June 10, 2026

The Hidden Shift Inside the World's Biggest Mining Company

Most investors watching commodity markets focus on price charts and quarterly earnings. But underneath BHP Group Ltd's (ASX: BHP) extraordinary run over the past twelve months lies a structural transformation that tells a far more interesting story than simple price momentum. For the first time in the company's history, copper has overtaken iron ore as the dominant contributor to group earnings, a shift that redefines what kind of company BHP actually is, and whether its current valuation truly captures that identity.

Understanding this transition is central to answering the question investors are asking right now: are BHP shares still a good buy today, or has the rally already done the heavy lifting?

When big ASX news breaks, our subscribers know first

A Performance Gap That Demands Explanation

Over the past twelve months, BHP shares have climbed 58.3%, a figure that sits in stark contrast to the 0.8% return posted by the broader S&P/ASX 200 Index over the same period. That is not marginal outperformance. It is a return roughly seventy times greater than the benchmark, which makes the current entry point a question worth taking seriously. The broader ASX market performance context helps explain why BHP's gains have drawn such significant investor attention.

BHP vs. ASX 200: Key Metrics at a Glance

| Metric | BHP Group (ASX: BHP) | ASX 200 Index |

|---|---|---|

| 12-Month Share Price Return | +58.3% | +0.8% |

| Trailing Dividend Yield | 3.2% (fully franked) | ~4.0% (index avg.) |

| Dividend Franking | 100% | Varies |

| Market Cap Status | Largest stock on ASX | — |

| Recent Share Price | ~$60.92 | — |

Beyond the price return, BHP paid two fully franked dividends to eligible shareholders across this period, adding further after-tax value for Australian resident investors. The 3.2% trailing fully franked yield remains meaningful, particularly for self-managed superannuation fund (SMSF) holders who can utilise franking credit refunds to enhance effective income.

Three primary forces have driven this outperformance:

- Copper prices surged approximately 39% over twelve months, reaching around US$13,615 per tonne, fuelled by structural demand from electrification themes, AI infrastructure buildout, and global grid expansion

- Iron ore prices remained more resilient than many analysts had forecast given China's ongoing property sector challenges

- BHP's operational execution delivered a half-year earnings result that surprised on the upside

The Copper Inflection: Why This Earnings Milestone Matters

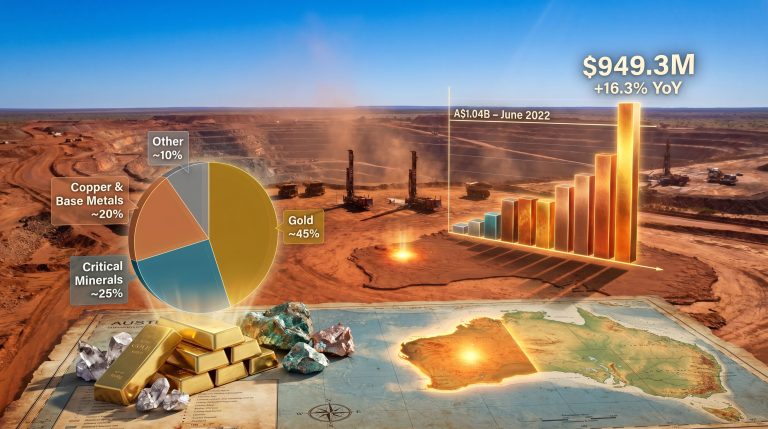

When BHP reported its first-half fiscal year 2026 results, the headline figure was compelling. Underlying earnings before interest, taxes, depreciation and amortisation (EBITDA) reached US$15.5 billion, representing a 25% increase on the prior corresponding period. That alone would have been a solid result for any major miner.

However, the figure that deserves far more attention is the commodity breakdown behind that number. For the first time in BHP's corporate history, copper contributed 51% of group EBITDA during the half. This is not a minor reshuffling of portfolio weights. It represents a fundamental change in BHP's earnings character. The ongoing copper supply crunch makes this shift even more strategically significant for long-term investors.

Historically, BHP was understood by the market as an iron ore company with diversification optionality. That framing is now genuinely outdated. Copper is no longer a supporting asset, it is the engine.

This matters for investors for several reasons that go beyond the obvious commodity price exposure:

- Copper demand is structurally tied to long-duration megatrends including electric vehicle production, renewable energy infrastructure, and data centre power systems, all of which require substantially more copper per unit of output than traditional industrial applications

- Iron ore demand is heavily concentrated in Chinese steel production, which faces well-documented structural headwinds as the country's property construction cycle matures

- A more balanced commodity mix reduces BHP's single-market concentration risk, which has historically been a key vulnerability flagged by analysts

BHP's Commodity Portfolio: Structure and Risk Assessment

| Commodity | Portfolio Role | Primary Demand Driver | Key Risk Factor |

|---|---|---|---|

| Iron Ore | Near-term earnings anchor | Chinese steel production | China macroeconomic slowdown |

| Copper | Long-term growth engine | Electrification, EVs, AI | Supply constraints, geopolitical |

| Potash (Jansen) | Future earnings optionality | Global food security | Extended development timeline |

| Metallurgical Coal | Secondary exposure | Steel manufacturing | Carbon transition pressure |

What the Copper Market Is Not Telling You

The mainstream narrative around copper focuses on demand. Every report mentions EVs, solar panels, and data centres. What receives far less attention is the supply side, and this is where the genuinely important insight lies.

