July 14, 2026

Why Commodity Cycles Reward the Patient and Punish the Impatient

Every seasoned resources investor understands a fundamental truth: the biggest gains in mining stocks are rarely made by chasing price momentum. They are made by understanding structural commodity dynamics, identifying quality operators, and maintaining conviction through the inevitable volatility. The question of whether the BHP share price could be a buy in 2026 is less about short-term price targets and more about whether the underlying commodity thesis justifies long-term ownership at current valuations.

BHP Group Ltd (ASX: BHP) sits at the intersection of several powerful macroeconomic forces simultaneously. Energy transition, food security, and infrastructure investment across emerging markets all converge on the three commodities that increasingly define BHP’s identity: copper, iron ore, and potash. Understanding each of these pillars, and the risks that sit beneath them, is the starting point for any serious investment assessment.

When big ASX news breaks, our subscribers know first

How BHP’s Commodity Portfolio Differs From Its ASX Peers

Most large ASX mining companies are defined by a single dominant commodity. Fortescue is iron ore. Pilbara Minerals is lithium. Even Rio Tinto, despite its diversification into aluminium and now lithium, carries a heavy iron ore weighting. The BHP strategic pivot toward a three-pillar commodity structure spanning iron ore, copper, and the emerging potash asset at Jansen gives it a qualitatively different earnings profile to almost any other company on the ASX 200.

This diversification matters for several reasons beyond the obvious risk-spreading narrative:

- Iron ore and copper prices are not perfectly correlated, meaning BHP’s earnings base has greater stability across different economic cycles

- Potash, once Jansen reaches production, will add exposure to agricultural commodity cycles that are entirely disconnected from industrial metals demand

- Copper’s structural demand story is driven by electrification timelines, while iron ore remains tied to Chinese construction activity, and potash demand is shaped by global food production pressures

This tri-commodity architecture is not accidental. BHP has spent years strategically repositioning its portfolio away from thermal coal and petroleum toward commodities it believes will benefit from multi-decade structural demand growth.

The Copper Thesis: Structural Scarcity Meets Surging Demand

Copper occupies a unique position in the global commodity landscape. It is simultaneously a barometer of industrial activity and a critical enabler of the energy transition. Every electric vehicle contains roughly two to four times more copper than a conventional internal combustion engine vehicle. Offshore wind turbines can require up to eight tonnes of copper per megawatt of capacity. Grid-scale battery storage systems and solar installations are similarly copper-intensive.

What makes the copper supply side particularly interesting is a dynamic that receives less attention than the demand story: the systematic decline in ore grades at existing mines. Furthermore, the copper supply crunch is a long-term structural challenge that underpins the investment case for major copper producers like BHP.

The Ore Grade Problem in Copper Mining

This is a geological reality that has significant long-term implications for supply economics. Copper ore grades at many of the world’s largest operating mines have been declining steadily for decades. Where mines once processed ore grading above 2% copper, many major operations now work material grading below 0.5%. Lower grades mean more rock must be moved and processed to produce the same quantity of copper, which increases energy consumption, water use, and unit production costs.

The implication is structural: finding a new large-scale, high-grade copper deposit that can be economically developed within a reasonable timeframe is becoming progressively harder. The exploration pipeline for world-class copper assets has been shrinking for years, and the lead time from discovery to first production at a major copper mine now regularly exceeds a decade.

This supply constraint dynamic, combined with accelerating demand from electrification, creates a fundamentally supportive backdrop for copper prices over the medium to long term.

BHP’s Copper Performance: The Numbers Behind the Narrative

BHP has been purposefully building copper exposure through acquisitions and organic development, and the financial results are beginning to reflect that strategy in a meaningful way.

