June 15, 2026

How Commodity Benchmarks Break Down When Physical Markets Change

Every commodity benchmark carries an implicit assumption: that the specification underpinning it still reflects what the market actually trades. When physical markets drift and product quality diverges, that assumption begins to crack. Price assessments that were once precise instruments for contract indexation and financial settlement start capturing a broader, noisier signal — one that conflates battery-grade material with substandard or unqualified product. The result is artificially wide price spreads that obscure where the real market sits.

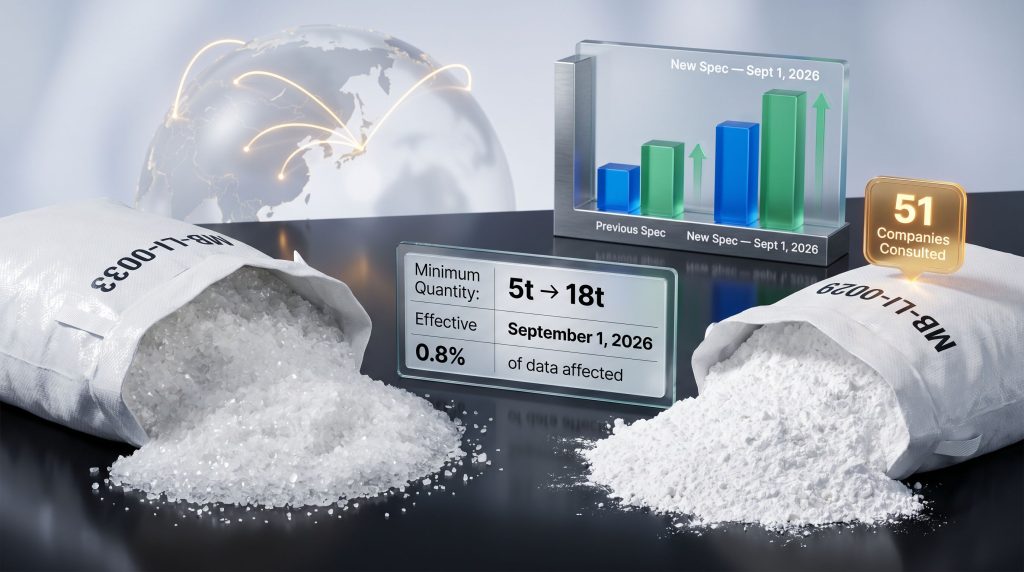

This is precisely the dynamic that triggered Fastmarkets' decision to update the specifications for its two core Fastmarkets battery-grade CIF CJK lithium salts methodology changes: MB-LI-0033 (lithium hydroxide monohydrate) and MB-LI-0029 (lithium carbonate). Effective Tuesday, September 1, 2026, both assessments will operate under revised quality, tonnage, payment, shelf life, and timing parameters designed to sharpen the signal and remove structural noise from the pricing data.

When big ASX news breaks, our subscribers know first

Understanding the Two CIF CJK Lithium Benchmarks at the Centre of This Review

What MB-LI-0033 and MB-LI-0029 Actually Measure

These two assessments are among the most widely referenced spot price indicators in the global battery-grade lithium market. They are not forward curves or forecasts. They are physical spot price assessments representing the cost of delivering lithium salts to buyers in China, Japan, or Korea under standard commercial conditions.

- MB-LI-0033 covers lithium hydroxide monohydrate (LiOH.H₂O) with a minimum 56.5% LiOH content, battery grade, assessed on a CIF China, Japan and Korea basis.

- MB-LI-0029 covers lithium carbonate (Li₂CO₃) at a minimum 99.5% purity, battery grade, on the same CIF CJK basis.

Both assessments serve as reference anchors for cathode active material (CAM) producers, OEM procurement departments, battery cell manufacturers, and commodity traders operating across the Asia-Pacific supply chain. They are also embedded in long-term offtake agreements and, in the case of hydroxide, in financial derivative contracts. Understanding the lithium carbonate supply dynamics that underpin these assessments is therefore essential for any participant navigating this market.

