June 30, 2026

Understanding Australia's Economic Vulnerability to External Shocks

Australia's economic framework presents a fascinating paradox that creates unique vulnerability to external price pressures. The nation operates as a major commodity exporter while simultaneously maintaining heavy dependence on imported refined petroleum products, creating dual exposure that can amplify economic volatility during periods of global uncertainty. These stagflation concerns in Australia have intensified as global economic conditions shift dramatically.

This structural imbalance becomes particularly pronounced when energy markets experience rapid price movements, as witnessed during recent geopolitical tensions that drove oil prices sharply higher. The transmission mechanism operates through multiple channels, affecting everything from transportation costs to manufacturing inputs, while simultaneously impacting the competitiveness of Australia's export sectors in global markets.

The Import Dependency Reality

Australia's reliance on imported refined petroleum products represents approximately 90% of domestic consumption, creating immediate vulnerability to global energy price fluctuations. This dependency means that external oil price increases translate directly into domestic cost pressures across virtually every sector of the economy, from logistics and manufacturing to household energy expenses.

The import dependency extends beyond simple fuel costs to encompass broader supply chain implications. When global energy prices surge, the cost structure of Australian businesses faces immediate pressure. Furthermore, the ability to pass these costs through to consumers depends heavily on domestic demand conditions and competitive dynamics within individual sectors.

Monetary Policy Constraints in a Resource Economy

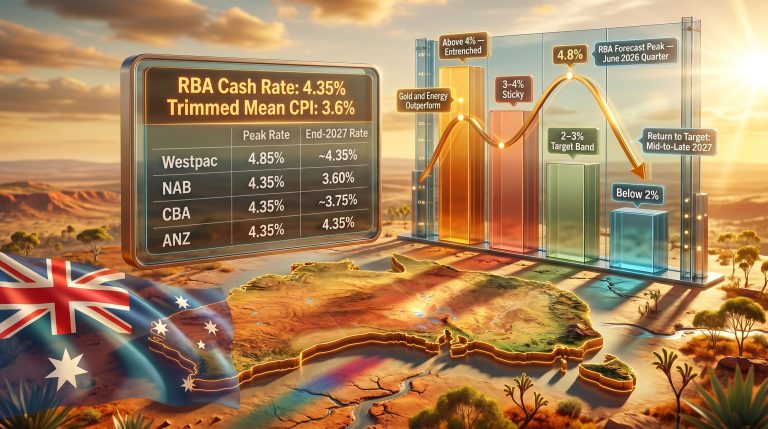

The Reserve Bank of Australia operates within a complex framework where traditional monetary policy tools must navigate the competing pressures of commodity price volatility and domestic economic conditions. Current cash rate positioning reflects this delicate balance, as policymakers attempt to maintain price stability while supporting sustainable economic growth.

However, persistent energy price increases create a policy dilemma that could force additional monetary tightening. This constraint becomes particularly binding when external price shocks coincide with weakening domestic demand, potentially creating the conditions for stagflationary pressures to emerge in circumstances where domestic economic conditions might otherwise warrant policy easing.

When big ASX news breaks, our subscribers know first

Energy Price Transmission and Inflationary Dynamics

The relationship between energy prices and broader inflation in the Australian context operates through multiple interconnected channels that can amplify initial price shocks. Recent market developments demonstrate how quickly external energy dynamics can alter Australia's inflation trajectory, with this oil price rally particularly concerning for policymakers.

Direct Cost Transmission Mechanisms

Energy price increases flow through the Australian economy via several direct channels:

- Transportation costs: Affecting freight, logistics, and passenger transport

- Industrial inputs: Impacting manufacturing and processing sectors

- Household energy: Direct utility bill increases for consumers

- Agricultural production: Fuel and fertiliser cost increases

These direct effects create immediate inflationary pressure that monetary policy cannot easily offset. In addition, they represent genuine increases in production costs rather than demand-driven price pressures.

Second-Round Effects and Expectations

The more concerning aspect of energy price shocks lies in their potential to trigger second-round effects through inflation expectations and wage-price dynamics. When businesses and consumers expect energy-driven inflation to persist, these expectations can become embedded in wage negotiations, pricing decisions, and investment planning.

This expectations channel represents the primary mechanism through which temporary energy price shocks can evolve into persistent inflationary pressures. Consequently, it may require more aggressive monetary policy responses to contain the broader economic implications.

China's Economic Slowdown and Australia's Terms of Trade

China's economic performance exerts profound influence on Australia's economic outlook through trade linkages that extend far beyond simple commodity exports. Recent indicators pointing to below-trend growth in China create particular challenges for Australia's resource-dependent economy, with iron ore price trends reflecting these concerns.

