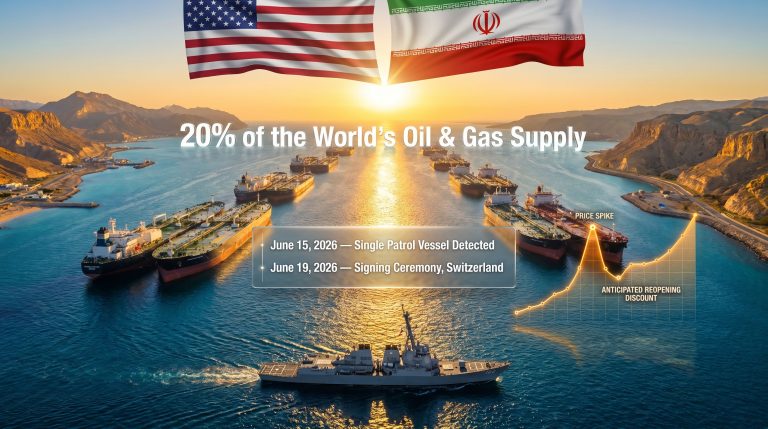

June 15, 2026

The Physical Reality Crude Markets Keep Ignoring

There is a peculiar behavioural pattern that repeats itself across commodity markets with clockwork regularity: traders respond to headlines before they respond to data. Geopolitical narratives move prices in hours, while physical supply conditions take weeks to register in the collective consciousness of market participants. The result is a recurring gap between sentiment-driven price discovery and ground-level commodity reality, and that gap is currently widening in the crude oil market in ways that deserve far closer attention than diplomatic headlines are receiving.

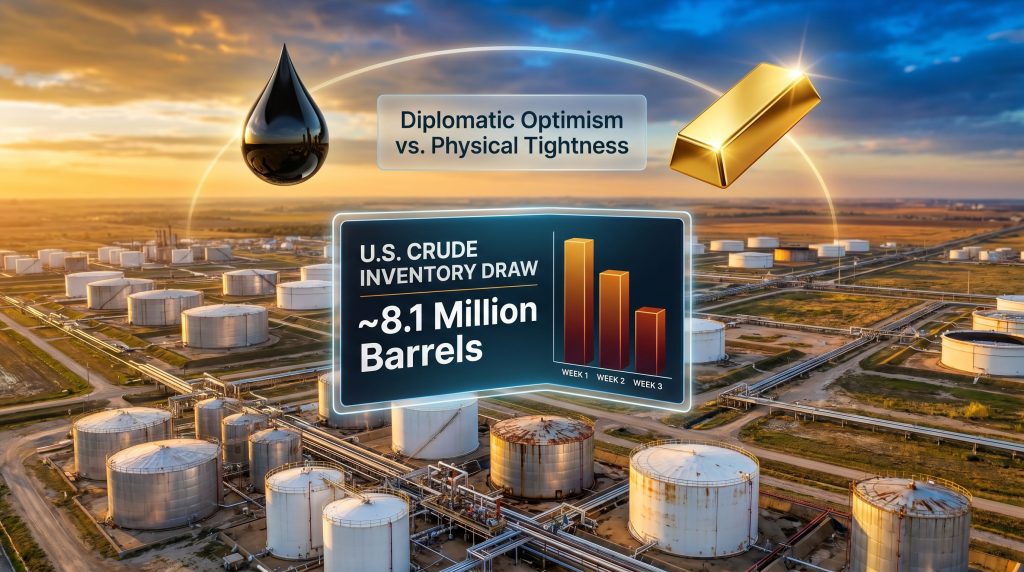

The phrase oil inventories near lows despite Iran peace chatter captures the essential contradiction defining energy markets heading into the second half of 2026. Prices are softening as traders price out geopolitical risk premiums, yet the physical infrastructure underpinning U.S. crude distribution is approaching stress levels that have historically preceded sharp and disorderly price corrections. Understanding why these two forces are moving in opposite directions, and which one ultimately dominates, is arguably the most important question in commodity markets right now.