| Period | Copper EBITDA | Average Realised Price | Year-on-Year Change |

|---|---|---|---|

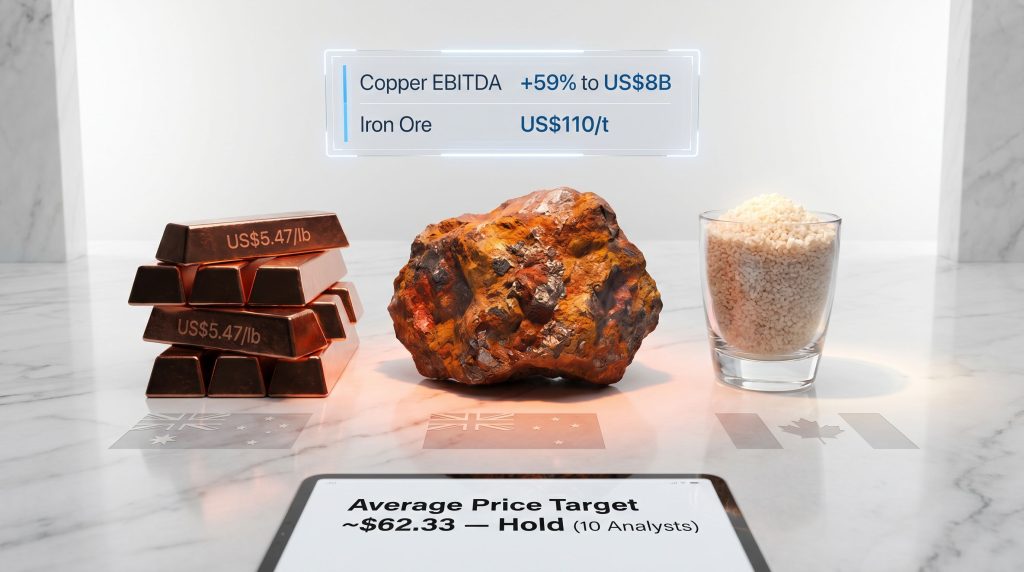

| FY26 First Half | US$8 billion | US$5.28 per pound | +59% EBITDA, +32% price |

| March 2026 Quarter | Update | US$5.47 per pound | +31% quarter-on-quarter |

The earnings leverage embedded in BHP’s copper division is substantial. A 59% surge in underlying copper EBITDA to US$8 billion during the FY26 first half, driven by a 32% increase in the average realised price to US$5.28 per pound, demonstrates how quickly copper price improvements flow through to BHP’s bottom line. The subsequent quarterly update for the March 2026 quarter showed the average realised copper price climbing a further 31% to US$5.47 per pound, a trajectory that suggests continued earnings momentum if prices hold.

For investors, the key analytical insight here is the concept of operating leverage: because BHP’s copper operations carry significant fixed costs, incremental price increases above a breakeven threshold flow disproportionately to earnings. This is why the copper division’s EBITDA grew at nearly twice the rate of the price increase. The commodity price impact on BHP’s earnings is perhaps most visible in this copper earnings leverage dynamic.

Iron Ore: When the Market Consensus Gets It Wrong

Few commodity price forecasts have been as consistently incorrect over the past two years as iron ore. Entering 2025 and again heading into 2026, the prevailing analyst consensus expected iron ore prices to drift toward the low US$90s per tonne, pressured by expanding supply from West Africa and other emerging producers entering the seaborne market.

That forecast has not materialised. Consequently, iron ore price trends have demonstrated significant resilience, trading at approximately US$110 per tonne, which is materially above the bearish consensus that shaped earlier earnings expectations. For BHP, this matters enormously because iron ore remains the company’s largest single earnings contributor and the primary engine funding its dividend programme.

What Drives Iron Ore’s Surprising Resilience

Several factors have contributed to iron ore holding above consensus forecasts:

- Chinese infrastructure stimulus offsetting the expected weakness in residential construction demand

- Delays in new African supply coming online at the scale and speed that analysts had anticipated

- Firm steel margins in certain segments of the Chinese steel complex, supporting blast furnace utilisation rates

- Inventory restocking cycles creating periodic demand surges that tighten the seaborne market

The wildcard remains Chinese policy. The China steel demand outlook for infrastructure spending and steel industry restructuring will continue to be the single most important variable in iron ore pricing. Investors who hold BHP are, to a meaningful extent, taking a position on the direction of Chinese economic activity.

Iron Ore Price Scenarios and Dividend Implications

| Iron Ore Price Range | Earnings Implication | Dividend Impact |

|---|---|---|

| Below US$90 per tonne | Significant earnings compression | Dividend reduction likely |

| US$100 to US$110 per tonne | Solid, in-line earnings | Dividend maintained at current levels |

| Above US$110 per tonne | Earnings upside relative to consensus | Potential for dividend uplift |

Potash: The Long-Duration Diversification Most Investors Underestimate

Potash rarely features prominently in discussions about BHP because it is still under construction. However, Jansen, located in Saskatchewan, Canada, represents one of the largest capital commitments BHP has made in the current era and could fundamentally change the company’s earnings profile over the next decade.

