June 19, 2026

The Hidden Economics of Mega-Project Mining: Why Cost Overruns Are the Rule, Not the Exception

There is a well-documented phenomenon in large-scale infrastructure and resource development known as the "optimism bias" — the systematic tendency of project planners to underestimate costs and timelines while overestimating benefits. In underground mining, this bias is amplified by geological uncertainty, commodity price volatility, and the sheer complexity of sustaining construction operations across multi-year horizons. The BHP Jansen potash mine cost overrun is not simply a corporate accounting event. It is a case study in the structural challenges that define mega-project execution in the modern mining industry, and it carries significant implications for investors, commodity markets, and the long-term economics of global fertilizer supply.

When big ASX news breaks, our subscribers know first

Why BHP Chose Potash as a Tier-1 Future-Facing Commodity

BHP's rationale for entering potash was built on a straightforward but powerful macro thesis. As global population growth continues to concentrate in developing economies with calorie-deficient diets, agricultural productivity must expand to meet demand. Potash — the potassium-rich mineral fertilizer that improves crop yields, water efficiency, and disease resistance — sits at the centre of that productivity equation.

Unlike many commodities, potash cannot be synthesised or substituted. Its supply is geographically concentrated, with Canada, Russia, and Belarus historically controlling the majority of global production capacity. This geographic concentration creates structural supply risk, particularly when geopolitical disruptions occur, as demonstrated by the market volatility that followed Russia's invasion of Ukraine in 2022.

Saskatchewan's Williston Basin is widely regarded as the world's highest-quality potash geology. The province sits atop the Prairie Evaporite formation, a vast geological sequence of marine evaporite deposits laid down approximately 380 million years ago during the Devonian period. These formations contain sylvinite ore — a mixture of sylvite (potassium chloride) and halite (sodium chloride) — at depths and grades that rank among the most economically attractive anywhere on Earth. For BHP, acquiring and developing the Jansen deposit was a once-in-a-generation opportunity to build a tier-1 asset in the world's premier potash district.

Breaking Down the BHP Jansen Potash Mine Cost Overrun

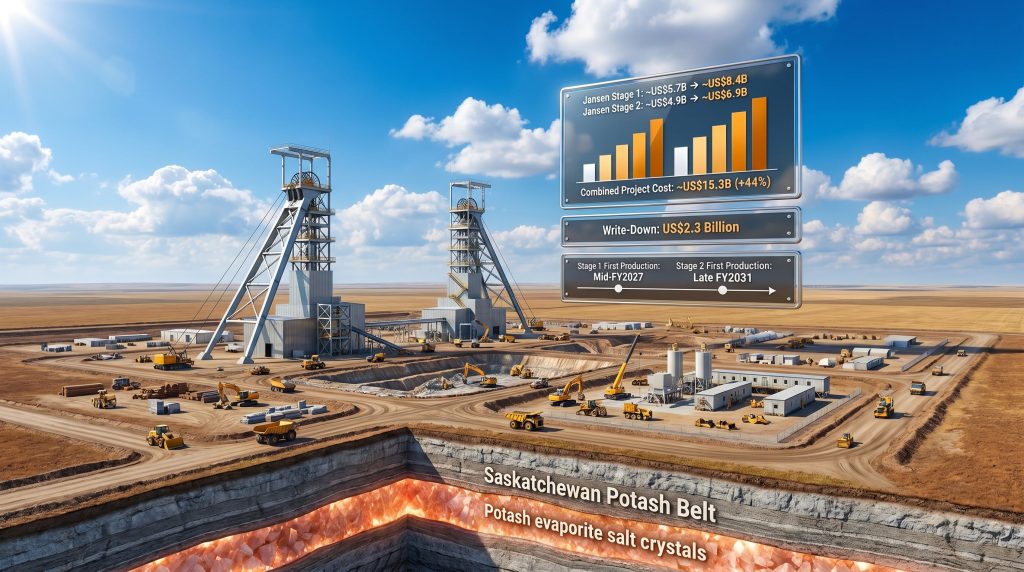

The scale of the budget revision now attached to Jansen is difficult to contextualise without examining each stage individually. Furthermore, understanding how these figures evolved helps illuminate why the definitive feasibility study assumptions underpinning the original sanction have proven insufficient against real-world conditions.

