June 19, 2026

The Hidden Complexity Behind Mining's Most Expensive Fertiliser Bet

Large-scale underground mining projects have a well-documented history of defying their original cost envelopes. From Olympic Dam's expansion studies to the prolonged development timelines of deep potash shafts in Central Europe, the gap between feasibility-stage estimates and final execution costs has become one of the most persistent structural risks in the global mining industry. When a project spans half a decade of construction in a remote location, involves specialised underground engineering, and is exposed to multiple inflationary cycles, the question is rarely whether costs will rise, but by how much.

Against that backdrop, the BHP Jansen potash cost overrun announced during the week ending 19 June 2026 landed with particular force, not because cost escalation is unusual, but because the magnitude and timing cut directly to the heart of BHP's long-cycle diversification thesis. Furthermore, mining project economics play a critical role in determining whether such capital commitments can ultimately deliver acceptable shareholder returns.

When big ASX news breaks, our subscribers know first

What the Numbers Actually Say About Jansen's Cost Blowout

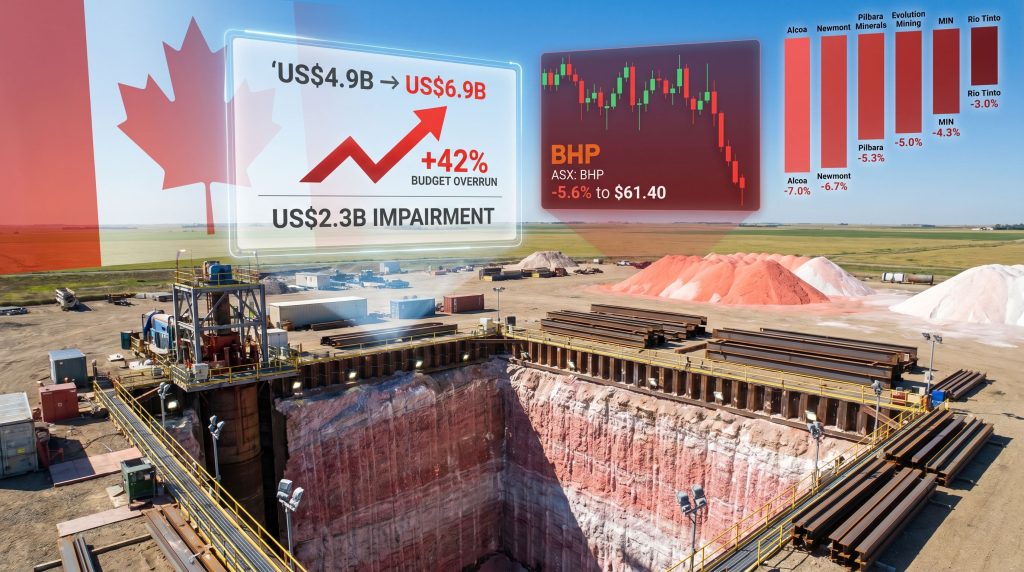

The revised budget for Jansen Stage 2 now sits at a minimum of US$6.9 billion, up from the originally approved estimate of US$4.9 billion. That represents a 42% cost overrun and more than US$2 billion in additional committed capital, accompanied by a US$2.3 billion impairment booked against the project.

Critically, this is not an isolated event within the Jansen complex. Stage 1 had already been revised upward to US$8.4 billion, with first production now expected in mid-2027. Stage 2 first production has been pushed to late financial year 2031.

| Parameter | Jansen Stage 1 | Jansen Stage 2 |

|---|---|---|

| Revised Cost Estimate | US$8.4 billion | US$6.9 billion |

| Expected First Production | Mid-FY2027 | Late FY2031 |

| Impairment Booked | Not specified separately | US$2.3 billion |

| Budget Overrun | Significant uplift from original | +42% / +US$2B |

When both stages are considered together, BHP's total capital commitment to the Jansen complex likely exceeds US$15 billion, making it one of the single largest capital allocations in the company's corporate history and a defining test of its strategic credibility beyond iron ore. According to BHP's official Jansen project page, the Saskatchewan deposit remains central to the company's long-term fertiliser strategy.

