June 4, 2026

The Australian resource sector operates within increasingly complex capital allocation frameworks, where traditional expansion models face scrutiny from shareholders demanding operational efficiency over growth at any cost. Mining companies now prioritise infrastructure optimisation and strategic partnerships to maximise returns from existing assets rather than pursuing capital-intensive greenfield developments. This shift reflects broader industry recognition that sustainable competitive advantages emerge through operational excellence and cost structure improvements, with the BHP and Rio Tinto iron ore partnership exemplifying this new approach rather than production volume alone.

What Makes the BHP and Rio Tinto Iron Ore Partnership a Game-Changer for Iron Ore Markets?

Understanding the Strategic Context Behind Historic Rival Cooperation

The January 2026 announcement of collaborative development between Australia's two largest iron ore producers represents a fundamental departure from decades of competitive dynamics in the Pilbara region. This strategic realignment stems from recognition that valuable mineral deposits located along operational boundaries remained inaccessible under traditional single-company development models due to prohibitive capital requirements.

The partnership structure addresses several critical market pressures simultaneously. Capital efficiency has become paramount as mining companies face investor demands for disciplined spending and improved returns on invested capital. Rather than pursuing duplicate infrastructure development, both organisations can now access previously stranded ore reserves through shared processing facilities and logistics networks.

Market forces driving this collaboration include:

• Increased shareholder focus on capital discipline over production growth

• Infrastructure cost escalation making independent development uneconomical

• Regulatory complexity requiring coordinated community engagement strategies

• Commodity price volatility demanding operational flexibility

The successful 2023 Mungadoo Pillar agreement provided operational precedent for this expanded partnership model, demonstrating that competitive rivals could effectively coordinate resource extraction while maintaining independent business operations. Furthermore, this development aligns with broader mining industry evolution trends emphasising collaboration over competition.

The Economics of Shared Infrastructure in Mining Operations

Infrastructure sharing fundamentally transforms the economics of resource development by eliminating capital redundancy whilst optimising facility utilisation rates. Under this partnership structure, BHP directs ore from its Yandi deposits to Rio Tinto's existing processing facilities, avoiding the need for duplicate infrastructure construction.

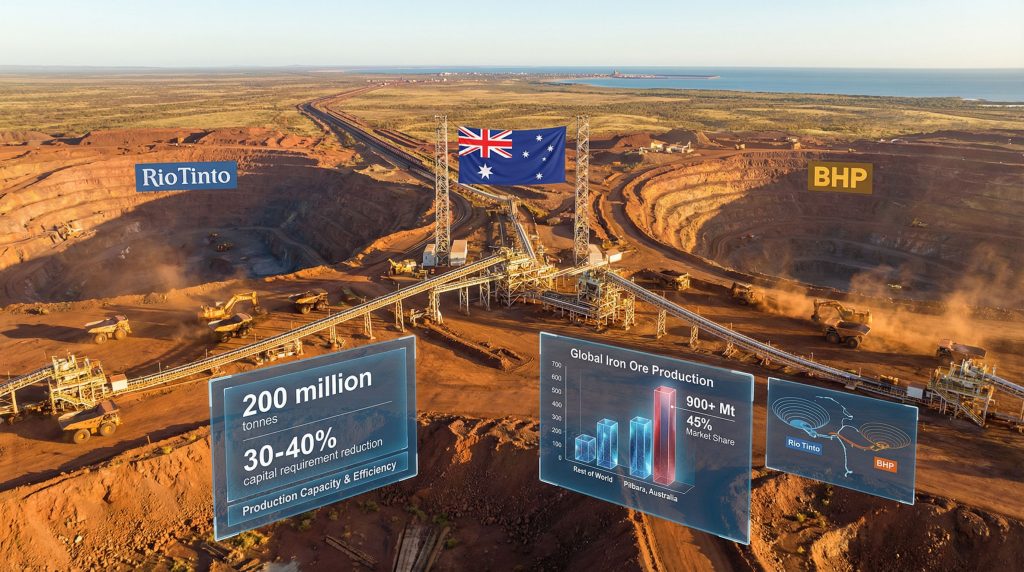

The financial mechanics create value for both participants through complementary operational strengths. Rio Tinto monetises excess processing capacity at its Yandicoogina operation whilst BHP avoids substantial capital expenditure for new facilities. This arrangement potentially reduces combined capital requirements by 30-40% whilst maintaining targeted production growth trajectories.

