May 23, 2026

China's latest battery recycling breakthrough represents one of the most significant advances in electrochemical engineering for extreme environments. Unlike conventional energy storage development that primarily optimises for room temperature performance, cold-weather battery systems must overcome fundamental molecular limitations that traditionally plague lithium-ion chemistry. The intersection of fluorinated electrolyte chemistry and semi-solid-state architectures creates new pathways for energy storage that function reliably across temperature ranges previously considered impossible for commercial deployment.

Understanding Fluorine-Based Electrochemical Systems

Molecular Foundation of Cold-Weather Performance

The electrochemical principles underlying China's cold-proof battery breakthrough centre on replacing traditional oxygen coordination frameworks with fluorine-based molecular structures. This represents a departure from conventional electrolyte design where oxygen atoms coordinate with lithium ions through relatively strong bonds that become increasingly restrictive at low temperatures.

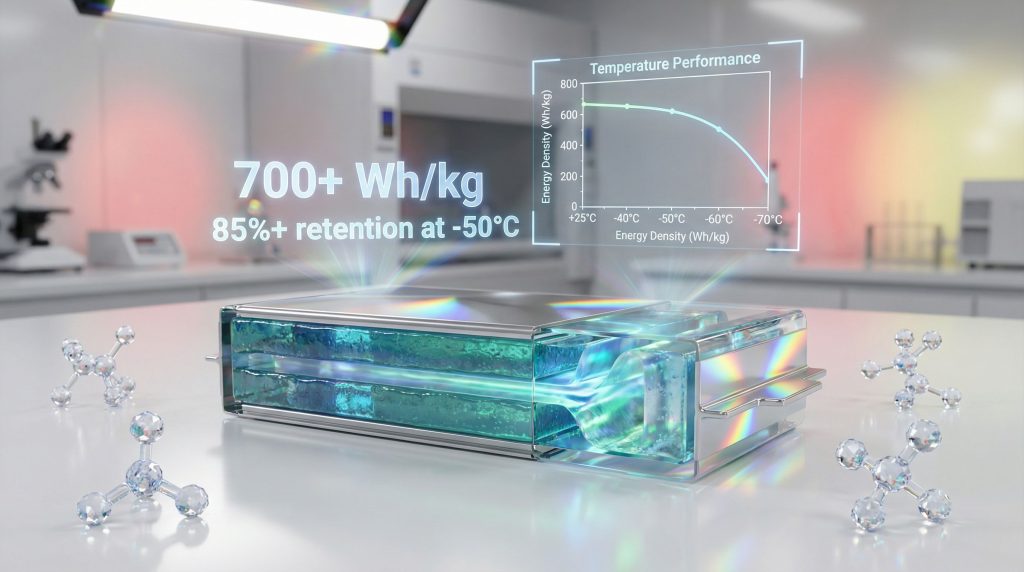

Key Performance Metrics:

- Energy density: Exceeding 700 Wh/kg at room temperature

- Cold-weather capacity: Approximately 400 Wh/kg at -50°C

- Operational threshold: Functional down to -70°C

- Capacity retention: 85%+ after 8 hours at extreme cold

The hydrofluorocarbon (HFC) system developed by researchers addresses the fundamental problem of ion mobility degradation. Traditional liquid electrolytes experience viscosity increases and ionic conductivity losses as temperatures drop below freezing. Furthermore, the fluorine coordination chemistry allows lithium ions to maintain faster release and transfer rates even under extreme cold conditions.

Semi-Solid-State Architecture Benefits

The semi-solid-state composition reduces reliance on flammable liquid components whilst maintaining the conductivity advantages of liquid systems. This hybrid approach provides several operational benefits:

- Enhanced fire resistance at elevated temperatures

- Reduced thermal runaway risk compared to pure liquid systems

- Maintained ionic conductivity in sub-zero conditions

- Improved mechanical stability during temperature cycling

Unlike fully solid-state batteries that can suffer from poor interfacial contact, the semi-solid design preserves adequate ion transport pathways. Consequently, this eliminates many safety concerns associated with volatile organic solvents whilst maintaining performance.

When big ASX news breaks, our subscribers know first

Industrial Manufacturing and Scale-Up Challenges

Production Engineering Requirements

Transitioning fluorinated electrolyte technology from laboratory demonstration to industrial scale presents significant manufacturing challenges. The synthesis of monofluorinated alkane solvents requires specialised chemical processing equipment designed for handling fluorinated compounds safely and efficiently.

Critical Manufacturing Elements:

- Fluorinated solvent synthesis with precise purity specifications

- Temperature-controlled assembly environments for electrolyte integration

- Quality assurance protocols for extreme-condition validation testing

- Specialised handling systems for semi-solid-state materials

The collaboration between Nankai University, Shanghai Institute of Space Power-Sources (SISP), and China Automotive New Energy Battery Technology Co. aims for limited mass production implementation by late 2026. However, this timeline reflects the complexity of scaling specialised chemistry from research-grade batches to commercially viable quantities.