Why Potash Megaprojects Are Structurally Prone to Overruns

What makes underground potash development uniquely challenging?

Understanding the BHP Jansen potash cost overrun requires understanding what makes underground potash development uniquely challenging compared to other large-scale mining builds.

Potash sits in evaporite sequences deep underground, often more than 1,000 metres below surface. Accessing these deposits requires shaft-sinking, a highly specialised technique that involves excavating vertical shafts through water-bearing strata using ground freezing or cementation methods before reaching the potash horizon. There is a very limited global pool of contractors capable of executing this work to the required standard and safety specification.

Several structural factors compound this scarcity:

- Shaft-sinking operations cannot be accelerated by simply adding more workers; the physics of the shaft diameter and the sequential nature of lining and deepening operations impose hard constraints on productivity.

- Saskatchewan's construction labour market has tightened considerably since BHP's original feasibility estimates were set, with competing infrastructure and resource projects drawing from the same regional workforce.

- Unlike brownfield iron ore or copper expansions where historical cost data is rich and comparable, greenfield potash developments offer limited benchmarking, making upfront estimate accuracy structurally weaker.

- Multi-year construction timelines expose projects to several inflationary cycles, with steel, cement, ventilation equipment, and electrical infrastructure all subject to price variance over a 5–8 year build period.

BHP attributed the Stage 2 overrun to four primary drivers: sustained construction-phase inflation, design and scope changes made during execution, lower-than-expected labour productivity, and higher volumes of labour hours and materials than originally estimated. These drivers closely mirror the patterns identified in definitive feasibility studies for comparable megaprojects, where estimate accuracy is inherently constrained by early-stage assumptions.

Each of these drivers reflects a pattern that recurs across megaproject literature globally. Feasibility-stage estimates, by their nature, are built on assumptions about productivity norms, input prices, and scope stability that rarely survive first contact with ground conditions and evolving engineering requirements.

Understanding Potash Itself: Why BHP Entered This Market

What is potash and why does it matter strategically?

For investors less familiar with the commodity, potash refers primarily to potassium chloride (KCl), one of three primary macronutrients in commercial fertiliser alongside nitrogen and phosphate. Potassium is essential for plant cell structure, water regulation, and disease resistance, and unlike nitrogen, it cannot be synthesised from the atmosphere. It must be mined.

Global potash supply is geographically concentrated to a degree that few other commodities match:

- Canada (primarily Saskatchewan) and Russia/Belarus together account for the overwhelming majority of global potash production.

- The 2022 sanctions placed on Belarusian potash exports and the broader disruption to Russian agricultural commodity flows briefly drove potash prices to multi-decade highs before gradually unwinding.

- BHP's original strategic rationale for Jansen centred on establishing a Western Hemisphere, ESG-aligned potash supply source with decades of mine life, positioned for structural fertiliser demand growth driven by global population expansion and agricultural intensification in emerging markets.

The Jansen basin deposit is considered one of the highest-quality undeveloped potash resources in the world in terms of grade, seam continuity, and mine design optionality. That geological quality has not changed. What has changed is the cost of converting that resource into production.

Market Reaction and Index Impact: BHP's Worst Day Since April 2025

The market's response to the Jansen announcement was immediate and significant. BHP (ASX: BHP) fell 5.6% to $61.40 on the day of the announcement, its largest single-session decline since April 2025. Given BHP's weighting within the S&P/ASX 200, this single-stock move stripped approximately 60 index points from the benchmark, contributing materially to the index closing the week down 0.9% at 8,828.70.

