August 4, 2026

Australia's emergence as a central player in global critical minerals energy transition initiatives reflects the profound transformation occurring in international resource security relationships. The intersection of energy transition requirements, defence applications, and technological advancement has fundamentally altered how nations approach mineral resource dependencies, moving far beyond traditional commodity trade frameworks toward strategic security partnerships.

As governments worldwide develop comprehensive critical minerals strategy frameworks, the geopolitical landscape has shifted dramatically. Traditional market mechanisms prove insufficient when materials become essential for national security infrastructure, renewable energy systems, and advanced manufacturing capabilities that define modern economic competitiveness.

Understanding Australia's Strategic Mineral Diplomacy Framework

Defining Critical Minerals in Modern Geopolitical Context

Critical minerals represent a distinct classification system that extends far beyond traditional commodity frameworks. These materials possess unique characteristics that make them indispensable for modern technological applications while simultaneously creating significant supply chain vulnerabilities for dependent nations.

The United States designates 50 critical minerals as those where supply disruptions could threaten national security or economic welfare, establishing a framework that other allied nations have largely adopted. Japan, the European Union, and Australia have developed similar classification systems, though with variations reflecting their specific strategic priorities and existing supply dependencies.

Key Classification Criteria:

• Economic importance to essential industries and applications

• High supply risk due to geographic concentration or political instability

• Lack of suitable substitutes for critical applications

• Strategic importance for defence and clean energy sectors

These materials differ fundamentally from traditional commodities because their strategic value often exceeds their market value. When China restricted rare earth exports in 2010-2011, the global response demonstrated how quickly mineral trade can become a tool of international coercion rather than simple economic exchange.

Australia's Unique Position in Global Supply Chain Architecture

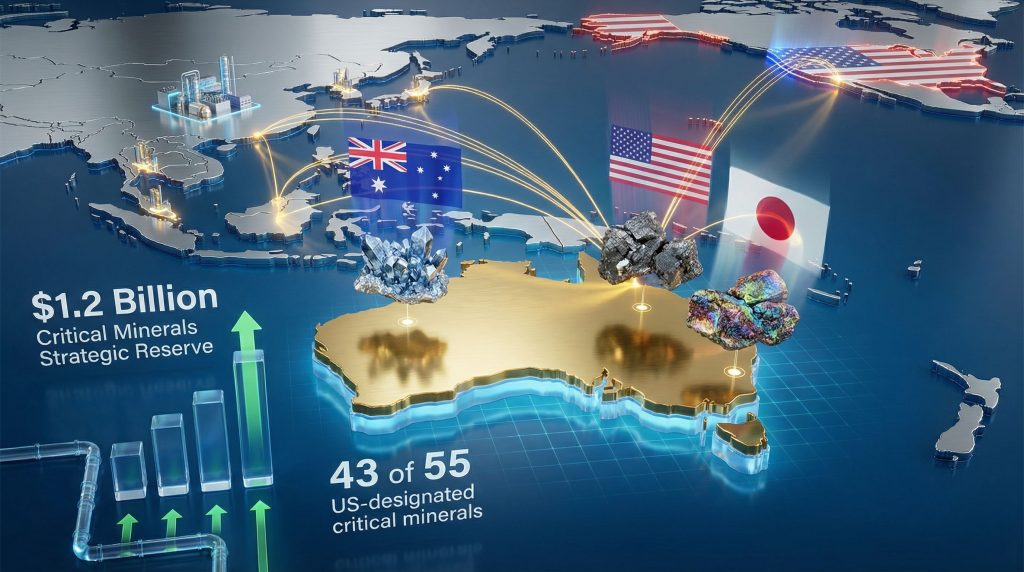

Australia possesses deposits of 43 of the 55 US-designated critical minerals, positioning it as one of the world's most resource-rich nations for the energy transition. This geological advantage represents more than mere mineral wealth; it provides the foundation for strategic partnerships and supply chain diversification initiatives across the Indo-Pacific region.

The country's competitive positioning stems from several converging factors that extend beyond raw geological endowments. Australia maintains one of the world's most advanced extractive resources sectors, with established mining infrastructure, regulatory frameworks, and proximity to major Indo-Pacific demand centres.