New copper mine development carries an average lead time of ten to fifteen years from discovery through to commercial production. The global copper industry has chronically underinvested in new supply over the past decade, partly due to commodity price cycles that depressed capital expenditure at precisely the wrong moment. This supply deficit is not hypothetical — it is already visible in declining ore grades at major producing mines worldwide.

Copper ore grades at many of the world's largest deposits have been declining over time as high-grade surface ore bodies are progressively exhausted. Miners are processing more rock to extract the same quantity of metal, which increases both operating costs and energy consumption per tonne of copper produced. BHP's Escondida mine in Chile, the world's largest copper operation by output, has experienced this dynamic, requiring significant capital reinvestment to sustain production levels.

This geological reality creates an important asymmetry for long-term investors: even if near-term copper demand softens due to macroeconomic headwinds, structural supply constraints mean the medium-term price floor is likely higher than historical cycles would suggest.

However, there is a legitimate counter-argument worth considering. With copper up 39% in twelve months and BHP's share price up 58%, the question is not whether copper demand is real. The question is whether the market has already priced in the next several years of that narrative. That distinction is critical for investors evaluating entry timing.

Analyst Landscape: Three Divergent Views

Current broker sentiment on BHP is genuinely divided, which itself provides useful information about the level of uncertainty embedded in the current valuation.

Morgans (Hold): Morgans analyst Damien Nguyen characterises BHP as offering broad diversification across its core commodity suite, supported by what the firm describes as a strong balance sheet and a disciplined capital returns framework. The firm views copper as providing meaningful exposure to the global energy transition theme over the long term, while acknowledging that iron ore continues to drive near-term earnings. The Hold recommendation reflects the view that current valuation appears broadly fair, with the macroeconomic backdrop introducing genuine uncertainty around Chinese steel demand and global growth signals.

Alto Capital (Sell): Alto Capital's Tony Locantro takes a more cautious position, acknowledging the strength of BHP's first-half fiscal 2026 result while arguing that elevated investor enthusiasm around electrification and AI-driven copper demand has materially contributed to the share price run. The firm's view is that the combination of a strong operational result and stretched expectations creates a risk-reward profile that favours taking profits rather than adding exposure at current prices.

Morgan Stanley (Overweight): Morgan Stanley maintains a more constructive stance, carrying a price target of $67.50, which implies moderate upside from recent trading levels near $60.92. This represents the more bullish end of current analyst opinion. Furthermore, the ongoing Rio versus BHP debate among major institutions adds an additional layer of strategic context for investors comparing large-cap mining allocations.

The spread between Hold, Sell, and Overweight ratings from credible institutions reflects a genuine valuation debate, not analyst noise. When experienced mining analysts disagree this sharply, it typically signals that the market is at an inflection point rather than offering obvious value in either direction.

Structural Risks That Could Reshape the Investment Case

China's Steel Demand: The Unavoidable Variable

China accounts for approximately 55% of global steel production, and BHP's iron ore division remains deeply exposed to Chinese steel mill purchasing decisions. The structural challenge is well understood but often underappreciated in its severity. Consequently, the challenges facing China steel and iron ore markets deserve careful consideration by any investor evaluating BHP's medium-term earnings outlook.

China's property construction sector, which historically consumed enormous quantities of steel-intensive materials, has entered a prolonged adjustment phase. Unlike cyclical downturns that recover within two to three years, China's property sector contraction reflects demographic and debt dynamics that are unlikely to reverse quickly. New residential construction starts have declined significantly from their 2021 peak, and while infrastructure spending has partially offset this, the substitution is not complete. For BHP's iron ore earnings, this translates into persistent price pressure that could weigh on cash generation precisely when the market has priced in continued strength.

Global Growth Divergence and Currency Dynamics

Monetary policy divergence between major central banks introduces additional complexity. A stronger US dollar, which often accompanies Federal Reserve tightening relative to other economies, typically creates headwinds for commodity prices denominated in US dollars. For Australian investors, currency movements between the Australian dollar and US dollar also affect the translated earnings value of BHP's predominantly USD-denominated revenue.

Trade policy uncertainty, particularly around critical mineral supply chains and tariff regimes, adds a layer of geopolitical risk that is difficult to model but real in its potential impact on commodity flows and pricing. In addition, the BHP strategic pivot away from certain commodities reflects management's own response to these evolving structural pressures.

