July 17, 2026

The Concentrate Market Is Being Redrawn From the Inside Out

There is a structural shift underway in global copper markets that goes far beyond cyclical supply disruptions or short-term price moves. For decades, the relationship between copper miners and smelters was relatively stable: miners produced concentrate, smelters processed it, and treatment and refining charges (TC/RCs) served as the negotiated price of that arrangement. Today, that relationship is being actively dismantled by grade deterioration, technology investment, and a new generation of vertically integrated processing strategies. The BHP copper concentrates market outlook for FY26 and beyond sits squarely at the centre of this transformation.

BHP's July 2026 operational review is not simply a set of production numbers. It is a detailed map of where concentrate supply is heading, how major miners are responding to geological reality, and why third-party smelters may face an increasingly challenging decade ahead.

When big ASX news breaks, our subscribers know first

FY26 Production Numbers and What They Conceal

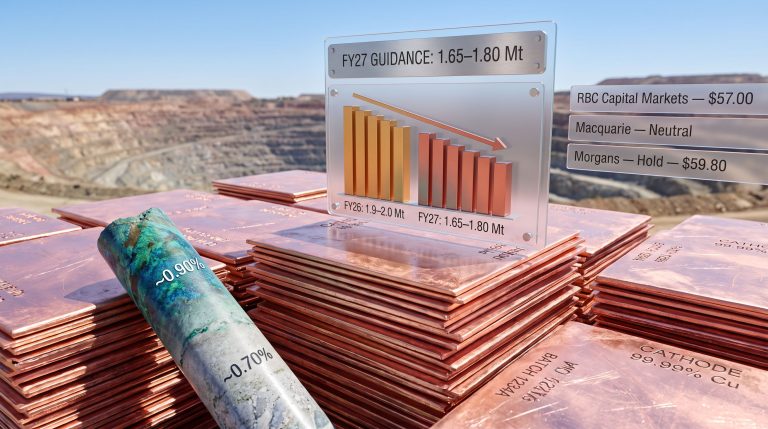

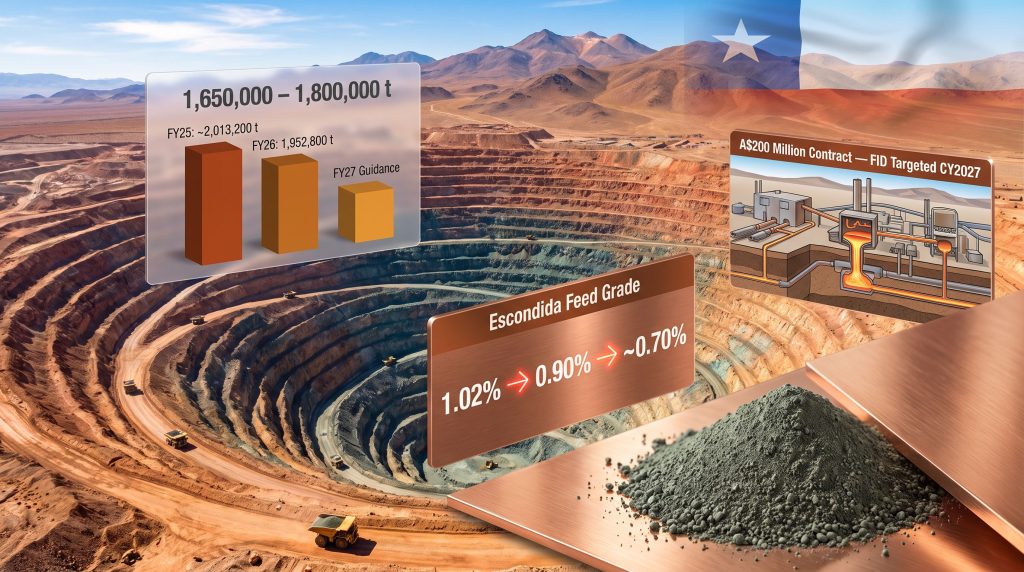

At face value, BHP delivered another year of roughly 2 million tonnes of group copper production. The headline figure of 1,952,800 tonnes in FY26 looks broadly steady against FY25's approximately 2,013,200 tonnes, a decline of around 3% year on year. However, that surface-level stability masks significant underlying deterioration that will become far more visible in FY27.