Australia's Strategic Advantages:

| Factor | Competitive Advantage | Strategic Implication |

|---|---|---|

| Geological Diversity | 43 of 55 critical minerals | Reduced single-source dependencies |

| Mining Infrastructure | Century of development experience | Rapid project deployment capability |

| Regulatory Stability | Established legal frameworks | Investment certainty for partners |

| Geographic Position | Indo-Pacific proximity | Lower transport costs and risks |

However, significant processing gaps create vulnerabilities in Australia's supply chain position. While the country excels at mineral extraction, it remains heavily dependent on overseas processing facilities, particularly those controlled by China. Furthermore, this processing bottleneck has become a central focus of strategic mineral diplomacy initiatives.

Federal Resources Minister Madeleine King emphasised that Australia remains a trusted, long-term and stable energy and resources partner for countries in the Indo-Pacific region, highlighting the nation's natural geology and advanced extractive resources sector as key competitive advantages.

Processing Capabilities and Strategic Vulnerabilities

The distinction between mineral extraction and processing represents the most critical vulnerability in global critical minerals supply chains. China currently processes an estimated 70-80% of the world's rare earth separation globally, creating a strategic chokepoint that affects even nations with domestic mining capabilities.

Australia's processing gap analysis reveals significant opportunities for value chain integration with allied partners. Joint investment in processing capabilities allows partner nations to reduce their exposure to potential supply disruptions while creating more resilient and diversified supply networks.

Processing Investment Examples:

• Iluka facility receiving $1.1 billion government investment for 2026 opening

• Arafura Resources expansion under bilateral framework agreements

• Technology transfer initiatives with Japanese and US partners

These investments represent more than industrial development; they constitute strategic infrastructure designed to reduce collective vulnerabilities to supply chain manipulation. The emphasis on processing capabilities reflects recognition that controlling mineral transformation is often more strategically valuable than controlling raw material extraction alone.

When big ASX news breaks, our subscribers know first

What Drives Australia's $1.2 Billion Critical Minerals Strategic Reserve?

Policy Architecture of the Critical Minerals Strategic Reserve

Australia's $1.2 billion Critical Minerals Strategic Reserve represents a fundamental shift toward demand-side certainty for private sector investment. This initiative operates through Export Finance Australia powers that authorise strategic stockpiling mechanisms, off-take agreements, and government backing designed to signal reduced geopolitical and market risk to private investors.

The strategic reserve functions as both market intervention tool and supply chain insurance policy. By providing guaranteed off-take agreements, the government can overcome what industry analysts term the "valley of death" in project development, where promising ventures fail due to uncertain future demand or commodity price volatility.

Reserve Implementation Timeline:

• 2026 operational deployment target

• Integration with $5 billion Critical Minerals Facility expansion

• Six-month bilateral framework implementation schedule

• $8.5-13 billion project pipeline activation potential

The legislative framework establishes mechanisms for strategic stockpiling that extend beyond traditional commodity storage. These reserves can be deployed to stabilise prices during supply disruptions, provide guaranteed markets for domestic producers, and serve as diplomatic tools for securing international partnerships.

Priority Mineral Selection and Strategic Rationale

The selection of minerals for strategic reserve inclusion reflects both current vulnerability assessments and future demand projections. Priority allocation considers defence applications, clean energy infrastructure requirements, and advanced technology dependencies that cannot be easily substituted or sourced from alternative suppliers.

Strategic Mineral Priorities:

| Mineral | Strategic Application | Current Dependency Risk | Reserve Priority Level |

|---|---|---|---|

| Antimony | Defence systems, flame retardants, electronics | 90% China-sourced dependency | High |

| Gallium | Semiconductors, solar panels, integrated circuits | China export ban effects since 2023 | Critical |

| Rare Earths | Permanent magnets, electronics, defence systems | Processing bottleneck outside China | Primary focus |

| Magnesium | Aerospace, automotive applications | Limited processing alternatives | Moderate |

| Germanium | Fibre optics, infrared systems | Export restrictions impact | High |

China's gallium and germanium export restrictions, effective from August 2023, demonstrated how quickly strategic materials can become unavailable through policy changes rather than geological scarcity. The Alcoa-Sojitz gallium project, formally announced in 2025 as a trilateral response involving Australia, Japan, and the United States, represents the template for future collaborative responses to such supply disruptions.

Market Intervention Mechanisms and Price Support

The strategic reserve employs sophisticated market intervention mechanisms that extend beyond simple stockpiling. Floor price agreements, such as the recently announced Japan Australia Rare Earths (JARE) Partnership arrangement with Lynas Rare Earths, provide minimum price guarantees that de-risk producer profitability and stabilise long-term investment returns.

