July 17, 2026

Ore Grades, Output Ceilings, and the Uncomfortable Truth About Copper Supply

There is a geological reality that underpins every copper price forecast, every energy transition model, and every mining valuation: ore bodies do not improve with age. The world's largest copper mines are, by definition, the ones that have been mined the longest. And the longer a deposit is exploited, the deeper you dig and the leaner the rock becomes. This is not a theory. It is the irreversible physics of mineral extraction, and it is now playing out in real time at the asset that matters most to global copper supply.

Understanding this dynamic is essential context for interpreting what BHP copper guidance misses expectations actually reveals. This is not a story about a bad quarter. It is a story about where the world's most strategically important copper mine sits on its depletion curve, and what that means for a metal that every electrification scenario on earth is betting on.

When big ASX news breaks, our subscribers know first

Decoding the FY27 Numbers: What the Guidance Actually Says

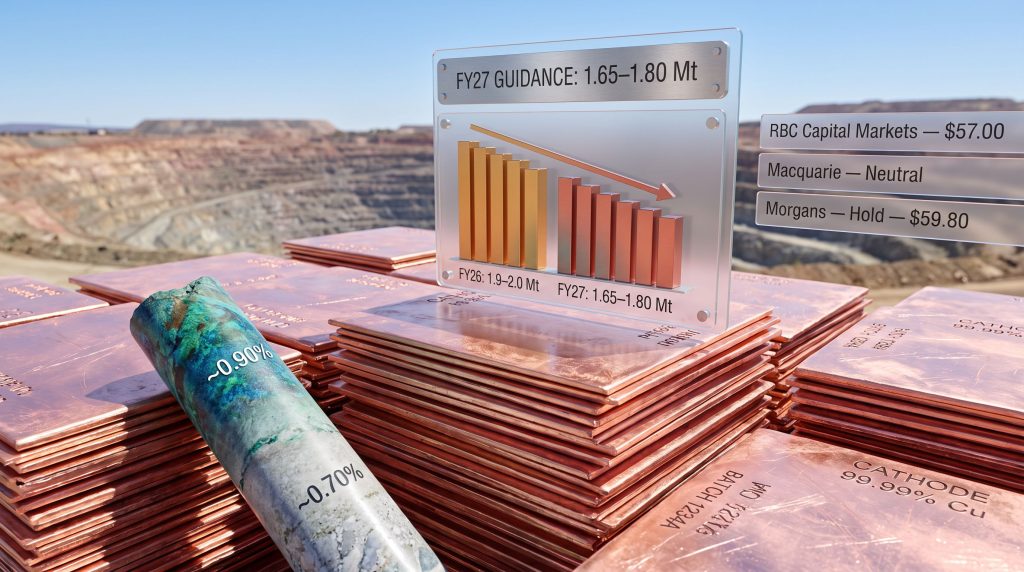

BHP's FY27 group copper production guidance of 1.65 to 1.80 million tonnes landed well below what the market had positioned for. The comparison to FY26 guidance of 1.9 to 2.0 million tonnes reveals a contraction of roughly 15% at the midpoint, a magnitude that cannot be dismissed as normal operational noise.

| Metric | FY26 | FY27 |

|---|---|---|

| Group Copper Guidance | 1.9 to 2.0 Mt | 1.65 to 1.80 Mt |

| Midpoint Comparison | ~1.95 Mt | ~1.725 Mt |

| Q4 Actual Output | 491.9 Kt | Not yet reported |

| Q4 Consensus Estimate | 492.7 Kt | Not applicable |

| Copper SA Guidance | Not provided | 290,000 to 320,000 t |

| Copper SA Consensus | Not provided | ~333,000 t |

| Escondida Feed Grade (est.) | ~0.90% | ~0.70% |

| Escondida Guidance Range | Not separately guided | 1.0 to 1.1 Mt |

The Copper SA guidance range of 290,000 to 320,000 tonnes came in significantly short of the 333,000 tonne consensus forecast tracked by RBC Capital Markets. That shortfall — a gap of roughly 13,000 to 43,000 tonnes depending on where in the range actual output lands — was the first signal that analyst models had not adequately priced in the operational pressures now bearing on BHP's South Australian copper portfolio.