The company also achieved record iron ore production in the same period, which is a useful operational context. High throughput and record material mined at Escondida generated headlines, but payable copper in concentrate from that operation still fell 7% to 1,046,800 tonnes in FY26. This is the critical distinction that investors and smelter counterparties need to understand: throughput records do not equate to concentrate volume records when ore grade is declining faster than operational efficiency improvements can compensate.

| Metric | FY25 | FY26 | FY27 Guidance |

|---|---|---|---|

| Group Copper Production (tonnes) | ~2,013,200 | 1,952,800 | 1,650,000–1,800,000 |

| Escondida Feed Grade | 1.02% | 0.90% | ~0.70% |

| Escondida Payable Cu in Concentrate | ~1,124,500 | 1,046,800 | 1,000,000–1,100,000 |

| Spence Payable Cu in Concentrate | ~149,800 | 121,300 | Part of 210,000–230,000 total |

| Copper SA Production (tonnes) | ~316,000 | 320,700 | 290,000–320,000 |

FY27 guidance of 1,650,000 to 1,800,000 tonnes represents a potential decline of up to approximately 15% from FY26 levels. That is a material step-down for a single mining group operating the world's largest copper mine.

Escondida's Grade Problem Is Structural, Not Temporary

Escondida's concentrator feed grade trajectory tells a story that few in the market have fully priced in. The decline from 1.02% in FY25 to 0.90% in FY26 and a forecast ~0.70% in FY27 represents a cumulative deterioration of roughly 31% in just two years. This is not a processing inefficiency that can be engineered away. It reflects the geological reality of mining progressively deeper and lower-grade ore within a maturing porphyry copper system.

Porphyry deposits, which account for the majority of global copper production, are characterised by large, disseminated ore bodies with gradational grade profiles. As mining advances through the higher-grade zones that typically exist closer to the mineralising intrusion, operations must process increasingly larger volumes of ore to maintain equivalent metal output. This drives up energy consumption, reagent usage, and water demand per tonne of copper produced, compressing operating margins even as nominal throughput records are set. These challenges are further compounded by the broader copper supply crunch affecting the global industry.

Industry Context: The grade decline challenge at Escondida is symptomatic of a broader systemic trend across the world's major copper deposits. The average ore grade processed by the global copper industry has fallen from around 1.8% in 2000 to below 0.6% in some regions today, according to long-term industry tracking data.

BHP acknowledged that FY26 performance was supported by new reagent introductions that improved metallurgical recovery rates. This represents a genuine operational achievement. Advanced flotation reagent chemistry, including the use of collector blends tailored to sulphide mineralogy, can meaningfully improve copper recovery from complex or lower-grade feeds. However, these techniques have diminishing marginal returns as ore bodies mature, and they cannot substitute for the sheer volume of contained metal that higher grades provide.

Spence: Two Technology Bets That Signal a Cathode-First Future

The sanctioning of two capital projects at BHP's Spence (Pampa Norte) operation in Chile in June 2026 deserves careful analysis, because these investments reveal a deliberate strategic intent that extends well beyond Spence's own production numbers. Furthermore, the Chile copper outlook suggests these investments are timed to capitalise on structurally higher prices through the decade.

Project 1: Spence Concentrator Upgrade Recovery Project

This project upgrades the existing flotation circuit to extend residence time, allowing ore particles more contact time with reagents and improving copper recovery rates into concentrate. First production is expected in FY28. While technically straightforward, extended residence time modifications can deliver meaningful recovery improvements, particularly in ores with fine-grained or complex sulphide mineralogy.

Project 2: Spence Chalcopyrite Leaching Project (SAL2 Technology)

This is the more strategically significant of the two. BHP's proprietary Simple Approach to Leaching 2 (SAL2) technology targets hypogene ores, which are primary sulphide mineralisation types found at depth in porphyry systems. Historically, hypogene ores could only be processed through flotation to produce concentrate. SAL2 is designed to leach these sulphide ores directly into solution, allowing copper to be recovered as cathode through conventional solvent extraction and electrowinning (SX-EW) circuits. First cathode production is expected in CY28.

Why This Matters for the Concentrate Market: If SAL2 technology is successfully scaled at Spence, a portion of Chilean copper production that would otherwise flow into the concentrate supply chain will instead be produced as cathode, bypassing third-party smelters entirely. This is a direct structural reduction in concentrate availability, not a cyclical one.

Spence payable copper in concentrate fell 19% to 121,300 tonnes in FY26, with total copper output declining 21% to 212,600 tonnes. FY27 guidance is 210,000 to 230,000 tonnes total, suggesting the volume trough is near but the pathway to recovery runs through technology rather than grade improvement alone.

