July 15, 2026

The Architecture of Maritime Pressure: Understanding Iran's Two-Chokepoint Strategy

Global energy markets have long understood that a handful of narrow maritime corridors function as the circulatory system of the world economy. When those corridors face genuine disruption risk, the consequences ripple outward with extraordinary speed, touching fuel prices, refining margins, shipping insurance, and the broader calculus of energy security policy across dozens of nations simultaneously. The current situation in the Middle East has moved this theoretical vulnerability into active market territory, as Iran threatens Bab el-Mandeb oil chokepoint access in a strategic escalation that goes beyond anything the global energy system has faced before.

What makes the current moment structurally different from previous periods of Gulf tension is not simply the threat to the Strait of Hormuz, a corridor that markets have priced political risk around for decades. It is the simultaneous activation of a second pressure point, one that directly undermines the primary contingency architecture that oil exporters and importers had developed precisely to manage Hormuz disruptions.

When big ASX news breaks, our subscribers know first

Why the Bab el-Mandeb Strait Cannot Be Replaced

Situated between Yemen's northwestern coastline and the Horn of Africa, the Bab el-Mandeb is a corridor approximately 29 kilometres wide at its narrowest navigable point. Under normal operating conditions, roughly 10% of global oil and natural gas transits this passage, making it one of the highest-density energy corridors on the planet. Unlike the Cape of Good Hope, which functions as a theoretical alternative, the Bab el-Mandeb is not merely a convenient shortcut. For most regional energy exporters and importers operating on tight procurement timelines, rerouting around southern Africa adds two to three weeks of transit time and substantially elevates per-unit delivery costs.

The distinction between the Bab el-Mandeb and the Strait of Hormuz is worth examining carefully, because both operate on similar strategic logic despite their geographic separation. Hormuz controls the exit point from the Persian Gulf, through which the bulk of Saudi, UAE, Iraqi, Kuwaiti, and Iranian crude must pass. Bab el-Mandeb, by contrast, governs access to and from the Red Sea, which is the corridor through which Saudi Arabia's Red Sea coast export terminal at Yanbu operates. This creates a critical vulnerability: when Hormuz risk forces Saudi Arabia to redirect crude exports toward Yanbu, the Bab el-Mandeb threat directly intercepts that contingency route.

The circular nature of this vulnerability deserves emphasis. Hormuz disruption drives Saudi exports toward Red Sea routing. A coordinated Bab el-Mandeb threat then places that Red Sea routing at risk. The result is that no viable maritime export corridor remains fully secure for Gulf crude.

Iran's Dual Chokepoint Doctrine: How It Works in Practice

Iran's Islamic Revolution Guards Corps issued a public statement carried by Iran's IRNA state news agency indicating that regional energy exports function as a collective resource, available to all or denied to all. This framing represents a significant escalation in the rhetorical architecture of Iranian maritime pressure, moving the conversation from Hormuz-specific threats toward a broader doctrine of coordinated corridor disruption. For further context on the dual chokepoint risk, analyst commentary has described this as an unprecedented strategic posture.

The operational mechanism for any Bab el-Mandeb interdiction does not rely on direct Iranian naval action. Instead, Houthi forces controlling Yemen's northwestern Red Sea coastline serve as the proximate capability. This is not a theoretical arrangement. The Houthis demonstrated during the 2023-2024 campaign that they possess the technical means to create genuine shipping disruption, including:

- Anti-ship ballistic and cruise missile systems with demonstrated range coverage over Red Sea shipping lanes

- Drone swarm platforms capable of coordinating multi-vector attacks on commercial vessels

- Naval mining capability that creates persistent area-denial risk even without active engagement

- Sophisticated maritime surveillance capacity developed through years of operational experience

Risk assessments for vessels with U.S. or Israeli commercial interests in the Red Sea corridor are currently rated at elevated levels, though as of mid-July 2026, no confirmed interdiction operations had been executed under the new escalation cycle. The threat remains in the strategic posturing phase, but the capability gap between posturing and execution is narrower than it has ever been.