Why Consensus Was So Far Off

Sell-side analysts build production models from throughput rates, historical recovery data, and disclosed mining plans. The challenge at Escondida is that grade depletion can occur faster than models anticipate, particularly when a mine transitions from processing higher-grade stockpiles to drawing more heavily on lower-grade run-of-mine material.

When BHP flagged grade decline as a known headwind, many models treated it as a manageable, gradual process. However, the FY27 guidance range suggests the decline is steeper than consensus assumed. This divergence between modelled expectations and operational reality is a recurring theme across mature porphyry copper systems globally.

The Escondida Effect: Grade Decline at the World's Largest Copper Mine

Escondida, located in Chile's Atacama Desert, is responsible for roughly 5 to 6% of annual global copper mine supply. No single asset outside of it comes close to that level of systemic influence. When Escondida's grade declines, it does not merely affect BHP's income statement — it affects the global copper balance. The Chile copper outlook is, in many respects, inseparable from Escondida's trajectory.

The mechanism of grade decline is worth understanding in some detail, because it is frequently misrepresented as a fixable operational problem rather than a geological inevitability.

Ore grade, expressed as a percentage of copper content per tonne of rock processed, is the single most important variable in copper mine economics. The estimated shift from a feed grade of approximately 0.90% in FY26 to roughly 0.70% in FY27 at Escondida's concentrator represents a decline of around 22% in copper content per tonne processed.

Even if BHP maintains or increases the volume of ore it pushes through the mill — which requires significant energy and water consumption in one of the world's most arid regions — it will recover meaningfully less copper per unit of throughput. Furthermore, cut-off grade economics become increasingly critical at this stage, as lower feed grades compress margins and force difficult decisions about which material is economically worth processing.

Technical Context: At Escondida's scale, a feed grade movement of 0.20 percentage points translates into hundreds of thousands of tonnes of lost copper recovery annually, assuming constant throughput. This is a structural, not cyclical, constraint. It reflects the natural depletion curve of a porphyry copper deposit that has been in continuous large-scale production since 1990.

This is a concept well understood in economic geology circles but often underappreciated by equity investors. Porphyry copper systems, which account for the majority of the world's copper production, typically have a high-grade core that gets mined early and a lower-grade halo that dominates production in later years. Escondida is now firmly in the halo phase for much of its current mining sequence — a reality that no amount of operational efficiency can fully offset.

Pampa Norte's Compounding Pressure

The grade story does not begin and end at Escondida. BHP's Pampa Norte operations, which include the Spence and Cerro Colorado mines in Chile, reported a year-on-year production decline of approximately 21%. Spence, in particular, has faced well-documented challenges with heap leach recovery rates as ore grades in its oxide zones decline.

The convergence of grade pressure across multiple Chilean assets amplifies the FY27 guidance compression beyond what any single site explanation can account for. Consequently, the copper supply crunch that analysts have long theorised about is beginning to manifest in the production guidance of the industry's largest operator.

Carrapateena's Conveyor Failure: Operational Risk in a Growth Asset

Separate from the grade decline story in Chile, BHP's Carrapateena mine in South Australia encountered an unplanned mechanical failure involving its underground conveyor system. The disruption, estimated to affect up to eight weeks of production, compounded the already below-consensus Copper SA guidance range and became a focal point for Macquarie's analysis of the guidance miss.

Carrapateena is an underground block cave operation that BHP acquired as part of the OZ Minerals takeover completed in 2023. It represents a meaningful component of BHP's growth narrative in copper, particularly given its sub-level cave to block cave transition plans that could significantly increase throughput over the coming years.