Carrapateena and the Fragility of Integrated Mining Systems

The unplanned failure of an underground conveyor belt at the Carrapateena mine in South Australia in July 2026 is a case study in how infrastructure dependencies amplify disruption risk within hub-and-spoke mining systems. The incident required a full belt replacement and is expected to cause up to eight weeks of lost mine production, directly affecting BHP's Copper South Australia production guidance for FY27, which was revised to 290,000 to 320,000 tonnes from 320,700 tonnes in FY26.

Carrapateena feeds into the centralised Olympic Dam smelter and refinery alongside Prominent Hill and Olympic Dam itself. This architecture, while operationally efficient under normal conditions, creates a situation where a single point of failure at any one mine affects the entire processing hub's throughput optimisation. The mining industry has seen repeated examples of this dynamic in recent years:

- The Cobre Panama closure removed a significant source of concentrate from the global market

- Weather-related disruptions at Chilean ports have caused cascading effects on spot TC negotiations

- Conveyor and shaft infrastructure failures at underground mines have historically caused outsized production impacts relative to their immediate physical scope

Olympic Dam Expansion: Processing Power as Competitive Advantage

The most strategically consequential element of BHP's FY26 operational review may be the progress on the Olympic Dam smelter and refinery expansion. On July 9, 2026, BHP awarded a design and supply contract valued at over A$200 million (approximately US$130 million) to China Nerin Engineering for key processing facilities. The contract will be executed in stages, with a potential final investment decision (FID) targeted for CY2027.

The expansion targets are substantial:

- Production growth to 500,000 tonnes per year through the 2030s

- Potentially 650,000 tonnes by end of decade

- Up from approximately 316,000 tonnes in FY25

The strategic logic is straightforward: by processing concentrate from all three South Australian mines in-house, BHP eliminates the TC/RC payments that currently flow to third-party smelters, recovers a greater proportion of valuable by-products (including uranium, gold, and silver from Olympic Dam's unique polymetallic ore body), and reduces transport costs associated with shipping concentrate to smelters in Asia. Copper smelting expansion of this kind reflects a broader industry pivot towards integrated processing as a strategic margin lever.

BHP's former CEO Mike Henry articulated the rationale at the company's half-year results briefing in February 2026, stating that expanding the smelter and refinery would allow the company to extract more value by recovering more by-products and avoiding the need to pay TC/RC upside to external processors. This framing positions vertical integration not merely as a cost management exercise but as a margin capture strategy in an environment where copper prices have risen sharply.

Market Question Worth Asking: Does additional Western smelting capacity meaningfully loosen the concentrate market, or does it simply relocate the bottleneck? This question, raised by a Latin America mining consultant in the market, captures the central tension. BHP processing more of its own concentrate in-house does not add to global smelting capacity in the way a new standalone smelter would. It effectively withdraws concentrate from the open market while adding refined copper supply.

The next major ASX story will hit our subscribers first

Treatment Charges at Negative Territory: A Historic Inversion

No single metric captures the state of the BHP copper concentrates market outlook more starkly than the current level of treatment charges. Fastmarkets calculated the weekly copper concentrates TC index, CIF Asia Pacific, at $(166.50) per tonne on July 10, 2026, a decline of $4.50 per tonne (2.78%) from $(162.00) per tonne the prior week.

Negative TC values represent a complete inversion of the traditional mining-smelting commercial relationship. Under normal market conditions, miners pay smelters a processing fee to convert concentrate into refined metal. When TCs go negative, smelters are effectively paying miners a premium to secure concentrate supply. This reflects a market where smelting capacity additions have outpaced concentrate supply growth, creating intense competition among smelters for available material.

| Driver | Impact on TC/RC Direction |

|---|---|

| Escondida grade decline | Reduces concentrate volumes, depresses TCs |

| New Chinese smelting capacity | Intensifies smelter competition for limited supply |

| Cobre Panama closure | Removes a major concentrate source from the market |

| BHP in-house processing expansion | Reduces third-party concentrate availability over time |

| Spence production decline (−19% FY26) | Further reduces Chilean export volumes |

The refined copper market is expected to remain broadly balanced or in marginal surplus near term, supported by strong Chinese smelting output. However, the concentrate market faces a structurally different dynamic, with supply growth unable to keep pace with smelting capacity additions. This bifurcation between the refined copper market and the concentrate market is increasingly important for participants on both sides of the value chain. The copper price drivers underpinning this divergence are likely to persist well into the next decade.