Three Scenarios: Mapping the Risk Spectrum

Constructing a rigorous scenario framework requires separating the probability of escalation from its consequence severity. The following three pathways represent the range of outcomes that energy market participants are currently pricing against.

| Scenario | Brent Price Range | Global Oil at Risk | Primary Trigger |

|---|---|---|---|

| Contained Pressure | $85-$90/bbl | ~10% | Intermittent harassment, no blockade |

| Partial Interdiction | $110-$130/bbl | ~15-18% | Targeted tanker strikes, Yanbu disruption |

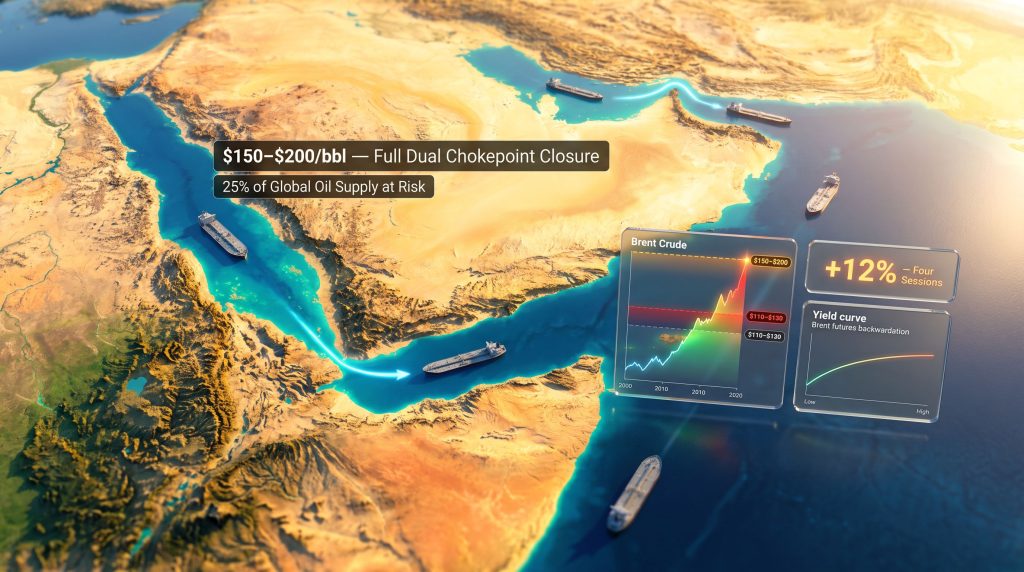

| Full Dual Closure | $150-$200/bbl | ~25% | Complete Hormuz and Bab el-Mandeb blockade |

Scenario One: Contained Pressure

The base case involves Houthi forces conducting periodic harassment operations sufficient to spike war risk insurance premiums without establishing a formal blockade. Under this scenario, commercial operators voluntarily reroute via the Cape of Good Hope to avoid elevated risk zones, creating de facto supply chain lengthening without physical interdiction. Brent sustains above $85-$90 per barrel, driven by insurance cost pass-through and procurement timeline disruption rather than hard supply reduction.

Scenario Two: Partial Interdiction

An elevated risk scenario involves selective targeting of vessel categories tied to U.S. or allied commercial interests. This approach, historically more operationally feasible than a full blockade, places Saudi Yanbu export volumes under direct pressure at precisely the moment those volumes are absorbing Hormuz-displaced export flows. Analyst projections under this scenario point toward a $110-$130 per barrel range. Furthermore, Asian LNG supply pressures cascade into procurement markets as importers scramble for alternative supply sources.

Scenario Three: Full Dual Chokepoint Closure

The tail risk scenario involves effective simultaneous closure of both Hormuz and Bab el-Mandeb. Under these conditions, an estimated 25% of global oil supply and approximately 30% of global container shipping would face simultaneous disruption. Price trajectory modelling under sustained closure conditions points toward a $150-$200 per barrel range, a level that would constitute a supply shock with no direct historical precedent in terms of geographic scope.

IEA member Strategic Petroleum Reserve coordination would represent the primary emergency response mechanism, though SPR volumes are finite and release timelines create a lag between decision and market impact. According to Al Jazeera's coverage of the Bab al-Mandeb closure threat, the implications for global trade under this scenario would be severe and wide-ranging.

A simultaneous closure of both the Strait of Hormuz and the Bab el-Mandeb would expose an estimated $10 billion per day in global trade to disruption, according to analyst assessments of combined throughput values.

