May 22, 2026

The Cyclical Giant Reasserting Itself: Understanding BHP's Position in the Current Commodity Landscape

Commodity cycles have a rhythm that long-term investors learn to respect rather than fear. The pattern is consistent across history: periods of oversupply and compressed margins eventually give way to supply discipline, demand recovery, and a repricing of the assets that underpin industrial civilisation. Within this framework, diversified mining majors occupy a unique structural position. They are not pure commodity bets, but rather complex, multi-stream businesses that distribute risk across several demand cycles simultaneously. For investors assessing BHP shares upside potential, understanding this layered architecture is more instructive than fixating on any single commodity price move.

BHP Group Ltd (ASX: BHP) sits near the apex of this category globally, and its recent performance trajectory has reignited a debate that surfaces at regular intervals among ASX-focused investors: after a substantial run, does the fundamental case still support further appreciation, or is the market simply catching up to a story that has already played out?

When big ASX news breaks, our subscribers know first

Why BHP Remains One of the ASX's Most Closely Watched Blue-Chip Miners

The Scale Advantage: Why Size Matters in Global Mining

In mining, scale is not merely a bragging right. It translates directly into margin protection, capital access, and operational leverage that smaller producers cannot replicate. Large-scale operations allow companies like BHP to spread fixed costs across vastly higher production volumes, negotiate more favourable terms with contractors and suppliers, and absorb commodity price downturns that would render smaller operations uneconomic.

BHP's operations span multiple continents and commodity streams, encompassing iron ore, copper, coal, and the emerging potash division in Canada. This geographic and commodity breadth creates a natural hedge that single-asset or single-commodity miners simply cannot construct without significant additional capital deployment. The BHP strategic pivot toward higher-growth commodities further reinforces this structural advantage.

BHP's Position Within the ASX 200 Resource Sector Hierarchy

Within the S&P/ASX 200 Index, BHP functions as a barometer for the broader resources sector. Its weighting within the index means that institutional funds with ASX 200 benchmark mandates are structurally required to hold it, creating a persistent baseline of institutional demand regardless of short-term sentiment. This differs fundamentally from how smaller resource companies trade, where price discovery is more sentiment-driven and liquidity can evaporate during stress periods.

The resources sector within the ASX 200 is dominated by a handful of major producers, and BHP remains the most widely followed among them. Its quarterly operational reports, capital allocation decisions, and dividend announcements generate outsized market attention relative to most other ASX constituents.

How BHP's Multi-Commodity Exposure Differs From Single-Asset Miners

Single-asset miners offer concentrated exposure to one commodity and one geography. The upside during commodity booms can be spectacular, but the downside during troughs is equally amplified. BHP's multi-commodity structure means that weakness in iron ore can be partially offset by copper strength, and vice versa. The forthcoming addition of potash through the Jansen project introduces a third earnings stream with demand dynamics tied to global food production rather than industrial or energy cycles.

Structural Insight: Multi-commodity diversification within a single miner reduces earnings volatility without requiring investors to construct complex portfolios across multiple positions. This is a significant structural advantage for income-focused investors who prioritise dividend consistency.

How Has BHP Performed Against the Broader Market in 2026?

BHP vs. ASX 200: A Performance Gap Worth Examining

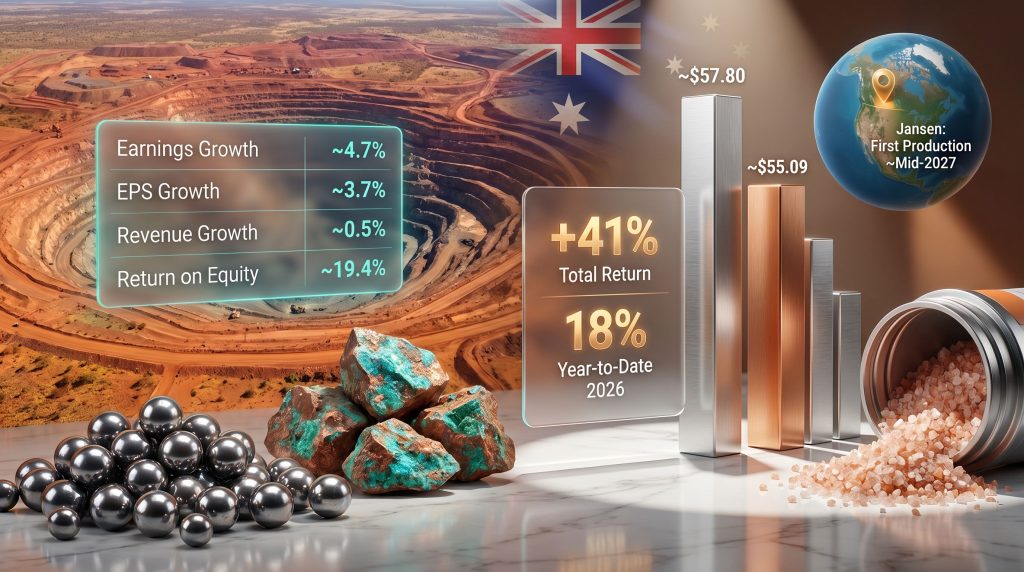

The divergence between BHP's share price trajectory and the broader ASX 200 Index over recent periods has been notable. Year-to-date in 2026, BHP shares have gained approximately 18%, including a particularly strong 7% rally during April alone. Over the trailing twelve months, the total return has reached approximately 41%, substantially outperforming the ASX 200's comparatively modest 7% gain across the same period.

