June 13, 2026

The Processing Bottleneck That Makes or Breaks U.S. Rare Earth Ambitions

For decades, the rare earth industry has operated under a peculiar paradox: the United States sits atop substantial domestic reserves of the very materials it depends on for defence systems, electric vehicles, and clean energy infrastructure, yet it remains structurally dependent on foreign processing capacity to transform those reserves into usable products. This is not primarily a mining problem. It is a separation and processing problem, and it is the lens through which the Bear Lodge rare earth project FAST-41 permitting milestone must be understood.

The geology was never the bottleneck. The regulatory calendar, and the absence of domestic hydrometallurgical infrastructure capable of producing magnet-grade rare earth oxides at commercial scale, have always been the rate-limiting factors. Bear Lodge, a high-grade carbonatite-hosted rare earth deposit in northeastern Wyoming, is now advancing on both fronts simultaneously, and the timing of each workstream relative to the other will define the project's commercial trajectory through the end of this decade.

When big ASX news breaks, our subscribers know first

Bear Lodge's Geological Advantage: Why Grade and Mineralogy Both Matter

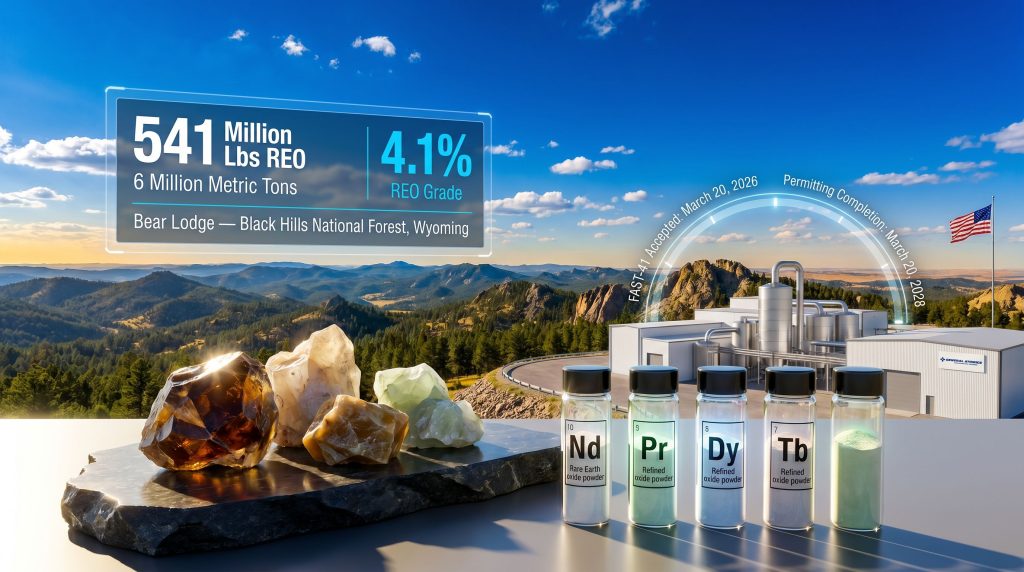

Not all rare earth deposits are equal, and grade alone tells only part of the story. Bear Lodge's measured and indicated resource totals 6 million metric tons averaging 4.1% rare earth oxides (REO), containing a total of 541 million pounds of rare earth oxides. By global hard-rock rare earth standards, this places the deposit in the upper tier for resource grade.

What elevates Bear Lodge beyond a simple volume story, however, is its mineralogical profile. The deposit is hosted in carbonatite intrusions within the Black Hills region of northeastern Wyoming, approximately 25 miles north of the town of Upton. Carbonatite-hosted rare earth systems are globally significant because they can concentrate rare earths to exceptional grades, but their economic value depends heavily on which rare earths dominate the mineral assemblage.

