June 15, 2026

Battery circularity innovation is shifting from niche sustainability theme to industrial capability

For most emerging technologies, the real bottleneck is not invention. It is what happens after the first growth wave, when supply chains tighten, waste streams build, and early design choices start locking in long-term economics. That is where battery circularity innovation now sits.

As electric vehicles, grid storage systems, and portable electronics spread through the global economy, batteries are becoming both a strategic asset and a future industrial waste challenge. The same lithium-ion pack that powers a vehicle today can become tomorrow’s source of recovered metals, refurbished modules, or second-life stationary storage. Whether that value is captured depends on far more than recycling alone.

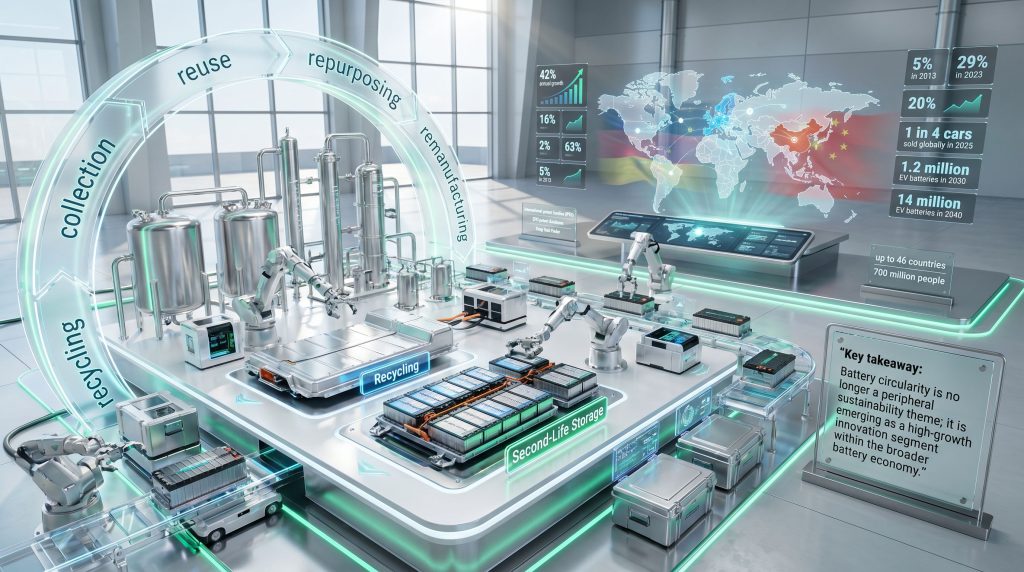

Battery circularity innovation refers to the technologies and business models that keep battery materials and components in productive use for longer through collection, reuse, repurposing, remanufacturing, and recycling. In practice, this means building a coordinated system that can identify batteries, move them safely, assess their condition, decide the best next use, and recover materials efficiently when reuse is no longer viable.

That system is drawing intense innovation attention. According to a 2026 joint analysis from the European Patent Office (EPO) and the International Energy Agency (IEA), international patent families related to battery circularity grew at an average 42% annual rate from 2017 to 2023. By comparison, rechargeable battery manufacturing grew at 16%, while all technical fields rose just 2% over the same period.

Key takeaway: Battery circularity is increasingly being treated as a strategic part of the battery economy, with implications for resource security, industrial competitiveness, and supply-chain resilience.

Why timing matters as EV battery retirements begin to scale

The opportunity is large partly because the retirement wave is predictable, even if the exact route each battery takes is not.

The IEA reported that more than 1 in 4 cars sold globally in 2025 were electric vehicles. That installed base will eventually feed a large end-of-life pipeline. The same EPO-IEA research indicates that around 1.2 million EV batteries could reach end of life in 2030, rising to roughly 14 million in 2040.

Those numbers matter because battery circularity is a throughput business as much as a chemistry business. At low volumes, collection networks are patchy, diagnostics can be costly, and recycling plants may struggle to secure feedstock. However, at higher volumes, unit economics can improve across the chain.

Battery circularity opportunity snapshot

- Global EV share of car sales: more than 25% in 2025

- EV batteries reaching end of life: 1.2 million in 2030

- EV batteries reaching end of life: 14 million in 2040

- Battery circularity patent growth: 42% CAGR, 2017 to 2023

- Rechargeable battery manufacturing patent growth: 16% CAGR

- All technical fields patent growth: 2% CAGR

- Asian share of battery circularity IPFs: 63% in 2023

- China share of battery circularity IPFs: 5% in 2013 to 29% in 2023

Not every retired battery goes directly to material recovery. A pack removed from an EV could follow several paths:

- Reuse in vehicles if performance remains acceptable after repair or module replacement

- Repurposing into stationary storage if residual capacity still supports lower-demand applications

- Direct recycling if the pack is damaged, degraded, unsafe, or economically unsuitable for second-life use

This distinction is important because waste volume and recoverable value are not the same thing.

