July 16, 2026

Why Australia's Moment in Green Metals Has Arrived

Electricity systems rarely change at the pace markets expect. Then, suddenly, they do. That is the core strategic backdrop behind the push to position Australia as an Australia green metals superpower. The modern economy is shifting toward electricity not only because transport, heating, and industry are substituting away from fossil fuels, but also because entirely new demand sources are arriving at scale.

AI infrastructure, grid batteries, industrial automation, and rising middle-class consumption across emerging markets are adding load that simply did not exist in prior energy cycles. The International Energy Agency has described this era as the Age of Electricity, reflecting a structural transformation rather than a temporary upswing. On current forecasts, global electricity demand is expected to grow by roughly 3.6% per year through 2030, with overall consumption projected to be 30% to 50% higher by 2035.

For Australia, that macro shift matters because electrification is not just an energy story. It is a materials story. Copper, lithium, nickel, and cobalt sit at the heart of transmission lines, batteries, electric vehicles, storage systems, and data centre buildouts. Australia holds unusually strong positions across several of these supply chains, yet the bigger question is whether resource abundance can be converted into durable industrial advantage.

Furthermore, the critical minerals energy transition is reshaping how governments and investors think about resource security globally.

The real strategic contest is not over who has rocks in the ground. It is over who captures processing, refining, certification, and premium end-market margins.

When big ASX news breaks, our subscribers know first

Why Electrification Is Reshaping Mineral Demand

A useful way to understand the demand surge is to split it into two interacting forces:

- Substitution demand from systems moving from oil, coal, and gas toward electricity

- Net-new demand from technologies and populations adding fresh pressure to the grid

These forces are visible across several datasets and industry trends:

- Australia's domestic electricity demand is projected by AEMO to roughly double by 2050.

- Australia's data centre sector may rise from around 1% of electricity consumption today to 8% to 11% by 2035.

- Global data centre energy demand increased by about 17% in 2025 and is widely expected to double by 2030 if current development pipelines hold.

- India's electricity consumption has climbed about 33% over the past five years and is forecast to rise a further 80% by 2035.

- In 2025, around 80% of global electricity demand growth came from emerging markets.

The battery side of the equation is equally important. Grid-scale lithium-ion storage reached about 300 GWh in 2025, with annual growth near 50%. This matters because lower storage costs improve the economics of renewable-heavy power systems, which in turn can support more electric vehicles, more electrified industry, and more onshore processing of minerals and metals.

Demand Snapshot

| Demand driver | Current reference point | Forecast direction |

|---|---|---|

| Global electricity demand | 2024 baseline | +30% to 50% by 2035 |

| Australia electricity demand | 2024 baseline | About 2x by 2050 |

| Australia data centre power share | About 1% today | 8% to 11% by 2035 |

| India electricity consumption | +33% in last 5 years | +80% more by 2035 |

| Global data centre demand | 2024 baseline | About 2x by 2030 |

| Grid-scale lithium-ion storage | 300 GWh in 2025 | Rapid expansion expected |

A lesser-discussed point for investors is that electricity consumption in Australia has been growing about 2.5 times faster than the broader energy market. That suggests the domestic transition is already underway in measurable form, even before many of the largest industrial and data-centre developments are fully built.

The Four Minerals at the Centre of the Transition

The IMF has highlighted copper, lithium, nickel, and cobalt as especially important to the electrification shift. Each serves a different function, and each carries different geological, commercial, and geopolitical risks.

Copper: The Enabling Metal

Copper is the basic conductor of the electric economy. It is embedded in transmission infrastructure, transformers, motors, wiring harnesses, charging systems, and cooling equipment.

Key facts include:

- A typical electric vehicle requires about 70 kilograms of copper.

- EVs are expected to account for roughly 14% of total copper demand growth between 2025 and 2035.

- A major Chicago data centre project developed by Microsoft reportedly used 2,177 tonnes of copper during construction.

However, the copper supply crunch facing global markets is already influencing investment decisions and long-term project planning. Copper grades, capital intensity, and permitting timelines matter more here than many retail investors realise. New copper mines often require very large upfront capital commitments, while declining ore grades globally can increase unit costs over time.

Lithium: High Demand, High Volatility

About 80% of global lithium production currently feeds battery manufacturing. Demand is expected to double by 2030 and potentially quadruple by 2040 under many transition scenarios.