Bear Lodge is notably enriched in the four rare earths that command the highest market premiums and carry the greatest strategic significance:

- Neodymium (Nd) and praseodymium (Pr): The principal inputs for neodymium-iron-boron (NdFeB) permanent magnets, combined and sold commercially as NdPr oxide

- Dysprosium (Dy) and terbium (Tb): Heavy rare earths used in relatively small but critical quantities to improve magnet performance at high temperatures, essential for EV motors and aerospace applications

This magnet-critical enrichment distinguishes Bear Lodge from deposits that are grade-rich but skewed towards cerium and lanthanum, which carry substantially lower market values and face persistent oversupply challenges. A deposit rich in cerium may look impressive on a contained-REO basis but generate far less revenue per tonne processed. Furthermore, Bear Lodge's chemistry aligns directly with where demand is actually growing.

The four magnet rare earths (Nd, Pr, Dy, Tb) represent a small fraction of global rare earth production by volume but account for a disproportionately large share of market value, given their irreplaceable role in high-performance permanent magnet manufacturing.

Understanding FAST-41: What Federal Permitting Coordination Actually Delivers

The Federal Permitting Improvement Steering Council's FAST-41 programme, established under Title 41 of the Fixing America's Surface Transportation Act, is frequently mischaracterised in industry commentary. It does not eliminate environmental review obligations, compress substantive scientific analysis, or provide project-specific government endorsement. What it does provide is something that has historically been equally scarce in U.S. mining permitting: predictability and inter-agency coordination.

Large resource projects requiring approvals from multiple federal agencies have historically suffered from sequential review processes in which one agency's delay cascades into another's timeline. FAST-41 addresses this by establishing a binding coordinated schedule, publicly documented on the Federal Permitting Improvement Steering Council's portfolio, that holds all participating agencies to synchronised milestones. This framework sits at the heart of broader U.S. critical minerals policy aimed at rebuilding domestic supply chains.

Bear Lodge FAST-41 Key Milestones at a Glance

| Milestone | Detail |

|---|---|

| FAST-41 Acceptance | March 20, 2026 |

| Lead Federal Agency | U.S. Forest Service (USFS) |

| Mine Site Land Status | Black Hills National Forest |

| Estimated Permitting Completion | March 20, 2028 |

| Total Coordinated Review Period | Approximately 24 months |

The U.S. Forest Service carries primary responsibility as the lead agency due to the mine's location on Black Hills National Forest lands. The NEPA environmental review process sits at the centre of this timeline, and its completion is a prerequisite to USFS approval of the Bear Lodge rare earth project Mine Plan of Operations.

Additional agencies with potential review roles include:

- The U.S. Army Corps of Engineers, which may have jurisdiction over water resource impacts

- The Nuclear Regulatory Commission (NRC), which may require a source material licence for processing operations given the naturally occurring radioactive material content typical of rare earth ores

- Wyoming state agencies, covering mining permits, air quality, water discharge, and industrial siting approvals for the planned processing facility on private land approximately 40 miles from the mine

The separation of the mine site (federal land) from the processing facility (private land, near Upton) creates a bifurcated jurisdictional structure that partly insulates the processing facility from some federal review requirements while maintaining separate state-level permitting obligations.

A 24-month federal permitting timeline is considered exceptionally predictable by U.S. hard-rock mining standards, where permitting timelines have historically extended beyond a decade for projects of comparable complexity.

The Demonstration Plant: Risk Reduction Before Capital Commitment

The Upton demonstration plant represents one of the most strategically consequential facilities in the current U.S. rare earth development pipeline, precisely because it addresses the processing bottleneck rather than the mining one. Built to validate a proprietary rare earth separation technology developed in partnership with General Atomics, the facility is designed to produce high-purity neodymium-praseodymium oxide (NdPr oxide) at pre-commercial scale.

General Atomics is not a conventional mining industry partner. The firm is primarily known for its work in defence systems, nuclear technology, and advanced energy research. Its involvement in rare earth separation technology development signals the degree to which rare earth processing challenges have become a national security-adjacent industrial problem, attracting partners with deep technical capabilities outside the traditional mining sector.