Key economic advantages include:

• Elimination of duplicate processing facility construction costs

• Improved asset utilisation rates across existing infrastructure

• Revenue diversification through processing fee arrangements

• Reduced operational complexity for regulatory compliance

• Enhanced operational flexibility during commodity price cycles

Revenue-sharing frameworks align incentives between the partners whilst distributing economic benefits proportionally to each company's contribution. Consequently, this collaborative approach enables both organisations to maintain profitability during iron ore price trends downturns through structural cost advantages versus competitors operating independent facilities.

When big ASX news breaks, our subscribers know first

Which Investment Scenarios Could Emerge from This Mining Partnership?

Scenario 1: Successful Implementation and Market Leadership

Optimal execution of this partnership could unlock approximately 200 million tonnes of additional iron ore production capacity by the early 2030s, significantly enhancing both companies' market positioning. Success in this scenario depends on seamless operational integration and effective coordination between separate corporate entities managing shared infrastructure.

Enhanced profit margins emerge through reduced operational costs per tonne, creating competitive advantages during periods of stable or declining iron ore prices. Lower cost structures position both companies favourably against global iron ore suppliers, particularly during market downturns when marginal producers face profitability pressures.

Success indicators for this scenario include:

• Achievement of production targets within projected timelines

• Operational cost reductions meeting or exceeding 30-40% projections

• Successful community engagement and regulatory approval processes

• Effective workforce integration across company boundaries

• Maintained safety and environmental compliance standards

The partnership potentially establishes a template for industry consolidation trends, demonstrating that strategic alliances can deliver superior returns compared to traditional competitive models in capital-intensive sectors.

Scenario 2: Regulatory and Execution Challenges

The non-binding nature of current agreements creates material execution risk, as either party could withdraw if market conditions or operational complexities prove unfavourable. Technical integration challenges may emerge from harmonising different operational systems, workforce protocols, and environmental compliance frameworks between separate organisations.

Traditional Owner consultation requirements represent substantive regulatory hurdles that could introduce project delays or require operational modifications. These consultation processes are mandatory under Australian mining law and can extend project timelines significantly beyond initial projections.

Important Consideration: Mining partnerships involving shared infrastructure typically encounter integration complexities that may require 12-24 months longer than independent development projects due to coordination requirements between separate corporate entities.

Potential risk factors include:

• Technical incompatibility between existing operational systems

• Extended Traditional Owner consultation and agreement processes

• Regulatory approval delays for joint venture structures

• Workforce coordination challenges across company boundaries

• Environmental compliance complexity for shared operations

• Market volatility affecting project economics

The five-plus year execution timeline creates extended exposure to changing market conditions, regulatory frameworks, and operational circumstances that could materially impact project viability. However, analysis of iron ore demand insights suggests long-term fundamentals remain supportive.

Scenario 3: Industry-Wide Collaboration Trend

This partnership may catalyse broader industry transformation toward strategic alliance models rather than traditional merger and acquisition approaches. The success of collaborative infrastructure sharing could inspire similar arrangements across copper, lithium, and other commodity sectors where geographic proximity enables operational synergies.

Asset-light operational models increasingly replace capital-intensive expansion strategies as mining companies optimise existing portfolios rather than pursuing greenfield developments. This shift reflects industry maturation and investor preferences for capital discipline over production growth.

Industry transformation indicators include:

• Increased strategic alliance formation versus traditional M&A activity

• Technology and expertise sharing agreements between competitors

• Cross-border collaboration in resource development projects

• Emphasis on processing and logistics optimisation

• Reduced capital intensity across mining sector participants

International mining companies may adopt similar collaborative frameworks, particularly in regions where regulatory complexity or community engagement requirements favour coordinated development approaches over competitive expansion models.

How Do Pilbara Operations Compare Globally in Iron Ore Production?

