July 15, 2026

The Economics of Stranded Gas: Why Pipeline Deals Are Harder Than They Look

Global energy markets operate on a fundamental tension that politicians rarely acknowledge openly: the gap between geopolitical narrative and commercial reality. When two nations declare a strategic partnership, the assumption in many policy circles is that energy flows will follow. But pipeline gas is not diplomacy. It is infrastructure finance, contract law, and commodity pricing compressed into a single instrument, and it cannot function without all three components aligned.

Nowhere is this more apparent than in the prolonged impasse surrounding the Power of Siberia 2 China Russia gas price dispute, a proposed 2,500-kilometre artery that would carry natural gas from Russia's western Siberian Yamal fields, through Mongolia, and into China. The project has been discussed for years, elevated to strategic priority status by Moscow, and met with studied patience by Beijing. What sits between the two governments is not political hostility but something more fundamental: a pricing gap that neither side has yet found a formula to bridge.

When big ASX news breaks, our subscribers know first

The Strategic Logic Behind Power of Siberia 2

Russia's Post-European Gas Crisis and the Search for a New Anchor Market

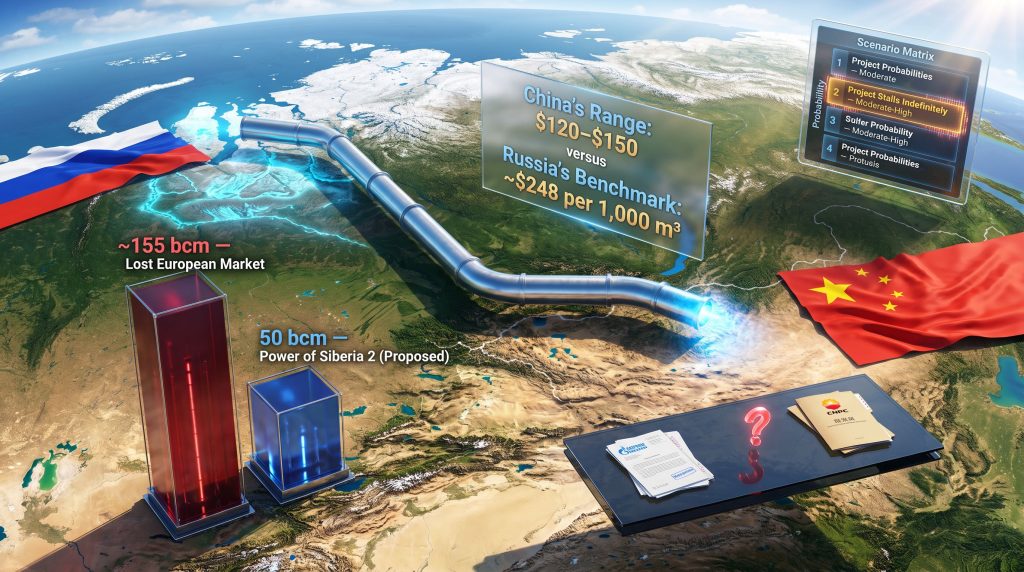

Before Russia's military intervention in Ukraine reshaped the European energy order, Gazprom exported approximately 155 billion cubic meters (bcm) of natural gas annually to the European Union. That volume underpinned a significant share of Russia's federal budget and represented decades of infrastructure investment across thousands of kilometres of pipeline.

The collapse of those export flows did not happen overnight, but by the time Ukrainian transit agreements expired and European buyers accelerated their diversification programmes, the structural damage to Russia's gas export model was severe. The Kremlin's response has been to reorient toward Asia, with China as the only realistic anchor market capable of absorbing volumes at scale. Furthermore, the US-China trade war impacts have added additional complexity to how Beijing approaches long-term energy supply agreements.

The problem is mathematical. Power of Siberia 2, at its proposed full capacity, would transport 50 bcm per year, which represents roughly 32% of Russia's pre-war EU export volumes. Even if every cubic metre of contracted gas flowed without interruption, Russia could not replace its lost European revenue through this single pipeline. The project is critical to Moscow not because it solves the problem but because without it, Russia's western Siberian gas reserves have no export outlet at all.