Why Potash Is Strategically Different From BHP’s Other Commodities

Potash is a fertiliser input, which means its demand is driven by agricultural productivity requirements rather than industrial activity or construction. Global population growth, dietary shifts toward more protein-intensive foods in developing economies, and the ongoing need to maintain crop yields on finite arable land all support long-term potash demand. Critically, these demand drivers are largely uncorrelated with the macroeconomic cycles that affect copper and iron ore.

Saskatchewan hosts some of the world’s highest-quality potash deposits. The Jansen deposit benefits from exceptional ore quality and scale, characteristics that underpin the economic rationale for a project of this magnitude.

Jansen Project Progress and Timeline

- Jansen Stage 1: Located in Saskatchewan, Canada, approximately 75% complete at the end of the FY26 first half period, with a targeted production commencement of mid-2027

- Jansen Stage 2: Approximately 14% complete, with a production target of FY31

- Combined, the two stages will establish BHP as a significant player in the global potash market

Investors should understand that Jansen is a long-duration asset. It carries execution risk, cost overrun risk, and the possibility that potash market conditions may evolve between now and first production. However, once operational, it provides an earnings stream with a very different demand driver profile from iron ore and copper.

The Analyst Landscape: Reading Between the Lines of a Mixed Consensus

The current broker and analyst consensus on BHP provides a useful framework for calibrating expectations, though it should not be read as a definitive verdict.

| Metric | Current Signal | What It Means |

|---|---|---|

| Wall Street Analyst Consensus | Hold (10 analysts) | Limited near-term upside conviction |

| Average 12-Month Price Target | Approximately $62.33 | Modest implied return at current prices |

| ASX Technical Summary | Bullish on shorter timeframes | Short-term price momentum supportive |

| Zacks Rank | 3 (Hold) | Adequate value and momentum, not a screaming buy |

| Deutsche Bank Rating | Hold with raised target | Constructive but not aggressively bullish |

The divergence between fundamental analyst ratings sitting at Hold and shorter-term technical indicators showing bullish momentum is a pattern worth noting. It suggests that recent price appreciation may have absorbed much of the near-term upside that fundamental valuations would support, while momentum-driven buying continues to carry the stock higher on shorter timeframes.

For longer-term investors, the more important question is whether the commodity thesis justifies paying the current price with a reasonable margin of safety. At an average price target of approximately $62.33 from covering analysts, the near-term fundamental upside appears limited rather than compelling. For a deeper look at BHP’s current share price and market data, the ASX company page provides up-to-date figures.

The next major ASX story will hit our subscribers first

BHP vs. RIO Tinto: A Practical Comparison for ASX Investors

| Factor | BHP (ASX: BHP) | RIO Tinto (ASX: RIO) |

|---|---|---|

| Primary Commodity | Iron Ore and Copper | Iron Ore and Aluminium |

| Growth Pipeline | Copper expansion plus Jansen Potash | Lithium via Rincon plus Copper |

| Dividend Track Record | Strong, partially franked | Strong, fully franked |

| Diversification Stage | Active mid-transition | Active mid-transition |

| Secondary Demand Driver | Electrification and agriculture | Aluminium from renewable energy transition |

| Analyst Sentiment | Hold consensus | Comparable Hold bias |

Both companies are undergoing commodity portfolio transitions, and both carry similar analyst sentiment at present. The differentiation lies in the secondary commodity profile. BHP’s copper positioning is arguably more advanced and more directly tied to electrification tailwinds than Rio’s aluminium exposure, while Jansen adds an agricultural commodity angle that Rio does not replicate.

Bull Case, Bear Case, and the Honest Middle Ground

The bull case for BHP rests on three structural pillars:

- Copper earnings leverage from a price trajectory that, if sustained above US$5.00 per pound, creates disproportionate EBITDA upside at the scale BHP operates

- Iron ore price resilience continuing to outperform bearish consensus forecasts, supporting dividend sustainability above market expectations

- Potash optionality from Jansen adding a low-correlation earnings stream that could re-rate BHP’s valuation multiple once production commences

The bear case centres on equally legitimate concerns:

- Cyclicality risk: all three core commodities remain exposed to macro deterioration, particularly any significant Chinese economic slowdown

- Valuation ceiling: with analyst price targets implying limited near-term upside, the margin of safety at current prices does not suit investors seeking deep value entry points

- Jansen execution risk: a multi-decade construction programme carries inherent cost overrun and commodity timing risks

Investor Note: BHP is a cyclical business operating within a cyclical industry. Paying a full valuation for a cyclical company during a commodity upswing inherently compresses the margin of safety that long-term capital preservation depends upon. This does not mean BHP is a poor investment, but it does mean that entry price and patience matter significantly to long-term returns.