These mechanisms recognise that critical minerals markets often fail to provide adequate investment signals due to their strategic rather than purely economic nature. Government intervention serves to bridge the gap between strategic necessity and market viability, ensuring adequate supply availability during potential crisis scenarios.

Price Support Mechanisms:

• Floor price guarantees for processed rare earths

• Off-take agreement terms extending 10-15 years

• Project development loan guarantees and tax incentives

• Risk insurance for geopolitical supply disruption scenarios

Minister King noted that by working together and jointly investing in industries, particularly in processing capabilities, nations can lock in a reliable supply of critical minerals and rare earth products. This approach signals government recognition that market forces alone are insufficient to drive the required supply chain diversification away from China-dependent pathways.

How Do US-Australia Bilateral Frameworks Transform Regional Supply Chains?

October 2025 Framework Analysis

The October 2025 US-Australia bilateral framework established minimum investment commitments of $1 billion from each nation, creating the largest coordinated critical minerals development initiative in the Indo-Pacific region. This framework moves beyond traditional trade relationships toward integrated value chains where Australia provides raw material mining, partner nations contribute processing technology and capital, and coordinated manufacturing reduces individual nation dependencies.

The six-month implementation timeline reflects the urgency with which both governments view critical minerals security. Unlike typical international agreements that unfold over years, this framework demands rapid project identification, funding allocation, and operational commencement across an estimated $8.5-13 billion project pipeline.

Framework Implementation Structure:

• $2 billion total bilateral investment commitment

• Technology transfer and joint venture requirements

• Third-party partnership expansion protocols including Japan, South Korea, and India

• Mining-to-processing vertical integration mandates

The framework explicitly targets supply chain architecture transformation rather than simple capacity expansion. Projects must demonstrate value chain integration that reduces collective dependence on Chinese processing capabilities while building alternative supply pathways for allied nations.

Value Chain Integration Strategy

Value chain integration represents the most innovative aspect of the bilateral framework, requiring projects to span multiple stages of mineral development rather than focusing on single extraction or processing activities. This approach ensures that strategic materials remain within allied supply networks from mine to final application.

The framework mandates technology transfer components that facilitate local capacity development in partner nations. Rather than creating new dependencies on US or Australian technology, these arrangements are designed to build distributed expertise that strengthens overall supply chain resilience.

Integration Requirements:

• Mining operations must include processing capability development

• Processing facilities require domestic market supply components

• Technology transfer must include skills development and workforce training

• Joint ventures must demonstrate third-party partnership potential

This approach addresses one of the fundamental vulnerabilities in current critical minerals supply chains: the concentration of processing capabilities in single nations or facilities. By distributing processing expertise across multiple allied nations, the framework reduces the impact of potential supply disruptions in any single location.

Countering Chinese Market Dominance

The bilateral framework directly responds to China's strategic use of critical minerals export restrictions as geopolitical tools. The 2023 gallium and germanium export bans provided a clear demonstration of how mineral supply can be weaponised, prompting coordinated allied responses that extend far beyond market-based solutions.

Minister King stated that Australia, Japan and the United States worked together to develop a solution to China banning the export of gallium and formally announced the start of the Alcoa-Sojitz project in 2025. This trilateral response demonstrates the template for future collaborative initiatives addressing other strategic minerals.

The success of coordinated critical minerals development depends on patient capital models that tolerate initial losses in service of long-term strategic objectives, fundamentally different from traditional commodity investment approaches.

Anti-Dominance Strategies:

• Alternative supply pathway development outside Chinese control

• Processing technology diversification across multiple allied nations

• Strategic stockpiling to weather short-term supply disruptions

• Joint research and development initiatives for substitute materials

The framework recognises that technological dependencies require multilateral responses rather than bilateral solutions alone. Future expansion to include European allies, Canada, and additional Indo-Pacific partners reflects the global scope of critical minerals security challenges.

What Role Does Multilateral Cooperation Play in Supply Chain Diversification?

Indo-Pacific Partnership Expansion

The March 2026 Tokyo Energy Security Ministerial and Business Forum brought together ministers from Japan, the United States, India, Indonesia, Malaysia, Singapore, South Korea, and Timor-Leste, representing the broadest multilateral engagement on critical minerals cooperation in the region's history. This ministerial-level participation signals recognition that energy security and critical minerals access have become central to regional stability and economic development.