When big ASX news breaks, our subscribers know first

What Critically Low Inventories Actually Mean for Supply Security

Most market observers treat inventory data as a directional indicator, a number that goes up or down and signals supply looseness or tightness. But the more important threshold is not directional at all. It is structural.

Crude oil storage facilities operate within a range bounded not just by capacity at the top, but by what industry professionals call the working storage minimum at the bottom. This floor represents the volume of oil that must remain in tanks at all times to maintain sufficient hydrostatic pressure for efficient pipeline pumping. When inventories fall below this threshold, the physical distribution network begins to lose operational integrity regardless of what futures markets are pricing.

Furthermore, the data currently painting this picture across U.S. crude inventories is striking:

| Indicator | Current Status | Market Significance |

|---|---|---|

| U.S. Weekly Crude Stocks | Multi-year lows | Removes pre-summer buffer capacity |

| Consecutive Weekly Draws | 3+ weeks of sustained declines | Signals structural rather than seasonal tightness |

| Single-Week Crude Draw | Approximately 8.1 million barrels | Unusually large for the pre-summer calendar period |

| Gasoline and Distillate Stocks | Declining in parallel | Confirms broad-based tightness across the entire barrel |

| Cushing, Oklahoma Hub | Approaching operational minimums | Creates acute stress at the WTI futures delivery point |

The breadth of these drawdowns matters as much as their depth. When crude, gasoline, and distillate stocks all fall simultaneously, it rules out simple product-mix explanations and points toward a genuine imbalance between aggregate supply and demand across the entire refining complex.

Why Cushing, Oklahoma Is the Single Most Important Number in U.S. Energy Markets

The Infrastructure Reality Behind WTI Pricing

Cushing, Oklahoma is not simply a storage location. It is the official physical delivery point for West Texas Intermediate futures contracts, which means it sits at the intersection of paper markets and physical reality in a way that few other commodity hubs do globally.

When a trader holds a WTI futures contract through to expiry, the underlying obligation is the physical delivery of crude oil at Cushing. This makes storage levels there uniquely consequential: they do not merely reflect supply and demand conditions, they directly constrain the mechanical function of the futures market itself.

Several cascading effects emerge as Cushing inventories approach operational minimums:

- Physical buyers face pipeline flow restrictions as tanks approach sludge-level thresholds where oil can no longer be pushed efficiently through infrastructure

- Futures market liquidity deteriorates as the physical delivery mechanism becomes constrained

- Refineries ramping up throughput for summer production schedules face feedstock availability risk that cannot be resolved through financial hedging

- Speculative short sellers face the prospect of forced short-covering as the physical squeeze tightens, amplifying price volatility

- The WTI forward curve can move into severe backwardation, reflecting acute near-term scarcity versus longer-dated supply expectations

Cushing inventory stress does not resolve on diplomatic timelines. Even if Iran negotiations produced an enforceable agreement tomorrow, restoring physical crude inventories at Cushing takes weeks to months of logistics, production ramp-up, and pipeline scheduling. The near-term supply risk is structurally present regardless of geopolitical headlines.

The Sludge Threshold: A Concept Most Investors Have Never Heard Of

One of the least understood dynamics in physical crude markets is what happens as storage approaches its absolute operational floor. Industry practitioners refer to the residual material at tank bottoms as sludge, a mixture of heavy hydrocarbons, sediment, and water that accumulates over time and cannot be efficiently pumped. As usable inventory shrinks toward this layer, the effective pumping capacity of the facility degrades before the tank is technically empty.

This means the practical operational floor is higher than the nominal empty level, and markets that focus purely on headline inventory numbers may systematically underestimate how close the physical system is to genuine stress. The warning signs do not always wait until tanks read zero.

Is the Iran Peace Narrative Actually Bearish for Oil?

