May 23, 2026

The Mineralogical Edge That Most Nickel Investors Overlook

Nickel's reputation as a battery-critical metal has made it one of the most discussed commodities in the clean energy transition. Yet the conversation almost always centres on where nickel comes from geographically, rather than what form it takes mineralogically. That distinction, largely invisible to generalist investors, may ultimately determine which projects survive long-term cost and carbon scrutiny, and which ones don't.

The Baptiste nickel project in British Columbia sits at the centre of this mineralogical debate. Hosted within a largely overlooked deposit type known as awaruite, Baptiste presents a genuinely different value proposition to conventional nickel projects. Understanding why requires stepping back from headline production numbers and examining what actually happens beneath the surface, and why that matters enormously for economics, emissions, and supply chain positioning.

When big ASX news breaks, our subscribers know first

What Awaruite Actually Is, and Why Most Analysts Underestimate It

Most of the world's nickel comes from two deposit types: sulfide and laterite. Both require energy-intensive processing pathways. Sulfide ores must be smelted and refined, generating substantial sulfur dioxide emissions and requiring high-temperature furnace operations. Laterites, which now dominate global nickel supply, typically require either high-pressure acid leaching or rotary kiln electric furnace processing, both of which are capital-heavy and carbon-intensive.

Awaruite is chemically distinct from both. It is a naturally occurring nickel-iron alloy with the formula Ni₃Fe, and crucially, it contains no sulfur. This is not a minor technical footnote. The complete absence of sulfur means the entire smelting stage — one of the most expensive and emissions-intensive components of conventional nickel metallurgy — is eliminated from the processing flowsheet. Understanding magmatic nickel deposits helps contextualise just how structurally different awaruite mineralisation truly is.

Instead, awaruite ore can be concentrated through magnetic separation, a relatively low-energy process that exploits the mineral's natural magnetic properties. The resulting concentrate is a sulfur-free nickel-iron product that is increasingly compatible with emerging direct-to-precursor processing routes being developed by battery cathode manufacturers seeking to bypass traditional refining steps entirely.

The structural absence of sulfur in awaruite deposits isn't simply an environmental benefit. It represents a fundamental redesign of the processing economics at the mine level, removing cost centres that most nickel producers cannot engineer away.

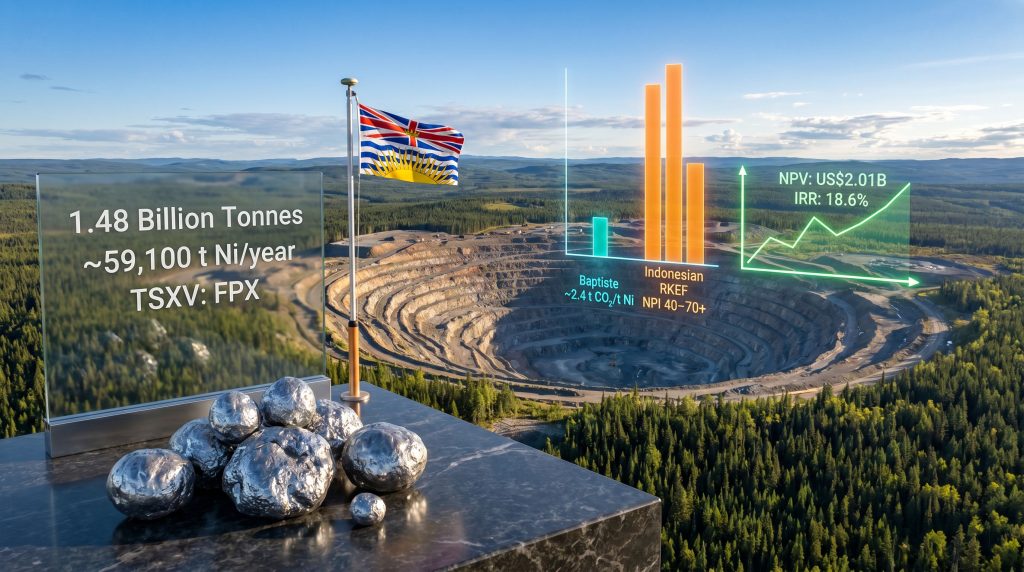

This processing simplicity translates directly into Baptiste's projected carbon profile. With access to BC Hydro's low-carbon hydroelectric grid powering magnetic separation rather than coal-fired furnaces driving smelters, Baptiste's estimated Scope 1 and Scope 2 carbon intensity sits at approximately 2.4 tonnes of CO₂ per tonne of nickel produced. To contextualise that figure, Indonesian nickel supply from pig iron operations powered by coal generates an estimated 40 to 70-plus tonnes of CO₂ per tonne of nickel, and even conventional sulfide operations average roughly 10 to 20 tonnes.