Each participating nation contributes distinct comparative advantages to regional supply chain diversification. Japan provides patient capital and advanced manufacturing technology, South Korea contributes processing innovations, India offers manufacturing integration opportunities, and Southeast Asian nations provide geographic diversity and logistics capabilities.

Regional Partnership Roles:

| Nation | Primary Contribution | Strategic Focus | Investment Model |

|---|---|---|---|

| Japan | Patient capital, manufacturing technology | Long-term partnerships | Minority equity stakes |

| South Korea | Processing technology innovations | Electronics applications | Joint venture development |

| India | Manufacturing integration | Defence, space applications | Technology licensing |

| Indonesia | Geographic diversification | Regional logistics hub | Resource partnerships |

The expansion beyond traditional security alliances reflects recognition that critical minerals cooperation requires broader participation than military-focused partnerships can provide. Economic integration and technological cooperation demand different diplomatic frameworks than defence cooperation arrangements.

Trilateral Investment Success Stories

The Japan-Australia rare earths partnership provides the most successful template for multilateral critical minerals cooperation in the Indo-Pacific region. Japan's decade-long investment in Lynas Rare Earths, beginning in 2012, transformed the company into the largest producer of rare earths outside China while providing Japan with alternative supply sources during Chinese export restrictions.

Minister King highlighted that the patient and trusted capital that began in 2012 has now transformed Lynas into the biggest producer of rare earths outside China, with the payoff for this investment being stability of supply. This demonstrates how long-term commitment beyond market cycles can achieve strategic objectives that pure market mechanisms cannot deliver.

Lynas Success Factors:

• Timeline: 2012 Japanese investment through 2026 market leadership (14 years)

• Patient Capital: Tolerance for initial losses and market volatility

• Strategic Objective: Supply chain diversification rather than profit maximisation

• Market Position: Controls significant portion of light and heavy rare earth production outside China

The recent Japan Australia Rare Earths (JARE) Partnership floor price agreement represents an evolution from passive investment to active price support mechanisms. This arrangement provides minimum price guarantees for processed rare earths, de-risking producer profitability while ensuring stable supply availability.

The Alcoa-Sojitz gallium project demonstrates replication potential for other critical minerals beyond rare earths. This trilateral initiative, involving Australia (mining), Japan (capital and manufacturing), and the United States (technology), was announced in 2025 as a direct response to China's gallium export ban.

Regional Forum Integration

The Tokyo Energy Security Ministerial serves as the primary discussion platform for regional critical minerals coordination, allowing consensus-building on technical standards and investment priorities. This forum approach enables participating nations to align policies without formal treaty obligations that might complicate domestic political approval processes.

The Australian Strategic Policy Institute (ASPI) Darwin Dialogue 2026 expansion plans provide additional coordination mechanisms for defence and security aspects of critical minerals cooperation. These forums allow discussion of sensitive topics related to supply chain security and strategic vulnerabilities that cannot be addressed in pure commercial contexts.

Forum Integration Benefits:

• Policy coordination without formal treaty obligations

• Technical standards harmonisation across participating nations

• Investment priority alignment and project coordination

• Information sharing on supply chain vulnerabilities and risks

QUAD and AUKUS framework alignment provides additional coordination mechanisms, though these security-focused partnerships operate on different timelines and priorities than economic cooperation initiatives. The challenge lies in ensuring that security and economic cooperation reinforce rather than complicate each other.

How Do Processing Capabilities Address Strategic Vulnerabilities?

Domestic Processing Infrastructure Development

Processing capability development represents the most critical component of critical minerals strategic autonomy. While Australia possesses abundant raw materials, the concentration of processing capabilities in China creates vulnerability points that can be exploited through export restrictions or geopolitical tensions.

Iluka's facility, scheduled for 2026 opening with $1.1 billion in government investment, represents the largest single commitment to domestic processing infrastructure in Australian history. This facility will provide rare earth separation capabilities that currently exist primarily in China, reducing allied dependence on potentially unreliable supply chains.

Major Processing Investments:

• Iluka Facility: $1.1 billion investment, 2026 operational target

• Arafura Resources: Expansion under bilateral framework agreements

• Technology Transfer Initiatives: Joint research with Japanese and US partners

• Skills Development: Workforce training for specialised processing techniques

Arafura Resources expansion under bilateral framework agreements demonstrates how government backing can accelerate private sector development while ensuring strategic objectives alignment. These projects must demonstrate technology transfer components that build local expertise rather than creating new dependencies on foreign technical support.