| Milestone | Original Estimate | Current Estimate | Change |

|---|---|---|---|

| Jansen Stage 1 Approved Cost (2021) | ~US$5.7 billion | ~US$8.4 billion | +~47% |

| Jansen Stage 2 Approved Cost (Oct 2023) | ~US$4.9 billion | ~US$6.9 billion | +~41% |

| Combined Jansen Project Cost | ~US$10.6 billion | ~US$15.3 billion | +~44% |

| Write-Down Recorded | N/A | US$2.3 billion | N/A |

This is the third instance in which BHP has revised both cost and schedule estimates upward across the two stages of the project. The drivers behind the Stage 2 blowout, as identified by BHP following a comprehensive internal review, include:

- Additional construction labour hours far beyond what was modelled in original project plans

- Greater volumes of raw materials consumed than initial scoping anticipated

- Design and scope modifications introduced during active construction phases

- Productivity rates that fell short of the baseline assumptions underpinning the project sanction

What makes the Stage 2 revision particularly notable is its timing. Construction is only approximately 16% complete as of June 2026. The vast majority of capital deployment still lies ahead, meaning the project carries substantial execution risk that has not yet been tested against real-world conditions.

Understanding the $2.3 Billion Impairment: What It Means in Mining Accounting

A mining impairment charge is recorded when the carrying value of an asset on a company's balance sheet exceeds the estimated recoverable amount of that asset. It is a non-cash accounting entry, meaning it does not immediately drain corporate liquidity, but it signals a genuine erosion in the expected economic returns of the project under revised assumptions.

In BHP's case, the US$2.3 billion impairment against Jansen Stage 2 reflects the gap between the value previously capitalised on the balance sheet and the lower recoverable value that results from the revised cost profile and the prevailing potash price environment. Importantly, BHP has maintained its group-level capital expenditure guidance at approximately US$11 billion, suggesting the impairment has not yet triggered a broader strategic reallocation of capital across the company's project portfolio.

Is This a Jansen Problem or an Industry-Wide Pattern?

Context matters when evaluating the BHP Jansen potash mine cost overrun. Mega-project cost escalation is a persistent feature of the global mining industry, not an isolated anomaly. Indeed, the commodity price impact on project economics compounds the difficulty of keeping long-duration capital programmes on budget.

| Project | Commodity | Original Budget | Final/Revised Cost | Overrun % |

|---|---|---|---|---|

| BHP Jansen (Stage 1 + 2) | Potash | ~US$10.6B | ~US$15.3B | ~44% |

| Oyu Tolgoi Underground (Rio Tinto) | Copper | ~US$5.3B | ~US$7.1B | ~34% |

| Goro Nickel (Vale) | Nickel | ~US$2.2B | ~US$6B+ | ~170%+ |

| Olympic Dam Expansion (BHP) | Copper/Uranium | ~US$20B+ | Shelved | N/A |

Note: Figures are approximate and sourced from publicly available industry disclosures.

Underground potash mining presents a particularly demanding set of cost challenges that surface operations do not encounter to the same degree:

- Shaft sinking is one of the most technically complex and time-sensitive operations in underground mining, requiring precision engineering over periods of several years. Any delay or design modification at the shaft sinking phase cascades through the entire project timeline.

- Saskatchewan's Prairie Evaporite formation, while geologically rich, contains localised zones of groundwater, brine inflows, and variable evaporite sequences that can introduce unexpected excavation complexity.

- Remote logistics in Western Canada impose significant cost premiums on labour mobilisation, equipment transport, and supply chain management.

- Extended construction timelines amplify exposure to inflationary pressures, particularly in labour and steel-intensive components of underground infrastructure.

One of the less-appreciated dynamics in Saskatchewan potash mining is the role of geological variability at depth. While the Prairie Evaporite is broadly predictable, localised brine pockets and dissolution features can create ground control challenges that force scope changes mid-construction, adding both cost and time in ways that surface-level feasibility models consistently underestimate.

Production Timeline: What the Delays Actually Mean

| Stage | Previous First Production Target | Revised First Production Target | Delay |

|---|---|---|---|

| Jansen Stage 1 | Earlier than 2027 | Mid-FY2027 | Modest |

| Jansen Stage 2 | FY2029 | Late FY2031 | ~2 years |

The two-year delay to Stage 2 is consequential for multiple reasons. First, it extends the period during which BHP is deploying capital without generating revenue from Stage 2's production. Second, it shifts the combined mine's full-capacity output further into a decade where potash price assumptions are increasingly uncertain. Third, it compresses the return on investment window for a project that requires sustained elevated prices to justify its expanded cost base.

