July 15, 2026

The LPG Industry's Next Competitive Frontier Is Not Upstream — It's Infrastructure

The energy transition debate tends to fixate on what fuels will be replaced, overlooking a more immediate and commercially critical question: which companies will control the infrastructure required to move affordable energy to the billions of people who still lack it. In the global LPG sector, Aygaz US LPG and clean cooking opportunities are rapidly becoming the defining competitive variable, and the window to build durable positions is narrowing.

Three converging macro forces are simultaneously reshaping how LPG flows around the world. First, US export capacity is entering a period of significant expansion, with new upstream projects expected to increase Mont Belvieu supply volumes by 30 to 50 percent in 2027 and 2028. Second, clean cooking transitions across sub-Saharan Africa and South Asia are accelerating at a pace that is outstripping distribution capacity. Third, geopolitical disruption to traditional Middle Eastern supply corridors has stress-tested procurement strategies and exposed the vulnerabilities of operators relying heavily on spot market access.

These forces are not unrelated. They are converging into a structural opportunity for operators who combine trading scale, owned shipping assets, and last-mile distribution networks across emerging markets. Understanding how Aygaz is positioning itself within this framework offers a rare window into how the world's most sophisticated regional LPG operators are thinking about the next decade.

When big ASX news breaks, our subscribers know first

Why US LPG Is Reshaping Global Trade Economics

Mont Belvieu: The World's Marginal Price Setter

Mont Belvieu in Texas has become the reference point around which global LPG trade economics are increasingly organised. The hub already offers the most competitively priced LPG supply globally, and this pricing advantage is set to widen as new US upstream projects reach production. LPG pricing benchmarks indicate that the projected 30 to 50 percent increase in US LPG supply through 2027 and 2028 means a significant volume of product must find export destinations, reinforcing the structural importance of shipping and terminal infrastructure to capture this arbitrage.

Turkey's own imports from the US reached record highs in the first half of 2026, driven by simultaneous disruptions to both Algerian and Russian supply channels. This was not an isolated event but a preview of a structural reorientation in Atlantic Basin LPG trade flows that is likely to persist well beyond any individual geopolitical episode.

The VLGC Technology Edge: LPG as Its Own Fuel

One of the less widely understood dynamics in this shift is the role of LPG-fuelled Very Large Gas Carriers, or VLGCs. Modern vessels in this class are capable of consuming LPG drawn directly from the cargo as propulsion fuel. This seemingly technical detail carries profound commercial implications.

On a typical 27 to 28 day voyage from the US Gulf Coast to Asian or Mediterranean markets, a fuel oil-powered vessel incurs propulsion costs of approximately $700 to $800 per tonne. An LPG-fuelled VLGC reduces this to approximately $400 per tonne, simultaneously cutting both voyage economics and carbon intensity. For operators moving millions of tonnes annually, this cost differential compounds into a material competitive advantage over the life of the vessel fleet.

Aygaz has committed $353 million to ordering three new VLGCs, a capital allocation decision grounded in the logic that operators who own the shipping infrastructure capture the arbitrage value that would otherwise accrue entirely to third-party vessel owners. As Aygaz's chief executive Melih Poyraz noted when discussing this investment, the correlation between Mont Belvieu arbitrage spreads and VLGC charter rates means that when the trade opportunity widens, so do the returns for those who own the vessels.

Strategic Insight: The average age of the global LPG tanker fleet remains elevated. As US export volumes scale, operators without owned modern shipping capacity will face increasing exposure to spot VLGC rate volatility during periods of peak trade demand.

Aygaz's Operational Scale and Market Position

Turkey as a Platform, Not a Ceiling

Aygaz commands more than 50 percent of both the retail and wholesale LPG sectors in Turkey, one of the world's most developed autogas markets. This domestic dominance generates the cash flow and operational credibility that underpins international expansion, but the company's leadership is explicit that Turkey is a platform, not a destination.

Current annual trading volumes of 2.4 to 2.5 million tonnes are targeted to reach 5 million tonnes per year within a decade. The pathway to this target runs through Africa and Southeast Asia, with the company's Bangladesh joint venture serving as the operational proof-of-concept for the model.

The Cylinder Market and the 2 Million Car Opportunity

Within Turkey itself, the near-term demand story rests on two distinct dynamics. The cylinder market, currently around 500,000 tonnes per year, is expected to hold relatively steady as natural gas network penetration has largely reached saturation.