Australia's Position in Global Iron Ore Supply Chains

The Pilbara region dominates global iron ore supply with annual production exceeding 900 million tonnes, representing approximately 45% of worldwide output. This production volume significantly exceeds major competitors, with Brazil's Vale producing approximately 300 million tonnes annually (15% market share) and Chinese domestic production reaching 240 million tonnes (12% market share).

| Production Region | Annual Output (Mt) | Global Market Share | Primary Advantages |

|---|---|---|---|

| Pilbara, Australia | 900+ | 45% | High-grade ore, Asian proximity |

| Vale, Brazil | 300+ | 15% | Large reserves, established infrastructure |

| China Domestic | 240+ | 12% | Local consumption, government support |

| Other Global | 560+ | 28% | Regional diversification, specialty grades |

Geographic proximity to Asian steel manufacturing centres provides structural advantages through reduced transportation costs and enhanced supply chain reliability. Shipping routes from Pilbara to major Asian ports are significantly shorter than alternatives from Brazil or other remote locations, creating cost competitiveness that strengthens during periods of elevated freight rates.

Moreover, australian iron ore leadership continues to benefit from these natural advantages, positioning the country as the world's most reliable supplier to Asian markets.

Competitive Advantages of Joint Pilbara Development

Superior ore quality characteristics distinguish Pilbara production from global competitors, particularly regarding iron content percentages and lower impurity levels. High-grade Australian ore commands premium pricing in specialty steel markets where metallurgical properties are critical for end-product quality.

Established rail and port infrastructure networks support efficient extraction, processing, and logistics operations at scales that newer operations struggle to replicate. The BHP and Rio Tinto iron ore partnership leverages these existing infrastructure advantages whilst optimising asset utilisation across a broader operational footprint.

Strategic positioning advantages include:

• Transportation efficiency: 7-14 day shipping to Asian steel mills versus 30+ days from Brazil

• Ore quality premium: Higher iron content and lower impurity levels

• Infrastructure maturity: Decades of rail and port capacity development

• Operational scale: Combined operations approaching 50% of global seaborne trade

• Supply chain reliability: Established relationships with Asian steelmakers

The joint development amplifies these natural competitive advantages by consolidating production scale and optimising logistics coordination across neighbouring operations, potentially creating insurmountable cost advantages versus global competitors.

What Are the Financial Implications for BHP and Rio Tinto Shareholders?

Capital Allocation Efficiency Analysis

Infrastructure sharing eliminates redundant facility construction whilst optimising capital deployment across both organisations. The partnership potentially reduces individual company infrastructure investment requirements by 30-40% whilst maintaining production growth targets, significantly improving capital efficiency metrics for shareholders.

Enhanced return on invested capital emerges through shared resource utilisation rather than duplicate facility development. This approach enables both companies to maintain competitive production capacity whilst preserving cash flow for dividend distributions or alternative investment opportunities.

Capital efficiency improvements include:

• Reduced individual company capital expenditure requirements

• Improved asset utilisation rates across existing infrastructure

• Enhanced free cash flow generation through cost structure optimisation

• Maintained production growth without proportional capital increases

• Diversified operational risk through shared infrastructure arrangements

Valuation Impact Assessment

The partnership structure creates potential valuation benefits through improved operational margins and reduced capital intensity. Lower cost structures enhance earnings stability during commodity price volatility, potentially supporting premium valuations compared to competitors with higher operational costs.

Current market positioning reflects these dynamics:

• Rio Tinto valuation: Trading at approximately 12-13 times earnings with 4.4% dividend yield

• BHP valuation: Trading at approximately 16-18 times earnings with 3.6% dividend yield

• Partnership premium: Potential margin improvements not yet reflected in current valuations

Investment Insight: The collaboration could reduce combined capital requirements by 30-40% whilst maintaining production growth targets, potentially improving both companies' free cash flow generation capacity over the medium term.

Risk-Adjusted Return Considerations

Diversification benefits emerge through operational collaboration, reducing execution risk compared to independent development approaches. Shared infrastructure arrangements provide operational flexibility during volatile commodity environments whilst maintaining competitive cost structures.

