May 18, 2026

The Copper Supply Crunch Is Coming Faster Than Most Investors Realise

The mining industry has spent the better part of a decade debating when the copper supply deficit will arrive. The answer, increasingly, is that it is already forming. Global demand trajectories tied to electric vehicle manufacturing, utility-scale battery storage, and grid modernisation are accelerating faster than greenfield mine development can keep pace with. The lead time from discovery to first production at a major copper mine now routinely exceeds fifteen years. That structural lag, compounded by a decade of underinvestment in exploration during the post-2012 commodity downturn, has left the pipeline of new large-scale copper assets dangerously thin.

Against this backdrop, the Barrick Zambia copper expansion at Lumwana super pit stands out not just as a corporate capital allocation decision, but as one of the most consequential copper development projects currently under construction anywhere in Africa. Furthermore, understanding this project requires examining both the geological context and the broader copper supply crunch that is reshaping investment priorities across the sector.

When big ASX news breaks, our subscribers know first

Why the Central African Copperbelt Still Dominates Global Copper Geology

Not all copper deposits are created equal. The Central African Copperbelt, spanning Zambia and the Democratic Republic of Congo, hosts some of the highest-grade sediment-hosted stratiform copper mineralisation on the planet. Unlike porphyry copper systems common in South America and the western United States, which typically grade between 0.3% and 0.6% copper, Copperbelt deposits frequently exceed 2% copper in ore, with some zones running considerably higher.

This geological distinction matters enormously for project economics. Higher-grade ore means more copper recovered per tonne of material processed, lower energy consumption per unit of metal produced, and a structurally lower cost position relative to lower-grade peers. The Copperbelt's ore types also tend to carry lower levels of deleterious impurities compared to certain South American deposits, simplifying metallurgical processing and improving recoveries.

Lumwana itself is somewhat different within the Copperbelt context. It is a large-tonnage, lower-grade disseminated copper deposit rather than the classic high-grade stratiform style, but its scale compensates through sheer volume. The expansion thesis rests precisely on this volume argument: process more tonnes, recover more copper, and spread fixed costs across a larger production base.

The Lumwana deposit's mineralogy is dominated by chalcopyrite, with the processing circuit designed around sulphide flotation. This metallurgical pathway is well-understood and capital-efficient at scale, reducing the technical execution risk that haunts more complex oxide-sulphide transitional ore bodies common elsewhere in Africa.

What the Lumwana Super Pit Expansion Actually Involves

The Barrick Zambia copper expansion at Lumwana super pit is a fundamentally different kind of mining project compared to the greenfield developments that dominate industry headlines. This is a brownfield expansion at an operating asset, which carries a materially different risk profile. The existing infrastructure, workforce, processing knowledge, and community relationships are already in place. What is being added is scale.