Overcoming Chinese Processing Dependencies

China currently processes an estimated 70-80% of global rare earth separation, creating a strategic chokepoint that affects even nations with domestic mining capabilities. This processing bottleneck has become more critical than raw material access, as demonstrated by China's ability to restrict processed material exports while maintaining raw material trade.

Joint research and development initiatives with allied partners aim to develop alternative processing technologies that can compete with established Chinese capabilities. These efforts require significant patient capital investment, as processing technology development timelines extend far beyond typical commercial investment horizons.

Processing Vulnerability Areas:

• Rare earth separation and purification technologies

• Advanced materials processing for semiconductor applications

• Battery-grade lithium processing and refinement

• High-purity gallium and germanium production

Minister King emphasised that by working together and jointly investing in processing capabilities, nations can lock in reliable supply of critical minerals and rare earth products. This approach recognises that processing control often provides more strategic leverage than raw material control alone.

Technology transfer arrangements must balance knowledge sharing with intellectual property protection, ensuring that processing expertise develops across multiple allied nations without compromising competitive advantages or creating new vulnerabilities.

Economic Sovereignty vs. Market Efficiency Trade-offs

Domestic processing development requires acceptance of higher costs compared to established international suppliers, particularly Chinese facilities that benefit from scale economies and lower labour costs. Strategic premium calculations must weigh long-term security benefits against short-term economic efficiency losses.

Government intervention mechanisms help bridge the cost gap through subsidies, loan guarantees, and price support arrangements that make domestic processing economically viable while maintaining competitive market pressures for innovation and efficiency improvements.

Cost Consideration Factors:

• Initial capital investment requirements significantly higher than overseas alternatives

• Operating costs may remain elevated until scale economies develop

• Strategic insurance value of supply chain security difficult to quantify

• Long-term competitiveness depends on technology advancement and process innovation

The challenge lies in structuring government support that achieves strategic objectives without creating permanent market distortions or inefficient resource allocation. Sunset clauses and performance requirements help ensure that processing investments contribute to long-term competitive advantage rather than creating ongoing subsidy dependencies.

Skills development and workforce planning represent critical success factors often overlooked in processing capability discussions. Specialised knowledge required for advanced materials processing cannot be rapidly developed, requiring sustained investment in education and training programmes that extend beyond individual project timelines.

What Are the Investment and Market Implications?

Project Pipeline Analysis

The February 2026 critical minerals prospectus profiled 78 projects across 60 companies, representing the most comprehensive investment opportunity assessment in Australian critical minerals development history. This pipeline spans multiple mineral categories and development stages, from early exploration through advanced processing facility construction.

Government backing through the strategic reserve framework significantly improves investor confidence by reducing perceived risks associated with commodity price volatility and geopolitical supply chain disruptions. Traditional mining investment models often fail to account for strategic value that extends beyond pure market economics.

Pipeline Investment Characteristics:

• Total Projects: 78 across diverse mineral categories

• Company Participation: 60 companies including major miners and specialised developers

• Geographic Distribution: Concentrated in Western Australia with national representation

• Development Stages: Early exploration through advanced construction phases

Investment attraction mechanisms emphasise strategic partnerships rather than purely financial returns, recognising that critical minerals development serves broader objectives than traditional commodity extraction. Joint venture requirements and technology transfer mandates create investment structures that serve multiple strategic objectives simultaneously.

Risk assessment frameworks for private sector participation must account for geopolitical factors that traditional mining investment models do not typically consider. Government guarantees and strategic reserve off-take agreements help bridge this gap by providing demand certainty that justifies higher initial investment requirements.

Market Volatility and Policy Response

Critical minerals markets exhibit different volatility patterns than traditional commodities due to their strategic importance and concentrated supply chains. Policy interventions by major consuming or producing nations can create rapid price movements that reflect geopolitical tensions rather than supply and demand fundamentals.

The US government's reversal of rare earth price guarantee policies in previous years demonstrated how quickly policy changes can affect market confidence and stock valuations. This volatility requires different risk management approaches than traditional commodity investments.

Volatility Risk Factors:

• Geopolitical tensions affecting export policies

• Technology substitution reducing demand for specific minerals

• New supply sources disrupting established market relationships

• Government stockpiling and reserve policies affecting available supply

Government intervention timing becomes critical for market signal effectiveness. Early intervention can prevent supply chain disruptions, while delayed responses may occur after alternative suppliers have already captured market share or strategic dependencies have developed.