How Power of Siberia 2 Differs From Its Predecessor

The existing Power of Siberia 1, which became operational in 2019, draws on eastern Siberian gas fields and connects to China's northeast. It operates on a separate gas supply system and was always conceived as a distinct commercial and geographic proposition. Power of Siberia 2 is fundamentally different in one critical respect: it would be the first pipeline to link the Yamalo-Nenets gas fields of western Siberia directly to Chinese buyers.

This matters because Yamal gas is the same resource base that historically fed European markets through pipelines crossing Ukraine and the Baltic Sea. Gazprom built its entire European export model around Yamal production. With those western routes now functionally closed, Power of Siberia 2 represents the only viable large-scale pathway for monetising that reserve base going forward.

| Pipeline | Annual Capacity | Source Region | Current Status |

|---|---|---|---|

| Nord Stream 1 | 55 bcm | Western Siberia (Yamal) | Destroyed (2022) |

| Power of Siberia 1 | ~38 bcm (design) | Eastern Siberia | Operational |

| Power of Siberia 2 | 50 bcm (proposed) | Western Siberia (Yamal) | Unbuilt, negotiations stalled |

What Are the Core Terms Being Disputed?

The Price Gap: A Chasm Measured in Hundreds of Dollars

The Power of Siberia 2 China Russia gas price dispute is not a minor commercial disagreement. According to reporting by the Wall Street Journal, China has sought pricing at or near Russia's heavily subsidised domestic rate, which sits at approximately $50 per 1,000 cubic meters. Russia's domestic gas prices are kept artificially low as a social and industrial policy instrument, and they bear no relationship to export economics.

Russia, for its part, has pursued a market-referenced pricing methodology broadly consistent with the long-term contract structures it used with European buyers. The existing Power of Siberia 1 benchmark provides a rough reference point at approximately $248 per 1,000 cubic meters, though this figure has fluctuated with oil-linked pricing formulas.

| Negotiating Position | Price per 1,000 m³ | Basis |

|---|---|---|

| China's opening demand | ~$50 | Russian domestic subsidised rate |

| China's negotiating range | $120–$150 | Near-domestic pricing |

| Russia's breakeven at Chinese border | ~$125 | Infrastructure cost recovery threshold |

| Power of Siberia 1 contract price | ~$248 | Existing long-term export benchmark |

| Asian LNG spot average | ~$370 | China's alternative import reference |

The most revealing figure in this table is Russia's estimated breakeven threshold at the Chinese border: approximately $125 per 1,000 cubic meters. This is the floor below which Gazprom cannot recover its infrastructure investment over any commercially viable timeframe. China's current negotiating range of $120 to $150 sits uncomfortably close to or below this threshold, leaving virtually no margin for Russia even in a best-case pricing scenario.

Why China Is Demanding Domestic-Rate Pricing

China's insistence on pricing at or near Russian domestic rates reflects a negotiating posture built on genuine optionality rather than bluff. Beijing can expand LNG import capacity, accelerate domestic unconventional gas production from Sichuan and Tarim basin reserves, or simply extend existing import contracts with Central Asian suppliers through the Central Asia-China pipeline network. None of these alternatives is as cheap as deeply discounted pipeline gas from Russia, but all of them are commercially viable at current market prices. Understanding how tariffs work in the broader context of Sino-Russian trade also illuminates why Beijing is reluctant to lock in pricing that undermines its overall negotiating leverage.

This gives China a patience advantage that Russia simply does not have. Moscow's western Siberian reserves are large but geologically static. Gas that cannot be exported generates no revenue and incurs ongoing maintenance costs across ageing field infrastructure.