The demonstration plant's core objectives are:

- Validate the proprietary separation process at a scale sufficient to generate engineering, operational, and economic data

- Identify and resolve mechanical and process challenges before capital is committed to a full commercial facility

- Produce high-purity NdPr oxide samples for potential customer qualification testing

- Generate the technical foundation required to support project financing and offtake negotiations

Commissioning Challenges: What the Filtration Issues Actually Signal

As of mid-2026, steady-state operations at the Upton plant have not yet been achieved, with commissioning encounters including supply chain disruptions and filtration inefficiencies in the primary processing circuit. The filtration challenge is worth examining in technical context.

In rare earth hydrometallurgical processing, the front-end circuit typically involves crushing, grinding, and flotation or leaching to produce a rare earth concentrate that feeds downstream separation circuits. Filtration efficiency at this stage directly controls the quality and consistency of the concentrate feed entering the solvent extraction or ion exchange separation systems. Inconsistent filtration performance can result in feed variability that destabilises separation circuit chemistry, producing off-specification product or reducing overall recovery.

The fact that most major systems have been successfully commissioned, with the current critical path focused on front-end circuit optimisation rather than fundamental process redesign, is a materially important distinction. It suggests the separation technology itself is not under question, and that the commissioning work remaining is operational refinement rather than engineering rethinking.

As Rare Element Resources CEO Ken Mushinski has communicated publicly, the resolution of these front-end challenges is understood as the de-risking function a demonstration plant is specifically designed to perform, with the intent that optimisation work completed now will reduce commercial-scale execution risk substantially. (Metal Tech News, June 2026)

Resolution of filtration inefficiencies and achievement of steady-state operations is targeted for late summer 2026.

The Timeline Convergence: Why 2027 Is the Critical Year

The relationship between the demonstration plant campaign and the FAST-41 permitting timeline creates a structural dependency that investors and industry observers should understand clearly.

The planned 12-month demonstration campaign cannot commence until steady-state operations are achieved. With steady operations targeted for late summer 2026, the campaign completion window falls in approximately mid-to-late 2027, assuming no further operational delays. Federal permitting is scheduled for completion in March 2028.

This alignment provides limited but real buffer between demonstration completion and permitting conclusion, with perhaps six to nine months of overlap in the current projected scenario. The risk scenario is straightforward: further delays in achieving steady operations at Upton compress or eliminate this buffer, potentially leaving the project in a position where federal mine authorisation has been granted before a commercial processing pathway has been technically and economically validated.

Timeline Sensitivity Analysis

| Scenario | Steady Ops Achieved | Campaign Completes | Buffer vs. March 2028 Permitting |

|---|---|---|---|

| Base Case | Late Summer 2026 | Mid-to-Late 2027 | ~4-8 months |

| Mild Delay | Q4 2026 | Late 2027 to Q1 2028 | Minimal |

| Significant Delay | Q1 2027 | Q1-Q2 2028 | None / Negative |

Note: Timeline projections are illustrative estimates based on publicly disclosed target dates. Actual outcomes will depend on operational performance at the Upton facility.

NdPr Oxide and the China Dependency: Understanding the Commercial Stakes

The downstream market context for Bear Lodge's primary product is important for framing why the demonstration plant timeline carries commercial urgency beyond internal project milestones. Indeed, understanding the broader rare earth supply chain context is essential for appreciating why this project matters.

China currently controls an estimated 85-90% of global rare earth separation and processing capacity, a dominance built over several decades through coordinated industrial policy, low-cost production, and systematic investment in hydrometallurgical expertise. This concentration creates a structural bottleneck that affects even countries with significant domestic rare earth mining operations: without separation capacity, mined ore or concentrate must be shipped offshore for processing, leaving the strategic value-add in foreign hands.

NdPr oxide is the foundational input for NdFeB permanent magnets, which are irreplaceable components in:

- Electric vehicle traction motors (a single EV motor typically contains approximately 1-2 kg of NdFeB magnet material)

- Direct-drive offshore wind turbine generators, which can require up to 600 kg of rare earth magnets per megawatt of installed capacity

- Defence systems including missile guidance, radar arrays, and autonomous vehicle platforms

- Industrial robotics, precision motion systems, and MRI medical imaging equipment

The absence of commercial-scale U.S. rare earth separation capacity is not a theoretical policy concern. It is an operational reality that currently forces domestic downstream manufacturers to source separated rare earth materials through channels that run through, or are priced relative to, Chinese production. Bear Lodge's commercial processing plant, if successfully demonstrated and constructed, would represent one of the very few facilities in the Western world capable of producing NdPr oxide from domestically mined feedstock.

