June 15, 2026

The Minerals Beneath the Alliance: How Supply Chain Fear Is Driving Indo-Pacific Diplomacy

There is a pattern embedded in the history of major resource diplomacy that rarely gets discussed in press releases or joint statements. Bilateral minerals agreements rarely emerge from optimism. They emerge from fear. The fear of scarcity, of strategic vulnerability, of waking up one morning to discover that an adversary controls the materials your economy cannot function without. Understanding this psychological and strategic undercurrent is essential to grasping why Australia and Japan critical minerals cooperation has accelerated so dramatically in recent years, and why the A$1.67 billion joint declaration signed on May 4, 2026 carries far more weight than its dollar figure suggests.

When big ASX news breaks, our subscribers know first

The Geopolitical Architecture Behind the Partnership

For decades, Japan operated under the assumption that global commodity markets would reliably deliver the minerals its economy required. That assumption has been progressively dismantled. China's dominant position in critical minerals processing, which extends across an estimated 60 to 80 percent of global rare earth processing capacity, has transformed what was once viewed as a trade question into a national security calculation.

China also controls approximately 80 percent of global gallium output and produces roughly 85 percent of the world's magnesium supply. For a nation with virtually no domestic mineral reserves of its own, Japan's exposure to these concentration risks is not theoretical. It is existential.

What makes Australia and Japan critical minerals cooperation structurally different from other bilateral resource arrangements is the depth of existing interdependency that precedes it. Australia already supplies approximately one-third of Japan's total energy needs and holds the position of Japan's largest LNG supplier. This is not a relationship being constructed from scratch. It is a relationship being deepened and extended into a new strategic domain.

The institutional architecture is also well-established: the Japan-Australia Economic Partnership Agreement (JAEPA), signed in 2014, created preferential trade terms and investment protections that dramatically reduce the friction cost of capital deployment. The October 2022 Australia-Japan Critical Minerals Partnership then provided the first dedicated bilateral framework specifically targeting minerals security, setting the groundwork for what followed in 2026.

China's Processing Dominance: The Threat Shaping Every Decision

It is worth pausing on the specific nature of China's mineral leverage, because it is frequently misunderstood. The strategic risk is not primarily about where minerals are extracted from the ground. Australia, Canada, Africa, and critical minerals geopolitics involving Greenland all involve significant mineral reserves. The leverage point is at the processing and refining stage, where raw ore is transformed into the refined materials that technology manufacturers actually require.

Nations controlling only the extraction stage remain price-takers in global supply chains. Nations controlling the processing stage hold structural economic and geopolitical power over every downstream industry that depends on those refined outputs.

China achieved this position through decades of deliberate industrial policy, accepting environmental costs and operating at margins that discouraged Western competitors from investing in comparable capacity. Furthermore, when Beijing implemented China's export controls on gallium in 2023, it was demonstrating precisely what that leverage looks like in practice. A mineral used in semiconductors, 5G infrastructure, and solar panels suddenly became the subject of emergency policy discussions across allied governments simultaneously.

The 2026 Australia-Japan Joint Declaration reflects an explicit recognition of this reality. Its emphasis on midstream processing projects, not just raw mineral extraction, signals a maturation in strategic thinking from both governments.

The Strait of Hormuz as an Accelerant

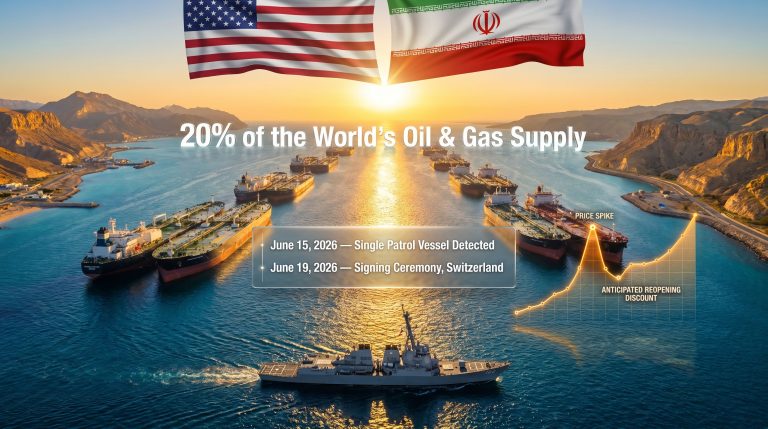

The urgency driving the May 2026 agreement cannot be fully understood without reference to the events of early 2026. The effective closure of the Strait of Hormuz following escalating conflict between the US, Israel, and Iran eliminated the transit of approximately 20 million barrels of petroleum per day through a single chokepoint, representing roughly 20 percent of global petroleum liquids consumption.