The more significant near-term catalyst is the autogas conversion opportunity. Turkey has an estimated 2 million gasoline-powered vehicles manufactured between 2010 and 2020 that represent viable conversion candidates. As US supply growth drives Mont Belvieu prices lower, the economic case for converting these vehicles to LPG autogas strengthens. Aygaz is actively engaged with both conversion companies and automotive manufacturers to accelerate factory-fitted LPG vehicle production, with particular focus on price-sensitive consumers outside major urban centres.

While hybrid and electric vehicle sales are growing in Turkey, the mass market, particularly in regional Anatolian areas, remains highly price-sensitive. LPG autogas retains a durable competitive position in this segment, and a falling global LPG price environment could meaningfully accelerate conversion rates.

Bangladesh: A Proof-of-Concept for Emerging Market Execution

From Zero to 12% Market Share in Four Years

The acquisition of a 50 percent stake in United Aygaz LPG in Bangladesh in 2019 has become one of the more compelling case studies in emerging market LPG expansion. Within four years of that initial investment, the joint venture grew from a standing start to a 12 percent market share at 300,000 tonnes per year, a trajectory that validates the greenfield entry model Aygaz intends to replicate elsewhere.

The structural foundation of this success is proprietary infrastructure. The Chittagong terminal, with 16,000 tonnes of storage capacity, is the only facility in Bangladesh capable of receiving midsize LPG vessels carrying up to 22,000 tonnes. This creates a competitive moat that is not easily replicated by competitors lacking the capital or planning lead time to build comparable infrastructure.

Bangladesh Infrastructure Expansion Timeline

| Facility | Current Capacity | Planned Expansion | Target Completion |

|---|---|---|---|

| Chittagong Terminal | 16,000t | +5,000t additional capacity | End of 2026 |

| Dhaka Storage Site | 3,000t | Expansion to 5,500t | H2 2027 |

| Chittagong Port Capability | 22,000t vessel handling | Only facility of its kind in Bangladesh | Operational |

Bangladesh's demand fundamentals are compelling. A population exceeding 200 million people, declining domestic natural gas supply being redirected toward industrial use, and a large young demographic cohort moving toward middle-income consumption all point toward a long-runway growth opportunity. The price sensitivity of Bangladeshi consumers, where demand destruction occurs near-immediately in response to Saudi Aramco Contract Price increases, underscores the importance of supply chain security and term-contract procurement discipline for operators serving this market.

During the Strait of Hormuz disruption caused by the Iran conflict, Aygaz's Bangladesh operation demonstrated this discipline in practice. Because the joint venture had secured term contracts with US suppliers in addition to Gulf sources, it was the only operator in the country able to maintain consistent supply availability, prioritising market stability over short-term margin optimisation.

Geopolitical Risk Management: Lessons From the Hormuz Disruption

Procurement Architecture as a Competitive Differentiator

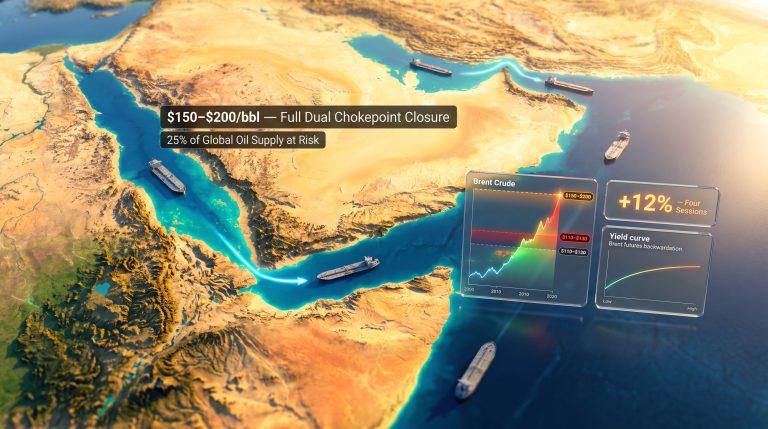

The temporary closure of the Strait of Hormuz served as an unplanned but highly instructive stress test of global LPG supply chain resilience. For Turkey, the insulating factor was the composition of its supply base. With procurement predominantly sourced from the US and Algeria rather than the Mideast Gulf, physical supply continuity was maintained. However, the disruption triggered a sharp spike in tanker rates as the entire market scrambled for available vessels, creating punishing cost conditions for buyers reliant on spot procurement.

Aygaz's risk management framework operates on an 80 percent term contract, 20 percent spot procurement split. When market stress materialised, the company drew down terminal inventories, typically maintained at approximately 60,000 tonnes, to avoid purchasing at peak spot premiums. This inventory management discipline, combined with the term-contract ratio, is not incidental to the company's risk architecture but a deliberate and tested strategy. Furthermore, understanding commodity market volatility is essential context for appreciating why this kind of procurement discipline matters so profoundly.

