May 22, 2026

The Technology Reshaping How the World Sources Battery Nickel

Most conversations about nickel supply chains begin and end with Indonesia. The archipelago nation accounts for roughly half of global mined nickel output, and its rapid expansion of nickel pig iron and high-pressure acid leach capacity has reshaped pricing dynamics across the entire market. However, the Indonesian nickel price trends that once made this concentration look advantageous are now becoming a liability for Western battery manufacturers facing mounting regulatory scrutiny over supply chain provenance, carbon intensity, and environmental governance.

Into this gap steps Brazil, and more specifically, a project in the northeastern state of Piauí that has been quietly accumulating geological data, metallurgical test work, and strategic financing interest for decades. The Brazilian Nickel Brejo Seco project in Piauí represents one of the most technically mature laterite nickel developments outside of operating production anywhere in the world, and its trajectory toward a final investment decision is attracting attention from investors, battery manufacturers, and development finance institutions alike.

When big ASX news breaks, our subscribers know first

Understanding the Laterite Nickel Opportunity

Why Laterites Have Been Both Promising and Problematic

Nickel deposits broadly divide into two categories: sulphide ores, which are typically higher-grade but increasingly rare and deep, and laterite ores, which are far more abundant but historically more difficult and expensive to process. Furthermore, understanding nickel uses and importance helps contextualise why laterites, which account for approximately 70% of global nickel resources, have attracted such persistent development interest despite their processing challenges.

The conventional routes for laterite processing carry significant cost and environmental burdens:

- High-Pressure Acid Leach (HPAL) requires extreme temperatures and pressures, generating wet tailings and demanding substantial capital investment

- Rotary Kiln Electric Furnace (RKEF) is extraordinarily energy-intensive and produces a ferronickel unsuitable for battery cathode chemistry without further refining

- Both methods carry high carbon footprints relative to what battery manufacturers increasingly require from their supply chains

The emergence of heap leaching as a viable laterite processing route changes this equation materially. By stacking crushed ore on engineered impermeable pads and irrigating it with an acidic lixiviant solution, operators can dissolve nickel and cobalt at ambient temperatures and pressures, dramatically reducing energy consumption and eliminating the wet tailings that have caused catastrophic dam failures at other Brazilian mining operations.

The Brejo Seco Deposit: Geology Built Over Half a Century

Located at Brejo Seco in the municipality of Capitão Gervásio Oliveira, Piauí, the deposit is a classic tropical laterite formed through deep weathering of ultramafic parent rocks over geological timescales. What makes it unusual is not its geology, which is broadly consistent with other major Latin American laterite systems, but the depth of human knowledge accumulated about it.

Brazilian Nickel's geology manager presented the project at Simexmin 2026, Brazil's foremost mining and mineral exploration symposium, describing how the accumulation of more than 50 years of geological studies has transformed the asset. That extraordinary knowledge base means the project's 3D geological model rests on an extensive drill core database and metallurgical test work library that most development-stage assets simply cannot match.

In operational terms, this translates into significantly greater predictability around ore variability, processing performance, and mine planning — factors that typically represent the highest sources of technical risk at comparable projects. The geology team at Simexmin noted that this depth of historical data enables greater operational predictability and quality control in laterite ore mining, a statement that carries real weight when considered against the track record of HPAL projects globally, where ore variability has caused repeated commissioning delays and cost overruns.

How Brazilian Nickel's Heap Leach Technology Works

Proprietary Process, Pilot-Validated Performance

Brazilian Nickel has not simply adopted a generic heap leach design. The company developed and validated a proprietary heap leach process specifically calibrated for the mineralogical characteristics of Piauí's laterite ore. Critically, this technology was proven at pilot-plant scale before the project advanced to commercial engineering design, a sequencing that meaningfully reduces the technical risk investors typically apply to pre-production laterite assets.

The process produces two intermediate products:

- Nickel hydroxide product (NHP): an accepted precursor feed for battery cathode manufacturing

- Cobalt hydroxide product (CHP): similarly positioned within battery material supply chains

A crucial distinction for investors and industry observers is that tonnage figures reported for NHP are substantially higher than figures reported for contained nickel metal, because the hydroxide product includes water and hydroxide content in addition to the metal itself. Consequently, comparing project outputs across the industry requires consistent use of contained-metal equivalents to avoid misleading comparisons.