How Markets Are Pricing the Risk Right Now

The four-session consecutive rally that carried Brent above $85 per barrel and WTI above $80 represents a cumulative gain of approximately 12% from pre-escalation levels. This price action alone is informative, but the structural signal embedded in futures market positioning tells a more complete story. Indeed, WTI and Brent futures have become a focal point for traders assessing the full scope of corridor disruption risk.

Brent futures have flipped into backwardation, meaning near-term contracts are trading at a premium to longer-dated contracts. This inversion is a critical market credibility signal. Contango, the more typical market structure when oversupply is anticipated, prices future delivery at a premium to account for storage costs. Backwardation reverses this logic, indicating that physical markets are pricing immediate supply tightness as the dominant concern. When backwardation emerges following a geopolitical threat rather than a confirmed physical supply disruption, it signals that professional market participants are assigning material probability to near-term supply reduction, not merely theoretical risk.

Downstream markets are amplifying this crude signal. U.S. gasoline prices have risen for the first time since May, with analyst projections pointing toward $4 per gallon within days. Refining margins have simultaneously reached record highs, reflecting tightening physical crude availability and the processing economics that flow from constrained feedstock supply.

Asian importers are repositioning in real time. China has reduced Saudi crude orders as Hormuz risk premiums reshape procurement economics, with Chinese crude oil imports falling toward decade lows as established Gulf trade flows face disruption. In response, Asian buyers have begun pivoting toward U.S. supply sources as a geographic diversification measure, a shift that realigns long-established procurement patterns under supply chain pressure. Pakistan's emergency LNG procurement represents a particularly acute case study in how smaller importers with limited procurement flexibility face disproportionate vulnerability during corridor disruption events.

Historical Precedent: Why This Time Is Different

Placing the current situation within a historical framework reveals both the precedents that apply and the structural differences that make this escalation cycle unique.

| Event | Chokepoint | Oil Price Impact | Duration | Resolution |

|---|---|---|---|---|

| 1973 Arab Oil Embargo | Multiple corridors | +400% over 12 months | ~6 months | Political negotiation |

| 1980-1988 Tanker War | Strait of Hormuz | +15-25% volatility | 8 years | End of Iran-Iraq War |

| 2019 Abqaiq-Khurais Attacks | Saudi infrastructure | +15% single-day spike | Days | Rapid production restoration |

| 2023-2024 Houthi Campaign | Bab el-Mandeb | +8-12% shipping cost surge | ~14 months | Ongoing U.S. naval operations |

| 2026 Dual Chokepoint Crisis | Hormuz and Bab el-Mandeb | +12% across four sessions | Active | Unresolved |

Three factors distinguish the 2026 situation from all prior precedents. First, this marks the first occasion on which both Hormuz and Bab el-Mandeb have been simultaneously threatened at an operational rather than rhetorical level. Second, the absence of a functioning U.S.-Iran ceasefire removes the primary diplomatic de-escalation mechanism that resolved previous tension cycles. Third, OPEC demand forecast revisions add a demand-side complexity absent from previous supply shock episodes, creating an unusual situation where supply risk and demand uncertainty are simultaneously elevated.

The next major ASX story will hit our subscribers first

The Compounding Exposure of Energy-Dependent Economies

The downstream consequences of sustained chokepoint disruption are not distributed evenly across the global economy. Several regions face compounding exposure that extends well beyond crude oil price elevation.

Europe confronts a particularly layered vulnerability. European gas price trends have already responded to Hormuz escalation through the LNG supply chain connection, as Middle Eastern LNG exports form a meaningful portion of European import flows. Compounding this, EU Russian LNG imports have reached record highs ahead of the scheduled 2027 ban, creating a situation where European buyers are simultaneously dependent on a supply source they are committed to eliminating while their alternative supply corridors face disruption risk.

India faces direct cost impact from elevated chokepoint risk given its heavy reliance on Gulf crude imports. The Indian government's strategic petroleum reserve expansion through new ONGC storage capacity represents a forward-looking buffer strategy, though storage volumes cannot substitute for sustained import disruption over an extended period. India's relationship with Iran adds a further complication, as sanctions pressure intersects with supply diversification imperatives in ways that limit procurement flexibility.