What Kind of Investor Does BHP Actually Suit?

Income investors will find BHP’s dividend track record attractive, though the sustainability of distributions at current levels depends materially on iron ore and copper prices maintaining their current trajectories. Franking credit coverage is partial rather than full, which is a consideration for Australian investors optimising for imputation credits.

Growth investors will need to assess whether the copper pipeline and Jansen development provide sufficient earnings growth to drive meaningful share price re-rating from current levels, given that analyst consensus already prices in a degree of improvement.

Long-term holders are arguably the investor category BHP suits best. The company’s commodity mix, operational scale, balance sheet strength, and development pipeline are best appreciated through a multi-year lens rather than a quarterly earnings horizon. Goldman Sachs, for instance, has previously suggested investors consider buying BHP shares, a sentiment echoed by BHP’s own chairman purchasing shares on market.

Frequently Asked Questions About the BHP Share Price

Is the BHP share price a buy right now in 2026?

BHP presents a constructive but not unambiguously compelling investment case. Copper earnings are accelerating, iron ore is outperforming bearish forecasts, and Jansen adds long-duration diversification. However, the analyst consensus sits at Hold, and the average price target of approximately $62.33 suggests limited near-term upside for investors entering at current prices. The BHP share price could be a buy for patient, long-term investors, but it is less suited to those seeking near-term capital growth or a deep-value margin of safety.

What is the analyst price target for BHP shares?

Based on available data from approximately 10 covering Wall Street analysts, the average 12-month price target sits at approximately $62.33, with the consensus rating at Hold.

Why is copper so critical to BHP’s earnings outlook?

Copper delivers exceptional earnings leverage at BHP’s operational scale. A 59% surge in copper EBITDA to US$8 billion in the FY26 first half, driven by a 32% rise in the average realised price to US$5.28 per pound, illustrates how powerfully copper price movements translate into earnings. The subsequent quarterly update showed the price rising further to US$5.47 per pound.

When will Jansen potash begin production?

Jansen Stage 1 is approximately 75% complete with first production targeted for mid-2027. Stage 2 is approximately 14% complete with a production target of FY31.

How does the iron ore price affect BHP’s dividends?

Iron ore remains BHP’s largest earnings division. A sustained price above US$100 per tonne supports dividends at current levels. A sustained decline toward US$80 to US$90 per tonne would likely pressure distributions downward.

Assessing the Investment Case Across Three Dimensions

Bringing the full picture together, the BHP investment case can be evaluated across three dimensions that matter most for long-term investors:

- Commodity quality: High. Copper, iron ore, and potash each carry long-duration, structurally supported demand profiles relevant to electrification, urbanisation, and food security

- Earnings momentum: Positive and accelerating. Copper EBITDA is growing rapidly, iron ore is ahead of consensus, and Jansen will introduce a new earnings stream from mid-2027

- Valuation discipline: Neutral to cautious. Analyst price targets suggest limited near-term upside, and cyclical businesses historically reward investors who maintain price discipline and wait for margin of safety

BHP is not a deep-value opportunity at current levels, but it is a high-quality operator with a commodity portfolio increasingly aligned with long-duration structural demand themes. For investors with a multi-year horizon and the discipline to hold through commodity price volatility, the BHP share price could be a buy worth serious consideration as part of a diversified portfolio.

This article contains general information only and does not constitute personalised financial advice. Investors should consider their own financial circumstances and consult a licensed financial adviser before making investment decisions. Past performance is not indicative of future results. All commodity prices and analyst data referenced reflect information available at time of writing and are subject to change.

Readers seeking broader perspectives on ASX mining sector analysis and general investment education may find value in exploring content available through Motley Fool Australia at fool.com.au.

Want to Spot the Next Major ASX Mineral Discovery Before the Broader Market Does?

While BHP offers exposure to structural commodity themes through copper, iron ore, and potash, significant wealth in the resources sector has historically been built by identifying transformative mineral discoveries at the earliest possible stage — exactly what Discovery Alert’s proprietary Discovery IQ model is designed to do, delivering real-time alerts on significant ASX discoveries the moment they are announced. Explore historic examples of major discovery returns and begin your 14-day free trial today to position yourself ahead of the market.