How Geopolitical Relief Gets Priced Into Crude Markets

When de-escalation narratives emerge around Iran, crude markets follow a predictable sequence of adjustments. Consequently, the oil and geopolitics relationship plays out through several overlapping mechanisms:

- The geopolitical risk premium is stripped out of Brent and WTI spot prices, sometimes representing several dollars per barrel depending on perceived conflict risk

- Strait of Hormuz supply assumptions are revised upward, given that approximately 20% of global seaborne crude transits this chokepoint

- Speculative long positions are liquidated by traders who had been holding them as conflict insurance

- The forward curve compresses as near-term tightness expectations ease and longer-dated supply normalisation gets priced in

Each of these adjustments is individually rational. Taken together, they produce the price softening currently observed in crude markets.

Why the Bearish Reaction May Be Getting Ahead of Reality

The critical analytical error in this framework is conflating diplomatic optimism with physical supply. These are different things on different timescales.

Iran has featured in de-escalation narratives repeatedly across the past decade, with markets pricing in supply normalisation multiple times before agreements either collapsed or produced far less additional supply than anticipated. Even a genuinely formalised framework involves sanctions relief processing, production infrastructure restart timelines, tanker fleet mobilisation, and buyer relationship re-establishment, all of which extend the gap between headline and barrel by months at minimum.

However, the 8.1 million barrel single-week crude draw that recently registered in U.S. data happened in the present tense, not in a diplomatic future. The asymmetry between what is actually occurring in physical markets and what diplomacy might eventually deliver is the core tension the market appears to be underweighting. For a broader view of how these forces interact with crude price trends, the medium-term picture remains notably complex.

Three Scenarios for Crude Pricing Over the Next 60 to 90 Days

| Scenario | Diplomatic Track | Inventory Trajectory | Probable Price Direction |

|---|---|---|---|

| Bear Case | Iran deal confirmed with rapid sanctions lifting | Inventories stabilise as new supply enters market | WTI and Brent decline meaningfully from current levels |

| Base Case | Negotiations continue but face delays or partial progress | Inventories remain structurally tight through peak summer | Prices stay range-bound with a modest upside bias |

| Bull Case | Talks stall, collapse, or are reversed by either party | Inventories hit operational floors at Cushing | Sharp WTI spike driven by physical market squeeze |

The base case commands the highest probability weighting given the historical pattern of Iran-related diplomatic timelines, but the bull case carries disproportionate price impact relative to its probability, given the physical infrastructure stress already present at Cushing.

Peak Summer Demand: The Seasonal Amplifier Markets Are Underestimating

Why Timing Matters More Than Direction

The U.S. summer driving season, which typically peaks between Memorial Day and Labor Day, represents the single largest seasonal surge in refined product demand across the domestic energy calendar. Refineries respond by running at elevated throughput rates, drawing heavily on crude feedstocks across precisely the window when inventories are currently most stressed.

Drawing down stocks at current rates before this demand peak removes the buffer that refineries rely on to manage unexpected supply disruptions, maintenance events, or weather-related logistics interruptions. The combination of:

- Low entering inventory levels at the start of peak demand season

- Declining gasoline and distillate stocks indicating refineries are already running hard

- Cushing approaching operational stress thresholds at the WTI delivery hub

- Diplomatic timelines that cannot deliver physical barrels in weeks

creates a compounding risk profile that diplomatic optimism cannot fully offset. Historically, this timing pattern — low stocks meeting high seasonal demand — has been associated with refinery margin spikes, retail fuel price surges, and elevated crude price volatility through the summer months. Analysts tracking oil market dynamics have noted that this seasonal amplifier is particularly pronounced when entering the peak period with depleted buffers.

The next major ASX story will hit our subscribers first

Gold and Oil: Why the Same News Produces Opposite Price Reactions

Understanding the Transmission Mechanism Difference

One of the more instructive features of the current macro environment is observing how gold and crude oil respond to identical geopolitical catalysts through entirely different economic channels. The same Iran peace narrative that softens crude prices is simultaneously constructive for precious metals, and the mechanism is worth examining carefully.