A conveyor failure at this stage of the asset's development does not alter the long-term thesis, but it removes production that the market had already incorporated into its near-term forecasts. The key distinction that investors and analysts must draw here is between structural production loss and one-off operational disruption. The Carrapateena conveyor failure belongs in the second category. Grade depletion at Escondida belongs firmly in the first.

How Sell-Side Analysts Positioned After the Guidance Update

Three broker responses capture the range of market sentiment following the FY27 guidance release.

| Broker | Rating | Price Target | Primary Concern |

|---|---|---|---|

| RBC Capital Markets | Not specified | A$57.00 | Copper SA guidance below 333Kt consensus |

| Macquarie | Neutral | Not specified | Carrapateena disruption as key miss driver |

| Morgans | Hold | A$59.80 | Grade decline; long-term thesis retained |

Morgans retained its Hold rating with a $59.80 price target, framing BHP as a structurally sound operator within a broadly supportive resources cycle. This framing is analytically important: it separates near-term volume disappointment from the long-term copper demand drivers thesis, effectively arguing that investors with a multi-year horizon should view the FY27 guidance as a temporary trough rather than a terminal inflection.

RBC's $57.00 price target positions slightly more conservatively, consistent with a view that the Copper SA shortfall deserves to be reflected in valuation. Macquarie's Neutral stance, with attention focused on the Carrapateena disruption, implies the market may have overreacted if the mechanically-driven losses prove to be genuinely transient.

Analyst Perspective: The divergence between RBC and Morgans targets — spanning A$57.00 to A$59.80 — reflects a genuine uncertainty about how much of the FY27 production loss should be discounted as recoverable versus how much represents the beginning of a sustained volume plateau at BHP's copper assets.

BHP's full-year FY26 results are scheduled for release on 18 August 2026, at which point management commentary on mine plans, capital allocation toward copper, and the Escondida grade trajectory will be closely scrutinised for any revision to the medium-term production outlook.

Coal and Iron Ore as Partial Offsets

BHP's quarterly result was not uniformly disappointing. The BMA coal operations, which cover the Queensland metallurgical coal joint venture with Mitsubishi, delivered production that beat consensus by approximately 11%, providing meaningful earnings support that partially cushioned the market reaction to the copper miss.

Iron ore performance also softened the immediate share price response, with the Pilbara operations continuing to run at high volumes. In addition, iron ore demand trends remain broadly supportive at the macro level, lending further ballast to BHP's diversified earnings base. The approximately 3% share price decline to $58.73 following the guidance update reflects a market that weighed the copper miss against the coal outperformance and landed on a net negative verdict, though not a catastrophic one.

The next major ASX story will hit our subscribers first

The Supply Paradox: Falling Output When Demand Is Accelerating

The deeper significance of the situation where BHP copper guidance misses expectations lies in its timing. The world is in the early stages of a structural copper demand expansion driven by electric vehicle manufacturing, grid-scale energy storage, data centre construction, and renewable energy infrastructure. Each of these sectors uses copper intensively and at scales that existing mine supply pipelines were not designed to meet.

Against this backdrop, the single largest copper-producing company on earth is guiding for a 15% reduction in copper output in FY27. The arithmetic is uncomfortable.

Strategic Scenario: If BHP's output contracts by approximately 250,000 tonnes in FY27 relative to the FY26 midpoint, while global copper demand continues to grow, the gap between available supply and required supply narrows further. BHP's scale gives its production trajectory an outsized influence on global copper market balance, functioning almost as a leading indicator for supply tightness.

Key Supply-Side Pressure Points Across the Copper Market

The Escondida grade issue is not an isolated case. Across the copper mining industry, a set of structural challenges is converging that makes replacement supply exceptionally difficult to source:

-

Grade depletion at legacy assets is a global trend. Average copper ore grades at major mines have declined by roughly 25% over the past two decades according to industry data, with no reversal expected at operating mines.