Why CIF CJK Differs From Other Regional Benchmarks

The global lithium pricing architecture is fragmented by region and trade structure. CIF CJK prices incorporate international freight, insurance, and delivery costs to North Asian ports, making them structurally different from:

- EXW domestic China prices, which reflect ex-works factory gate valuations subject to Chinese VAT treatment

- DDP Europe assessments, which include import duties and inland delivery to European buyers

- DDP US and Canada prices, which layer in tariff costs and North American logistics

South American-origin lithium salts introduce an additional layer of complexity into CIF CJK price formation. Transit times from Chile or Argentina to northern Asian ports can exceed 60 days, which means that much of the South American spot material entering the CIF CJK market is pre-positioned in warehouses closer to destination ports before the clock starts on delivery timelines. To better understand how lithium brines work in this context, it's worth noting that brine-sourced material from South America represents a significant share of CIF CJK spot supply.

The Full Specification Changes Taking Effect September 1, 2026

Side-by-Side Comparison: What Changes Across Both Benchmarks

| Parameter | MB-LI-0033 Previous | MB-LI-0033 New (Sept 1, 2026) | MB-LI-0029 Previous | MB-LI-0029 New (Sept 1, 2026) |

|---|---|---|---|---|

| Quality | Powder, accepted by buyer for battery applications | Non-clumping, non-agglomerated coarse powder; D50 200-700 μm; widely qualified by buyers in destination country | Powder, accepted by buyer for battery applications | Powder, widely qualified by buyers in destination country |

| Minimum Quantity | 5 tonnes | 18 tonnes (one container-load) | 5 tonnes | 18 tonnes (one container-load) |

| Payment Terms | Not specified | Letter of credit at sight | Not specified | Letter of credit at sight |

| Shelf Life | Not specified | Big bags, within 6 months of production or reprocessing date | Not specified | Big bags, within 9 months of production or reprocessing date |

| Timing | 60 days (undefined) | Delivery from seller to buyer within 60 days | 60 days (undefined) | Delivery from seller to buyer within 60 days |

The Physical Chemistry Behind the Hydroxide Quality Upgrade

The most technically significant change in this revision applies exclusively to MB-LI-0033. Beyond tightening the qualification language, the new specification introduces a physical particle size standard: coarse powder defined as a D50 between 200 micrometres and 700 micrometres, with explicit requirements that material be non-clumping and non-agglomerated.

This matters for several reasons that are not immediately obvious to non-specialist observers:

- D50 is the median particle diameter in a particle size distribution. A D50 of 200-700 μm defines a coarse powder range that matches the handling and processing requirements of most battery-grade hydroxide slurry preparation systems used in cathode manufacturing.

- Clumping and agglomeration in lithium hydroxide occur primarily through moisture absorption during storage or transport. Agglomerated material presents inconsistent reactivity profiles in cathode synthesis, creating yield variability that battery producers actively screen against.

- Fine powder (below 200 μm D50) behaves differently in processing environments, with higher surface area increasing reactivity but also dust hazard. Its qualification profile in battery facilities differs from coarse powder.

A product that looks chemically identical on a specification sheet can have profoundly different processing characteristics depending on its physical form. The D50 threshold formalises what buyers in the CJK market have already been applying informally in qualification decisions.

Why Lithium Carbonate Gets Lighter Treatment

The MB-LI-0029 changes are narrower in scope. The quality language shifts from accepted to widely qualified, but no particle size specification is imposed. This reflects the different end-use profile of lithium carbonate, which feeds into lithium iron phosphate (LFP) cathode chemistry and industrial applications that carry distinct processing requirements compared to the nickel-heavy cathode chemistries that drive hydroxide demand.

Furthermore, the spodumene-to-lithium salts conversion pathway remains an important upstream consideration, particularly as hard-rock-sourced carbonate and hydroxide both feed into these assessments. The specification changes to MB-LI-0029 are expected to have a negligible pricing effect on the assessment — a conclusion that received broadly supportive feedback from across the supply chain during consultation.

The Data Behind the 18-Tonne Minimum Volume Decision

Why Sub-Container Volumes Distort Physical Benchmarks

The increase in minimum tradeable quantity from 5 tonnes to 18 tonnes is arguably the most commercially logical of the changes, even if it received the most scrutiny on liquidity grounds. The reasoning is straightforward: the CIF CJK lithium salt spot market trades in container-load units. A standard shipping container holds approximately 18 tonnes of lithium hydroxide or carbonate in big bags. Pricing data from sub-container transactions represents a fundamentally different commercial context.

Sub-18-tonne lots consistently trade at a significant premium over standard container-load quantities, reflecting the higher per-unit logistics cost, bespoke handling requirements, and limited counterparty base for small-volume spot transactions. Including such data in a benchmark designed to reflect the mainstream commercial market introduces an upward distortion.