| Nickel Production Method | Approximate CO₂ Intensity (t CO₂/t Ni) |

|---|---|

| Baptiste awaruite, hydro-powered | ~2.4 |

| Global nickel sulfide average | ~10–20 |

| Global laterite average | ~20–40 |

| Indonesian RKEF NPI, coal-powered | 40–70+ |

Note: Competitor figures represent indicative industry estimates used for contextual comparison only. Individual operations will vary.

Baptiste's Geological Setting and the Decar Nickel District

The Baptiste nickel project in British Columbia is located approximately 90 kilometres northwest of Fort St. James in the Nechako region of central British Columbia. It is hosted within an ultramafic and ophiolite complex, a rock suite formed from ancient oceanic mantle material that was tectonically emplaced onto the continental crust.

Ophiolite complexes are the geological environments most commonly associated with awaruite mineralisation globally, because the high-temperature, low-oxygen conditions within these rocks favour the formation of native nickel-iron alloys rather than sulfide minerals. The Decar nickel district, within which Baptiste sits, represents one of the largest known concentrations of awaruite mineralisation anywhere in the world.

FPX Nickel Corp (TSXV: FPX), a Vancouver-based junior mining company, has been advancing Baptiste since 2010, committing approximately US$55 million to exploration and development activities across that period. The scale of the defined ore body reflects that sustained investment.

Scale, Reserves, and the Production Architecture

Baptiste's resource base is genuinely large by any measure. Proven and probable mineral reserves stand at 1.48 billion tonnes, graded at 0.13% nickel as recovered through Davis Tube Magnetic separation, the standard metallurgical test used to characterise awaruite recovery. At that scale, the project supports a projected mine life of 28 to 29 years using open-pit mining methods.

The production plan is structured in two phases:

- Phase One (Years 1 to 9): Ore throughput of 108,000 tonnes per day

- Phase Two (Years 9 onward): Expanded throughput of 162,000 tonnes per day

- Average annual nickel production across the mine life: approximately 59,100 tonnes

That annualised production figure would, if realised, represent a meaningful contribution to Canadian and Western nickel supply, particularly at a time when the geopolitical reliability of Indonesian and Chinese-controlled nickel processing chains is under intensifying scrutiny from Western manufacturers and policymakers.

The Economics: What the Numbers Actually Represent

Baptiste's prefeasibility economics present a project with compelling fundamentals, though investors should treat all forward-looking projections with appropriate caution given the long pathway to production and the sensitivity of nickel project economics to price assumptions.

| Economic Indicator | Projected Value |

|---|---|

| After-Tax Net Present Value (NPV) | US$2.01 billion |

| Internal Rate of Return (IRR) | 18.6% |

| Base Case Nickel Price Assumption | US$8.75/lb |

| Initial Capital Cost (CAPEX) | US$2.18 billion |

| Projected GDP Contribution over Mine Life | CAD$45 billion |

| Direct Employment (Annual) | ~1,000 jobs |

Several dimensions of these figures deserve closer examination. An initial CAPEX of US$2.18 billion is a substantial financing challenge for a junior mining company. At this scale, the project almost certainly requires strategic partners, offtake agreements with battery supply chain participants, or co-investment structures to reach a construction decision. This is a material risk that investors must weigh against the project's long-term economic potential.

The NPV of US$2.01 billion is calculated at a nickel price of US$8.75 per pound. Nickel markets have experienced significant volatility in recent years, partly driven by the rapid expansion of Indonesian laterite processing capacity. Sustained nickel prices below the base case assumption would materially alter the project's economics, and investors should model multiple price scenarios rather than relying on a single base case.