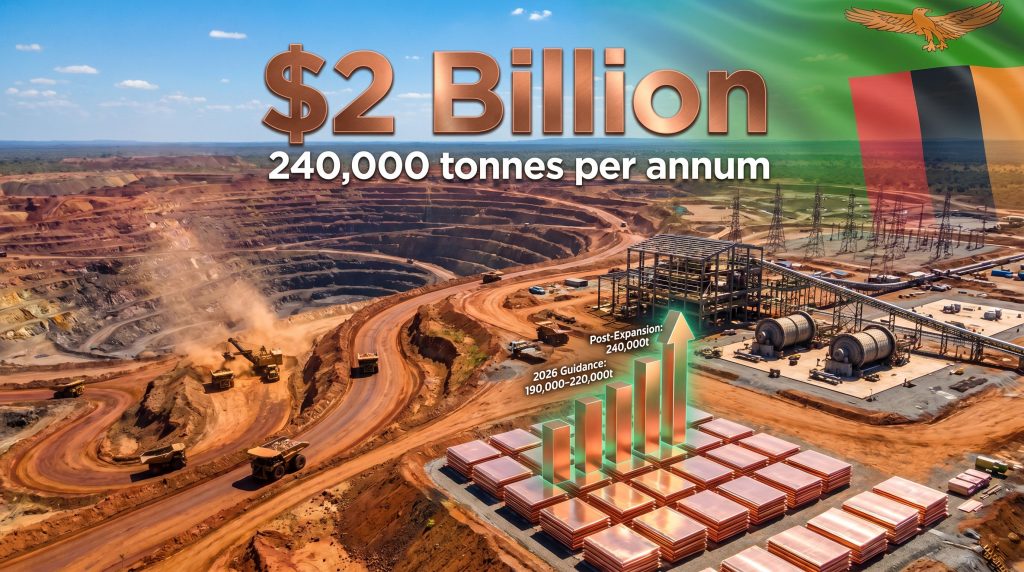

The core of the expansion involves scaling the processing plant to handle 50 million tonnes per annum of ore throughput, compared to the current operating rate. This throughput increase is the mechanical foundation for doubling annual copper output to approximately 240,000 tonnes per year. To put that in regional context, a Lumwana operating at that production rate would rank among the largest copper mines on the African continent.

Key physical components of the expansion include:

- Mill building wall construction, with the initial lift completed in Q1 2026

- Mill shells successfully delivered to site during the same period

- First structural steel loads anticipated to arrive on site in Q2 2026 (April to June)

- A new power transmission framework developed in partnership with ZESCO, Zambia's national electricity utility

- Development of a new airstrip to improve logistical connectivity

- Construction of an industrial supplier park designed to build in-country supply chain depth

- Manyama township infrastructure upgrades to support workforce accommodation

The project's construction schedule represents a carefully sequenced campaign. Long-lead equipment procurement, which is typically the greatest source of schedule risk in large mining expansions, has already been completed. This is a critical de-risking milestone that significantly reduces the probability of timeline slippage through the 2026 to 2027 construction peak.

Construction Timeline at a Glance

| Milestone | Expected Timing |

|---|---|

| Super Pit Expansion officially launched | 2024 |

| Construction commencement | 2025 |

| Mill shell delivery to site | Q1 2026 |

| First structural steel loads on site | Q2 2026 |

| First copper production from expansion | End of Q1 2028 |

| Target annual output post-expansion | 240,000 tonnes |

According to Barrick's official expansion update, the project is progressing on schedule, with construction firmly in full swing as Barrick works to establish Lumwana as a genuine Tier One copper mine.

Q1 2026 Operating Performance: Reading Between the Cost Numbers

Barrick's copper division produced 49,000 tonnes of copper in Q1 2026, representing an 11% year-on-year increase and a result that came in line with internal targets. That production outcome, while positive, is less analytically interesting than the cost structure sitting behind it.

Copper Cost Metrics: Q1 2026 vs Full-Year Guidance

| Cost Metric | Q1 2026 Actual | YoY Change | Full-Year 2026 Guidance |

|---|---|---|---|

| Cost of Sales (per lb) | $3.41 | +17% | $3.05 to $3.35 |

| Cash Costs (per lb) | $2.57 | +14% | $2.20 to $2.45 |

| All-In Sustaining Costs (per lb) | $3.67 | +20% | $3.45 to $3.75 |

The Q1 cost figures running above full-year guidance deserves unpacking. Two drivers explain most of the variance. First, royalties are calculated as a percentage of realised copper prices, so when copper prices are elevated, royalty obligations rise mechanically and proportionally. This is not an operational inefficiency; it is a structural feature of Zambia's fiscal regime that simultaneously increases the government's take when prices are strong.

Second, elevated site operating costs during Q1 reflect the pattern typical of large open-pit operations that front-load waste stripping and maintenance activities in the first quarter of the year. In addition, the copper price growth drivers currently underpinning the market are simultaneously amplifying royalty obligations at operating assets like Lumwana.

The gap between Q1 actuals and full-year guidance implies Barrick's internal modelling anticipates improving cost efficiency through the second half of 2026. This trajectory is consistent with mining operations where strip ratio management and scheduled maintenance cycles create an inherently uneven cost distribution across calendar quarters.