Analysts at Jefferies flagged the Stage 2 cost increase of nearly 30% as having exceeded market expectations, describing the update as unhelpful given the challenging near-term outlook for potash prices. The bank maintained its hold rating on BHP, noting that more attractive value opportunities exist elsewhere within global mining at this point in the cycle.

The Potash Market: Does Jansen's Investment Case Still Hold?

The potash market has undergone a dramatic repricing cycle since 2021. Following Russia's invasion of Ukraine in February 2022, potash prices surged to historic highs above US$1,000 per tonne in some markets, driven by fears of supply disruption from Russia and Belarus, which together account for roughly 40% of global export supply. That price spike provided the market backdrop against which BHP sanctioned Jansen Stage 2 in October 2023.

However, the tailwind that supported that sanction decision has since moderated materially. Global potash prices have retreated significantly from their 2022 peaks, with benchmark prices trading in a range that has prompted analysts to question the return profile of high-capital greenfield projects. Consequently, the cut-off grade economics that underpin long-term project viability are under closer scrutiny than at any point since sanction.

Three Scenarios for Jansen's Value Creation Trajectory

Scenario 1: Potash Price Recovery

If global potash prices recover toward the post-Ukraine highs of US$500 to US$600 per tonne, Jansen's projected unit cost position of US$114 to US$130 per tonne generates exceptional operating margins. In this environment, the capital overrun becomes a smaller percentage of lifetime project value, and BHP's patience is rewarded.

Scenario 2: Sustained Price Weakness

If potash prices remain below US$300 per tonne through the late 2020s, the higher capital cost base compresses internal rates of return substantially. The extended timeline to Stage 2 production means BHP will have deployed the majority of that capital before testing the market at full output. This scenario raises legitimate questions about whether the Stage 2 sanction decision, made in a more favourable price environment, would withstand scrutiny today.

Scenario 3: Further Cost Escalation

Given that Stage 2 construction is only 16% complete, a fourth round of budget revisions cannot be ruled out. A further material cost increase would significantly damage investor confidence in BHP's project execution capabilities and could force a strategic review of the Jansen portfolio in its entirety.

The next major ASX story will hit our subscribers first

Jansen's Scale and Competitive Position in Global Potash

| Metric | Jansen (Full Capacity) | Global Context |

|---|---|---|

| Stage 1 Annual Output | ~4.36 Mtpa | Comparable to mid-tier global producers |

| Stage 2 Annual Output | ~4.36 Mtpa | Combined ~8.72 Mtpa total |

| Estimated Global Potash Share | ~10% | Among the world's largest single-site operations |

| Stage 2 Construction Completion | ~16% (as of June 2026) | Majority of capital yet to be deployed |

| Combined Unit Cost Target | US$114-130/t | Lowest-cost Canadian potash producer (projected) |

At full combined capacity, Jansen is projected to supply approximately 10% of total global potash production, placing it among the world's largest single-site potash operations. The unit cost target of US$114 to US$130 per tonne is the central pillar of BHP's competitive positioning argument. Even as capital costs have escalated, BHP has maintained that the operating cost structure remains intact, positioning Jansen as the lowest-cost potash producer in Canada at steady state.

This is a critically important distinction. In commodity markets, the difference between a cost-advantaged and a cost-disadvantaged producer is the difference between generating free cash flow through price cycles and being structurally uncompetitive during downturns. If BHP can deliver on its unit cost guidance, Jansen will remain economically viable across a wide range of potash price scenarios, even if the return on invested capital is lower than originally modelled.

What Investors Should Watch Beyond the Headline Write-Down

The US$2.3 billion impairment number dominates the narrative, but sophisticated investors should be monitoring a different set of variables. In addition, those alert to management red flags will recognise that repeated budget revisions warrant careful scrutiny of project governance and executive accountability:

- Stage 2 construction productivity rates as the project progresses beyond 16% completion. If productivity improves from the sub-baseline levels that contributed to the current overrun, it could signal that the revised budget holds.

- Potash benchmark pricing, particularly the granular and standard benchmark prices published through major contracts between Canadian producers and Asian buyers. These quarterly and semi-annual contract resets serve as a real-world stress test of Jansen's projected operating margins.