What the Historical Data Actually Shows

Fastmarkets collected 2,799 data inputs for MB-LI-0033 between January 1, 2025 and May 14, 2026. The breakdown is illuminating:

- Only 8 data points recorded volumes below 5 tonnes (the previous minimum)

- A further 23 data points fell between 5 and 18 tonnes

- Applying the new 18-tonne threshold retroactively would have excluded just 31 data points out of 2,799, or roughly 0.8% of the total assessment dataset

The 18-tonne minimum change affects less than 1% of historical pricing data. This is a precision adjustment, not a liquidity curtailment.

Payment Terms and Shelf Life: Clarifying What Was Always Implied

Letter of Credit at Sight as the Base Standard

The absence of specified payment terms in the previous methodology created a subtle but real distortion risk. In a market where settlement timelines range from immediate (telegraphic transfer, cash against documents) to 30 or 60 days deferred, allowing mixed-term data into the same assessment pool introduces a time-value-of-money premium that varies across transactions.

Letter of credit at sight is the dominant settlement instrument in the CIF CJK lithium spot market, reflecting the cross-border, multi-party nature of transactions where buyers and sellers may not have established credit relationships. The normalisation pathway for equivalent instruments — including cash against documents, telegraphic transfer, and bank acceptance — preserves the assessment's ability to incorporate the full breadth of spot market data while anchoring to a consistent base.

Critically, all 51 companies that submitted feedback on payment terms were supportive of this change, making it the single area of unanimous agreement across a consultation that otherwise generated considerable debate.

Shelf Life as a Material Quality Variable

Lithium hydroxide is hygroscopic. It absorbs atmospheric moisture readily, and once stored in permeable packaging or exposed to humid conditions, the quality profile can degrade in ways that affect qualification status with battery producers. This makes shelf life a genuinely material variable in benchmark design, not an administrative footnote.

The final specifications reflect a carefully negotiated middle ground between buyer and producer preferences:

- Buy-side participants argued for a 3-month maximum shelf life window, reflecting strict incoming quality control requirements at cathode plants

- Producer participants maintained that material stored correctly can remain battery-grade for up to 12 months

- The final standard lands at 6 months for hydroxide (MB-LI-0033) and 9 months for carbonate (MB-LI-0029), with a normalisation pathway for material stored in airtight bags or drums

The longer window for carbonate reflects its greater chemical stability relative to hydroxide under standard storage conditions.

What Triggered the Review: Unqualified Material Entering the Pricing Pool

The Problem With Widening Price Spreads

Price reporting agencies publish not just a mid-point but a low-high assessment range that captures the spread of reported transaction prices within the specification window. When that range widens materially, it is a diagnostic signal that the assessed specification is capturing heterogeneous product.

This is precisely what began occurring in the CIF CJK battery-grade lithium hydroxide market. An increasing volume of pricing data was being submitted for unqualified lithium hydroxide — a category of material that trades at a significant discount to the majority of the market because it has not received qualification approval from cathode or battery producers in China, Japan, or Korea.

Unqualified material often serves as feedstock for chemical conversion processes or non-battery industrial applications. Its pricing reflects these alternative use-case economics rather than the competitive spot market for battery-qualified lithium hydroxide. Including it alongside widely qualified material created assessment ranges that were technically accurate but commercially misleading. Innovations in direct lithium extraction may, however, eventually alter the qualification landscape by producing higher-consistency output that is easier to standardise across assessments.

Internal Data Analysis: March to May 2026

An internal analysis of pricing data conducted over the March to May 2026 period demonstrated that applying the revised widely qualified specification to the same historical dataset produced a narrower low-high assessment range positioned at a higher level than the existing methodology generated over the same timeframe.

This finding is significant but requires careful interpretation. It reflects the historical relationship between qualified and unqualified material pricing during that specific window. It does not constitute a forecast that lithium hydroxide prices will be higher after September 1, 2026. Future supply-demand fundamentals, the evolving qualification status of lithium salt brands across CJK markets, and broader battery raw materials market conditions will all influence where prices ultimately land.