One additional cost sensitivity worth understanding: Barrick's 2026 cost guidance is based on an oil price assumption of $70 per barrel. For every $10 per barrel movement in oil prices, copper site costs shift by $0.04 per pound. This is a modest but real exposure given the diesel-intensive nature of open-pit truck-and-shovel operations at a super pit scale. At Lumwana, earthmoving volumes will increase significantly during the expansion construction peak, amplifying this oil price sensitivity compared to the steady-state operating period.

The Financial Engine Funding a $2 Billion Build

Understanding how Barrick can simultaneously fund the Lumwana expansion, maintain progressive shareholder returns, and execute a major buyback programme requires looking at the group-level financials that sit behind the copper division.

Barrick Group Financial Performance: Q1 2026

| Financial Metric | Q1 2026 Result |

|---|---|

| Total Revenue | $5.22 billion |

| Operating Cash Flow | $2.55 billion |

| Attributable Operating Cash Flow | $1.97 billion |

| Attributable Free Cash Flow | $1.21 billion |

| Net Earnings | $1.60 billion |

| Adjusted Net Earnings | $1.65 billion |

| EBITDA | $2.76 billion |

| EBITDA Growth (YoY) | +103% |

| EBITDA Margin Growth (YoY) | +66% |

Gold production of 719,000 ounces in Q1 2026 beat internal guidance, driven by the ramp-up at Loulo-Gounkoto in West Africa alongside strong performances at Nevada Gold Mines and Veladero. Gold cost of sales came in at $1,922 per ounce, with total cash costs of $1,327 per ounce and AISC of $1,708 per ounce, all benefiting from mining and processing efficiencies.

The doubling of EBITDA year-on-year to $2.76 billion is the headline number that explains Barrick's capital allocation confidence. At that cash generation rate, the full $2 billion Lumwana project capital represents less than one year of group EBITDA, and the $750 million to $850 million of 2026 capital expenditure guidance represents a fraction of annual free cash flow.

Barrick's board declared a quarterly dividend of $0.175 per share, with a stated policy of targeting a total annual payout equivalent to 50% of attributable free cash flow. The board also authorised a $3 billion share buyback programme at prevailing market prices. The coexistence of a large growth capex programme, a progressive dividend, and a $3 billion buyback is only arithmetically possible in a high gold price environment, and it signals a management team with high confidence in the sustainability of current cash generation.

Zambia's Economic Relationship With Lumwana: A Deeper Look

The Barrick Zambia copper expansion at Lumwana super pit carries economic implications that extend well beyond Barrick's corporate results. Since 2019, Lumwana has contributed more than $4 billion to the Zambian economy, with $3.4 billion of that total flowing to local and regional suppliers rather than being repatriated offshore. That localisation of expenditure is one of the more meaningful statistics in African mining, and it represents a structural feature of the Lumwana operation rather than a discretionary corporate responsibility initiative.

The workforce localisation rate of 98% Zambian nationals is equally notable. Most large-scale mining operations in Sub-Saharan Africa operate with expatriate technical staff filling a significant share of supervisory and specialist roles. A 98% local employment rate implies that Barrick has built deep technical capability within the Zambian workforce over the mine's operating life, reducing dependency on costly and logistically complex expatriate staffing arrangements.

Community and infrastructure investments accompanying the expansion include:

- Manyama township development with residential and community infrastructure upgrades

- An industrial supplier park intended to build local supply chain capacity and reduce import dependency for mining consumables

- A technical training centre designed to develop operational and maintenance skills within the Zambian workforce pipeline

- A new airstrip improving logistical connectivity for both equipment supply and personnel movements

These investments reflect a longer-term operational calculus as much as community relations strategy. A well-developed local supply chain reduces lead times, lowers transport costs, and decreases exposure to international logistics disruptions. The training centre directly addresses the technical skills pipeline needed to operate an increasingly complex and large-scale facility after the expansion is complete. Mining Weekly's coverage of the expansion further highlights how Barrick's high gold price environment is enabling these substantial community commitments alongside the core construction programme.

The next major ASX story will hit our subscribers first

Key Risks That Investors and Observers Should Monitor

Despite the positive Q1 2026 progress report, the Lumwana expansion faces several execution challenges that merit careful ongoing assessment.