Processing Method Comparison

| Processing Method | Energy Intensity | Wet Tailings Generated | Relative Capital Cost | Carbon Footprint |

|---|---|---|---|---|

| High-Pressure Acid Leach (HPAL) | Very High | Yes | Very High | High |

| Rotary Kiln Electric Furnace (RKEF) | Very High | No | High | Very High |

| Brejo Seco Heap Leach | Low to Moderate | Zero | Moderate | Low |

The zero wet tailings outcome is not merely an environmental credential. It is a direct response to the legacy of Brazil's own mining disasters, most notably the 2019 Brumadinho tailings dam collapse, which killed 270 people and permanently altered the regulatory and social licence landscape for mining in Brazil. A processing route that structurally eliminates wet tailings removes a category of catastrophic risk that would otherwise shadow the project's financing and community relations indefinitely.

Project Scale, Production Targets, and Development Status

What the Numbers Say

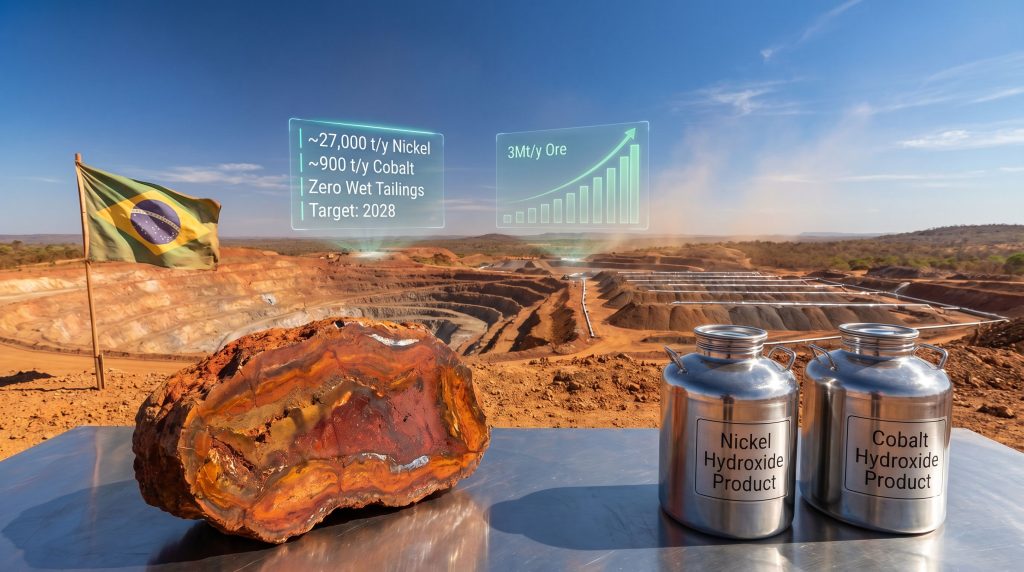

The Brejo Seco project is designed around an ore processing throughput of approximately 3 million tonnes per year. Based on disclosures from strategic investor TechMet, the project targets:

- Approximately 27,000 tonnes of contained nickel per annum

- Approximately 900 tonnes of contained cobalt per annum

Earlier project materials have referenced figures of up to 100,000 tonnes per year of nickel hydroxide product, a figure that is technically consistent with the contained-metal targets once the hydroxide product's composition is accounted for. Both numbers describe the same production plan measured at different points in the value chain.

Current Development Stage

As of mid-2026, the Brazilian Nickel Brejo Seco project in Piauí remains in the pre-final investment decision (pre-FID) and financing phase. The development pathway has progressed through demonstration-scale technical validation and environmental permitting stages, with first commercial production targeted for 2028 based on TechMet's most recent public disclosures.

The extended geological study history provides an unusual degree of permitting confidence. Regulatory bodies reviewing a project with five decades of site-specific data face a materially different information environment than they would with a greenfield discovery, and this reduces one of the most unpredictable variables in laterite project timelines.