Under normal conditions, approximately 138 vessels transited the strait daily, according to the Joint Maritime Information Centre. The disruption stopped that traffic entirely, with maritime monitors recording zero oil tanker movements on March 3, 2026.

Asia absorbed the largest share of that impact. According to the US Energy Information Administration, 84 percent of crude oil and condensate and 83 percent of LNG moving through Hormuz in 2024 was destined for Asian markets. For Japan, almost entirely dependent on energy imports, the immediate consequences were severe.

For Australia, the disruption exposed its own structural vulnerability: with only two operational refineries supplying approximately 20 percent of domestic liquid fuel demand, Australia is a price-taker on refined oil products derived from Asia, despite being a significant raw commodity exporter.

Federal Climate Change and Energy Minister Chris Bowen publicly confirmed Australia held 36 days of petrol reserves, 34 days of diesel, and 32 days of jet fuel at the time, well below the International Energy Agency's benchmark requirement of 90 days of net import equivalents for member countries.

The mining sector's exposure was particularly acute. According to analysis from the Institute for Energy Economics and Financial Analysis, a single ultra-class haul truck consumes approximately one million litres of diesel annually, and nationally, fuel combustion emissions across Australian mining doubled from FY11 levels to 21.8 megatonnes in FY23, growing at 6.8 percent per year. For both nations, the Hormuz disruption made the case for locked-in, geographically diversified supply chain partnerships impossible to defer.

What Australia and Japan Committed to on May 4, 2026

The joint declaration signed by Australian Prime Minister Anthony Albanese and Japanese Prime Minister Sanae Takaichi on May 4, 2026 represents the most substantive bilateral minerals commitment between the two nations in their shared history.

| Agreement Element | Detail |

|---|---|

| Total Committed Capital | A$1.67 billion |

| Australia's Contribution | Up to A$1.3 billion |

| Signing Date | May 4, 2026 |

| Signatories | PM Anthony Albanese and PM Sanae Takaichi |

| Target Minerals | Nickel, cobalt, gallium, graphite, rare earths, fluorite |

| Strategic Goal | Supply chain diversification away from single-source dependency |

Australia's contribution represents approximately 78 percent of the total commitment, reflecting its role as the primary supply-side partner and host jurisdiction for project development. The agreement does not operate in isolation. It builds directly on the Australia-US Critical Minerals and Rare Earths Framework, signed by Prime Minister Albanese and US President Donald Trump in Washington the previous year, establishing parallel allied diplomatic tracks that reinforce each other's strategic objectives.

The timing of the 2026 declaration also connects to a pre-existing investment pipeline. In February 2026, Federal Resources Minister Madeleine King launched the Australian Critical Minerals Prospectus, identifying 49 mines and 29 midstream critical minerals processing projects across Australia ready for international investment. The six projects designated under the Japan agreement represent a curated selection from this broader portfolio, prioritising minerals with the highest concentration risk and clearest downstream application across Japanese industry.

Resources Minister Madeleine King articulated Australia's positioning clearly when she launched the prospectus: Australia holds both the geological endowment and the technical capability to develop critical minerals projects reliably, sustainably, and at scale.

The Six Projects Anchoring the Investment Pipeline

The selection of six specific projects under Australia and Japan critical minerals cooperation is not arbitrary. Each targets a distinct mineral vulnerability in Japan's industrial and defence supply chains, and collectively they cover the full technology spectrum from battery manufacturing to semiconductor fabrication.