Yet lithium also illustrates why thematic investing can be treacherous. Unlike some scarcer minerals, lithium is geologically abundant. When prices spike, more projects become economic, new supply enters the market, and price collapses can follow. That boom-bust dynamic was visible after the 2021 to 2022 price surge.

In addition, lithium oversupply risks remain a key consideration for investors evaluating battery metal exposure in 2025 and beyond. Another technical risk is chemistry substitution. Sodium-ion batteries are advancing, particularly in China, and while they are not a universal replacement for lithium-ion, they could reduce lithium intensity in some lower-cost or lower-range applications over time.

Nickel: Battery Relevance, But Not Battery Dependence

Nickel is often discussed as a battery metal, but that can obscure its current demand base. Around two-thirds of nickel demand still comes from stainless steel. Batteries account for roughly 14% of total nickel demand, but that slice is one of the fastest-growing segments.

Not all nickel is equal. Battery-grade nickel generally requires higher purity and more complex refining than lower-grade nickel used elsewhere. Consequently, Indonesian nickel expansion has created a structural challenge for Australian producers, given the lower-cost production and aggressive downstream policy settings deployed there.

Cobalt: Useful, Controversial, Uncertain

Cobalt improves thermal stability in lithium-ion batteries and helps reduce overheating risk. The EV sector now represents about 40% of cobalt demand.

The problem is supply concentration. More than 70% of global cobalt supply comes from the Democratic Republic of Congo, where ethical sourcing concerns, political risk, and supply-chain scrutiny remain persistent issues. Australian cobalt output is comparatively small at around 2% of global supply, largely because cobalt is often produced as a byproduct of nickel mining rather than from standalone operations.

Cobalt's strategic value is shaped as much by where it comes from as by what it does inside a battery.

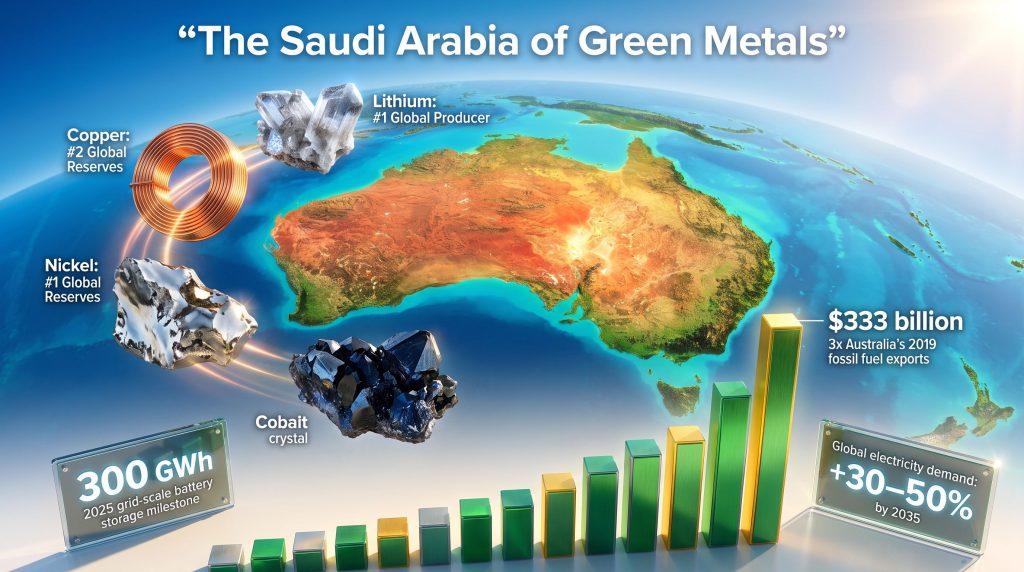

How Strong Is Australia's Resource Position?

Australia's geology gives it a rare combination of scale and diversity across critical minerals.

Comparative Position by Mineral

| Mineral | Australia reserve rank | Australia production rank | Strategic context |

|---|---|---|---|

| Lithium | #1 | #1 | About half of global output, roughly double Chile |

| Copper | #2 | #8 | Large reserve base, production growth potential |

| Nickel | #1 tied with Indonesia | Top tier | Strong reserves, but faces Indonesian cost pressure |

| Cobalt | #2 | About 2% global supply | Mostly linked to nickel operations |

| Iron ore | #1 | #1 | Dominant reserve and export position |

Australia's structural advantages are not limited to geology:

- Proximity to Asia supports export logistics to China, Japan, South Korea, and India.