Investor confidence building mechanisms must demonstrate consistency across political cycles and government changes. Strategic frameworks that survive electoral transitions provide greater investment certainty than initiatives tied to specific political administrations or policy frameworks.

Global Supply Chain Reconfiguration

The transformation of critical minerals supply chains extends far beyond bilateral or even multilateral cooperation agreements. Global reconfiguration affects established trade relationships, technology transfer patterns, and investment flows across multiple regions and economic systems.

Regional Supply Chain Roles:

| Region | Primary Function | Investment Focus | Implementation Timeline |

|---|---|---|---|

| Australia | Mining and Processing Hub | $1.2B Strategic Reserve | 2026-2030 primary phase |

| United States | Technology and End Markets | $1B+ Bilateral Commitment | 2025-2026 deployment |

| Japan | Patient Capital and Advanced Manufacturing | Ongoing via Lynas model | Established since 2012 |

| Europe/UK/Canada | Standards and System Integration | Consultation and alignment | 2026+ coordination phase |

Supply chain reconfiguration requires coordination mechanisms that extend beyond government-to-government agreements to include industry standards, technical specifications, and quality assurance systems. Harmonisation across multiple supply chain participants ensures interoperability and reduces transaction costs.

The timeline for comprehensive reconfiguration extends well beyond current political and investment cycles, requiring institutional frameworks that can maintain consistency across decades rather than electoral periods. Patient capital models pioneered in the Japan-Australia rare earths partnership provide templates for sustained long-term engagement.

Investment flows accompanying supply chain reconfiguration affect not only critical minerals development but related infrastructure, logistics, and manufacturing capabilities. Port facilities, rail connections, and processing equipment manufacturing all experience increased demand as supply chains diversify geographically.

The next major ASX story will hit our subscribers first

How Does This Strategy Address Long-term Energy Security?

Clean Energy Transition Dependencies

The global transition to renewable energy systems creates unprecedented demand for specific critical minerals that have limited substitution possibilities. Battery technology alone requires lithium, cobalt, nickel, and rare earth elements in quantities that dwarf historical consumption patterns, while solar panels and wind turbines demand additional strategic materials.

Energy security increasingly depends on mineral security, creating direct linkages between geological resources and national energy independence. Unlike fossil fuel dependencies that can be managed through strategic petroleum reserves and supply diversification, critical minerals requirements are embedded in physical infrastructure with decades-long operational lifespans.

Clean Energy Mineral Dependencies:

• Battery Systems: Lithium, cobalt, nickel, graphite for grid storage and electric vehicles

• Solar Infrastructure: Silver, gallium, germanium for photovoltaic cells and inverters

• Wind Power: Rare earth magnets for generator systems and power electronics

• Grid Integration: Copper, aluminium, specialised alloys for transmission infrastructure

Demand projections through 2030 suggest requirements for some critical minerals may increase by 300-500% compared to current consumption levels. This demand acceleration occurs during the same period when supply chain diversification efforts are attempting to reduce dependence on concentrated suppliers.

The mismatch between rapid demand growth and slower supply chain development creates potential bottlenecks that could constrain energy transition timelines. Strategic reserve policies and international cooperation frameworks attempt to bridge this gap by accelerating supply development and providing buffer capacity during transition periods.

Defence and Advanced Technology Applications

Defence systems increasingly depend on advanced materials that require critical minerals for their sophisticated electronics, guidance systems, and communications equipment. Modern military platforms contain dozens of strategic materials that cannot be easily substituted or sourced from unreliable suppliers during conflict scenarios.

The defence-critical materials strategy requirements create additional demands for high-purity materials and specialised alloys that require advanced processing capabilities. The intersection of defence, space, and energy security applications means that critical minerals supply chain disruptions can affect multiple strategic sectors simultaneously.

Defence Application Categories:

• Electronics and Communications: Rare earth elements for radar and guidance systems

• Armour and Structural Materials: Titanium, tungsten, specialised steel alloys

• Propulsion Systems: High-temperature materials for jet engines and rocket propulsion

• Sensor Technologies: Germanium, gallium for infrared and night vision systems

Semiconductor manufacturing security represents a particularly critical vulnerability, as advanced chips require multiple strategic materials and cannot be easily stockpiled due to technological obsolescence. This creates ongoing supply chain dependencies that strategic reserves alone cannot fully address.

The dual-use nature of many critical minerals means that civilian and military applications compete for the same supply sources, creating potential conflicts between economic efficiency and strategic security objectives during supply shortage scenarios.

