply challenges associated with this concentration of supply have become increasingly difficult to ignore.

The combination of a single domestic enrichment facility and deep historical reliance on Russian supply created a structural vulnerability that no short-term procurement adjustment could resolve. Only the physical expansion of domestic infrastructure could close that gap.

What Is a Separative Work Unit and Why Does It Matter?

The SWU is not widely understood outside specialist circles, yet it is the fundamental unit of measurement governing enrichment economics and capacity planning.

| Term | Definition | Relevance to Reactors |

|---|---|---|

| SWU (Separative Work Unit) | A measure of the energy and effort required to enrich uranium to a specific U-235 concentration | Determines annual fuel production capacity of a facility |

| LEU (Low-Enriched Uranium) | Uranium enriched to below 20% U-235 | Standard fuel for conventional light water reactors |

| LEU+ | Uranium enriched between 5% and 10% U-235 | Required for advanced reactor designs and SMRs |

| Natural Uranium | Contains approximately 0.7% U-235 | Must be enriched before use in most reactors |

In practical terms, a reactor requiring 100,000 SWU per year of enrichment services would consume roughly 2.3% of the NEF's current annual output. The US commercial reactor fleet of approximately 90 operating units collectively requires an estimated 13 million SWU per year, meaning the NEF currently supplies around one-third of that figure.

What the Urenco USA Expansion Actually Involves

The scale of the planned expansion is significant by any measure. The programme unfolds in two distinct phases, each with separate timelines, capital commitments, and strategic objectives.

Phase One: Near-Term Capacity Addition (2025 to 2027)

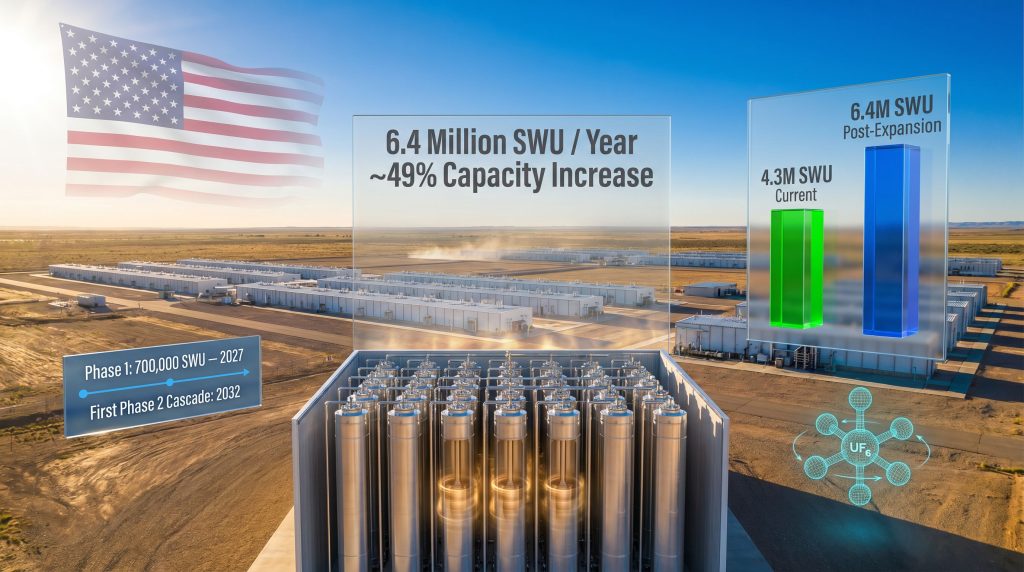

The first phase is already underway. Urenco USA has commenced a 700,000 SWU capacity addition at the Eunice facility, representing approximately a 15% increase in existing plant output. Multiple new centrifuge cascades from this phase have reportedly come online ahead of schedule and within budget, which carries important implications for regulatory confidence and investor credibility as the larger Phase Two programme is developed.

This near-term addition is part of a broader Urenco Group programme targeting 2.5 million SWU of additional capacity across its facilities in the US, Netherlands, and Germany combined.

Phase Two: The Multibillion-Dollar Long-Term Build

The larger and more consequential component involves the installation of 24 sets of centrifuge cascades at the Eunice site. This phase will add 2.1 million SWU of enrichment capacity, bringing the NEF's projected total annual output to approximately 6.4 million SWU, representing a ~49% increase over current levels.

The first new cascade set from this long-term programme is expected to be operational by 2032, with the full build-out completing within approximately six years of announcement.