The damage spread across the broader materials complex. Consequently, ASX market performance for the week reflected widespread repositioning across resource-exposed names:

| Company | Weekly Move | Primary Driver |

|---|---|---|

| BHP (ASX: BHP) | -5.6% | Jansen cost overrun announcement |

| Newmont | -6.7% | Gold price reversal and hawkish Fed |

| Alcoa | -7.0% | Extended ~30% slide since early June |

| Pilbara Minerals | -5.3% | Softer lithium sentiment |

| Evolution Mining | -5.0% | Gold price headwinds |

| Mineral Resources (ASX: MIN) | -4.3% | Iron ore and lithium weakness |

| Rio Tinto | -3.0% | Broad materials sector rotation |

Notably, the ASX 200 VIX slipped to 11.71, a three-month low, suggesting the selling reflected deliberate portfolio repositioning rather than panic-driven liquidation. Quarterly index rebalancing flows amplified price moves across the materials sector during this period.

What This Reveals About Capital Discipline and Investor Confidence

A 42% cost overrun on a flagship growth project crosses a threshold that institutional investors treat differently from routine budget variance. Industry analysis of large mining capital projects historically shows that overruns exceeding 20% tend to trigger a re-rating of the entire growth pipeline, not just the asset directly affected. The logic is straightforward: if management's cost estimation and project controls are shown to be materially insufficient on one major project, markets apply a scepticism discount to all remaining growth optionality.

For BHP specifically, several strategic questions now require answers:

- Does Jansen Stage 2 still clear BHP's internal hurdle rate at a US$6.9 billion cost base, and what potash price assumption is required to justify continuation?

- Will BHP proceed on its current trajectory, or will a further strategic review of Stage 2 be conducted before additional capital is committed?

- How does the revised 2031 timeline interact with projected global potash supply-demand dynamics, particularly given that Nutrien and Mosaic, as established Saskatchewan operators with decades of cost optimisation, remain the benchmark competitors?

- Does the US$2.3 billion impairment signal a structural reassessment of BHP's potash conviction, or is it a discrete accounting correction tied to revised engineering estimates?

BHP's long-term potash thesis rests on macro forces that remain intact: rising global protein consumption, farmland productivity pressures, and the strategic rationale for non-Russian potash supply. The challenge is not the thesis, it is whether the economics of executing it at Jansen can still deliver adequate returns at the revised cost structure.

The next major ASX story will hit our subscribers first

The Macro Environment That Amplified BHP's Individual Shock

The Jansen announcement did not land in a neutral market environment. The week ending 19 June 2026 was characterised by dual central bank hawkishness that was already pressuring commodity-sensitive equities before BHP's news compounded the selloff.

The Federal Reserve, at its first meeting under new Chair Kevin Warsh, held rates steady at a target of approximately 3.625%, but the accompanying Summary of Economic Projections delivered a surprise: roughly half of FOMC members now anticipate at least one additional rate hike before year-end. Warsh's messaging emphasised a stronger commitment to inflation control and a reduced reliance on forward guidance, driving the US dollar index to a one-year high and applying pressure on USD-denominated commodity prices across the board.

Domestically, the Reserve Bank of Australia held the cash rate at 4.35%, its first pause after three consecutive hikes in 2026. However, Governor Michele Bullock's tone remained notably hawkish, making clear that inflation remained too high and that further increases could not be ruled out. Australia's 10-year bond yield held near 15-week lows below 4.8%, while the Australian dollar drifted toward 10-week lows below US$0.705 as the US dollar strengthened.

How did commodity-specific pressures compound the selloff?

Commodity-specific pressures added further headwinds, and commodity price impacts were felt broadly across the resources sector:

- Gold fell 1.7% to approximately US$4,137/oz as monetary tightening signals outweighed fading geopolitical risk premiums.

- Iron ore softened on weaker seasonal demand from Chinese steel mills, compounded by soft May data showing contracting retail sales and a 35th consecutive monthly decline in new Chinese home prices. In addition, China steel demand concerns continued to weigh on iron ore-exposed producers throughout the week.

- Oil experienced its most dramatic weekly move, collapsing more than 5% on Monday following reports of a US/Iran agreement before partially recovering, with Brent finishing near US$80 and WTI back above US$77.