Future Demand Projections and Capacity Planning

Global energy transition acceleration impacts critical minerals demand through multiple pathways that extend beyond direct renewable energy applications. Electric vehicle adoption, grid modernisation, and industrial electrification create compounding demand effects that are difficult to forecast accurately.

Supply-demand gap analysis through 2030 reveals potential shortfalls in multiple mineral categories, even assuming successful implementation of current development projects and supply chain diversification initiatives. These gaps require sustained investment and international cooperation over timelines that exceed typical commercial planning horizons.

Projected Demand Growth Rates (2025-2030):

• Lithium: 400-600% increase driven primarily by battery applications

• Rare Earth Elements: 200-300% growth for permanent magnet applications

• Gallium: 150-250% expansion in semiconductor and solar applications

• Graphite: 300-400% demand growth for battery anodes and industrial applications

Capacity expansion requirements extend beyond mining to include processing, refining, and manufacturing capabilities that can transform raw materials into application-ready products. The capital investment required for comprehensive capacity development exceeds the financial capabilities of individual companies or even nations.

Investment needs assessment suggests total requirements of $200-300 billion globally over the next decade for adequate critical minerals capacity development. This investment must be coordinated across multiple nations and sectors to avoid duplication while ensuring adequate geographic and political diversification.

What Challenges and Risks Remain?

Implementation and Execution Risks

Regulatory approval timelines for new critical minerals projects can extend 5-10 years in many jurisdictions, creating significant delays between investment commitments and operational capacity. Environmental assessments, indigenous land rights considerations, and community consultation processes all contribute to extended development timelines that may not align with strategic urgency requirements.

Technical challenges in processing development represent significant execution risks, particularly for minerals where processing expertise is concentrated in Chinese facilities. Replicating complex separation and purification technologies requires substantial trial and error periods that can extend project timelines and increase costs beyond initial projections.

Primary Implementation Challenges:

• Regulatory Complexity: Multiple approval processes across federal and state jurisdictions

• Environmental Requirements: Comprehensive impact assessments and mitigation measures

• Indigenous Consultation: Traditional owner agreements and cultural heritage protections

• Technical Expertise: Limited availability of specialised processing knowledge

Workforce development represents a critical constraint often overlooked in project planning. Specialised skills required for critical minerals processing cannot be rapidly developed through standard training programmes, requiring sustained educational investment that begins years before operational requirements.

Environmental and social licence considerations have become more complex as communities and environmental groups scrutinise critical minerals projects more closely. Unlike traditional mining operations, these projects carry additional scrutiny due to their strategic importance and government involvement.

Market and Geopolitical Uncertainties

Chinese policy responses to allied supply chain diversification efforts could include market retaliation, technology export restrictions, or strategic dumping designed to undermine alternative supplier viability. The scale of Chinese critical minerals processing capabilities provides significant leverage for such responses.

Commodity price volatility creates ongoing challenges for project economics, particularly when government support mechanisms must balance strategic objectives with fiscal responsibility. Price guarantees and strategic stockpiling can provide some protection, but cannot eliminate all market risks from critical minerals development.

Geopolitical Risk Scenarios:

• Market Retaliation: Chinese suppliers reducing prices to undermine alternative suppliers

• Technology Restrictions: Export controls on processing equipment and expertise

• Third-Party Disruption: Supply chain attacks on allied mineral processing facilities

• Alliance Fragmentation: Political changes affecting international cooperation commitments

Allied coordination sustainability represents a significant challenge as political changes in participating nations could affect long-term commitment reliability. Strategic frameworks that depend on sustained cooperation over decades face risks from electoral cycles and changing political priorities.

Technological disruption could affect demand patterns for specific critical minerals, potentially stranding investments in processing facilities or mining projects. The recent battery recycling breakthrough developments in China demonstrate how rapidly technology advances can alter strategic mineral requirements and recycling capabilities.

Measuring Success and Accountability

Key performance indicators for strategic reserve effectiveness must balance multiple objectives including supply security, economic efficiency, and international cooperation success. Traditional financial metrics may not capture strategic value, while purely strategic measures may ignore economic sustainability requirements.

Supply chain resilience metrics require development of new measurement frameworks that can assess vulnerability reduction and disruption response capabilities. These metrics must account for potential rather than actual disruptions, making assessment methodologies inherently speculative.