The Take-or-Pay Clause: A Technical Dispute With Multi-Billion Dollar Consequences

*A take-or-pay clause in a gas supply contract obligates the buyer to either physically accept a minimum contracted volume or pay a financial penalty equivalent to the value of that volume. Russia has historically required buyers to commit to around 80% of contracted annual volumes under such clauses. Reports suggest China has pushed to reduce this threshold to approximately 50%, which would substantially undermine the financial foundation of the entire project.*

This technical detail matters enormously for project financing. Pipeline infrastructure of this scale requires lenders and investors to model predictable cash flows over multi-decade time horizons. A take-or-pay threshold of 50% introduces volume risk that makes debt financing significantly more expensive and equity investment less attractive. Russia's insistence on a higher threshold is not merely commercial stubbornness. It reflects the basic economics of building a pipeline that costs tens of billions of dollars through challenging terrain before a single cubic metre of gas has been sold.

Who Holds the Leverage?

Russia's Urgency: Stranded Reserves and Declining Export Revenue

The negotiating dynamic in the Power of Siberia 2 discussions has inverted the historical template of Russian gas diplomacy. For decades, Russia's leverage with European buyers rested on infrastructure dependency. European countries had built their industrial and residential heating systems around the assumption of reliable Russian pipeline gas, and diversifying away from that dependency required years and significant capital expenditure.

China faces no equivalent dependency on Russian gas. Its existing import infrastructure is diversified across LNG terminals on the eastern coast, Central Asian pipeline connections in the northwest, and growing domestic production. Russia arrives at the negotiating table not as an indispensable supplier but as one among several competing options. In addition, the ongoing sanctions on Russian energy have further eroded Gazprom's ability to attract Western financing or technology for new pipeline construction.

China's Patience: Why Beijing Is in No Rush

The asymmetry extends beyond infrastructure to time preference. Russia needs to monetise its Yamal reserves to sustain Gazprom's balance sheet and federal budget contributions. Every year that Power of Siberia 2 remains unbuilt is a year in which those reserves generate no export revenue. China, operating with a long-term planning horizon typical of its state-directed industrial policy, has no equivalent fiscal urgency.

Beijing has also observed how Russia's desperation to preserve European export relationships was historically exploited by Moscow itself through supply interruptions and pricing pressure. China is consequently unlikely to allow itself to become structurally dependent on a single supplier from whom leverage extraction is a documented historical practice.

LNG as China's Silent Weapon

Asian LNG spot prices have averaged approximately $370 per 1,000 cubic meters in recent periods, which establishes the ceiling above which Russian pipeline gas ceases to be economically rational for Chinese buyers. The global LNG supply outlook for 2025 and beyond suggests that new export capacity from the United States, Qatar, and Australia will continue to provide Beijing with credible alternatives. The spread between this ceiling and Russia's breakeven threshold gives China a negotiating corridor of roughly $245 per 1,000 cubic meters within which any deal must eventually be structured.

Negotiation Timeline and Current Status

What Progress Has Actually Been Made?

The progression of Power of Siberia 2 negotiations has been characterised by periodic announcements of procedural progress combined with persistent silence on the commercial terms that actually determine whether the project can proceed.

- September 2025: A legally binding memorandum was signed between the relevant parties covering the pipeline's proposed route through Mongolia and its general scale parameters. This represented a genuine technical milestone but explicitly excluded pricing terms.

- May 2026: Russian officials characterised discussions as having reached broad agreement on primary parameters, though no pricing framework or take-or-pay structure was confirmed.

- July 2026: Reporting indicates that Chinese representatives communicated to Russian counterparts prior to a high-level meeting in Beijing that Power of Siberia 2 should not be placed on the formal agenda, given the continued distance between the two sides on commercial terms.

Why Official Statements Must Be Read Carefully

Both governments have a strategic interest in avoiding public declarations that negotiations have failed. Russia cannot afford to signal that its most important gas export project has no viable buyer. China benefits from keeping Russia at the table while continuing to press for more favourable terms.