- Institutional stability lowers sovereign risk relative to many competing jurisdictions.

- Mining expertise is already deeply embedded across engineering, services, and project development.

- Renewable resource quality in solar and wind creates long-run potential for lower-emissions processing.

But the weaknesses are equally important:

- High labour costs reduce competitiveness against lower-cost producers.

- Industrial power costs remain a major hurdle despite strong renewable potential.

- Processing gaps mean a large share of value-added refining still occurs offshore, especially in China.

That last point is central to the Australia green metals superpower thesis. A country can dominate reserves and still miss the most profitable part of the value chain. For a broader view of how this competitive position is being framed nationally, the Superpower Institute's green metals framework outlines several pathways for capturing downstream value.

The Economic Scale of the Green Metals Opportunity

The upside case for Australia is not about shipping more concentrate alone. It is about moving from raw material exports toward green iron, green aluminium, and battery-grade processed materials.

Illustrative Export Potential

| Category | Indicative target | Potential annual export value |

|---|---|---|

| Green iron | 10 million tonnes by 2030 | $295 billion |

| Green iron at larger scale | Long-term by 2060 | Up to $386 billion |

| Green aluminium | Major scale-up scenario | $60 billion |

| Total green metal exports | By 2050 | $333 billion |

These projections are ambitious and highly scenario-dependent. They rely on technology costs falling, renewable electricity remaining competitive, infrastructure being built on time, and international customers paying premiums for lower-emissions materials. They should not be treated as guaranteed outcomes.

Still, the strategic logic is powerful. Australia already proved that large-scale commodity exports can reshape national income through iron ore and LNG. The green metals opportunity asks whether the next chapter can capture more downstream margin rather than repeating the old model of shipping ore and importing value-added products.

Policy Settings Helping Shape the Opportunity

Australia has announced several programmes relevant to low-emissions metals and industrial technology. These are important policy signals, but they should not be overstated as project-specific support unless explicitly confirmed for individual companies.

Major Policy Commitments

| Initiative | Capital committed | Purpose |

|---|---|---|

| Future Made in Australia Innovation Fund | $1.7 billion | Broader green industry commercialisation |

| Green metals component | $750 million | Green metals technology deployment |

| Green Iron Investment Fund | $1 billion | Support early green iron development |

| Domestic allocation within green iron fund | At least $500 million | Australian-based applicants |

| Green aluminium support | $2 billion | Lower-emissions aluminium scale-up |

| Combined low-emissions metals package | About $5 billion | Sector development framework |

Another important piece is the Guarantee of Origin framework, designed to certify emissions intensity for products such as hydrogen and potentially low-emissions metals. Certification could matter if buyers in Europe and other markets increasingly differentiate between high-carbon and low-carbon material streams. The government's broader ambitions in this space were outlined at the launch of the Superpower Institute's green iron plan, signalling strong institutional alignment behind the strategy.

However, policy gaps remain significant:

- Carbon pricing signals are still relatively incomplete.

- Shared infrastructure such as ports, transmission, and water systems often needs coordination beyond what private capital can efficiently deliver alone.

- Trade diplomacy may be needed to help secure durable green premiums in export markets.

The next major ASX story will hit our subscribers first

Growth Catalysts Investors Should Watch

1. Emerging Market Electrification

India is the standout case. It already consumes roughly six times as much electricity as Australia and could become the second-largest copper consumer after China if its demand rises from 1.7 million tonnes to 5 million tonnes annually by 2035.

Africa is another underappreciated demand driver. The World Bank and African Development Bank have set out Mission 300, targeting electrification for 300 million Africans by 2030 with around $45 billion in financing support. That does not automatically translate one-for-one into immediate metals demand, but it reinforces the scale of potential grid expansion ahead.

2. Electric Vehicles and Storage

A battery electric vehicle today can require approximately:

- 70 kg of copper

- 10 kg of lithium

- 45 kg of nickel

- Up to 20 kg of cobalt

These figures vary by chemistry, vehicle size, and design, but the directional point remains clear: electrified transport is materially more mineral-intensive than internal combustion transport.

