June 15, 2026

The Hidden Architecture of Battery-Grade Lithium Pricing: Why the CJK Differential Matters More Than You Think

Commodity benchmarks rarely make headlines until something changes. For most of the past decade, lithium pricing infrastructure evolved reactively, scrambling to keep pace with an electrification wave that transformed a niche industrial mineral into one of the most strategically watched commodities on earth. The result is a pricing ecosystem that remains far less standardised than most market participants realise, and one where a single methodology revision can send ripples through billions of dollars in derivatives exposure. The CJK lithium hydroxide differential arriving in August 2026 is exactly that kind of event, and understanding it requires unpacking several layers of pricing architecture that most investors and supply chain professionals have never had reason to examine closely.

When big ASX news breaks, our subscribers know first

The Regional Pricing Geometry of Battery-Grade Lithium

Lithium is not priced like iron ore or copper, where a dominant global benchmark absorbs most market activity. Instead, it trades across a matrix of delivery zones, chemical forms, purity thresholds, and particle specifications, each of which generates its own price signal. The CIF China, Japan and Korea (CJK) delivery zone sits at the apex of this matrix, representing the world's most concentrated cluster of lithium consumption.

China alone accounts for roughly 70% of global lithium-ion battery manufacturing capacity, with Japan and South Korea contributing significant additional volumes through cell makers and cathode producers. A CIF CJK price therefore reflects the landed cost of material at the ports most relevant to the actual buyers who convert lithium salts into battery components. Any distortion in this benchmark propagates downstream into cathode pricing, cell pricing, and ultimately pack-level cost models used by automotive OEMs.

The two dominant chemical forms assessed within this zone are:

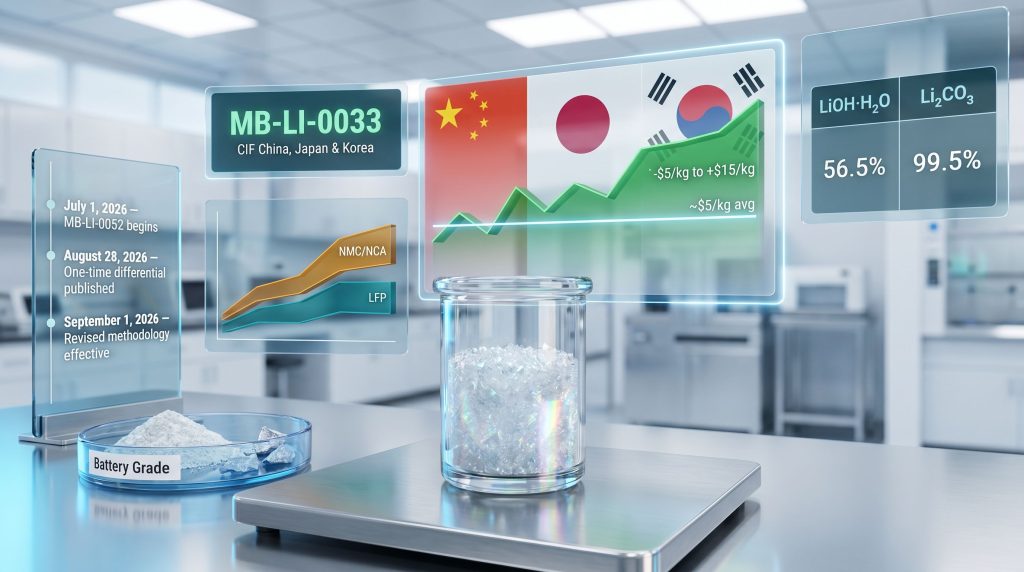

- Lithium hydroxide monohydrate (LiOH·H₂O) at a minimum purity of 56.5%, the preferred precursor for high-nickel NMC and NCA cathode chemistries

- Lithium carbonate (Li₂CO₃) at a minimum of 99.5% purity, the primary input for lithium iron phosphate (LFP) cathodes

These are not interchangeable. The cathode chemistry you choose largely determines which lithium salt you need, which is why the spread between hydroxide and carbonate prices functions as one of the most telling indicators of battery technology sentiment in global markets. Furthermore, the lithium carbonate supply-demand balance in any given period can independently shift this spread, adding another layer of complexity for analysts tracking the broader global lithium market.