Gulf exporters themselves face a structural irony. The nations most dependent on maritime corridor integrity for revenue generation, principally Saudi Arabia, are simultaneously the nations whose contingency export infrastructure sits most directly in the path of the Bab el-Mandeb threat. Dubai has reportedly begun planning for next-generation Hormuz crisis scenarios, recognising that the current disruption cycle may not be the last.

Factors That Could Limit Sustained Price Escalation

Despite the severity of the risk architecture, however, several supply-side factors are working against the kind of sustained price spike that the most extreme scenarios would otherwise generate.

- UAE oil output has reached all-time highs, providing incremental non-Hormuz supply to global markets

- Nigeria's oil production has hit a six-year peak, adding non-Gulf volume to the global supply picture

- OPEC's downward revision to demand forecasts creates a supply buffer narrative that caps the upside of sustained price elevation

- IEA member SPR release coordination capacity functions as a market price ceiling mechanism, though its effectiveness decays over time with sustained release volumes

The pipeline bypass calculus also deserves attention. U.S. backing for an Iraq-Syria oil pipeline has emerged as a medium-term infrastructure response to Hormuz constraints. However, the Saudi East-West pipeline, which provides partial Red Sea routing capacity, cannot absorb full Gulf export volumes. Physical infrastructure alternatives require months to years to scale meaningfully, leaving near-term supply fundamentally dependent on maritime corridor security in any scenario that unfolds over weeks rather than years. Consequently, the broader oil geopolitics analysis continues to evolve rapidly as the situation on the ground develops.

Frequently Asked Questions: Iran's Bab el-Mandeb Threat

What is the Bab el-Mandeb Strait and why does it matter for oil markets?

The Bab el-Mandeb is a narrow maritime corridor connecting the Red Sea to the Gulf of Aden, positioned between Yemen and the Horn of Africa. Roughly 10% of global oil and natural gas transits this passage under normal conditions. Disruption forces tankers onto significantly longer Cape of Good Hope routes, adding weeks of transit time and substantial cost to global energy supply chains.

How would Iran actually activate a Bab el-Mandeb disruption?

Iran does not directly control the strait but exercises operational influence through Houthi forces holding Yemen's northwestern Red Sea coastline. The Houthis possess documented anti-ship missile systems, armed drone platforms, and naval mining capability sufficient to create credible interdiction risk against commercial shipping, as demonstrated during the 2023-2024 campaign.

What oil price levels could result from a dual chokepoint closure?

Scenario modelling suggests a full simultaneous closure of both the Strait of Hormuz and the Bab el-Mandeb could drive Brent crude into the $150-$200 per barrel range, representing a severe supply shock with no comparable historical precedent in terms of geographic scope. Iran threatens Bab el-Mandeb oil chokepoint access precisely because the consequences at this level would be globally destabilising.

Why did Brent futures flip to backwardation?

Backwardation, where near-term futures prices exceed longer-dated contracts, signals that physical markets are pricing immediate supply tightness as the dominant concern. This structural shift indicates that professional market participants are assigning material probability to near-term supply disruption rather than treating the threat as a long-horizon tail risk.

What alternatives exist if both straits are effectively blocked?

Options are limited and slow to scale. The Saudi East-West pipeline provides partial capacity relief but cannot absorb full Gulf export volumes. The U.S.-backed Iraq-Syria pipeline remains in planning stages. Most Gulf exporters would face months-long rerouting via the Cape of Good Hope, adding significant cost and transit time to global supply chains with no rapid physical solution available.

Disclaimer: This article contains forward-looking scenario analysis and market projections based on publicly available information as of mid-July 2026. Oil price scenarios represent analytical modelling outputs and not investment advice. Energy markets involve significant uncertainty, and actual outcomes may differ materially from any scenario described herein. Readers should conduct their own independent research before making any investment or commercial decisions based on information contained in this article.

Want to Track the ASX Mining Stocks Most Exposed to Energy Market Shocks?

When geopolitical disruptions reshape commodity markets at this speed, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, ensuring subscribers can identify actionable opportunities before the broader market reacts — explore historic discovery returns on the Discovery Alert discoveries page and begin a 14-day free trial to position ahead of the next major market move.