1. Goongarrie Hub (Nickel and Cobalt)

Developed by Ardea Resources in partnership with Sumitomo Metal Mining and Mitsubishi, the Goongarrie Hub represents one of Australia's largest nickel-cobalt resources. Its strategic significance lies in its direct feed into Japan's electric vehicle battery manufacturing supply chain, where both nickel and cobalt are foundational inputs for cathode chemistry.

2. Lynas Rare Earths Project

Rare earth supply chains are essential for the permanent magnets used in electric vehicle drive systems, wind turbine generators, and precision-guided defence munitions. Lynas Rare Earths is already one of the world's largest rare earth producers outside of China, making this designation a natural extension of existing production capability into a formalised bilateral supply framework.

3. Alcoa Gallium Recovery Project

Gallium's inclusion reflects one of the most acute supply vulnerabilities in advanced technology manufacturing. China's export restrictions on gallium, implemented in 2023, directly targeted semiconductor production capacity across allied nations. Alcoa's gallium recovery process, which extracts gallium as a byproduct of aluminium refining, offers a pathway to meaningful non-Chinese supply.

4. Magnium Magnesium Project

With China producing approximately 85 percent of global magnesium, this lightweight metal represents one of the most concentrated single-source dependencies in industrial manufacturing. Magnesium is essential for lightweight alloys used across automotive and aerospace applications, two sectors Japan dominates globally.

5. Tivan Fluorite Project

Fluorite is a less widely discussed but critically important mineral. As the primary feedstock for hydrogen fluoride, it is indispensable in semiconductor manufacturing processes. Japan's position as a global leader in semiconductor production and chip design makes fluorite supply security a direct national industrial priority.

6. RZ Resources Critical Minerals Project

The inclusion of RZ Resources broadens the portfolio across diversified mineral categories, providing resilience against concentration in any single commodity within the designated project set.

Mapping Minerals to Industrial Dependencies

| Mineral | Primary Industrial Application | Japan's Dependency Risk |

|---|---|---|

| Nickel and Cobalt | EV batteries, stainless steel | High: limited domestic supply |

| Rare Earths | Magnets, defence electronics, AI hardware | Critical: historically China-dependent |

| Gallium | Semiconductors, 5G, solar panels | Extreme: China controls ~80% of output |

| Magnesium | Lightweight alloys, aerospace | High: China produces ~85% globally |

| Fluorite | Semiconductor manufacturing, hydrogen fluoride | Moderate to High |

Why Midstream Processing Is the Real Strategic Battleground

A persistent blind spot in public discussion of critical minerals agreements is the tendency to treat raw mineral extraction as the primary objective. In strategic terms, extraction without processing capacity leaves a nation only marginally less dependent on its adversaries. The refined material is what manufacturers actually require, and the refining stage is where China's leverage is concentrated.

The 2026 Australia-Japan agreement's explicit focus on midstream processing projects reflects an understanding that has taken allied governments considerable time to internalise. Federal Trade and Tourism Minister Don Farrel articulated this when the Critical Minerals Prospectus launched, noting that the document was specifically designed to showcase midstream processing opportunities to international investors, not simply raw extraction sites.

This distinction carries significant economic implications as well. Processing minerals domestically before export captures substantially more value per tonne extracted. A nation exporting refined rare earth oxides, for instance, commands a dramatically higher price and establishes longer-term customer relationships than one exporting raw ore. Australia's transition from passive resource exporter toward an integrated supply chain participant is both a strategic and an economic ambition embedded in the bilateral architecture being constructed.

Australia's Broader Critical Minerals Diplomatic Strategy

The Japan agreement does not exist in isolation. It forms one track within a coordinated allied strategy that Australia has been building systematically through 2025 and 2026. In addition, critical minerals in Australia have become a central pillar of the nation's broader foreign and economic policy framework.

| Partnership | Year Established | Key Mechanism | Primary Minerals Focus |

|---|---|---|---|

| Japan-Australia (JAEPA) | 2014 | Trade and investment preferences | Broad commodities |

| Australia-Japan Critical Minerals Partnership | 2022 | Bilateral minerals framework | Critical minerals broadly |

| Australia-US Critical Minerals Framework | 2025 | Ministerial-level supply chain pact | Rare earths, gallium, antimony |

| Australia-Japan Joint Declaration | 2026 | A$1.67B co-investment commitment | Nickel, cobalt, gallium, rare earths, fluorite |

The A$1.2 billion Australian Critical Minerals Strategic Reserve, initially focused on gallium, antimony, and rare earths, signals a deliberate shift from Australia's historical role as a passive resource exporter toward active participation in supply chain architecture. Minister King's attendance at the US-led critical minerals ministerial dialogue, hosted by US Secretary of State Marco Rubio, further reflects Australia's positioning at the centre of allied supply chain resilience efforts.