Urenco CEO Boris Schucht confirmed that the expansion is designed to directly support the long-term needs of US utility customers and the broader energy security objectives of the United States. The emphasis on long-term customer commitments is notable, suggesting that substantial portions of the additional capacity are already being contracted in advance.

| Milestone | Target Timeline |

|---|---|

| Phase 1 expansion commencement | 2025 |

| Phase 1 completion (700,000 SWU added) | 2027 |

| First Phase 2 cascade set operational | 2032 |

| Full Phase 2 completion (2.1M SWU added) | ~2031-2032 |

| Total NEF capacity post-expansion | ~6.4M SWU/year |

LEU+: A Technical Capability With Long-Term Commercial Consequences

Alongside the capacity expansion, the US Nuclear Regulatory Commission (NRC) has authorised Urenco USA to enrich uranium to concentrations of up to 10% U-235, qualifying the facility to produce LEU+. This is technically and commercially significant because it opens the facility to a new and growing category of customer: operators of advanced reactor designs and small modular reactors (SMRs) that require higher-assay fuel than conventional light water reactors.

Most commercial enrichment facilities are licensed and optimised for standard LEU production in the 3% to 5% U-235 range. The ability to produce fuel at concentrations up to 10% is not universally available and positions Urenco USA as a critical supplier for the next generation of US reactor designs currently in development and early deployment. Consequently, the uranium market dynamics around LEU+ demand are expected to shift meaningfully as SMR deployments gather pace.

LEU+ is not simply a technical footnote. As SMR deployments accelerate across the US through the 2030s, demand for higher-assay fuel will grow substantially. Facilities with existing LEU+ authorisation will hold a meaningful first-mover advantage in this segment.

The Geopolitical Catalyst: Russia's Enrichment Dominance and the 2024 Ban

The urgency behind the Urenco USA uranium enrichment expansion cannot be fully appreciated without understanding the scale of Russia's grip on the global enrichment market.

| Enrichment Provider | Country | Estimated Global Market Share |

|---|---|---|

| TENEX / Rosatom | Russia | ~35-40% |

| Urenco | UK / Netherlands / Germany / US | ~25-30% |

| Orano | France | ~15% |

| CNNC | China | ~10% |

| Other | Various | ~5-10% |

Russia did not achieve this position through low-cost natural resources alone. Rosatom's dominance reflects decades of sustained state investment in centrifuge technology, downstream conversion and fabrication integration, and aggressive long-term contract pricing that made Russian enrichment economically difficult for utilities to bypass even when geopolitical tensions were rising.

The US ban on Russian uranium imports, enacted in 2024, severed access to a supplier that had provided approximately one-fifth of US enrichment demand. Limited contract waivers remain available until 2028, providing a transitional window, but utilities that have relied on Russian-origin enrichment services must fundamentally restructure their fuel procurement portfolios before that deadline expires.

The structural consequence is a period of acute demand pressure on Western enrichers, particularly Urenco and France's Orano, who must together absorb the demand previously served by Russian supply. With Orano operating primarily in European and global markets, Urenco USA faces the most concentrated domestic pressure to expand.

A Parallel That Captures the Scale: Manhattan Project 2.0

Some industry observers have framed the current domestic nuclear fuel buildout as comparable in ambition, if not in mechanism, to the original Manhattan Project. The comparison is instructive but incomplete. The Manhattan Project was a government-directed, weapons-focused, time-compressed emergency programme. The current effort is commercially driven, civilian in purpose, and measured in decades rather than years.

What the comparison captures accurately is the scale of industrial mobilisation required to rebuild a domestic nuclear fuel infrastructure that was systematically allowed to decline over decades of post-Cold War complacency. The NEF has operated since 2010 and now represents the accumulated foundation upon which a significantly larger domestic capacity base must be built.

Demand Projections and the Arithmetic of Sufficiency

Even after the combined Phase 1 and Phase 2 additions are complete, the capacity arithmetic reveals that the Urenco USA uranium enrichment expansion solves the near-term supply gap without resolving the longer-term structural shortfall.

| Demand Scenario | Estimated Annual SWU Requirement | NEF Coverage Post-Expansion |

|---|---|---|

| Current US reactor fleet | ~13 million SWU | ~49% (6.4M SWU) |

| Moderate fleet expansion | ~15-16 million SWU | ~40-43% |

| Nuclear quadrupling scenario | ~26-30 million SWU | ~21-25% |

The US administration's stated policy target of quadrupling domestic nuclear power output would require enrichment capacity to increase proportionally. At that scale, even a fully expanded NEF would supply only around one-fifth of total enrichment demand. This arithmetic strongly implies that additional domestic enrichment investment, whether from new entrants or further Urenco expansion, will be necessary over the coming two decades.