Risk mitigation factors include:

• Reduced individual company exposure to capital cost overruns

• Shared operational risk across partnership structure

• Enhanced operational flexibility during market downturns

• Diversified revenue streams through processing arrangements

• Improved operational resilience through shared expertise

Market timing advantages enable both companies to access stranded reserves without significant capital commitments during uncertain commodity price environments, preserving financial flexibility for shareholders.

How Does This Partnership Address China's Steel Demand Dynamics?

Understanding Chinese Steel Market Evolution

China's steel demand patterns are transitioning from infrastructure-driven consumption toward manufacturing-focused applications, creating implications for iron ore quality requirements and supply chain preferences. This evolution favours high-grade ore suppliers like the BHP and Rio Tinto iron ore partnership over lower-quality alternatives.

Carbon neutrality commitments are reshaping Chinese steel production processes, emphasising efficiency improvements and quality inputs that reduce energy consumption per tonne of steel output. Premium Australian ore supports these objectives through superior metallurgical properties.

Chinese market transformation factors:

• Demand composition shift: Infrastructure to manufacturing-focused consumption

• Quality preferences: Premium ore for energy-efficient steel production

• Policy influence: Carbon neutrality goals affecting production methods

• Supply diversification: Reduced dependency on single-source suppliers

• Technology adoption: Advanced steel production requiring high-grade inputs

Supply Chain Resilience Strategies

The partnership enhances supply chain reliability for Asian steelmakers through coordinated production planning and shared logistics infrastructure. Combined operations provide operational flexibility that individual companies cannot achieve independently, supporting consistent delivery schedules during operational disruptions.

Quality premium positioning enables both companies to maintain profitability during commodity price downturns when lower-grade suppliers face margin pressures. This positioning supports long-term contract structures with Asian steelmakers seeking reliable, high-quality ore supplies.

Strategic supply chain advantages:

• Operational coordination: Shared logistics planning across neighbouring operations

• Quality consistency: Standardised ore grades through coordinated processing

• Delivery reliability: Backup operational capacity during maintenance periods

• Contract flexibility: Enhanced ability to meet varying customer specifications

• Risk diversification: Reduced operational disruption exposure for customers

What Lessons Can Other Mining Companies Learn from This Collaboration?

Best Practices in Resource Sector Partnerships

The BHP and Rio Tinto collaboration demonstrates structured approaches to competitor cooperation without compromising individual company strategic objectives. Key success factors include clearly defined operational boundaries, transparent revenue-sharing arrangements, and coordinated regulatory engagement strategies.

Partnership framework elements:

• Operational clarity: Defined responsibilities and decision-making authorities

• Financial transparency: Clear revenue and cost allocation methodologies

• Regulatory coordination: Joint community engagement and approval processes

• Risk allocation: Shared operational and financial risk distribution

• Performance metrics: Aligned operational targets and measurement systems

Structured competitor collaboration requires robust governance frameworks that maintain competitive independence whilst enabling operational coordination. This balance is critical for regulatory approval and long-term partnership sustainability.

Industry Transformation Indicators

The partnership signals broader industry evolution from growth-focused strategies toward capital discipline and operational optimisation. This transformation reflects mining sector maturation and investor demands for improved capital efficiency across resource development projects.

Industry evolution patterns:

• Capital discipline emphasis: Operational optimisation over greenfield expansion

• Technology sharing opportunities: Collaborative innovation in autonomous operations

• Regulatory efficiency: Coordinated engagement with government and community stakeholders

• Asset optimisation: Existing infrastructure utilisation versus new development

• Strategic alliance formation: Partnership models versus traditional acquisition strategies

International mining companies may adopt similar collaborative frameworks, particularly in jurisdictions where regulatory complexity or community engagement requirements favour coordinated development approaches.

The next major ASX story will hit our subscribers first

Which Risks Should Investors Monitor in This Partnership?

Operational Integration Challenges

Technical compatibility between different mining systems presents ongoing operational complexity throughout the partnership duration. Harmonising separate corporate cultures, operational procedures, and safety protocols requires sustained management attention that could impact operational efficiency during integration periods.

Workforce coordination across company boundaries creates potential operational disruptions during transition periods. Different employment terms, safety training requirements, and operational procedures must be reconciled to ensure seamless collaboration between separate organisations.