The next major ASX story will hit our subscribers first

How the 51-Company Consultation Shaped the Final Outcome

Stakeholder Alignment by Supply Chain Position

| Stakeholder Group | Count | General Stance |

|---|---|---|

| OEMs | 14 | Broadly supportive of tighter quality language |

| CAM Makers | 10 | Broadly supportive |

| Trading Houses | 8 | Mixed; concerns on pricing impact |

| Producers | 17 | Mixed; some opposed on pricing grounds |

| Miners | 2 | Limited feedback submitted |

The consultation ran from January 23 to May 29, 2026, with the feedback window extended from its original close date following a notice published on May 15. The implementation date was itself shifted from the originally proposed August 3 to September 1, again in direct response to market feedback requesting additional transition time. Fastmarkets has published a detailed consultation summary for those wishing to review the full scope of market responses.

58% of respondents on the quality specification question expressed support for the tightened widely qualified language, spanning OEMs, CAM makers, traders, and producers. Opposition was concentrated among a subset of producers who raised concerns that narrowing the specification would elevate the assessed price by removing lower-priced unqualified data.

Fastmarkets has made clear that price direction is not a criterion in methodology decisions. The benchmark must reflect the most representative specification of the prevailing physical spot market, regardless of whether that has upward or downward price implications.

Operationalising "Widely Qualified": The Evidence Framework

What Market Participants Will Need to Demonstrate

The shift from accepted by buyer to widely qualified introduces an evidentiary dimension that did not previously exist in formal benchmark administration for these assessments. In practice, widely qualified means product that is evidenced to be accepted for battery applications by more than one cathode or battery producer in the destination country, though the precise threshold can vary based on the evidence submitted alongside pricing data.

Reporters engaging with the market will assess qualification status through:

- Direct engagement with producers, traders, CAM manufacturers, and cell producers to track brand-level qualification status across CJK markets

- Review of transactional evidence submitted alongside pricing data, where market participants may be asked to substantiate qualification claims

- Daily publication of pricing rationales that explain why specific data points were excluded or treated with lower confidence, without naming product brands to preserve source confidentiality

Data submitted without qualification evidence, or from sources unwilling to provide supporting documentation, will be treated with lower confidence in the assessment process. This creates a soft enforcement mechanism without imposing a rigid binary pass/fail standard that could introduce its own distortions.

Derivative Contract Implications: The One-Time Differential Adjustment

What Holders of CJK Lithium Hydroxide Derivative Contracts Need to Know

The methodology changes carry direct implications for participants in the financial derivatives market linked to the CIF CJK lithium hydroxide assessment. Participants can also reference the CME Group lithium hydroxide contract for further context on how these benchmarks underpin exchange-traded instruments. A separate Fastmarkets notice confirms that a one-time differential adjustment will be published for the CJK lithium hydroxide derivative contract when the revised methodology takes effect on September 1, 2026.

This adjustment will be calculated as the average of a daily differential measured between the existing assessment and the daily valuation of the market under the revised methodology over the transition period. Derivative contract holders and financial market participants managing positions indexed to MB-LI-0033 will need to incorporate this adjustment into settlement calculations and risk management frameworks before the implementation date.

Cross-Regional Alignment: Beyond the CJK Market

The September 1, 2026 Fastmarkets battery-grade CIF CJK lithium salts methodology changes are being implemented in parallel with corresponding specification updates across other Fastmarkets lithium carbonate benchmarks, including:

- EXW domestic China lithium carbonate assessments

- DDP Europe lithium carbonate assessments

- DDP US and Canada lithium carbonate assessments

This cross-regional alignment is significant from a price discovery perspective. When different regional benchmarks operate under materially different specifications, the differentials between them can reflect specification divergence as much as genuine logistics cost differences or regional supply-demand fundamentals. Harmonising the quality language across geographies consequently creates a more coherent global pricing architecture for battery-grade lithium carbonate. The Fastmarkets battery-grade CIF CJK lithium salts methodology changes represent, in this sense, not just a technical revision but a foundational step in improving the integrity of global lithium price benchmarking.

This article is based on publicly available information from Fastmarkets pricing notices and methodology documentation. The data analysis referenced regarding price assessment ranges during March to May 2026 reflects historical conditions and does not constitute a forecast of future lithium price movements. Methodology changes are designed to ensure benchmark representativeness and are not intended to signal any particular price direction. Readers should not rely on this article for investment or commercial decision-making without consulting qualified advisers and primary source documentation.

Want to Stay Ahead of the Next Major Lithium Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries — including battery metals like lithium — are announced on the ASX, transforming complex data across 30+ commodities into a single, actionable gold-equivalent metric. Explore historic examples of exceptional discovery returns and begin a 14-day free trial to position yourself ahead of the broader market.