The next major ASX story will hit our subscribers first

Is BHP Still a Buy? A Framework by Investor Type

The honest answer to whether are BHP shares still a good buy today depends entirely on what kind of investor is asking the question.

| Investor Profile | Investment Case Strength | Recommended Approach |

|---|---|---|

| Long-term growth investor | Strong, copper megatrend intact | Consider staged accumulation |

| Dividend income investor | Moderate, 3.2% fully franked yield | Evaluate yield vs. alternatives |

| Value-focused investor | Weak, post-rally valuation appears fair | Wait for pullback or correction |

| Risk-averse or conservative | Weak, commodity cycle exposure remains | Underweight or avoid |

| Resources portfolio holder | Neutral, already likely a core holding | Monitor for re-rating catalysts |

The Case for Staged Accumulation

For investors who remain constructive on BHP's long-term commodity exposure but are uncomfortable committing full capital after a 58% price rally, a staged accumulation strategy offers a disciplined middle path. Rather than making a single purchase decision at current prices, investors can deploy capital in tranches over a defined period, averaging their entry price across different market conditions. This approach reduces the psychological and financial impact of buying at a cyclical peak while maintaining exposure to upside if the copper supercycle narrative continues to drive re-rating. For a broader perspective, Morningstar's valuation analysis of BHP after its recent price movements offers additional context worth reviewing.

Understanding the Franking Credit Advantage

One dimension of BHP's investment case that is frequently underappreciated by newer investors is the after-tax value of fully franked dividends. For Australian resident shareholders in lower tax brackets, and particularly for SMSF investors in pension phase who face a zero percent tax rate, fully franked dividends carry attached tax credits that can be refunded or offset against other tax liabilities. The effective yield on BHP's dividends, once franking credits are factored in, exceeds the headline 3.2% figure for many eligible investors. Those seeking a detailed breakdown of BHP's long-term buy and hold case will find further analysis worth consulting before making a final decision.

Comparing BHP to Its ASX Peers

| Company | Primary Commodity | Key Differentiator |

|---|---|---|

| BHP Group (ASX: BHP) | Iron ore, copper, potash | Scale, diversification, franked dividends |

| Rio Tinto (ASX: RIO) | Iron ore, aluminium, copper | Aluminium exposure, lithium project optionality |

| South32 (ASX: S32) | Manganese, aluminium, base metals | Broader base metals diversification |

| Mineral Resources (ASX: MIN) | Lithium, iron ore | Lithium leverage, infrastructure assets |

BHP's primary competitive advantage within the ASX resources sector is its combination of scale, commodity diversification, and balance sheet strength. No other Australian-listed miner offers comparable exposure across iron ore, copper, and potash simultaneously, with the financial capacity to sustain dividends through commodity price cycles.

Frequently Asked Questions

Why did BHP's share price rise so sharply over the past year?

Three converging forces drove BHP's 58.3% share price gain: copper prices surged approximately 39% to around US$13,615 per tonne on the back of electrification and AI infrastructure demand narratives; iron ore prices proved more resilient than expected given China's macroeconomic challenges; and BHP's first-half fiscal 2026 results delivered underlying EBITDA of US$15.5 billion, up 25% on the prior period.

What is the significance of copper reaching 51% of group EBITDA?

This milestone signals a fundamental shift in BHP's earnings composition. For most of its history, BHP was primarily an iron ore business. The copper milestone means its earnings are now more directly tied to long-duration energy transition demand, which many analysts view as more structurally durable than iron ore's China-dependent demand base.

What are the main risks of investing in BHP at current prices?

Key risks include:

- Potential softening of Chinese steel demand reducing iron ore price support

- The possibility that copper's electrification premium is already embedded in the share price

- Global macroeconomic uncertainty and monetary policy divergence affecting commodity demand

- Currency risk between the Australian and US dollars affecting translated earnings

- Limited near-term re-rating catalysts identified by some analysts

Is BHP's dividend sustainable?

BHP operates a progressive dividend policy linked to underlying earnings performance. Dividend sustainability depends primarily on iron ore and copper price levels. The current 3.2% fully franked trailing yield reflects recent earnings strength, but commodity price cyclicality means dividend levels can vary materially between periods.

Key Takeaways for Investors Evaluating BHP Today

- BHP's 58.3% twelve-month return dwarfs the ASX 200's 0.8% gain, raising legitimate questions about how much upside remains at current prices

- Copper reaching 51% of group EBITDA for the first time marks a structural transformation in BHP's earnings profile, not a cyclical event

- Underlying EBITDA of US$15.5 billion in the first half of fiscal 2026 represents one of the strongest half-year results in the company's recent history

- Analyst opinion spans Hold (Morgans), Sell (Alto Capital), and Overweight (Morgan Stanley, $67.50 price target), reflecting genuine valuation uncertainty

- Long-term investors with tolerance for commodity cycle volatility may still find BHP investable; value-focused and risk-averse investors face a less compelling entry point at current levels

- A staged accumulation approach reduces the risk of committing full capital at a potential cyclical price peak

This article contains general information only and does not constitute personal financial advice. Commodity markets and individual company share prices can move significantly in either direction, and past performance is not indicative of future returns. Investors should consider their personal circumstances and consult a licensed financial adviser before making investment decisions.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

While BHP's copper transformation illustrates just how transformative a commodity shift can be, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries the moment they are announced — turning complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their remarkable returns, then begin your 14-day free trial to position yourself ahead of the broader market.