- BHP's capital expenditure guidance adherence. The company has maintained its ~US$11 billion group capex guidance despite the impairment. Any revision to this figure would signal broader capital pressure across the portfolio.

- Stage 2 sanction review risk. BHP has not publicly indicated any intention to revisit the Stage 2 decision, but at 16% completion, the option to pause or restructure technically still exists. Investor communications around this optionality will be an important signal to track.

Saskatchewan's Economic Stakes in Jansen's Timeline

The provincial economy of Saskatchewan is disproportionately exposed to the performance of its potash industry. The sector contributes substantially to provincial royalty revenues, employment, and infrastructure investment. A two-year delay to Jansen Stage 2 has tangible consequences for communities, contractors, and supply chain businesses across the province that had planned their own investment and hiring cycles around BHP's original timelines.

Saskatchewan is home to the world's most significant potash reserves, and the province's regulatory and infrastructure ecosystem has been built over decades to support large-scale underground potash operations. BHP's Jansen project, given its scale and projected output, represents a generational investment in that ecosystem. The delays do not eliminate the long-term economic contribution of the project, but they defer and resequence the provincial economic benefits in ways that local governments and Indigenous communities must now factor into their own planning horizons. Furthermore, broader mining industry consolidation trends mean that the competitive landscape for Saskatchewan potash development could shift considerably before Jansen reaches full capacity.

Frequently Asked Questions: BHP Jansen Potash Mine Cost Overrun

What is the total cost of BHP's Jansen potash mine?

The combined estimated cost of both stages now stands at approximately US$15.3 billion, following multiple budget revisions. Stage 1 alone has risen from an approved cost of roughly US$5.7 billion to approximately US$8.4 billion, an increase of nearly 50% since its 2021 sanction.

Why has BHP taken a $2.3 billion write-down on Jansen?

The impairment reflects the difference between the previously capitalised carrying value of Jansen Stage 2 and the revised recoverable amount following a comprehensive project review. The charge was triggered by a roughly US$2 billion cost increase on Stage 2 alone, lifting its budget from approximately US$4.9 billion to US$6.9 billion. Reporting from the AFR confirmed the scale of the cost blowout and its significance to BHP's broader capital programme.

When will BHP's Jansen potash mine start production?

Stage 1 first production is targeted for mid-fiscal year 2027. Stage 2 has been delayed by approximately two years, with first production now expected in late fiscal year 2031.

How much of global potash production will Jansen supply at full capacity?

At full combined output, BHP projects Jansen will account for approximately 10% of total global potash production, with each stage delivering roughly 4.36 million tonnes per annum.

What is Jansen's projected unit cost of production?

BHP has maintained its unit cost guidance of approximately US$114 to US$130 per tonne, which would position Jansen as the lowest-cost potash operation in Canada on a combined basis.

Has BHP changed its overall capital expenditure guidance?

Despite recording a US$2.3 billion impairment, BHP has maintained its group-level capital expenditure guidance at approximately US$11 billion, indicating the write-down has not yet forced a material reallocation of capital across the broader portfolio.

Key Takeaways

- The BHP Jansen potash mine cost overrun has lifted the combined project cost to approximately US$15.3 billion, some 44% above the original combined estimates at sanction

- The US$2.3 billion impairment is a non-cash accounting charge but reflects genuine erosion in the project's expected return profile under current potash market conditions

- BHP's unit cost target of US$114 to US$130 per tonne remains the central investment thesis, and if achieved, positions Jansen as a durable low-cost competitor through commodity price cycles

- With Stage 2 construction only 16% complete, the majority of capital deployment and execution risk still lies ahead, making continued cost discipline the critical variable for project value recovery

- Analyst sentiment has turned cautious following the latest revision, with at least one major investment bank maintaining a hold rating and noting superior value opportunities elsewhere in global mining at present

- The Saskatchewan provincial economy, which is deeply integrated with potash sector performance, faces a two-year deferral of the economic benefits associated with Stage 2's original timeline

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forward-looking statements, scenario projections, and analyst sentiment references involve inherent uncertainty. Readers should conduct their own due diligence before making any investment decisions. Potash price forecasts and project cost estimates are subject to revision as market and operational conditions evolve.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

While mega-project cost overruns like Jansen highlight the complexity of large-scale mining investment, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data into actionable opportunities for investors at every experience level. Explore Discovery Alert's discoveries page to see how historic discoveries have generated substantial returns, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.