Russia's Ust-Luga Terminal: Conditional Optionality

Russia's new Ust-Luga terminal, capable of loading VLGCs, presents a geographically compelling supply option for Turkish buyers given proximity. However, the current sanctions environment constrains Russian cargo flows in a way that infrastructure capability alone cannot overcome. Any meaningful increase in Russian LPG imports to Turkey remains contingent on a broader geopolitical normalisation, representing what might be characterised as conditional optionality in supply diversification planning.

A peace scenario in Ukraine and associated sanctions unwinding would reopen this corridor, potentially reshaping the competitive economics of Bosphorus-region LPG trade meaningfully. For now, it remains a scenario to monitor rather than a basis for supply planning.

Black Sea Security and Re-Export Constraints

Drone attack risk in the Black Sea region is currently the primary constraint on LPG re-export flows to Bulgaria and other regional markets. Insurance cost escalation driven by maritime security risk directly compresses the economics of short-haul re-export routes. Syria's post-sanctions reopening and a potential normalisation of the Iran corridor represent the two most significant near-term upside scenarios for regional trade volume expansion. These dynamics are closely linked to broader trade war impacts that continue to reshape global energy flows in 2025.

The Clean Cooking Market: Scale, Urgency, and Commercial Opportunity

Sub-Saharan Africa: Fastest-Growing Clean Cooking Market in the World

The IEA's 2026 progress report on clean cooking describes an acceleration that is reshaping investment and trade flows across the LPG industry. Around 12 million people gained access to clean cooking in sub-Saharan Africa in 2024, three times the number who did so in 2010. Early data for 2025 points to a record 15 million people gaining access, with LPG accounting for approximately 90 percent of all fuel transitions since 2024.

The investment backdrop is substantial and growing. Governments and companies pledged a further $900 million for clean cooking initiatives in sub-Saharan Africa at a recent IEA online event, adding to the $2.2 billion secured at the IEA's Paris summit in 2024. Of the $750 million already disbursed from that summit pledge, nearly half has gone directly to LPG, reflecting the fuel's dominant position in the transition.

Clean Cooking Market Data at a Glance

| Metric | Data Point |

|---|---|

| Sub-Saharan Africa clean cooking access gains (2024) | ~12 million people |

| Projected gains (2025) | ~15 million people (record) |

| LPG share of clean cooking transitions since 2024 | ~90% |

| Total clean cooking investment pledges (Africa) | $3.1 billion+ |

| LPG's share of direct investment in clean cooking | ~75% |

| Sub-Saharan Africa LPG storage capacity | ~800,000t (+12% since 2021) |

| Additional LPG storage under development (Africa) | 250,000t+ |

West Africa is the fastest-growing sub-region, with access expanding more than twice as fast as other parts of sub-Saharan Africa between 2020 and 2024. Nigeria, Ghana, Ivory Coast, and Senegal are the primary growth markets. Senegal alone saw butane imports nearly double to approximately 11,000 barrels per day, or 372,000 tonnes per year, in 2025 to meet the needs of roughly five million people.

It is worth noting, however, that sub-Saharan Africa's LPG supply is heavily dependent on US exports, with approximately 80 percent of the region's imports arriving from the US. The Strait of Hormuz disruption, while not directly impacting physical supply to the region, caused East African import prices to roughly double compared with 2025 averages, while west African prices rose by approximately 70 percent, demonstrating the indirect price transmission risk that comes with dependence on globally priced commodities.

Why LPG Dominates the Transition

LPG's appeal in emerging market clean cooking is not simply a matter of cost. Its portability, high energy density, and compatibility with existing cylinder-based distribution systems make it the most deployable near-term solution for off-grid and semi-urban populations. The fuel now accounts for 70 percent of all people in sub-Saharan Africa with clean cooking access. These developments sit firmly within the broader context of energy transition and security, where LPG plays a critical bridging role for developing nations.

Key Insight: Aygaz's clean cooking expansion into Africa and Southeast Asia is not a philanthropic positioning exercise. It is a commercially structured growth strategy targeting markets where LPG demand is at the very beginning of a multi-decade adoption curve.

The next major ASX story will hit our subscribers first

Pay-As-You-Go LPG: Unlocking Demand in Price-Sensitive Markets

Removing the Upfront Barrier to Adoption

One of the structural barriers to LPG uptake in low-income markets is the upfront cost burden associated with cylinder procurement and refilling infrastructure. Pay-As-You-Go (PAYG) smart meter technology addresses this directly by enabling households to purchase LPG in micro-increments, with transactions starting from as little as $0.50, without bearing the full cylinder cost upfront.