What the Assessment Code MB-LI-0033 Actually Measures

The specific benchmark at the centre of the September 2026 methodology change is MB-LI-0033, the Fastmarkets assessment for lithium hydroxide monohydrate, minimum 56.5% LiOH·H₂O, battery grade, spot price, CIF China, Japan and Korea, denominated in USD per kilogram.

This is not merely an internal data product. MB-LI-0033 serves as the settlement reference for exchange-traded derivatives on platforms including CME Group, as well as over-the-counter swap contracts and long-term offtake agreements that incorporate price indexation. When this assessment changes, every open financial position referencing it faces a potential valuation discontinuity.

The Hydroxide-Carbonate Spread: A Battery Technology Barometer

One of the least appreciated analytical tools available to battery materials investors is the ongoing price relationship between lithium hydroxide and lithium carbonate on a CIF CJK basis. This spread is not static and its movement encodes information about where battery chemistry demand is heading.

| Metric | Lithium Hydroxide (MB-LI-0033) | Lithium Carbonate (MB-LI-0029) |

|---|---|---|

| Chemical form | LiOH·H₂O monohydrate | Li₂CO₃ |

| Minimum purity | 56.5% LiOH·H₂O | 99.5% Li₂CO₃ |

| Primary cathode application | NMC/NCA high-nickel | LFP |

| Historical spread range | Approx. -$5/kg to +$15/kg | Baseline reference |

| Long-run average premium | Approximately $5/kg above carbonate | N/A |

Market Intelligence: When the hydroxide-carbonate spread widens, it typically signals accelerating demand for premium NMC-chemistry EVs. When it compresses toward zero or inverts, it often reflects either overcapacity in hydroxide conversion or a surge in LFP adoption, a pattern closely associated with Chinese domestic EV market cycles where cost competitiveness favours iron phosphate chemistries.

The historical range of approximately negative $5 per kilogram to positive $15 per kilogram illustrates just how dramatically technology preferences can shift the relative value of two chemically distinct lithium compounds. This is not commodity noise. It is a structural signal.

Why the 2026 Methodology Revision Became Necessary

The decision to revise the MB-LI-0033 assessment specification did not emerge from administrative preference. It was driven by an observable deterioration in the quality of transactions being captured within the existing assessment window.

Fastmarkets documented an increase in reports of unqualified lithium hydroxide entering the assessment pool. This material, which does not meet standard battery-grade requirements, typically trades at a meaningful discount to product that cathode manufacturers will actually accept. When discounted, substandard material is included in a benchmark calculation, the reported price is suppressed below the level at which commercially usable material actually changes hands.

This creates a systematic distortion that disadvantages producers of qualified product and provides misleading price signals to buyers benchmarking their procurement costs. Consequently, the integrity of the entire derivatives settlement ecosystem built upon MB-LI-0033 was being gradually undermined.

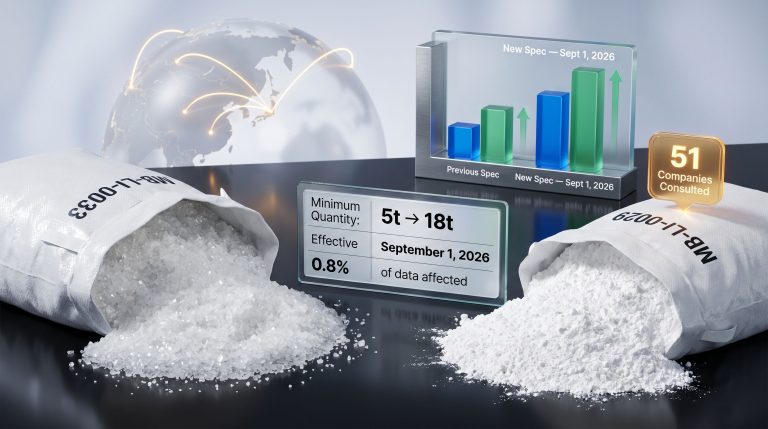

To validate the scope of the problem, Fastmarkets conducted an extensive consultation process involving more than 50 companies spanning the full lithium supply chain, including miners, converters, cathode manufacturers, and battery cell producers. The majority of respondents supported tighter qualification criteria, providing the empirical foundation for the methodology change.