Commodity Demand Destruction Patterns

Chinese economic deceleration affects Australian exports through multiple channels:

Key Export Vulnerabilities:

- Iron ore demand linked to Chinese steel production

- Thermal coal consumption tied to industrial activity

- Lithium demand connected to battery production capacity

- Agricultural exports facing reduced Chinese consumer demand

The China Composite Leading Indicator readings provide early warning signals about demand conditions that directly impact Australia's key export revenues. For instance, this creates external sector pressures that compound domestic economic challenges.

Terms of Trade Deterioration Risks

When Chinese demand weakens while global energy costs rise, Australia faces the challenging scenario of deteriorating terms of trade. Export commodity prices face downward pressure while import costs, particularly energy, experience upward pressure.

This combination creates external sector stress that can constrain domestic economic growth while maintaining inflationary pressures. However, these dynamics establish the fundamental conditions for stagflation concerns in Australia to materialise and potentially worsen.

Financial Market Risk Repricing and Economic Concerns

Financial markets have begun repricing equity risk premiums to reflect growing concerns about stagflationary scenarios. The ASX 200's significant weekly decline represents more than simple profit-taking, indicating fundamental reassessment of economic trajectory assumptions amid global trade tensions and domestic vulnerabilities.

Equity Market Vulnerability Indicators

Recent market performance reveals several concerning patterns:

| Sector | Weekly Performance | Key Drivers |

|---|---|---|

| Materials | -4.0% decline | Chinese demand concerns |

| Energy | Mixed (+1% to -1%) | Stagflation fears offset commodity gains |

| Financials | Under pressure | Rising rates, credit risk concerns |

| Consumer Discretionary | Weakness | Household spending pressure |

The disconnect between rising energy prices and modest energy sector gains illustrates how stagflationary concerns can override traditional commodity price benefits. Furthermore, investors weigh higher input costs against potential demand destruction.

Safe Haven Asset Flows

Gold's breakthrough above A$5,000 per ounce represents classic stagflationary hedging behaviour. Investors seek assets capable of maintaining purchasing power during periods of high inflation and economic uncertainty, with gold as an inflation hedge becoming increasingly attractive.

Government bond markets are simultaneously repricing scenarios where the RBA may need to maintain restrictive monetary policy for extended periods. Consequently, this could potentially require additional rate increases despite weakening growth prospects.

Sectoral Vulnerabilities and Performance Divergence

Different sectors of the Australian economy exhibit varying degrees of vulnerability to stagflationary pressures. Resource companies face particularly complex dynamics despite their traditional role as inflation hedges.

The Resource Sector Paradox

Major resource companies experienced significant declines despite rising commodity prices, highlighting the market's focus on demand destruction rather than short-term price benefits:

Resource Company Performance During Energy Price Surge:

- BHP: -4.1% weekly performance

- Rio Tinto: -4.3% decline

- Fortescue: -2.9% decrease

- Woodside: +1.0% modest gain

- Santos: +1.4% limited upside

This performance pattern reflects investor concerns about Chinese demand sustainability rather than celebration of higher commodity prices. In addition, it indicates market sophistication in pricing complex economic scenarios.

Consumer Sector Pressure Points

Consumer discretionary sectors face dual pressure from higher energy costs and elevated interest rates. This creates a squeeze on household disposable income that affects retail, hospitality, and consumer services companies relying on sustained consumer confidence.

Financial services companies encounter the challenge of rising funding costs alongside increased credit risk as economic growth slows. However, this could potentially create margin compression and require higher provisions for loan losses.

Economic Data Manifestation Patterns

Stagflation concerns in Australia typically manifest through specific patterns in key economic indicators that distinguish them from standard recessionary or inflationary periods. Understanding these patterns provides insight into monitoring frameworks for detecting stagflationary developments.

Growth Deceleration Indicators

Stagflationary periods are characterised by:

- GDP growth: Persistently below-trend performance (sub-2% annually)

- Productivity growth: Declining efficiency measures

- Business investment: Reduced capital expenditure despite capacity constraints

- Consumer spending: Weakening discretionary expenditure

Current forecasts suggesting 2.0-2.2% growth for 2026 remain vulnerable to downward revision if energy costs maintain elevated levels. Furthermore, this risk increases while Chinese demand continues weakening.

Labour Market Stress Signals

Employment conditions during stagflationary periods often exhibit counterintuitive patterns:

Critical Monitoring Metrics:

- Unemployment rate progression above 4.5%

- Underemployment increases despite headline job creation

- Real wage growth turning negative

- Labour force participation rate declines

- Skills mismatches in tight labour markets

Inflation Persistence Measures

Core inflation measures, particularly trimmed mean CPI, remaining above 3% for extended periods would indicate embedded stagflationary pressures. This becomes particularly concerning when driven by services inflation rather than temporary supply shocks.

The next major ASX story will hit our subscribers first

Policy Response Frameworks and Constraints

Policymakers face significant constraints when addressing stagflationary pressures. Traditional monetary and fiscal policy tools can exacerbate rather than resolve the underlying economic tensions that create these conditions.