The Kremlin has framed ongoing discussions as operating at the corporate level between Gazprom and the China National Petroleum Corporation (CNPC), a framing that allows Moscow to maintain the appearance of active progress without committing to a timeline. Beijing's public posture has remained non-committal, which serves Chinese interests by preserving optionality without formally closing off a deal that might eventually become attractive. According to analysis from Columbia University's Centre on Global Energy Policy, this dynamic reflects a broader pattern in which China consistently uses its position as a demand anchor to extract structural concessions from suppliers.

Does the Dispute Disprove the "Friendship Price" Narrative?

One of the more consequential insights to emerge from the Power of Siberia 2 China Russia gas price dispute is what it reveals about the structural economics of Russian gas exports. There has been a persistent assumption in some European policy discussions that Russia might offer preferential or politically motivated pricing to strategically aligned partners. However, the evidence from these negotiations suggests otherwise.

Russia's reported pricing approach for Power of Siberia 2 mirrors the methodology used in its long-term European contracts: market-referenced formulas anchored to oil price indices or competing fuel benchmarks. Reuters reporting indicates that Gazprom's target price formula for the China deal is structurally similar to the approach applied in legacy European supply agreements.

This has a specific implication for European energy policy thinking. The assumption that pipeline gas from Russia would automatically be available at deeply discounted rates, whether to China or to a hypothetically reconnected European buyer, is not supported by the actual negotiating behaviour of Gazprom and the Russian government. Infrastructure cost recovery, not geopolitical generosity, appears to drive Russia's minimum acceptable price.

The next major ASX story will hit our subscribers first

What Scenarios Could Break the Deadlock?

| Scenario | Probability Assessment | Key Condition Required |

|---|---|---|

| Phased LNG-linked price formula | Moderate | Russia accepts a market-floor pricing structure |

| Higher take-or-pay for lower base price | Low-Moderate | China accepts meaningful volume commitment risk |

| Third-party financing arrangement | Low | Requires aligned geopolitical and commercial interests |

| Project stalls indefinitely through the decade | Moderate-High | Neither side makes substantive concessions |

Scenario 1: A Phased Price Structure Tied to LNG Benchmarks

One potential resolution involves a formula that sets an initial lower price with escalation mechanisms tied to Asian LNG spot prices. This approach would give China cost certainty in the early years while giving Russia confidence that pricing would converge toward market levels as the pipeline matures. The difficulty is agreeing on the floor, the escalation trigger, and the reference index, all of which involve the same commercial tensions that have blocked agreement to date.

Scenario 2: Volume Commitment in Exchange for Price Concessions

China accepting a higher take-or-pay threshold in exchange for a lower base price would represent a trade of volume risk for price certainty. This is theoretically logical but runs counter to China's established negotiating behaviour, which has consistently sought to minimise long-term volume commitments across its energy import portfolio.

Scenario 3: Third-Party Financing

If a third-party financing structure could reduce Russia's capital costs, the breakeven threshold would fall, potentially creating space for a price that both sides could accept. This scenario requires commercial and political conditions that do not currently appear to be in place.

Scenario 4: Indefinite Stalemate

The scenario that observers should weight most seriously is continued delay. Russia has no alternative buyer for Yamal gas at export scale. China has no urgent need to lock in a long-term Russian supply commitment. Both conditions favour Beijing's preferred strategy of patient negotiation. If Gazprom's financial position continues to deteriorate and the Russian government faces growing pressure to generate export revenue, the balance of leverage may eventually shift enough to produce a deal, but on terms considerably closer to China's current position than Russia's.

Frequently Asked Questions: Power of Siberia 2 China Russia Gas Price Dispute

What is the Power of Siberia 2 pipeline?

Power of Siberia 2 is a proposed natural gas pipeline designed to transport up to 50 bcm of gas per year from Russia's Yamalo-Nenets gas fields in western Siberia through Mongolia to China. It would be the largest new gas pipeline project under active negotiation between the two countries and would represent the first direct connection of Yamal production to Chinese markets.

Why has the deal not been signed?