The revised specification targets non-clumping, non-agglomerated coarse powder material that has achieved broad qualification status among end-buyers. This is a technically specific requirement: agglomerated or clumping hydroxide presents handling and processing challenges in cathode production lines, and its exclusion from the benchmark ensures the assessment better reflects material that is operationally viable for battery manufacturing.

The Full Consultation and Implementation Timeline

| Date | Milestone |

|---|---|

| January 23, 2026 | Initial market consultation opened |

| March 30, 2026 | Formal methodology change proposal published |

| June 15, 2026 | Decision confirmed and pricing notice issued |

| July 1, 2026 | Daily differential tracking begins under MB-LI-0052 |

| August 28, 2026 | One-time differential published via subscriber note |

| September 1, 2026 | Revised methodology becomes effective |

| December 31, 2026 | Daily differential code publication ceases |

How the One-Time CJK Lithium Hydroxide Differential Is Calculated

The mechanics behind the differential are designed to resist manipulation and minimise the impact of short-term volatility. Rather than using a single day's price gap as the adjustment figure, a rigorous averaging process runs across approximately 42 UK working days.

The step-by-step calculation process works as follows:

- Each UK working day between July 1 and August 28, 2026, a daily spread is calculated between the existing MB-LI-0033 assessment and the value the market would register under the revised specification

- This daily spread is published at close of business under the new code MB-LI-0052, providing real-time transparency throughout the transition window

- At the close of the observation period, the arithmetic average of all published daily spreads is calculated

- The averaged figure is released as the one-time differential via subscriber note on August 28, 2026, three days before the methodology goes live

Why arithmetic averaging over a snapshot? A single-day differential is inherently fragile. Thin volumes, a one-sided trade, or an anomalous market event could produce a figure unrepresentative of the actual price impact. Averaging across roughly two months of working days creates statistical robustness and a figure that supply chain participants can defend to their own counterparties and finance teams.

The transparency architecture around MB-LI-0052 is particularly notable. Rather than presenting the final differential as a black-box calculation, publishing the underlying daily spreads in real time allows every market participant to monitor the evolving trajectory and anticipate the final figure well before it is formalised.

What the Differential Is and What It Is Not

| The Differential IS | The Differential IS NOT |

|---|---|

| A reference point for adjusting contract valuations | A mandated settlement price for any specific contract |

| A transparent estimate of the specification change's forward curve impact | A guarantee of actual price effect on individual trades |

| A market transition support tool, published with full daily data | Applicable to lithium carbonate (MB-LI-0029) |

| Available to all Fastmarkets subscribers via notice | A liability-bearing figure accepted by the publishing agency |

Why Lithium Carbonate Is Excluded From the Differential

A question that will naturally arise among market participants is why a parallel differential is not being published for MB-LI-0029, the companion carbonate assessment. The answer is empirical rather than arbitrary.

Fastmarkets conducted an internal data analysis of the transactions that would be excluded under the tightened specification for lithium carbonate and found that these data points had no material effect, or only a negligible effect, on carbonate price formation. The transactions falling outside the new qualification window were not meaningfully influencing where the carbonate benchmark settled, which means the specification change will not create a measurable pricing discontinuity for that assessment.

This asymmetry between the two lithium salts reflects genuinely different market structures. The hydroxide market has historically attracted a wider dispersion of product quality, partly because conversion capacity has expanded rapidly in recent years. The spodumene-to-lithium salts conversion pathway, in particular, has seen aggressive capacity additions from newer entrants producing material that meets chemical purity thresholds but fails physical handling specifications.

The carbonate market, which is more closely tied to brine-based production in South America and established processing infrastructure, appears to have maintained tighter de facto quality consistency within its transaction pool. However, emerging direct lithium extraction technologies may eventually alter that dynamic as new production methods enter the commercial assessment pool.