Antamina's Record and the Wheaton Silver Deal

BHP's 33.75% share in the Antamina polymetallic mine in Peru delivered a financial-year record of 151,500 tonnes of payable copper in concentrate in FY26, up 27% year on year, driven by higher feed grades and improved operational performance. However, zinc production fell to 96,127 tonnes due to lower feed grades through the same period.

FY27 guidance reflects a planned reversion to lower feed grades: 120,000 to 140,000 tonnes copper and 35,000 to 55,000 tonnes zinc. The FY26 outperformance was partly a function of mine sequencing through higher-grade zones, which is a common dynamic at polymetallic skarn deposits where different ore domains carry very different metal ratios.

Separately, BHP announced a US$4.3 billion silver streaming agreement with Wheaton Precious Metals covering BHP's share of Antamina's future silver production. Streaming agreements of this type are an important financing tool in the mining sector. A streaming company provides an upfront capital payment in exchange for the right to purchase future by-product metal at a pre-agreed fixed price, typically well below spot market levels. For BHP, this transaction monetises a non-core by-product stream at a premium to its value in the ground while generating capital available for redeployment into copper growth assets. You can explore BHP's copper growth strategy in greater detail through the company's own dedicated resources.

Vicuña and the Long Pipeline of Future Supply

The Vicuña joint venture between BHP and Lundin Mining secured a landmark regulatory milestone in June 2026, receiving approval for inclusion in Argentina's Incentive Regime for Large Investments (RIGI) under the Long-Term Strategic Export Projects designation. Vicuña was the first mining project to receive this designation, which provides 40 years of fiscal certainty covering the Josemaria and Filo del Sol deposits in the Atacama region of Argentina.

A Stage 1 final investment decision is targeted for CY2026, with first production from the copper-gold-silver project potentially commencing in CY2030. Vicuña represents a meaningful future addition to the global concentrate supply pipeline, but it remains a decade-horizon consideration for market balance purposes.

Portfolio Rationalisation and Technology-Led Cathode Growth

BHP's portfolio management activity in FY26 signals a clear preference for high-quality, large-scale assets with processing integration potential. The divestment of the Carajás copper operation in Brazil was completed on April 2, 2026, concentrating capital and management attention on Tier 1 assets.

Two additional growth options advanced during the period:

- An Environmental Impact Assessment (EIA) submitted in June 2026 for a potential 20-year restart of the idled Cerro Colorado operation in northern Chile, which would use chloride-leaching technology to produce copper cathode directly, again bypassing the concentrate supply chain

- A memorandum of understanding signed between Spence and Sierra Gorda SCM to explore commercial collaboration on efficiency and long-term competitiveness for the two adjacent Chilean operations, the specific scope of which has not been disclosed

Both developments reinforce the same overarching theme: BHP is systematically expanding its capability to produce copper without generating concentrate, reducing its dependence on smelter relationships and the volatility of TC/RC negotiations.

The Decade-Long Supply-Demand Trajectory

Synthesising the operational data from BHP's FY26 results with broader industry fundamentals produces a coherent picture of where the copper concentrates market is heading through the early 2030s.

| Period | Market Condition | Primary Dynamic |

|---|---|---|

| CY2024–CY2025 | Marginal refined surplus; concentrate very tight | New Chinese smelting capacity absorbing limited concentrate |

| FY2026 | Broadly balanced refined market; concentrate extremely tight | Grade declines, Cobre Panama absence, smelter competition |

| Late 2020s | Structural concentrate deficit emerging | Supply growth outpaced by demand and in-house processing |

| 2030s | Durable copper price outperformance expected | ~10Mt supply gap requires significant new mine development |

Global copper demand is projected to grow by approximately 70% by 2050, anchored by electrification infrastructure, renewable energy deployment, and electric vehicle adoption. The world is estimated to require roughly 10 million tonnes of new copper supply to balance demand by 2035. Consequently, the BHP copper concentrates market outlook points to a prolonged period of tightness that no single operational adjustment can resolve. Against this backdrop, every tonne that moves from the concentrate supply chain into in-house cathode production effectively tightens the external market further. BHP's own economic outlook details how the company is positioning for this structural shift across its portfolio.

Disclaimer: This article contains forward-looking statements, production forecasts, and market projections drawn from publicly available company announcements and industry data. These statements involve inherent uncertainty and should not be construed as financial advice or a recommendation to buy or sell any security. Past production performance and pricing trends do not guarantee future outcomes. Readers should conduct independent research and seek professional advice before making investment decisions.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex geological and commodity data into actionable investment insights — explore historic discoveries and their exceptional returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market as structural copper tightness deepens through the decade.