-

Greenfield development timelines remain prohibitively long. A newly discovered copper deposit typically requires 10 to 15 years from initial discovery to first production, meaning that decisions made today do not yield supply until well into the 2030s.

-

Geopolitical concentration risk is structurally elevated, with a disproportionate share of global production concentrated in Chile, Peru, and the Democratic Republic of Congo, each of which presents distinct regulatory and sovereign risk considerations.

-

Capital allocation competition within major diversified miners means copper investment competes against iron ore, coal, potash, and nickel for internal funding, particularly in years where copper volumes disappoint and free cash flow guidance is trimmed.

Frequently Asked Questions: BHP Copper Guidance and FY27 Outlook

Why Did BHP's Share Price Fall Approximately 3% After the Guidance Update?

The share price reaction reflected the gap between the FY27 copper guidance midpoint and market consensus, compounded by the Carrapateena disruption news. The decline to $58.73 was cushioned by coal outperformance and stable iron ore volumes.

What Is the Core Driver of the FY27 Copper Production Decline?

The primary driver is feed grade decline at Escondida, Chile, with the concentrator feed grade estimated to drop from approximately 0.90% to 0.70%, reducing copper recovery per tonne of ore processed. The Carrapateena conveyor failure is a secondary, largely non-recurring contributor.

What Is the Difference Between BHP's FY26 and FY27 Copper Guidance?

FY26 guidance was 1.9 to 2.0 million tonnes. FY27 guidance is 1.65 to 1.80 million tonnes, representing a midpoint reduction of approximately 15%.

When Will BHP Report Its Full-Year FY26 Financial Results?

BHP's full-year FY26 results are scheduled for 18 August 2026.

Does the FY27 Guidance Cut Change BHP's Long-Term Copper Investment Case?

Most analysts retain a constructive long-term view on BHP's copper exposure. The grade decline at Escondida is a known geological feature of the asset's maturation, and BHP's development pipeline — including Carrapateena's block cave expansion and the Copper SA portfolio — retains optionality on future volume recovery. The near-term disappointment does not extinguish the long-term thesis, but it does lengthen the timeline before volume growth can be expected to resume.

Framing BHP's FY27 Copper Guidance Miss in a Longer-Term Context

The most important analytical distinction to make in the aftermath of this guidance update is the one between what is geological and what is mechanical. Escondida's grade trajectory is the former. Carrapateena's conveyor is the latter. Investors who conflate the two risk either overreacting to a fixable disruption or, conversely, underestimating the sustained production headwind that a maturing porphyry deposit introduces into multi-year forecasts.

BHP remains one of the most credible large-scale copper operators on earth, with diversified revenue streams, strong cost positions, and a management track record of navigating grade transitions. However, the instance where BHP copper guidance misses expectations represents a genuine near-term production ceiling — one that arrives at an analytically awkward moment when copper demand narratives are at their most bullish.

Bottom Line: BHP's FY27 copper guidance of 1.65 to 1.80 million tonnes reflects a structurally lower near-term output trajectory, driven primarily by ore grade depletion at Escondida, and compounded by an unplanned operational disruption at Carrapateena. The FY26 production year remains broadly on track, and coal has outperformed. However, the scale of the FY27 copper contraction raises legitimate questions about the pace and shape of BHP's copper volume recovery story at precisely the moment when the global energy transition is generating its most intense demand expectations for the metal.

This article contains forward-looking statements, analyst price targets, and production estimates that are subject to change. Nothing in this article constitutes investment advice. Investors should conduct their own due diligence and seek independent financial counsel before making any investment decisions. Past performance of a company's production guidance accuracy is not indicative of future guidance reliability.

Want to Track the Next Major Copper Discovery Before the Market Catches On?

As grade depletion tightens copper supply and demand from the energy transition accelerates, identifying significant new discoveries early has never been more critical — Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex geological data into actionable opportunities instantly. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position ahead of the market.