ESG Credentials and the Nickel Mark Achievement

A First for Brazilian Mining

In a development that carries both symbolic and commercial weight, Piauí Níquel Metais, the operating entity for the Brejo Seco project, became the first mining site in Brazil to achieve The Nickel Mark certification at this stage of development. Administered by the Nickel Institute, The Nickel Mark is a third-party responsible production standard that evaluates environmental, social, and governance performance across a defined set of criteria.

This certification matters for several interconnected reasons:

- Western battery manufacturers and automakers operating under the EU Battery Regulation must increasingly demonstrate responsible sourcing across their supply chains

- The US Inflation Reduction Act creates financial incentives tied to supply chain provenance for battery materials

- Development finance institutions including export credit agencies are applying stricter ESG screens to project financing applications

- Offtake counterparties are paying premiums for verified ESG-compliant nickel supply, creating a direct commercial benefit beyond reputational value

Brejo Seco's combination of zero wet tailings, low CO₂ processing intensity, and third-party Nickel Mark certification positions it as one of the most ESG-differentiated pre-production nickel assets in the Western hemisphere.

The Simexmin presentation by Brazilian Nickel's geology team reinforced this positioning, emphasising that combining operational efficiency, technological innovation, and sustainability is not just aspirational for Brazilian mining — it is demonstrably achievable within the Brejo Seco framework.

Financing Structure and Strategic Investor Alignment

The US DFC Letter of Interest

The most significant financing development disclosed publicly is the US International Development Finance Corporation (DFC) letter of interest for up to USD $550 million in project financing. The DFC is the US government's development finance institution, and its engagement with critical mineral projects reflects Washington's broader strategic objective of reducing Western battery supply chain dependence on Chinese-controlled or geopolitically exposed supply sources. The broader battery metals investment landscape underscores precisely why institutions like the DFC are prioritising assets such as Brejo Seco.

Environmental review processes associated with DFC involvement have been completed, a procedural milestone that supports advancement toward a formal financing decision.

TechMet and Ecora Royalties

TechMet, the private critical minerals investment company that serves as Brazilian Nickel's strategic investor, has a notable structural characteristic: the US DFC is itself among TechMet's investors. This creates a vertically aligned financing and development structure where the same institution has strategic exposure at both the equity and debt levels of the project capital stack, an unusual configuration that reflects the depth of Western supply chain security interest in the asset.

Ecora Royalties, formerly known as Anglo Pacific Group, holds a royalty interest over the project. Ecora has indicated publicly that Brazilian Nickel continues working with financing partners and that a financing decision is expected post-2026. Royalty structures provide investors with leveraged upside to production volumes without direct operational responsibility, and Ecora's public reporting obligations create an additional transparency layer for observers tracking the project's progress.

The next major ASX story will hit our subscribers first

Brejo Seco Against the Global Laterite Landscape

Competitive Project Comparison

| Project | Country | Processing Method | Target Ni Production | Key ESG Factor | Status |

|---|---|---|---|---|---|

| Brejo Seco (Brazilian Nickel) | Brazil | Proprietary Heap Leach | ~27,000 t/y | Zero wet tailings, Nickel Mark | Pre-FID, 2028 target |

| Ramu (MCC) | Papua New Guinea | HPAL | ~33,000 t/y | Moderate | Operating |

| Taganito (Sumitomo) | Philippines | HPAL | ~30,000 t/y | Moderate | Operating |

| Weda Bay (Eramet/Tsingshan) | Indonesia | RKEF | ~50,000 t/y | Lower ESG profile | Operating |

| Jaguar (Centaurus Metals) | Brazil, Pará | Sulphide | TBD | High-grade sulphide | Development |

Brejo Seco's capital efficiency advantage over HPAL peers is meaningful. HPAL facilities for comparable nickel output have historically required capital expenditures in the range of USD $3 billion to USD $5 billion or more, while heap leach designs of equivalent scale are typically constructable at a fraction of that investment, even accounting for project-specific infrastructure requirements.