The primary obstacle is a significant gap in pricing expectations. China has sought pricing close to Russia's domestic gas rate, while Russia requires a market-referenced price to recover the infrastructure investment required to build the pipeline. Additional unresolved issues include the structure of take-or-pay volume commitments, contract duration, and construction financing.

What price is China demanding?

According to Wall Street Journal reporting, China initially sought pricing at approximately $50 per 1,000 cubic meters, equivalent to Russia's heavily subsidised domestic rate. Subsequent negotiating positions have reportedly shifted toward a range of $120 to $150 per 1,000 cubic meters, still substantially below Russia's cost recovery threshold and far below the Power of Siberia 1 benchmark.

Could Power of Siberia 2 replace Russia's lost European gas revenues?

No. At full capacity, Power of Siberia 2 would carry 50 bcm per year, representing approximately 32% of the roughly 155 bcm that Russia exported annually to the EU before 2022. Even a fully operational pipeline at commercially viable prices would leave a substantial and likely permanent gap in Russia's gas export revenues.

What the Stalled Deal Means for Global Gas Markets

Implications for LNG Supply Dynamics

If Power of Siberia 2 is not built, or is significantly delayed, the structural consequence for global LNG markets is a China that remains a large and growing spot and term LNG buyer rather than a locked-in pipeline gas customer. This sustains demand for LNG infrastructure investment globally and supports pricing for Australian, Qatari, and American LNG exporters competing for Asian market share. Consequently, Australia's energy export challenges may, in fact, be partially offset by the sustained demand that a stalled Power of Siberia 2 generates for alternative suppliers.

What Stranded Yamal Reserves Mean for Gazprom's Balance Sheet

Gazprom's financial position has deteriorated materially since 2022. The company recorded a net loss for fiscal year 2023, a dramatic reversal from the profit levels it sustained during the period of high European gas prices. Without a major new export outlet for Yamal production, Gazprom faces an extended period of underutilised reserve capacity, ongoing maintenance costs on dormant infrastructure, and limited ability to attract the international financing that large capital projects typically require.

The Signal for European Energy Policymakers

The Power of Siberia 2 China Russia gas price dispute provides European governments with a data point that is relevant to their own energy security planning. Russia's behaviour in these negotiations suggests that any future re-engagement with Russian pipeline gas, under whatever political circumstances, would be structured around market-referenced pricing rather than discounted rates. The idea that European buyers might access Russian gas at preferential terms because of a change in political alignment finds no support in the actual commercial framework Russia has pursued with China.

Key Data Summary

The following figures capture the essential commercial parameters of the dispute:

- Proposed pipeline annual capacity: 50 bcm

- China's reported price demand: $120 to $150 per 1,000 m³

- Russia's estimated border breakeven: ~$125 per 1,000 m³

- Power of Siberia 1 existing contract benchmark: ~$248 per 1,000 m³

- Asian LNG spot price reference: ~$370 per 1,000 m³

- Russia's pre-war EU gas exports: ~155 bcm per year

- Power of Siberia 2 as a share of lost EU volumes: ~32%

- Pipeline route length through Mongolia: ~2,500 km

- Legally binding route memorandum signed: September 2025

The outcome of this negotiation will define not only Gazprom's commercial future but the structural balance of energy leverage between Russia and China for the next generation. What has become clear from the current impasse is that pipeline gas, regardless of the political relationship surrounding it, ultimately answers to the economics of steel, compression, and capital recovery. Neither friendship nor strategic alignment changes the arithmetic of infrastructure finance.

This article contains forward-looking analysis and scenario assessments that are inherently uncertain. Pricing figures, negotiating positions, and timeline references are drawn from publicly available reporting including the Wall Street Journal and Reuters and are subject to change as negotiations evolve. Nothing in this article constitutes investment or financial advice.

Want to Stay Ahead of the Commodity Shifts Driving Global Energy Markets?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across more than 30 commodities — including those tied to the energy transition reshaping global gas and resource markets. Explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial to position yourself ahead of the next major market move.