Which technologies are shaping battery circularity innovation?

Battery circularity innovation spans much more than shredding and metal extraction. The strongest systems usually combine upstream logistics, diagnostics, and downstream processing.

1. Collection and reverse logistics

The first challenge is getting spent batteries into the right channel safely and efficiently.

Key functions include:

- Battery identification and labelling

- Safe storage and transport of high-voltage packs

- Sorting by chemistry, form factor, and damage condition

- Disassembly workflows for modules and cells

- Traceability tools such as digital battery passports

Collection may sound mundane compared with advanced chemistry, but it can become a decisive bottleneck. A recycler with excellent process technology still needs steady, compliant feedstock. In addition, insights from the National Battery Strategy priority on sustainability and circular economy reinforce how policy and infrastructure must develop together.

2. Reuse and second-life applications

Some batteries retire from vehicles before they are truly exhausted. The critical issue is state-of-health assessment.

Typical second-life steps include:

- Testing residual capacity, resistance, and safety

- Identifying modules suited to refurbishment

- Matching viable assets to backup power or stationary storage use cases

- Routing unfit material to recycling

This creates room for software-led and diagnostics-led business models. Furthermore, OEM activity in high-voltage battery recycling shows how design and end-of-life planning are increasingly linked.

3. Materials recovery and chemical transformation

When reuse is no longer practical, the battery enters recovery pathways designed to capture usable inputs for future manufacturing.

Common pathways include:

- Mechanical pre-processing

- Pyrometallurgical recovery

- Hydrometallurgical recovery

- Direct recycling

The source material specifically highlights chemical transformation processes that provide raw materials for new batteries as a major innovation focus. Europe appears particularly active here. Meanwhile, developments around the battery recycling process in China suggest scale and process integration are moving quickly.

What patent activity reveals about the market direction

Patent counts are not the same as revenue, margins, or commercial success. Still, they can be useful indicators when interpreted carefully.

An international patent family, or IPF, is a group of patent filings made in multiple countries for the same invention. Because filing internationally is expensive, IPFs often signal inventions that applicants see as commercially important or globally relevant.

That makes the recent growth trend meaningful. The 42% average annual growth in battery circularity IPFs from 2017 to 2023 suggests this is no longer a peripheral subtheme within clean tech. It is becoming a core innovation front inside the broader battery economy.

Energy storage, including batteries, now accounts for about 40% of all energy-related patenting, according to the EPO-IEA analysis. Patent intelligence is most useful when paired with plant commissioning data, lifecycle studies, and policy databases. For instance, the battery circular economy initiative also underlines the need to connect technology progress with real-world system design.

Which regions are leading battery circularity innovation?

Regional leadership is uneven, and each geography appears to be building a different model.

Regional innovation models in battery circularity

- Asia: 63% of IPFs in 2023, with broad value-chain coverage

- China: 29% in 2023, up from 5% in 2013

- Europe: roughly 20%, with strengths in collection and chemical transformation

Asia’s 63% share of 2023 IPFs reflects a scale advantage built on battery manufacturing density and industrial clustering. Japan and Korea were early leaders, with companies such as Toyota, LG, and Sumitomo prominent before 2020.

China’s rise is especially notable. Its share of battery circularity IPFs climbed from 5% in 2013 to 29% in 2023. The EPO-IEA analysis also noted that Chinese applicants are increasingly filing for protection outside China. Consequently, this points to a more global commercialisation strategy. It also aligns with interest in the Chinese battery recycling breakthrough.

Europe, at around 20% of IPFs, appears strongest in collection technologies and chemical transformation. That specialisation fits a market that is a major battery user but not the leading battery producer.

How policy frameworks shape innovation incentives

Policy does not replace good technology, but it can strongly influence whether circular systems reach scale.

The EPO-IEA analysis points to legislation in Europe and China that places responsibility on companies for end-of-life EV batteries as one factor accelerating innovation. That type of rule matters because it changes incentives around design, collection, traceability, and treatment.