Industrial Partnership Framework

The institutional collaboration model demonstrates how academic research institutions can integrate with commercial manufacturing partners. In addition, this approach bridges the gap between laboratory breakthroughs and market deployment by leveraging university research capabilities whilst accessing industrial manufacturing expertise and capital resources.

The partnership structure addresses several key development areas:

- Research and development coordination between institutions

- Technology transfer protocols for commercial implementation

- Quality control standardisation across production facilities

- Supply chain development for specialised fluorinated materials

Competitive Landscape Analysis

Solid-State Battery Development Timelines

The broader battery metals investment landscape reveals multiple competing approaches to next-generation energy storage. Solid-state batteries represent the most widely pursued alternative to conventional lithium-ion systems, with several major manufacturers targeting commercial deployment within similar timeframes.

Toyota's Strategic Approach:

- Target timeline: 2027-2028 commercial launch

- Performance specifications: 1,000+ km range with 10-minute charging

- Manufacturing partnerships: Collaboration with Idemitsu for solid electrolyte production

- Technology focus: Ceramic and polymer solid electrolytes

QuantumScape Performance Benchmarks:

- Cycle testing: Over 1,000 full charge/discharge cycles demonstrated

- Capacity retention: 95% after 1,000 cycles (exceeding 80% industry standard)

- Projected vehicle lifespan: 500,000+ kilometres without significant range degradation

- Technology foundation: Lithium-metal anode with ceramic solid electrolyte

Samsung SDI Production Timeline:

- Mass production target: 2027 for all-solid-state batteries (ASSBs)

- Range specifications: 600-mile capability

- Charging performance: 9-minute charging to 80% capacity

- Lifespan projections: 20-year operational life for premium vehicles

Alternative Chemistry Pathways

Beyond solid-state approaches, several other battery technologies compete for market adoption based on different performance priorities and cost considerations. For instance, direct lithium extraction technologies are revolutionising upstream production capabilities.

Silicon Anode Integration:

Silicon-based anodes replace traditional graphite materials to increase energy density by allowing greater lithium-ion storage capacity per unit volume. Amprius Technologies has demonstrated silicon anode systems capable of delivering 500+ Wh/kg energy density. Sila Nanotechnologies partners with Panasonic to implement silicon anode technology in existing production lines, representing a more evolutionary upgrade path compared to complete chemistry changes.

Lithium Iron Phosphate (LFP) Systems:

LFP batteries prioritise cost reduction and safety enhancement over maximum energy density. These systems eliminate nickel and cobalt from their chemical composition, addressing both material cost concerns and ethical mining considerations. Tesla has strategically adopted LFP technology for standard-range vehicles and energy storage applications.

Strategic Applications in Extreme Environments

Aerospace and Defence Applications

Cold-proof battery technology extends beyond passenger vehicle markets into specialised applications where reliable power storage under extreme conditions provides critical operational advantages. Spacecraft power systems represent one of the most demanding applications, where batteries must function reliably across the extreme temperature variations encountered in space environments.

Key Application Sectors:

- Deep-space mission power systems with extended operational requirements

- High-altitude drone operations in polar regions and stratospheric conditions

- Autonomous robotics for sub-Arctic industrial applications

- Emergency communication systems for disaster response in extreme weather

The aerospace sector particularly benefits from the high energy density characteristics, where weight minimisation directly impacts mission capabilities and launch costs. Moreover, the ability to maintain performance at -70°C addresses operational requirements for missions to Mars or outer planetary systems where conventional battery technologies would fail.

Industrial and Commercial Deployment

Industrial applications in cold climates represent significant market opportunities for specialised battery technologies. Forest fire prevention drone fleets operating in northern regions require reliable power systems that maintain performance during extended winter operations. Power grid inspection systems in Canadian and Scandinavian markets need batteries capable of functioning during extreme weather events when grid reliability becomes most critical.

Geographic Market Opportunities:

- Northern European transportation networks requiring cold-weather reliability

- Canadian and Alaskan commercial vehicle fleets

- Russian and Siberian industrial transportation systems

- Antarctic research station equipment and emergency backup power

The military and defence sectors present additional deployment opportunities where operational reliability under extreme conditions often outweighs cost considerations. Furthermore, cold-weather battery technology enables extended operational capabilities for equipment deployed in polar regions or high-altitude environments.

Global Market Impact and Economic Implications

Regional Adoption Strategies

The introduction of reliable cold-weather battery technology has the potential to accelerate electric vehicle adoption in regions previously considered unsuitable for battery-electric transportation. Northern European markets, which have historically relied on internal combustion engines due to cold-weather performance concerns, represent significant expansion opportunities.

Canadian and Alaskan transportation networks present unique challenges where conventional electric vehicles experience significant range reduction during winter months. The new cold-weather battery breakthrough could fundamentally alter the viability of electric commercial vehicles in these markets by maintaining 85%+ capacity retention at -50°C.