The next major ASX story will hit our subscribers first

Comparing Bear Lodge to the U.S. Rare Earth Development Landscape

| Project | Location | Resource Scale | Magnet REE Enrichment | Processing Status |

|---|---|---|---|---|

| Bear Lodge | Wyoming | 541M lbs REO, 4.1% grade | High (Nd, Pr, Dy, Tb) | Demo plant commissioning |

| Mountain Pass | California | Operating | Moderate | Producing (concentrate exported) |

| Round Top | Texas | Large tonnage, lower grade | Lower magnet REE intensity | Pre-permitting |

| Halleck Creek | Wyoming | Large tonnage | NdPr enriched | Resource/exploration stage |

Note: Table reflects publicly available information as of mid-2026. Comparative assessments are based on publicly disclosed resource and development data.

Mountain Pass, operated by MP Materials, is the only currently producing rare earth mine in the United States, but has historically shipped concentrate to China for separation, though domestic processing capacity is being developed. Bear Lodge's combination of high grade, magnet-critical mineralogy, and an in-house proprietary separation technology positions it as a structurally differentiated development-stage asset within this landscape. In addition, the broader rare earth geopolitics driving investment in projects like Bear Lodge continue to intensify as Western nations reassess supply chain vulnerabilities.

Key Risks Investors and Industry Observers Should Monitor

Permitting risk under FAST-41 is reduced relative to historical U.S. mining timelines but is not eliminated. NEPA review outcomes remain unpredictable in their conclusions, and USFS Mine Plan of Operations approval involves substantive environmental and land management considerations specific to Black Hills National Forest.

Technology demonstration risk is currently concentrated in the filtration optimisation challenge at Upton. If front-end circuit performance cannot be stabilised by late summer 2026, the campaign timeline compresses towards the March 2028 permitting milestone with decreasing buffer.

Market risk is material for NdPr oxide, a commodity subject to significant price volatility driven by Chinese export policy decisions, EV production ramp trajectories, and shifts in magnet manufacturing capacity outside China. NdPr oxide prices have historically been capable of multi-year cycles that can alter project economics substantially.

Financing risk for the transition from demonstration to commercial-scale processing facility is significant. The capital requirements for a commercial separation plant are substantial, and project financing will depend on the strength of demonstration campaign outcomes, the availability of offtake agreements, and the continued relevance of federal financing mechanisms aligned with domestic critical mineral strategy objectives.

This article contains forward-looking projections and analysis based on publicly available information. It does not constitute financial advice. Readers should conduct independent due diligence before making investment decisions.

Milestones to Watch Through 2028

Near-term (2026):

- Filtration circuit resolution and commencement of steady-state operations at Upton

- Launch of the 12-month demonstration campaign

- Initial NdPr oxide sample production for customer qualification

Medium-term (2027):

- Completion of NEPA environmental review under USFS coordination

- Demonstration campaign conclusion and compilation of commercial feasibility data

- Progress on Wyoming state permitting requirements

- Advancement of customer qualification and preliminary offtake discussions

Late-stage (2028):

- Federal permitting completion (estimated March 20, 2028)

- Capital decision on commercial processing facility construction

- Potential integration into broader U.S. domestic rare earth supply chain architecture

The Bear Lodge rare earth project FAST-41 permitting timeline has provided the project with something genuinely rare in U.S. critical minerals development: a predictable federal review schedule. Whether the demonstration plant can deliver validated separation technology within the window that schedule creates is the defining question of the next 18 months.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across rare earths and critical minerals, instantly translating complex data into actionable investment insights for traders and long-term investors alike — start your 14-day free trial today and explore why historic discoveries have generated extraordinary returns for those who acted early.