Important policy levers include:

- Extended producer responsibility regimes

- Collection rate requirements

- Labelling and traceability standards

- Rules for battery shipment and handling

- Recycled-content compliance frameworks

- Support for pilot plants, scale-up, and research ecosystems

A subtle but important issue is feedstock certainty. Recycling plants need reliable inflows to justify capital investment. Stronger rules around take-back, classification, and reporting can improve visibility on future supply.

Emerging business models across the circular battery chain

Several commercial models are taking shape, and none relies on a single step.

Recycler-led models

These businesses focus on throughput, recovery yield, and exposure to underlying metal values. Their economics can be influenced by:

- Commodity price volatility

- Process efficiency

- Feedstock contracts

- Recovery purity and downstream offtake

OEM-led and vertically integrated models

Automakers and battery manufacturers may pursue closed-loop sourcing, take-back systems, and design-for-disassembly advantages. The strategic goal is often to retain material visibility and reduce reliance on primary supply over time. In that context, closed-loop battery recycling is becoming an increasingly important commercial template.

Platform and data-led models

This is one of the less appreciated areas of battery circularity innovation.

Examples include:

- Battery diagnostics software

- State-of-health analytics

- Digital compliance and traceability tools

- Asset routing marketplaces

A regional closed-loop ecosystem could involve a collection partner, diagnostics provider, refurbishment channel, recycler, and downstream manufacturer all linked by data and material tracking. Moreover, the wider push towards critical minerals recycling highlights why recovered battery materials are strategically valuable well beyond waste management.

The biggest bottlenecks investors and operators should watch

Despite the momentum, the sector still faces major technical and commercial friction.

Technical bottlenecks

- Diverse cell chemistries and pack formats

- Complex pack designs that slow disassembly

- Transport and handling safety risks

- Inconsistent state-of-health testing standards

Economic bottlenecks

- Uncertain feedstock volumes in the early years

- High capital requirements for processing facilities

- Margin sensitivity to commodity prices

- Competition from low-cost primary material supply

Regulatory and operational bottlenecks

- Cross-border waste classification problems

- Gaps in harmonised standards

- Limited visibility into battery composition and provenance

- Permitting delays for industrial facilities

Watchpoint: A circular battery economy may be technically feasible well before it becomes commercially durable. Scale tends to depend on logistics, policy consistency, and process economics rising together.

What the next phase may look like

The next phase is likely to be less about novelty alone and more about execution quality.

Areas likely to matter more over time include:

- Automation in disassembly and sorting

- Better purity and recovery yields

- Faster diagnostics and routing decisions

- More standardised pack design and traceability

- Tighter links between recyclers, OEMs, and downstream users

In strategic terms, secondary supply is unlikely to replace mining altogether. However, it may become a meaningful complement as retired battery volumes rise into the 2030s and 2040s. That matters in a world where battery mineral and component supply chains remain concentrated.

FAQ: Battery circularity innovation

What is battery circularity innovation?

It is the set of technologies and business models that extend battery usefulness and recover value through collection, reuse, repurposing, and recycling.

Why is it important for energy security?

It can reduce pressure on concentrated critical mineral supply chains, improve domestic material recovery, and build resilience into battery-dependent industries.

How fast is battery circularity patenting growing?

According to the EPO and IEA, battery circularity IPFs grew at an average 42% annually from 2017 to 2023.

Which regions lead battery circularity patents?

Asia led with 63% of 2023 IPFs, while Europe accounted for roughly 20%. China’s share rose from 5% in 2013 to 29% in 2023.

What happens to EV batteries at end of life?

Some are repaired or reused, some are repurposed for stationary applications, and others go directly to recycling depending on condition, safety, and economics.

The bottom line on battery circularity innovation

Battery circularity innovation is becoming an industrial race shaped by far more than recycling chemistry. The strongest positions are likely to come from integrated systems that link policy, logistics, diagnostics, processing, and end-market demand.

Patent growth data shows clear momentum. End-of-life EV battery volumes point to a much larger future opportunity. Regional competition is intensifying, with Asia leading in scale, China expanding globally, and Europe showing specific strengths in collection and chemical transformation.

For investors, operators, and policymakers, the central insight is simple: the long-term winners may not be the firms with the best lab result alone, but the ones that can convert future battery returns into a scalable, compliant, and economically resilient circular supply chain.

Could The Next Battery Supply Chain Winner Come From A Discovery?

Track the ASX companies shaping future-facing resource themes with real-time mineral discovery alerts powered by Discovery Alert’s proprietary Discovery IQ model, helping investors spot actionable opportunities early. See how major discoveries have historically driven exceptional returns on Discovery Alert’s discoveries page or start at the Discovery Alert home page with a 14-day free trial.