The US itself unveiled a US$17.2 billion strategic critical minerals stockpile, referred to as Project Vault, in early 2026, with the stated objective of reducing industrial reliance on China and protecting manufacturers from supply disruptions. Australia's own reserve and bilateral partnership framework aligns directly with this allied accumulation strategy.

The next major ASX story will hit our subscribers first

The Domestic Stakes: Regional Communities and Economic Development

The economic implications of Australia and Japan critical minerals cooperation extend well beyond bilateral trade statistics. The Minerals Council of Australia's submission to Federal Parliament's inquiry into critical minerals project outcomes provides a granular picture of what is at stake for regional Australia.

Across the Australian Mining Cities Alliance regions of Mount Isa and Isaac, Broken Hill, Karratha, East Pilbara, and Kalgoorlie-Boulder, the unemployment rate sits at 3.58 percent, compared to the national average of 5.1 percent at the time of measurement. Median income in these mining regions reaches $74,490, against a national average of $41,860: a differential of $33,000 per household per year.

MCA chief executive Tania Constable framed the stakes directly: mining functions as the central driver of long-term regional development across Australia, sustaining communities that would otherwise face structural economic decline. In towns operating on a fine line between viability and contraction, with small population bases, stretched health and education services, and high infrastructure costs, critical minerals development can serve as the stabilising force that makes every other development pathway possible.

The Policy Enablement Challenge

Capital commitment does not automatically translate into operational projects. The MCA has been explicit that the progression of critical minerals projects requires policy settings that actually enable investment to proceed at scale. Its submission outlines a range of necessary reforms:

- Strengthening planning, environmental, and project approval systems to reduce timeline uncertainty

- Reforming the Native Title Act 1993 future acts framework to provide clearer pathways for project development

- Aligning migration and workforce training measures with the skills requirements of a scaling critical minerals sector

- Coordinating infrastructure planning across jurisdictions to prevent bottlenecks

- Expanding capability programmes for local and Aboriginal and Torres Strait Islander businesses

- Achieving cross-jurisdictional policy alignment to prevent capital from redirecting to competing jurisdictions

The MCA's submission to parliament warned that opportunities will only translate into regional economic strength if projects can actually move from approval to construction and into long-term operation, not just from announcement to press release.

This is the critical gap between diplomatic ambition and economic outcome. If Australian project approval timelines remain lengthy or unpredictable, Japanese corporate partners may redirect co-investment capital to alternative jurisdictions, regardless of the political commitments made at the bilateral level.

Technologies and Industries That Cannot Function Without These Minerals

The strategic importance of the designated minerals becomes clearer when mapped against the specific technologies they enable. This is not a list of industrial commodities. It is a list of the physical prerequisites for the advanced economy both Australia and Japan are attempting to build and protect. Furthermore, the growing critical minerals demand driven by the energy transition continues to intensify pressure on all of these supply chains simultaneously.

- Electric vehicle batteries: Nickel, cobalt, and graphite form the foundational chemistry of lithium-ion battery cathodes and anodes

- Artificial intelligence infrastructure: Gallium-based semiconductors underpin the chips powering data centre compute; rare earths are used in cooling systems and precision magnetic components

- Advanced defence systems: Rare earth elements are embedded in guided munitions, radar systems, communications equipment, and targeting hardware across every branch of modern military capability

- Renewable energy generation: Rare earths drive the permanent magnets in wind turbine generators; gallium is integral to high-efficiency solar panel manufacturing

- Quantum computing: Rare earth elements are increasingly investigated for qubit stabilisation in emerging quantum hardware architectures

The rapid scaling of AI compute infrastructure represents a demand vector for gallium and rare earths that did not exist at meaningful scale a decade ago. Data centre construction has accelerated globally at a pace that is creating supply pressure on multiple critical minerals simultaneously, adding urgency to the bilateral frameworks being established.