The projected CAD$45 billion incremental GDP contribution over the 29-year mine life would represent one of the largest economic footprints of any junior-operated resource project in Canadian history, with approximately 1,000 direct jobs annually anchoring employment across the Nechako region. Indirect and supply chain employment multipliers would extend those benefits considerably further.

British Columbia's Designation and What It Signals

In April 2026, the British Columbia government formally designated the Baptiste nickel project in British Columbia as a major priority project under the province's Look West economic strategy. What makes this designation particularly notable is the company behind it: Baptiste is the only critical minerals project operated by a junior mining company to appear on B.C.'s major project priority list.

Provincial priority designations in British Columbia have historically been dominated by major and mid-tier mining companies with established balance sheets and long development track records. Baptiste's inclusion signals a degree of institutional confidence in the project's technical credibility and economic significance that is uncommon for junior-stage assets.

The Look West strategy is designed to streamline permitting processes, reduce regulatory duplication between provincial and federal agencies, and eliminate structural barriers that have historically extended mine development timelines in British Columbia. It does not guarantee approvals or predetermined outcomes from regulatory processes, but it does create a coordinating framework intended to reduce the administrative fragmentation that has extended timelines on comparable projects.

The next major ASX story will hit our subscribers first

The Critical Minerals Office: A First-Mover Advantage

Distinct from the Look West designation, Baptiste holds another significant institutional distinction. In 2024, it became the first project admitted to British Columbia's Critical Minerals Office concierge service, a newly established body created to provide centralised, coordinated government engagement for strategically important critical mineral projects.

The CMO operates as a single-window interface between project proponents and the multiple regulatory agencies involved in mine development approvals. In practice, this means FPX Nickel receives coordinated guidance rather than navigating fragmented, and sometimes conflicting, requirements from separate provincial and federal departments simultaneously.

The significance of being the inaugural CMO project extends beyond administrative convenience. It positions Baptiste as a test case for how B.C. intends to manage its most strategically important critical mineral assets through the EA process, which creates both visibility and a degree of institutional momentum that later-admitted projects will not have experienced from the beginning.

In April 2026, both provincial and federal authorities jointly published the Joint Summary of Issues and Engagement, a formal procedural document that identifies the key environmental, social, and technical issues that Baptiste's full Environmental Impact Statement must address. Joint publication by both levels of government signals active intergovernmental coordination and reduces the risk of conflicting regulatory demands emerging later in the process.

Environmental Assessment Timeline: Where Baptiste Stands

Understanding where Baptiste currently sits in the regulatory pipeline is essential for accurately assessing timelines and investment risk. Furthermore, the definitive feasibility study expected in 2028 will be a critical milestone that investors and regulators alike will scrutinise closely.

| Milestone | Status or Date |

|---|---|

| CMO Concierge Service Admission | 2024 |

| Public Comment Period Closed | March 9, 2026 |

| Joint Summary of Issues and Engagement Published | April 2026 |

| Detailed Project Description Submission (Planned) | Mid-2027 |

| Full Feasibility Study (Expected) | 2028 |

The gap between the current milestone and planned first production is substantial. With a detailed project description not planned until mid-2027 and a full feasibility study not expected until 2028, construction commencement remains several years away. This is not an unusual timeline for a project of Baptiste's scale and complexity, but it is a material consideration for investors evaluating near-term catalysts.

First Nations Engagement: A Structural Prerequisite, Not a Checkbox

British Columbia's regulatory environment places considerable legal weight on meaningful consultation and accommodation with First Nations whose traditional territories overlap with proposed resource developments. For a project located in the Nechako region, this means sustained engagement with the relevant communities is not simply good practice but a legal and regulatory prerequisite for EA approval.

FPX Nickel has publicly committed to deepening its collaborative relationships with relevant First Nations as a core development pillar. The company's position, as articulated by President and CEO Martin Turenne, frames this as an ongoing commitment to developing Baptiste in a way that creates substantial and sustainable benefits while protecting the environment for future generations, according to reporting by the Canadian Mining Journal (April 30, 2026).

Projects in British Columbia that proceed without substantive Indigenous support face materially elevated legal and permitting risk, regardless of any provincial priority designation. Baptiste's 29-year mine life also creates an unusually extended window for structured multi-generational economic participation by Indigenous communities, including benefit-sharing agreements, employment targets, and equity participation mechanisms that are increasingly standard in modern Canadian mine development agreements.