The next major ASX story will hit our subscribers first

Derivative Exposure and Practical Contract Scenarios

Who Needs to Pay Attention

The practical significance of the CJK lithium hydroxide differential extends across several categories of market participant:

- Lithium producers and converters with open futures or swap positions referencing MB-LI-0033 who need to understand how their mark-to-market exposure may be affected by the methodology transition

- Cathode manufacturers and battery cell producers operating under long-term indexed supply agreements where the reference price shifts on September 1

- Commodity exchanges administering futures and options contracts that settle against the weekly Fastmarkets CJK hydroxide assessment

- Banks and trading houses providing price risk management services to the battery materials supply chain

Two Practical Scenarios

Scenario A, Exchange-Traded Position: A lithium producer holds open CME futures contracts settling against MB-LI-0033. Under the new specification, the settlement price may diverge from what it would have been under the old methodology. The one-time differential provides a reference value that the exchange or counterparties can apply to reconcile the position across the methodology boundary.

Scenario B, Long-Term Offtake Agreement: A battery manufacturer holds a multi-year supply contract priced at a fixed discount to the CIF CJK spot assessment. As the specification changes what transactions feed into that assessment, the differential offers a mechanism to recalibrate the contract's reference baseline without reopening the entire commercial agreement.

Important Disclaimer: The one-time differential is published as a reference tool only. Fastmarkets explicitly accepts no responsibility or liability for any use of the adjustment figure, whether in exchange settlement, OTC derivative valuation, or any other contractual context. Each market participant must independently determine whether and how the differential applies to its specific arrangements, taking its own professional advice where necessary.

Reading the Differential as a Forward Signal for Battery Technology

Beyond its immediate function as a transition mechanism, the CJK lithium hydroxide differential and the hydroxide-carbonate spread it sits within carry longer-range analytical value for investors tracking the battery technology landscape. In addition, the battery storage lithium demand trajectory will increasingly influence how much weight the market places on hydroxide versus carbonate signals.

The key market signals embedded in the spread dynamics include:

- A widening hydroxide premium typically accompanies accelerating NMC and NCA adoption, driven by demand for higher energy density cells in premium EV segments and grid storage applications where weight and volume constraints are critical

- A compressing or negative differential tends to reflect either oversupply in hydroxide conversion capacity, which has expanded aggressively across Chinese and South Korean refining infrastructure, or a rotation in battery chemistry preferences toward LFP

- The 2026 specification tightening may itself create a short-term widening effect in the assessed price of qualifying hydroxide, since the exclusion of discounted unqualified material will, by construction, raise the average price of transactions included in the benchmark

| Supply Chain Driver | Impact on Hydroxide Premium |

|---|---|

| Expansion of spodumene-to-hydroxide conversion capacity | Compresses premium |

| Growth in high-nickel NMC/NCA adoption | Widens premium |

| LFP battery market share gains | Compresses premium |

| Quality specification tightening | Short-term widening for qualifying material |

| Brine-based carbonate supply growth | Neutral to mild compression |

Benchmark Maturation in the Battery Materials Era

The process surrounding the 2026 CJK lithium hydroxide differential illustrates something important about where battery materials pricing infrastructure currently sits in its development cycle. Unlike crude oil, which has operated under mature benchmark frameworks for decades, battery-grade lithium only began attracting serious financial market participation within the past several years. The assessment methodologies underpinning derivatives settlement are still being actively refined.

What distinguishes this particular revision is the transparency of the process. An extended consultation involving over 50 supply chain stakeholders, a multi-month pre-publication window for daily tracking data, clear delineation of which assessments require a differential and empirical justification for the exclusions, and explicit disclaimer framing around the reference-only nature of the published figure all point toward a maturing benchmarking ecosystem.

As battery material markets deepen and the volume of financial instruments referencing lithium price assessments grows, the precision and credibility of these benchmarks will become increasingly foundational, not just for physical traders, but for the project finance structures, index products, and risk management frameworks that the broader energy transition depends upon.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and analytical interpretations involve inherent uncertainty. Readers should conduct their own due diligence and seek independent professional advice before making any commercial or investment decisions based on the information presented here. Methodology documentation and pricing notices for battery-grade lithium assessments are publicly available at Fastmarkets.

Want to Stay Ahead of Major ASX Mineral Discoveries in the Battery Materials Sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across lithium and more than 30 other commodities, instantly converting complex geological data into actionable investment insights for traders and long-term investors alike. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.