Integration risk factors:

• System compatibility: Technical integration between separate operational platforms

• Workforce coordination: Cultural and procedural harmonisation requirements

• Safety compliance: Unified safety standards across different corporate frameworks

• Operational efficiency: Potential productivity impacts during transition periods

• Management complexity: Sustained coordination requirements between separate entities

Market and Regulatory Risk Factors

Chinese government policy changes affecting steel demand represent material risk factors for Pilbara iron ore producers regardless of operational efficiency improvements. Economic policy shifts, environmental regulations, or trade restrictions could significantly impact demand patterns independent of operational performance.

Australian regulatory approval processes for joint ventures involve multiple stakeholder consultations and environmental assessments that could extend project timelines or require operational modifications. Traditional Owner consultation requirements are mandatory and may introduce delays beyond current project schedules.

External risk considerations:

• Chinese policy changes: Steel demand regulations or trade restrictions

• Australian regulatory approval: Joint venture and environmental assessment processes

• Traditional Owner consultations: Community agreement requirements and timelines

• Market volatility: Iron ore price fluctuations affecting project economics

• Currency fluctuations: Australian dollar movements impacting revenue streams

Financial Performance Dependencies

Iron ore price volatility significantly impacts project economics independent of operational efficiency improvements. Capital cost escalation during construction phases could erode projected returns if global inflation pressures continue affecting mining industry input costs.

Financial risk factors include:

• Commodity price volatility: Iron ore market fluctuations affecting project returns

• Capital cost inflation: Construction and equipment price increases

• Currency exposure: Australian dollar exchange rate movements

• Operational cost escalation: Labour and energy price increases

• Market demand shifts: Structural changes in global steel consumption patterns

Disclaimer: This analysis involves forward-looking projections and industry speculation that may not materialise as expected. Mining partnerships involve significant operational and financial risks that could materially impact investor returns. Past performance of similar partnerships does not guarantee future results.

How Could This Model Transform Global Mining Industry Practices?

Precedent Setting for International Resource Partnerships

The BHP and Rio Tinto collaboration establishes operational frameworks that international mining companies could replicate across copper, lithium, and other commodity sectors. Geographic proximity enabling infrastructure sharing exists in numerous global mining regions where competitive dynamics have historically prevented collaborative development.

Cross-border collaboration opportunities may emerge in resource development projects where regulatory frameworks favour coordinated approaches over competitive expansion. This model demonstrates that strategic partnerships can deliver superior returns compared to traditional merger and acquisition strategies in capital-intensive industries.

International replication opportunities:

• Copper sector partnerships: Shared processing facilities in Chilean or Peruvian operations

• Lithium collaboration: Coordinated development in Australian or South American regions

• Technology sharing frameworks: Collaborative innovation in autonomous mining systems

• Cross-border alliances: International partnerships in complex regulatory environments

• Infrastructure optimisation: Shared logistics and processing across neighbouring operations

Long-Term Industry Structure Evolution

Movement toward asset-light operational models reflects industry maturation and investor demands for capital efficiency over production growth. This structural shift may permanently alter competitive dynamics within global mining sectors as companies prioritise operational optimisation over traditional expansion strategies.

Strategic alliance formation increasingly replaces traditional merger and acquisition activity as companies seek operational synergies without full corporate integration. This approach enables competitive cooperation whilst maintaining independent strategic flexibility for participants.

Industry structure implications:

• Reduced capital intensity: Emphasis on operational efficiency over expansion

• Enhanced collaboration: Strategic partnerships versus competitive expansion

• Technology integration: Shared innovation and development costs

• Regulatory efficiency: Coordinated stakeholder engagement approaches

• Market responsiveness: Flexible operational capacity during demand fluctuations

The partnership model may become the preferred development approach in mature mining regions where infrastructure exists and regulatory complexity favours coordinated development over independent expansion strategies. As this historic collaboration demonstrates, even traditional rivals can find mutual benefit through strategic cooperation when market conditions favour efficiency over competition.

Ready to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Begin your 30-day free trial today to position yourself ahead of the market, and discover why major mineral discoveries can lead to substantial returns by exploring historic examples of exceptional outcomes.