The three-pillar governance structure now surrounding Baptiste, combining provincial priority designation, CMO coordination, and First Nations engagement, represents a de-risking combination that is genuinely uncommon for a junior-operated project at this stage of development.

Nickel's Role in the Battery Supply Chain and Why Provenance Is Becoming Critical

Nickel is a core input in the cathode chemistries that power high-energy-density lithium-ion batteries, particularly NMC (nickel-manganese-cobalt) and NCA (nickel-cobalt-aluminium) formulations used in electric vehicles. As part of the broader critical minerals energy transition, a growing tension has emerged between the availability of low-cost Indonesian nickel and the supply chain traceability requirements being embedded into procurement policies across North America and Europe.

Canadian nickel, produced from a stable jurisdiction under stringent environmental oversight, carries provenance attributes that Indonesian NPI cannot easily replicate. Furthermore, nickel's properties and uses in high-energy-density battery chemistries make it uniquely difficult to substitute at scale. Baptiste's combination of large scale, low carbon intensity, and Canadian jurisdiction positions it as a rare convergence of the three attributes most consistently cited by Western battery supply chain buyers as priority criteria.

The awaruite chemistry may also open a fourth advantage. Sulfur-free nickel feedstocks are increasingly being examined as potential inputs for direct-to-battery-precursor processing pathways that bypass conventional refining steps. If those pathways commercialise at scale, awaruite-sourced nickel concentrates could attract a processing premium or access to offtake structures unavailable to conventional sulfide producers.

Key Risks Investors Should Understand

Baptiste's strategic positioning does not eliminate execution risk. Several factors warrant careful monitoring:

- Capital intensity: Securing US$2.18 billion in project financing as a junior company is a significant challenge requiring strategic partnerships or offtake agreements with well-capitalised counterparties

- Nickel price sensitivity: The base case NPV of US$2.01 billion assumes US$8.75 per pound nickel; sustained price weakness below this level would materially reduce project economics

- Timeline execution: The EA process remains multi-year and subject to delays; adverse findings could require project redesign

- Indonesian supply competition: Continued low-cost nickel supply expansion from Indonesia creates persistent downward pressure on benchmark prices

- Financing environment: Commodity market volatility and broader capital market conditions affect lender confidence in long-dated mining projects

This article does not constitute financial advice. All financial projections, NPV figures, IRR estimates, and production forecasts referenced are drawn from FPX Nickel's publicly disclosed prefeasibility study and should not be relied upon as guarantees of future performance. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions.

The Path Ahead: What Has to Happen Before Baptiste Becomes a Mine

The institutional scaffolding now surrounding the Baptiste nickel project in British Columbia is genuinely unusual for a junior-operated asset. However, scaffolding is not a mine. The steps remaining before Baptiste can move to construction are substantial, and each carries execution risk. British Columbia's environmental assessment process for a project of this scale is rigorous, multi-staged, and inherently unpredictable in its timing.

- Successful completion of the full Environmental Assessment process

- Finalisation of First Nations benefit-sharing and partnership agreements

- Submission and regulatory acceptance of the detailed project description, targeted for mid-2027

- Completion of the full feasibility study, expected in 2028

- Securing of project financing and strategic offtake partnerships at a scale commensurate with the US$2.18 billion initial CAPEX

- Receipt of all major construction and operating permits

Each step represents a genuine threshold, not a formality. The history of Canadian mining is full of technically strong projects that stalled at the financing or permitting stage despite compelling economics. What differentiates Baptiste is the combination of mineralogical distinctiveness, documented economic significance, and the institutional framework now assembled around it — including the CMO concierge designation, Look West priority status, and joint federal-provincial EA coordination.

Whether that combination is sufficient to navigate the years ahead will depend on commodity markets, regulatory outcomes, financing conditions, and the quality of Indigenous partnership structures that emerge over the next two to three years. For observers of Canada's critical minerals sector, Baptiste remains one of the most technically and strategically interesting projects on the development horizon.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across nickel, battery metals, and over 30 other commodities — translating complex data into clear, actionable opportunities for investors at every level. Explore how major discoveries have historically delivered substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.