This model, which has been pioneered largely by US-based innovators, is now scaling across sub-Saharan Africa and South Asia. Its commercial significance extends beyond affordability. By breaking the price elasticity barrier at the point of household adoption, PAYG technology effectively opens a market segment that was previously inaccessible to conventional LPG distribution economics.

The contrast between how Turkish and Bangladeshi consumers respond to LPG price changes illustrates why this technology matters so much for emerging market expansion:

| Market | Consumer Price Sensitivity | Key Driver | Demand Elasticity |

|---|---|---|---|

| Turkey | Moderate | Government consumption tax adjustments buffer price swings | Relatively inelastic |

| Bangladesh | High | Lower income per capita; direct exposure to Saudi CP movements | Highly elastic |

In Turkey, the government has the capacity to reduce the special consumption tax on fuels during periods of global price spikes, effectively buffering the pass-through to end consumers. When global prices fell after the Hormuz disruption eased, the tax rate was adjusted back upward. This policy flexibility provides a structural demand stabiliser that simply does not exist in markets like Bangladesh, where demand responds almost immediately to changes in the Saudi Aramco Contract Price.

COP 31 and the WLGA Platform: Advocacy as Commercial Strategy

Turkey's Dual Hosting Role

Turkey's hosting of both COP 31 and the World Liquid Gas Association's Liquid Gas Week in the same year creates an unusually concentrated platform for the LPG industry to engage with climate policy decision-makers. The WLGA has already secured formal recognition of LPG as a clean cooking fuel in the G20 Leaders' Declaration, a milestone that strengthens the regulatory and investment framework supporting LPG-based clean cooking programmes globally.

IEA Executive Director Fatih Birol is confirmed as the keynote speaker at the WLGA event, signalling meaningful institutional alignment between the IEA's clean cooking agenda and the LPG industry's expansion priorities. Aygaz's chief executive serves as vice-president of the WLGA, embedding the company directly within this advocacy architecture.

The Turkish government has expressed interest in supporting LPG deployment in Africa and Bangladesh, creating potential alignment between sovereign diplomatic relationships and commercial expansion objectives. Whether this support translates into concrete bilateral energy cooperation agreements remains to be seen, but the strategic positioning is deliberate. In addition, Australia's own energy export challenges offer a comparative lens through which to understand how export-dependent energy economies manage similar structural pressures.

The Road to 5 Million Tonnes: Scenario Outlook

What Needs to Go Right

Aygaz's stated target of doubling trading volumes to 5 million tonnes per year over the next decade is ambitious but structured around identifiable catalysts:

- US supply growth drives Mont Belvieu prices lower through 2028, improving LPG adoption economics across all target markets.

- Three new VLGCs enter service, capturing shipping arbitrage and reducing per-tonne logistics costs on long-haul routes.

- Bangladesh terminal expansions are completed on schedule, supporting volume growth toward the five million tonne target.

- Africa and Southeast Asia market entries are executed through joint venture structures at disciplined valuations, replicating the Bangladesh model.

- PAYG technology adoption unlocks the next tier of price-sensitive household demand in sub-Saharan Africa and South Asia.

The Risks That Could Delay the Trajectory

No strategic scenario is complete without accounting for the forces that could slow it. Key risk factors include:

- Prolonged VLGC rate spikes driven by sustained Hormuz or Black Sea disruptions compressing trade economics.

- Acquisition valuations in target African and Southeast Asian markets remaining elevated, forcing a patient hold on geographic expansion.

- Demand destruction in Bangladesh if Saudi Aramco CP remains elevated for extended periods, constraining volume growth.

- A slower-than-expected conversion rate for Turkey's two million eligible gasoline vehicles, limiting domestic demand upside.

The discipline Aygaz has demonstrated in procurement risk management, the structural moat created by its Chittagong terminal, and the capital commitment represented by its VLGC order collectively suggest a company building for a decade-long opportunity, not a single-cycle trade. For the broader LPG industry, the trajectory of Aygaz US LPG and clean cooking strategy offers a detailed case study in how to build integrated infrastructure positions at the precise moment when global supply growth and emerging market demand are converging.

This article contains forward-looking statements and scenario projections based on publicly available information and industry analysis. Actual outcomes may differ materially from those described. This article does not constitute financial or investment advice.

Want to Capitalise on the Commodities and Energy Infrastructure Trends Shaping Global Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex commodity data into actionable investment insights across energy, resources, and beyond. Explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.