Market Penetration Factors:

- Infrastructure investment requirements for cold-weather charging networks

- Consumer adoption patterns in previously problematic climate zones

- Total cost of ownership improvements in extreme weather regions

- Insurance and warranty implications for extended temperature operation

Competitive Positioning Analysis

Chinese manufacturers developing fluorinated battery technology may achieve temporary competitive advantages through earlier commercialisation timelines compared to solid-state alternatives. The 2026 limited production target positions these systems ahead of most competing technologies targeting 2027-2028 commercial launches.

Western automaker response strategies likely include accelerated development partnerships, technology licensing agreements, and potential acquisition of specialised electrolyte chemistry companies. However, the intellectual property landscape surrounding fluorinated electrolyte systems will significantly influence market dynamics and technology access.

Strategic Considerations:

- Supply chain implications for specialised fluorinated materials

- Technology licensing revenue potential for research institutions

- Manufacturing localisation requirements in key markets

- Currency and trade policy impacts on global production

Technical Validation and Commercialisation Hurdles

What Are the Real-World Testing Requirements?

The transition from laboratory demonstration to commercial deployment requires extensive validation testing under actual operating conditions. Laboratory testing at controlled temperatures differs significantly from real-world scenarios involving temperature cycling, vibration, humidity variations, and other environmental stresses.

Critical Validation Areas:

- Long-term degradation patterns under repeated cold cycling

- Safety certification processes for semi-solid-state systems

- Thermal management system integration requirements

- Standardisation efforts for cold-weather battery specifications

Automotive safety certification presents particular challenges for new battery chemistries. Consequently, regulatory bodies must develop testing protocols specifically addressing fluorinated electrolyte safety characteristics, thermal runaway behaviour, and crash safety performance.

Manufacturing Scale-Up Challenges

Industrial-scale production of fluorinated electrolyte systems requires significant capital investment in specialised manufacturing equipment. The synthesis of monofluorinated alkane solvents demands chemical processing capabilities distinct from conventional battery manufacturing, including specialised storage, handling, and quality control systems.

Production Considerations:

- Specialised equipment for fluorinated solvent synthesis and purification

- Temperature-controlled assembly environments for electrolyte integration

- Workforce training requirements for advanced battery manufacturing

- Quality control systems for temperature-sensitive materials

The establishment of supply chains for specialised fluorinated materials represents another significant hurdle. Unlike conventional lithium-ion battery materials with established global supply networks, fluorinated electrolyte components may require development of entirely new supplier relationships and quality assurance protocols.

The next major ASX story will hit our subscribers first

Investment Implications and Market Projections

Near-Term Development Milestones

The 2026-2028 timeframe represents a critical period for China's cold-proof battery breakthrough commercialisation. Limited production validation and field testing will provide crucial performance data under real-world conditions, informing decisions about broader market deployment.

Key Milestones:

- Partnership expansion with major automotive manufacturers

- Regulatory approval processes in key global markets

- Cost reduction strategies through manufacturing optimisation

- Technology transfer and licensing opportunity development

Investment opportunities during this validation period may focus on companies developing specialised materials, manufacturing equipment, or testing capabilities for fluorinated electrolyte systems. In addition, the semiconductor industry's experience with fluorinated chemistry provides potential technology transfer opportunities.

Long-Term Market Transformation Potential

The successful deployment of cold-weather battery technology could fundamentally alter global electric vehicle market dynamics by eliminating geographic limitations on battery-electric transportation. This expansion could accelerate the transition away from internal combustion engines in previously challenging markets.

Transformation Scenarios:

- Integration with autonomous vehicle platforms for all-weather operation

- Expansion into commercial and industrial vehicle segments

- Global supply chain establishment and manufacturing localisation

- Technology standardisation and cross-platform compatibility development

The broader implications extend beyond transportation to include stationary energy storage applications in cold climates, backup power systems for critical infrastructure, and specialised equipment for extreme environment operations. Furthermore, advances in battery-grade lithium production and pure lithium batteries revolution complement these developments.

The integration of advanced battery technologies with China's cold-proof battery breakthrough represents a paradigm shift in energy storage capabilities. This convergence positions the technology to address previously insurmountable challenges in extreme environment applications.

Disclaimer: This analysis is based on publicly available information and industry reports. Battery technology development involves significant technical and commercial risks. Performance claims should be validated through independent testing. Investment decisions should consider multiple factors beyond individual technology developments. Market projections are speculative and subject to significant uncertainty based on technological, regulatory, and competitive developments.

Could Cold-Weather Battery Breakthroughs Signal the Next Mining Boom?

China's revolutionary battery technology requiring specialised fluorinated materials could trigger substantial demand for previously overlooked mineral deposits in extreme environments. Discovery Alert's proprietary Discovery IQ model instantly identifies emerging opportunities in battery metals and rare earth discoveries, delivering real-time alerts when ASX companies announce breakthroughs that could capitalise on this technological shift. Explore historic discovery returns that demonstrate how early identification of game-changing mineral announcements creates exceptional investment opportunities, then begin your 14-day free trial today.