Monetary Policy Dilemmas

The RBA confronts limited options in a stagflationary environment where conventional policy responses create unintended consequences:

- Rate increases: Combat inflation but risk deepening growth slowdown

- Rate cuts: Support growth but could entrench inflation expectations

- Policy paralysis: Maintaining status quo while conditions deteriorate

This policy constraint represents one of the defining characteristics of stagflationary periods. However, central banks lose their traditional ability to stabilise economic conditions through interest rate adjustments.

Fiscal Policy Considerations

Government spending programs face similar challenges, where stimulative measures could provide growth support but risk adding to inflationary pressures. Targeted energy subsidies might provide temporary household relief but could distort price signals and delay necessary economic adjustments.

Structural Reform Imperatives

Long-term solutions require addressing fundamental structural vulnerabilities:

- Domestic refining capacity expansion

- Renewable energy transition acceleration

- Supply chain diversification initiatives

- Energy storage infrastructure development

These reforms require sustained political commitment and significant capital investment. Consequently, they become difficult to implement during periods of economic stress when resources are constrained.

Investment Strategy Frameworks for Stagflationary Periods

Stagflationary environments require fundamental reconsideration of traditional investment approaches. Both growth and income strategies face unique challenges when inflation remains elevated while economic growth stagnates, making the gold market outlook particularly relevant for portfolio construction.

Real Asset Allocation Strategies

Historical analysis indicates that certain asset classes demonstrate superior performance during stagflationary periods:

Stagflation-Resistant Asset Categories:

- Precious metals: Direct inflation hedge with currency debasement protection

- Real estate: Assets with inflation-linked rental income streams

- Infrastructure: Essential services with regulated pricing power

- Commodity producers: Companies maintaining pricing power in essential materials

Gold's recent performance above A$5,000 per ounce exemplifies investor recognition of precious metals' role as inflation hedges. Furthermore, this occurs during periods of currency debasement concerns.

Equity Sector Positioning

Companies demonstrating strong pricing power, essential service provision, or inflation-linked revenue streams typically outperform during stagflationary periods:

- Utilities: Regulated pricing mechanisms and essential service provision

- Healthcare: Inelastic demand characteristics and aging demographic trends

- Consumer staples: Non-discretionary consumption patterns

- Energy infrastructure: Long-term contracts with inflation escalation clauses

Currency and International Diversification

A weakening Australian dollar during stagflationary periods can benefit international equity exposure while providing natural hedging against domestic economic deterioration. Currency diversification becomes particularly important when domestic purchasing power faces persistent erosion.

Risk Monitoring and Early Warning Systems

Effective monitoring of stagflation risk development requires comprehensive tracking of leading indicators across multiple economic dimensions. This provides early warning signals before stagflation concerns in Australia become entrenched and more difficult to address.

Critical Metrics Dashboard

| Indicator | Current Level | Stagflation Threshold | Monitoring Frequency |

|---|---|---|---|

| Core CPI | ~3.1% | >3.5% sustained | Monthly |

| GDP Growth | 2.0-2.2% forecast | <1.5% sustained | Quarterly |

| Unemployment | 4.3% | >5.0% | Monthly |

| Oil Prices | Brent $85/WTI $80 | >$90 sustained | Daily |

| RBA Cash Rate | 3.85% | >4.1% | Monthly |

| China Leading Indicator | 98.80 | <98.0 sustained | Monthly |

Market Sentiment Gauges

Real-time market indicators provide immediate insight into how financial markets are pricing stagflationary scenarios:

- Equity volatility indices: Measuring uncertainty and risk aversion

- Credit spreads: Indicating credit market stress and default expectations

- Commodity curve structures: Revealing supply-demand expectations

- Currency volatility: Reflecting exchange rate uncertainty

Policy Communication Analysis

Central bank communication patterns offer crucial insight into policymaker assessment of stagflationary risks. RBA statements regarding the balance between growth and inflation objectives provide early indication of policy direction changes.

The current confluence of rising energy costs, weakening Chinese demand, and monetary policy constraints creates legitimate foundations for ongoing economic monitoring. However, these conditions require careful assessment and adaptive policy responses to navigate potential challenges ahead.

Disclaimer: This analysis contains forward-looking statements and economic projections that involve inherent uncertainty. Past performance does not guarantee future results. Investors should consider their individual financial circumstances and consult with qualified financial advisors before making investment decisions. Economic conditions can change rapidly, and stagflationary scenarios represent one of several possible economic outcomes.

Ready to Navigate Market Volatility from Australia's Stagflation Risks?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, helping investors identify opportunities that can outperform during periods of economic uncertainty like potential stagflationary conditions. See how historic discoveries can generate substantial returns by exploring Discovery Alert's discoveries page, then begin your 14-day free trial to position yourself ahead of market volatility.