The US Energy Information Administration issued a formal warning in September 2025 that American reactor operators face potential uranium fuel shortages over the coming decade. That assessment underlines the urgency of the current expansion and simultaneously signals that the NEF buildout, while substantial, is unlikely to be the last word in domestic enrichment capacity development. In addition, the uranium supply-demand volatility being observed across global markets further reinforces this concern.

The AI Data Centre Effect on Nuclear Demand

One of the more consequential demand drivers now being factored into nuclear fuel planning is the extraordinary electricity consumption growth associated with AI data centre proliferation across the United States. Unlike intermittent renewable sources, nuclear power offers dispatchable, 24/7 baseload generation that data centre operators require to maintain operational continuity.

This dynamic is accelerating both new reactor construction planning and life extension decisions for existing units, both of which translate directly into increased long-term enriched uranium demand. Several major technology companies have already signed agreements with nuclear operators, and the financial weight of that demand signal is beginning to flow upstream into enrichment capacity planning.

Centrifuge Technology: The Industrial Backbone of Enrichment

The centrifuge cascade technology at the core of the NEF expansion deserves specific attention because it differs fundamentally from the gaseous diffusion processes that defined the first generation of US enrichment infrastructure.

Gas centrifuge enrichment works by spinning uranium hexafluoride (UF6) gas at extremely high rotational speeds. Because U-238 is slightly heavier than U-235, centrifugal force causes the heavier isotope to migrate outward, allowing the lighter, fissile U-235 to be selectively extracted. Individual centrifuges achieve only small separation factors, so they are arranged in cascades, where each stage feeds incrementally enriched material into the next, progressively raising the U-235 concentration toward the target assay.

The operational advantages of centrifuge technology over older gaseous diffusion methods are substantial:

- Centrifuge enrichment uses approximately 50 times less electricity per SWU than gaseous diffusion

- Cascades can be modularly expanded by adding units, enabling the kind of phased capacity additions that Urenco is implementing

- The technology produces significantly lower carbon emissions per unit of output

- Individual centrifuge units can be replaced or upgraded without shutting down entire cascades

The installation of 24 new cascade sets at Eunice is therefore not a monolithic construction project but a structured, modular buildout that can be sequenced to match market demand and licensing milestones.

The next major ASX story will hit our subscribers first

What This Means for US Nuclear Utilities and Fuel Buyers

For reactor operators currently managing the transition away from Russian-origin enrichment services, the confirmed expansion timeline provides a credible planning anchor. The Phase 1 addition of 700,000 SWU by 2027 arrives within the Russian contract waiver window, offering partial domestic supply relief before the 2028 waiver expiry. The Phase 2 additions from 2032 onward provide structural medium-term supply security that utilities can incorporate into long-term fuel procurement planning.

Several strategic implications flow from this:

- Utilities evaluating new reactor construction can factor expanded domestic enrichment capacity into feasibility modelling with greater confidence

- Operators considering reactor life extensions have a clearer domestic fuel supply pathway extending into the 2030s and beyond

- Companies developing SMR projects that require LEU+ fuel have a confirmed domestic supplier with existing NRC authorisation

- Long-term supply contracts with Urenco USA now offer price visibility and supply certainty that was unavailable when domestic capacity was insufficient

Furthermore, the nuclear growth investment case has strengthened considerably as these structural supply-side developments have become more visible to capital markets. The Urenco USA uranium enrichment expansion also reinforces a broader trend in US industrial policy: the active domestication of critical supply chains that were allowed to become dangerously concentrated in adversarial or geopolitically vulnerable sources.

Uranium enrichment joins rare earth processing, battery materials, and semiconductor manufacturing as sectors where the US is investing to restore meaningful domestic industrial capacity.

The structural lesson from the Russian enrichment dependency is clear. Energy security in the nuclear sector is not simply about fuel reserves in the ground. It is about the full industrial chain from ore to enriched fuel, and every link in that chain must be domestically anchored or allied-nation secured.

The expansion underway in Eunice, New Mexico represents the most significant single investment in American enrichment infrastructure in a generation. Whether it proves sufficient will depend on how aggressively the US nuclear fleet actually expands over the coming decades, and how many additional investors decide to enter a domestic enrichment market that is, for the first time in years, showing clear and durable signals of long-term demand growth.

This article contains forward-looking statements and projections regarding energy demand, enrichment capacity timelines, and policy outcomes. These involve inherent uncertainties and should not be construed as investment advice. Readers should conduct independent due diligence before making any investment decisions related to uranium, nuclear energy, or related sectors.

Want to Capitalise on the Next Major Uranium Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore why major mineral discoveries have historically generated substantial returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market as uranium's structural supply transformation accelerates.