The transmission pathway for gold runs as follows:

- Middle East de-escalation reduces geopolitical risk embedded in global energy costs

- Lower energy costs feed directly into headline inflation figures across major economies

- Cooler inflation reduces pressure on central banks to maintain restrictive monetary policy, creating conditions for yield compression or rate cuts

- Declining real interest rates reduce the opportunity cost of holding non-yielding assets like gold

- Gold prices respond positively to the disinflationary impulse driven by the same peace narrative that weighs on crude

In addition, gold safe-haven demand has remained structurally elevated through much of 2025 and into 2026, underpinning the metal's resilience even as short-term geopolitical risk premiums fluctuate.

Oil prices reflect physical supply expectations. Gold prices reflect real interest rate and monetary policy expectations. The same geopolitical catalyst feeds both systems through entirely different channels, producing divergent price outcomes that are not contradictory but mechanically consistent.

This divergence provides a useful analytical framework for portfolio positioning during geopolitical de-escalation cycles: energy exposure faces near-term headwinds from sentiment while physical fundamentals remain supportive, whereas precious metals exposure benefits from the disinflationary monetary transmission even as the underlying catalyst is the same headline.

El Niño Adds a Southern Hemisphere Dimension to the Commodity Outlook

The Bureau of Meteorology has officially declared the commencement of El Niño conditions, introducing a separate but overlapping layer of commodity market risk that intersects with the global energy and agricultural picture.

For Australian commodity markets specifically, the implications span several sectors:

- Agricultural soft commodities face supply pressure from drought risk, historically driving domestic food inflation and export volume reductions

- Power grid stress from extreme heat events increases electricity demand, placing upward pressure on gas and thermal coal pricing during peak load periods

- Bushfire risk threatens regional logistics infrastructure and supply chains, with potential flow-on effects for mining operations and transport costs

- Water availability constraints affect mining operations across affected regions, with potential impacts on production output and operating cost structures

El Niño conditions also interact with global agricultural commodity pricing in ways that extend beyond Australian borders, given the country's role as a significant exporter of wheat, barley, and other weather-sensitive commodities.

Key Indicators to Monitor Over the Coming Quarter

For investors and market participants navigating this environment, the following data points represent the most direct signals of how the competing forces described above are resolving:

- Weekly EIA Crude Inventory Reports: Watch for sustained draws versus any inventory rebuild that would suggest supply is catching up with demand

- Cushing, Oklahoma storage levels: The operational floor threshold is the critical line; any approach toward it deserves attention disproportionate to its media coverage

- Iran diplomatic timeline specificity: Distinguish between framework announcements and enforceable agreements with confirmed sanctions relief timetables

- U.S. summer driving season gasoline consumption data: The rate of gasoline drawdown through June and July will determine whether the oil inventories near lows despite Iran peace chatter dynamic deteriorates further

- Gold-oil ratio movements: A widening ratio signals sustained disinflationary pressure; a narrowing ratio suggests the physical crude supply squeeze is beginning to dominate

- El Niño weather development monitoring: Agricultural and energy grid impacts will become clearer as the Southern Hemisphere winter progresses

For further context on current market positioning, Reuters analysis offers useful coverage of how oil markets are responding to the evolving U.S.-Iran diplomatic situation, while Baird Maritime provides a shipping and tanker industry perspective on how peace prospects are influencing crude transport flows.

This article is intended for informational and educational purposes only and does not constitute financial product advice. Forecasts, scenarios, and market analysis presented here involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers should consult a qualified financial adviser before making any investment choices.

Want to Stay Ahead of the Next Major Commodity Market Move?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across oil, gold, and 30+ other commodities — turning complex market data into actionable investment insights before the broader market catches on. Explore historic discoveries and their returns, then begin your 14-day free trial to position yourself ahead of the next major market shift.