Sector Rotation: Healthcare and Defensives as the Beneficiaries

Capital that exited the materials sector rotated firmly into defensive and healthcare names. CSL (ASX: CSL) surged 7.6% to $116.32, its largest single-session gain since February 2022, as investors sought earnings quality and domestic revenue visibility. The S&P/ASX 200 Healthcare Index finished the week up approximately 5%.

Other notable beneficiaries of the rotation included:

- A2 Milk +8%

- Meridian Energy +7%

- Life360 +6%

- 4DMedical +17.6%

- Electro Optic Systems +14.3% on a US$124 million UAE counter-drone contract

- SkyCity Entertainment +14.6% following a $21 million settlement of anti-money laundering breaches

The pattern of the week, described by analysts as rotation without conviction, reflected capital shifting between sectors without any single group establishing durable leadership.

Key Catalysts and Risk Factors Investors Should Monitor

Several near-term data points carry the potential to meaningfully shift the market's trajectory following the BHP Jansen potash cost overrun and the broader resources selloff. Furthermore, the Financial Post's coverage of BHP's revised cost structure highlights the scale of the challenge facing management as it attempts to rebuild investor confidence.

Domestic catalysts:

- Australian May CPI (24 June): The most significant near-term release. A softer print would support the case that the rate cycle has peaked, providing relief for rate-sensitive and commodity-exposed equities. An upside surprise would likely revive RBA tightening expectations.

- Australian employment data (25 June): Labour market resilience would reinforce the hawkish RBA narrative and extend pressure on interest rate sensitive sectors.

International catalysts:

- Fed follow-through: Any further hawkish signals from the Federal Reserve would strengthen the USD and apply additional pressure on commodity prices.

- China NBS Manufacturing PMI: Month-end data will provide a read on commodity demand conditions heading into the second half of the year.

- US/Iran diplomatic progress: The formal signing ceremony scheduled for Switzerland was cancelled after the US delegation withdrew, preserving implementation risk and near-term oil price uncertainty.

With the ASX 200 technically capped near resistance around 9,000 and support around 8,700, the index's near-term direction is increasingly set by a narrow band of large-cap resource and financial names, making the upcoming CPI print especially consequential.

BHP's Jansen Potash Cost Overrun: Key Takeaways for Investors

The BHP Jansen potash cost overrun is a multi-dimensional event that carries implications well beyond a single line item in a project budget. Investors assessing BHP's risk/reward profile should consider the following:

- The 42% blowout on Stage 2 combined with Stage 1's prior revision establishes a pattern of cost escalation that markets will discount into BHP's remaining growth pipeline until a credible track record of execution is re-established.

- The US$2.3 billion impairment is a material earnings event that will flow through BHP's financials and is likely to prompt analyst earnings revisions for the current and forward financial years.

- The long-term potash thesis anchored in food security demand, Western supply chain diversification, and the strategic value of the Jansen deposit's geological quality remains structurally sound. The deterioration is in execution economics, not in the underlying commodity rationale.

- BHP's total Jansen capital commitment now likely exceeds US$15 billion across both stages, representing a defining capital allocation decision that will shape the company's free cash flow profile for the remainder of the decade.

- The broader market reaction, including the 60-point drag on the ASX 200 and the sector-wide materials selloff, reflects investor concern about megaproject execution risk as a systemic issue, not merely a Jansen-specific one.

This article is intended for informational purposes only and does not constitute financial product advice. Past project performance and market movements are not indicative of future outcomes. Readers should seek independent financial advice before making investment decisions. Forward-looking statements and timeline projections involve inherent uncertainty.

Want To Stay Ahead of Major ASX Resource Discoveries Before the Broader Market Reacts?

While BHP's Jansen potash cost overrun dominated headlines and dragged the broader materials sector lower, Discovery Alert's proprietary Discovery IQ model continuously scans ASX announcements in real time, instantly alerting subscribers to significant mineral discoveries with actionable investment potential — explore Discovery Alert's discoveries page to understand how historic finds have generated substantial returns, and begin a 14-day free trial at discoveryalert.com.au to position yourself ahead of the next major market-moving announcement.