3. AI and Data Centres

Data centres are emerging as one of the most important incremental load sources in developed electricity systems. They are also metal-intensive during construction and retrofitting. The market often focuses on chips and software, but the physical layer requires cabling, substations, cooling systems, transformers, and backup power equipment.

How Investors Can Access the Theme

The Australia green metals superpower theme can be approached through diversified miners, single-commodity producers, or thematic ETFs. Furthermore, Australia green metals leadership is increasingly being discussed as a distinct investment category among institutional and retail investors alike.

Selected Listed Exposures

| Segment | Example | Notes |

|---|---|---|

| Diversified large cap | BHP (ASX: BHP) | Copper now a major profit contributor; broad commodity exposure |

| Diversified large cap | Rio Tinto (ASX: RIO) | Copper plus more visible lithium positioning |

| Copper pure play | Sandfire Resources (ASX: SFR) | More direct copper leverage |

| Lithium producer | Pilbara Minerals (ASX: PLS) | Major hard-rock lithium exposure |

| Diversified lithium | Mineral Resources (ASX: MIN) | Lithium and iron ore mix |

| Lithium developer/producer | Liontown Resources (ASX: LTR) | Higher-risk lithium exposure |

| Nickel exposure | Nickel Industries (ASX: NIC) | More concentrated nickel exposure |

| Cobalt speculation | Cobalt Blue Holdings (ASX: COB) | Pre-revenue, high-risk cobalt theme |

ETF Options

- Global X Copper Miners ETF (ASX: WIRE) for diversified copper miner exposure

- BetaShares Energy Transition Metals ETF (ASX: XME) for broader transition metal exposure, including some China weight

- Global X Green Metal Miners ETF (ASX: GMTL) for a basket focused on copper, nickel, lithium, and cobalt

- Global X Battery Tech & Lithium ETF (ASX: ACDC) for broader battery supply-chain exposure

A subtle but important investing distinction is whether an investor wants commodity exposure or operator exposure. Commodity themes can be right while individual companies disappoint due to cost overruns, poor geology, weak balance sheets, or bad capital allocation. Conversely, strong operators sometimes outperform even in mediocre price environments.

The Biggest Risks to the Thesis

No serious analysis of this theme is complete without the downside cases.

Key Risks

- Commodity cyclicality — Lithium's recent boom and correction showed how quickly supply responses can hit prices.

- Technology substitution — Battery chemistry changes could reduce demand intensity for some minerals.

- Geopolitical concentration — China dominates much of global refining, while Indonesia has reshaped nickel markets through downstream policy controls.

- Value leakage — Australia may continue exporting raw or lightly processed material while others capture refining and manufacturing margins.

- Execution risk — Industrial transformation requires far more than public funding announcements. It depends on power, logistics, workforce, permitting, and customer demand aligning over many years.

Investors should treat long-range green metals projections as scenario analysis, not certainty. Commodity markets are cyclical, policy settings evolve, and technology pathways can change faster than consensus expects.

Can Australia Actually Become a Green Metals Superpower?

There are three broad pathways.

Scenario A: Value-Chain Capture

Australia expands renewable-powered processing, green iron, green aluminium, and battery-material refining. Export volumes rise, margins improve, and the country captures more economic value per tonne extracted.

Scenario B: Raw Material Dominance Only

Australia remains a major supplier of lithium, copper, iron ore, and nickel, but most higher-margin processing stays offshore. Revenues still grow, but the deepest industrial upside is missed.

Scenario C: Strategic Underperformance

Competing jurisdictions outgrow Australia in downstream capacity, substitution reduces demand for selected materials, and domestic costs block major industrial expansion.

The most realistic near-term conclusion is that Australia has the ingredients to become an Australia green metals superpower, but not the result itself. Geology has already done its part. The harder work lies in energy pricing, refining capacity, infrastructure coordination, certification systems, and commercial execution.

For investors, that means this theme is attractive, but not simple. It should be viewed as a long-duration structural opportunity filtered through very short-duration commodity cycles. This article is general information only and is not personal financial advice. Investors should consider their objectives, risk tolerance, and time horizon before acting on any mineral, mining, or ETF exposure.

Want to Catch the Next Major ASX Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across copper, lithium, nickel, cobalt, and beyond — instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the market.