Three Scenarios for the Partnership's Future

The following scenarios are speculative projections based on current geopolitical and policy trajectories. They do not constitute financial advice or certainty about future outcomes.

Scenario 1: Accelerated Midstream Integration

If both governments successfully streamline project approvals and co-invest in processing infrastructure, Australia could transition toward a fully integrated supply chain partner within a decade. This would allow Australia to capture significantly more economic value per tonne of mineral extracted, shifting the terms of trade in its favour while providing Japan with price and supply certainty it cannot obtain elsewhere.

Scenario 2: Geopolitical Escalation Accelerates the Timeline

Further Chinese restrictions on mineral exports, particularly targeting gallium, graphite, or heavy rare earths, would dramatically intensify the urgency of the Australia-Japan pipeline. Emergency procurement arrangements and fast-tracked project approvals become possible under this scenario, compressing a decade-long development timeline into a matter of years.

Scenario 3: Regulatory Friction Diverts Capital

If Australian project approval timelines remain protracted and unpredictable, the capital committed under the 2026 declaration risks being delayed, restructured, or redirected. Alternative jurisdictions are actively competing for the same Japanese and allied investment. The diplomatic signing is a necessary but insufficient condition for the agreement's ultimate success.

The 2026 Australia-Japan Joint Declaration represents one of the most substantive bilateral minerals commitments in Indo-Pacific history. Whether it reshapes regional supply chains or fades into a footnote of diplomatic intention will be determined entirely by what happens on the ground in Australian mining regions over the coming years, not in the signing ceremony itself.

Frequently Asked Questions

What minerals are covered under the 2026 Australia-Japan critical minerals agreement?

The agreement covers nickel, cobalt, gallium, graphite, rare earth elements, and fluorite. These minerals are central to battery technology, semiconductor manufacturing, clean energy systems, and advanced defence applications.

How much has been committed under the 2026 joint declaration?

The total commitment is A$1.67 billion. Australia is contributing up to A$1.3 billion, with the remainder reflecting Japanese co-investment through corporate partners including Sumitomo Metal Mining and Mitsubishi.

Why is Japan so dependent on Australia for critical minerals?

Japan has negligible domestic critical mineral reserves and has historically relied on Chinese processing capacity for refined materials. Australia's geological abundance, political stability, and well-established trade infrastructure make it Japan's most viable and strategically aligned alternative supply partner.

What is the Goongarrie Hub and why does it matter?

Developed by Ardea Resources in partnership with Sumitomo Metal Mining and Mitsubishi, the Goongarrie Hub is one of Australia's largest nickel-cobalt resources. It is a flagship project under the 2026 agreement, directly targeting Japan's electric vehicle battery manufacturing supply chain.

What role does gallium play in Australia and Japan's critical minerals cooperation?

Gallium is a semiconductor-critical mineral subject to Chinese export restrictions since 2023. Australia's Alcoa Gallium Recovery Project, designated under the 2026 agreement, directly addresses this vulnerability for both Japanese and broader allied semiconductor supply chains.

How does the Australia-Japan agreement relate to the Australia-US framework?

Both frameworks operate as complementary diplomatic tracks within a coordinated allied strategy. The Australia-US Critical Minerals and Rare Earths Framework, signed by PM Albanese and President Trump, and the 2026 Australia-Japan Joint Declaration both reflect a shared objective of reducing dependence on Chinese mineral processing, with Australia positioned as the primary supply and midstream processing partner for both allied nations.

Want to Know Which ASX Mineral Discoveries Could Reshape Indo-Pacific Supply Chains?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced — instantly translating complex geological data into actionable investment insights across critical commodities including nickel, cobalt, rare earths, and gallium. Explore historic discoveries and the exceptional returns they have generated, then begin a 14-day free trial to position yourself ahead of the market before the next major find is announced.