Brazil's regulatory environment and the DFC financing alignment also give Brejo Seco a geopolitical differentiation that Indonesian and Filipino projects structurally cannot replicate for Western-aligned offtake contracts.

Brazil's Broader Critical Minerals Context

A Country Awakening to Its Geological Inheritance

The Brazilian Nickel Brejo Seco project in Piauí sits within a larger Brazilian critical minerals story that is accelerating across multiple fronts. The country holds some of the world's largest assessed nickel laterite resources, yet has remained a minor producer relative to its endowment. In addition, the growing critical minerals demand tied to the global energy transition is further intensifying interest in Brazil's untapped resource base.

Simultaneously, rare earth developments are advancing in Mato Grosso, lithium projects are maturing in Minas Gerais, and sulphide nickel development in Pará is progressing through Centaurus Metals' Jaguar project. For context, a recent major nickel sulphide discovery elsewhere illustrates just how actively the global mining community is pursuing new nickel supply to meet battery demand.

What connects these developments is a convergence of improving ESG standards, Western financing interest, and growing domestic industrial policy focus on critical minerals as inputs for Brazil's own EV manufacturing ambitions. The country is positioning itself as a supplier not just to foreign battery chains but to its own emerging automotive electrification sector.

The outcome of Brejo Seco's financing process will serve as a meaningful reference point for the entire Brazilian laterite development pipeline. A successful FID and construction commencement would validate the heap leach technology at commercial scale, demonstrate the bankability of Brazilian laterite assets for international development finance, and signal to the market that a credible alternative to Indonesian supply is moving into production.

Brejo Seco Project: Key Parameters at a Glance

| Parameter | Detail |

|---|---|

| Location | Brejo Seco, Capitão Gervásio Oliveira, Piauí, Brazil |

| Deposit Type | Nickel-cobalt laterite |

| Processing Method | Proprietary heap leach |

| Planned Ore Throughput | ~3 million tonnes per year |

| Target Nickel Output | ~27,000 t/y (contained metal) |

| Target Cobalt Output | ~900 t/y (contained metal) |

| Tailings Profile | Zero wet tailings |

| ESG Certification | Nickel Mark (first in Brazil at this stage) |

| Key Investors and Partners | TechMet, US DFC (letter of interest: up to USD $550M) |

| Royalty Holder | Ecora Royalties |

| Target First Production | 2028 |

| Current Stage | Pre-FID and Financing Phase |

| Geological Study History | 50+ years |

Frequently Asked Questions

What is the Brejo Seco nickel project?

The Brejo Seco project is a nickel-cobalt laterite development in Piauí, northeastern Brazil, being advanced by Brazilian Nickel through its operating entity Piauí Níquel Metais. It uses proprietary heap leach technology validated at pilot-plant scale to produce nickel and cobalt hydroxide products targeting battery supply chains, with first commercial production aimed at 2028.

What makes the heap leach approach different from HPAL?

HPAL processes laterite ore under extreme temperature and pressure conditions, generating wet tailings and requiring very high capital investment. Brejo Seco's heap leach operates at ambient conditions, produces zero wet tailings, and requires materially lower capital expenditure, while still producing battery-grade nickel and cobalt hydroxide intermediates.

Who holds the financing interest in the project?

The US DFC has issued a letter of interest for up to USD $550 million in financing. TechMet serves as the strategic equity investor, and Ecora Royalties holds a royalty interest. A formal financing decision is anticipated post-2026 based on public disclosures from Ecora.

Why does the 50-year geological study history matter?

It translates directly into reduced technical and permitting risk. A project underpinned by five decades of drilling, sampling, and metallurgical test work carries a 3D geological model of exceptional resolution. This gives mine planners, financiers, and regulators an information base that dramatically narrows the range of operational uncertainty relative to younger or less-studied deposits.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding production targets, financing timelines, and project milestones are based on publicly available disclosures and are subject to change. Readers should conduct their own due diligence before making any investment decisions.

Want to Be First When the Next Major Battery Metals Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical battery metals like nickel and cobalt — instantly translating complex data into actionable opportunities for investors at every experience level. Explore historic discoveries and the returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.