Capital cost discipline is the primary concern. Mining megaprojects globally have a well-documented history of cost overruns, often attributable to labour productivity shortfalls, equipment availability constraints, and design changes during construction. The on-budget progress through Q1 2026 is an early positive signal, but the project is entering its capital-intensive construction peak through 2026 and 2027, where execution risk is historically highest.

Power supply reliability is a structural operational dependency for any large open-pit copper operation. Zambia's electricity grid has historically experienced capacity constraints that have periodically disrupted mining operations across the Copperbelt. The ZESCO partnership for dedicated transmission infrastructure is a structural mitigation, but grid reliability will remain a monitoring variable throughout construction and ramp-up.

Royalty mechanics and fiscal exposure create a partial counter-intuitive dynamic: when copper prices rise, Barrick's costs also increase due to price-linked royalty obligations. This is not a risk in isolation but a cost planning consideration that means the relationship between copper price upside and net earnings uplift is not perfectly linear.

Oil price sensitivity at $0.04 per pound per $10 per barrel movement becomes more material during the construction and ramp-up phase when diesel consumption is at its peak across both the expanding mine and the construction fleet simultaneously. However, the broader global copper supply gap means that even with these cost pressures, the long-term demand fundamentals remain compelling for projects of Lumwana's scale and quality.

Frequently Asked Questions: Barrick Zambia Copper Expansion at Lumwana Super Pit

When will the Lumwana Super Pit expansion produce first copper?

First copper production from the expansion is targeted for the end of Q1 2028. The project was officially launched in 2024, construction commenced in 2025, and key equipment milestones including mill shell delivery were completed in Q1 2026.

What is the total capital budget for the Lumwana expansion?

The total project capital is $2 billion. The 2026 capital expenditure allocation is expected to come in at the lower end of the $750 million to $850 million guidance range.

How much copper will Lumwana produce annually after the expansion?

The expanded operation targets approximately 240,000 tonnes per year, supported by a processing plant scaled to 50 million tonnes per annum of throughput, roughly doubling the current production rate.

What is Barrick's full-year 2026 copper production guidance?

Full-year 2026 copper production guidance is 190,000 to 220,000 tonnes, with cash costs guided at $2.20 to $2.45 per pound and AISC at $3.45 to $3.75 per pound.

Is the Lumwana expansion currently on schedule and on budget?

As of Q1 2026 reporting, Barrick confirmed construction was progressing on time and on budget. The initial mill building wall lift was completed, mill shells were delivered to site, and first structural steel loads were expected in Q2 2026.

How much has Lumwana contributed to Zambia's economy?

Lumwana has contributed more than $4 billion to the Zambian economy since 2019, with $3.4 billion directed to local and regional suppliers. The mine's workforce is 98% Zambian nationals.

Why the Timing of Lumwana's First Production in 2028 Is Strategically Significant

Copper supply forecasts from multiple independent industry sources converge on the late 2020s as the period when demand from electrification and grid infrastructure investments begins to structurally outpace primary mine supply. Existing operating mines face declining grades and rising strip ratios as deposits mature, while new greenfield projects face average development timelines that make meaningful supply additions before 2030 practically impossible for projects not already in construction today.

Lumwana is already in construction. That positioning places its expansion copper in a category of future supply that is genuinely scarce. For investors evaluating copper investment strategies in the current environment, a mine producing 240,000 tonnes per year from a Tier One jurisdiction, with a long mine life, an established processing infrastructure, and a deeply localised workforce, represents exactly the type of asset the copper market will need most precisely when it will be hardest to find.

For Barrick specifically, the expansion transforms copper from a meaningful but secondary revenue stream into a genuine strategic pillar capable of generating material cash flows independently of gold price movements. The combination of gold's current high price environment funding the construction phase, and copper's anticipated demand surge coinciding with the production ramp-up, represents an unusually favourable convergence of timing for one of the sector's most ambitious growth projects currently under development.

This article contains forward-looking statements and financial projections based on publicly available company guidance and industry forecasts. These involve inherent uncertainties and should not be construed as financial advice. Readers should conduct their own independent research before making any investment decisions.

Want To Catch the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors — explore Discovery Alert's discoveries page to understand how historic mineral finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the next major copper discovery.