Success Measurement Categories:

• Supply Security: Percentage of critical mineral requirements met from allied sources

• Economic Efficiency: Cost premiums for strategic supply compared to market alternatives

• Partnership Effectiveness: Number and scale of successful multilateral development projects

• Innovation Impact: Technology advancement and processing capability development

Economic and security outcome assessments require long-term data collection and analysis capabilities that extend beyond typical government planning horizons. Institutional mechanisms for sustained performance measurement and strategic adjustment must survive political transitions and budget pressures.

Accountability frameworks must balance transparency requirements with operational security considerations, as detailed information about strategic reserves and supply chain vulnerabilities could be valuable to potential adversaries seeking to exploit weaknesses in allied cooperation arrangements.

Australia's Critical Minerals Leadership in Regional Security

Strategic Positioning for the Next Decade

Australia's integration of economic and security objectives through critical minerals diplomacy positions the nation as a central node in emerging Indo-Pacific supply chain architecture. This leadership role extends beyond traditional resource supplier relationships toward strategic partnership facilitation and technology development coordination.

The convergence of geological advantages, established mining expertise, and strategic alliance relationships creates unique opportunities for Australia to influence global critical minerals supply chain development. However, this influence requires sustained investment in processing capabilities and international coordination mechanisms that extend far beyond current political planning horizons.

Leadership Opportunity Areas:

• Supply Chain Architecture: Designing alternative pathways that reduce China dependencies

• Technology Development: Advancing processing and separation technologies through international partnerships

• Standards Development: Establishing quality and sustainability frameworks for critical minerals trade

• Partnership Facilitation: Serving as trusted intermediary for multilateral cooperation initiatives

Innovation and technology development priorities must balance immediate strategic requirements with long-term competitive positioning. Investment in research and development capabilities ensures that Australia maintains relevance as global technology requirements evolve and new applications for critical minerals emerge.

Regional leadership sustainability requires institutional frameworks that can maintain consistency across political cycles while adapting to changing strategic circumstances. The success of Japan's decade-long investment in Lynas demonstrates the importance of patient capital and sustained commitment for achieving strategic objectives.

Policy Recommendations for Sustained Success

Continued investment in processing capabilities represents the most critical requirement for Australian critical minerals leadership sustainability. Without domestic processing capacity, Australia remains vulnerable to supply chain manipulation regardless of its geological advantages or international partnership agreements.

Expansion of multilateral partnerships beyond current bilateral and trilateral arrangements can provide additional resilience and market opportunities while distributing risks across broader coalition structures. Regional forum development and institutional cooperation mechanisms facilitate such expansion while maintaining strategic coherence.

Strategic Policy Priorities:

• Processing Investment: Sustained government support for domestic separation and refinement capabilities

• Partnership Expansion: Inclusion of European allies, Canada, and additional Indo-Pacific nations in cooperation frameworks

• Technology Development: Joint research initiatives that advance alternative processing methods and substitute materials

• Institutional Capacity: Long-term planning and coordination mechanisms that survive political transitions

Long-term strategic planning and adaptation mechanisms must account for changing technology requirements, evolving geopolitical relationships, and emerging strategic challenges that cannot be anticipated in current policy frameworks. Flexibility and responsiveness capabilities ensure that strategic investments remain relevant as circumstances change.

Workforce development and skills enhancement programmes require immediate attention to support processing capability development and technology transfer initiatives. Educational partnerships with allied nations can facilitate knowledge sharing while building domestic expertise in critical areas.

The success of Australia pushes critical minerals cooperation ultimately depends on maintaining balance between economic opportunity and strategic necessity, ensuring that commercial viability supports rather than undermines long-term security objectives. This balance requires ongoing policy adjustment and international coordination that extends well beyond current planning horizons.

Consequently, the framework established through Canada and Australia's strengthened partnership demonstrates how like-minded nations can coordinate efforts while the recent US-Australia critical minerals framework agreement provides a blueprint for similar partnerships with other strategic allies. These bilateral and multilateral arrangements ensure that Australia pushes critical minerals cooperation forward as both an economic imperative and security necessity for the Indo-Pacific region.

Looking to Capitalise on Australia's Critical Minerals Boom?

Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, transforming complex mineral data into actionable investment opportunities. With Australia's critical minerals sector receiving unprecedented government backing and international investment, subscribers gain rapid insights that position them ahead of market movements in this strategically vital industry. Begin your 14-day free trial today to secure your market-leading advantage in critical minerals investing.