| Performance Metric | BHP (ASX: BHP) | S&P/ASX 200 Index |

|---|---|---|

| Year-to-date 2026 return | ~18% | Below BHP |

| April 2026 gain | ~7% | Marginal |

| Trailing 12-month total return | ~41% | ~7% |

| Reference share price (late April 2026) | ~$54.88 | N/A |

Source: Motley Fool Australia, May 2026. Past performance is not indicative of future returns.

Breaking Down the April 2026 Rally: Momentum or Fundamentals?

The April surge warrants scrutiny. Momentum-driven rallies and fundamentally supported rallies can look identical in the short term but diverge sharply once the triggering factor resolves. In BHP's case, the April move coincided with reports of record-level iron ore production from its Western Australian operations and continued strength in copper output, both of which represent genuine operational improvements rather than speculative repositioning.

This distinction matters for investors assessing sustainability. A fundamentals-backed rally suggests the share price is reflecting improved earnings quality, which is a more durable foundation than sentiment-driven momentum. However, it also means the performance may already be partially priced in, a point reflected in the mixed analyst consensus discussed below. Furthermore, the commodity price impact on BHP's earnings quality remains a central consideration for investors weighing entry timing.

What the 12-Month Return Tells Us About Commodity Cycle Positioning

A 41% total return over twelve months from a company of BHP's size and market capitalisation is not a routine occurrence. Returns of this magnitude from large-cap mining companies typically reflect a combination of commodity price recovery, operational execution above expectations, and capital return events such as elevated dividends or buybacks. Investors considering entry at current levels should weigh whether these conditions are likely to persist or whether the period of exceptional outperformance is drawing to a close.

Investor Caution: Strong trailing returns in cyclical industries can create anchoring bias, where investors assume recent performance predicts future outcomes. In commodity-linked businesses, the opposite is often true: the conditions that generated past outperformance (rising prices, improving margins) frequently moderate after a strong run.

What Are the Current Analyst Price Targets for BHP Shares?

Analyst Consensus Summary: A Market Divided

As of late April 2026, analyst opinion on BHP shares upside potential is genuinely divided across different research platforms, with targets varying significantly depending on the source methodology, currency assumptions, and commodity price forecasts embedded in each model.

| Analytical Source | Implied Price Target | Estimated Upside / Downside | Consensus Rating |

|---|---|---|---|

| ASX-focused coverage | ~$55.09 | +9.3% from ~$49.97 | Buy |

| Broad market aggregator | ~$43.10 | Up to +42% (select analysts) | Mixed |

| NYSE-listed coverage (MarketBeat) | $48.50 to $56.00 | -12.85% to -18.51% from $55.65 | Hold / Moderate Buy |

| Zacks Investment Research | ~$57.80 | +15.32% from ~$50.12 | Between Hold and Buy (ABR 2.33) |

| TradingView analyst pool (21 analysts) | Slightly above $54.88 | Modest upside | 13 Hold / 6 Buy / 2 Sell |

Disclaimer: Analyst price targets are forward-looking estimates subject to change. They do not constitute financial advice. Always consider your personal circumstances before making investment decisions.

Why Do ASX and NYSE Analyst Targets Diverge?

The variation between ASX-listed and NYSE-listed analyst targets is not unusual for dual-listed companies but can create confusion for retail investors comparing figures across platforms. Several structural factors drive this divergence:

- Exchange-specific pricing dynamics: BHP trades as BHP Group Ltd on the ASX (in AUD) and as an ADR equivalent on the NYSE (in USD), meaning currency conversion at different rates can produce apparent price discrepancies even when underlying valuations are aligned.

- Timing differences in analyst report cycles: ASX-focused analysts typically refresh price targets more frequently in response to Australian operational updates, whereas US-based analysts may operate on quarterly review cycles tied to different reporting calendars.

- Currency conversion effects on target pricing: A shift in the AUD/USD exchange rate of 5% can translate directly into a 5% movement in implied USD targets without any change in the underlying AUD-denominated valuation model.

- Variation in analyst pool composition and methodology: Different platforms aggregate research from different broker networks, with ASX-focused pools drawing more heavily on Australian-domiciled research teams with direct operational access.

The Bull Case: Where the 27% Upside Argument Comes From

The most optimistic analyst scenarios project roughly 27% upside from late April 2026 reference levels. These forecasts are typically anchored in assumptions of copper price recovery, sustained iron ore demand outlook from Chinese steel mills, and successful execution of the Jansen potash project on schedule. The structural copper demand thesis driven by electrification and renewable energy buildout also features prominently in bull-case modelling.

The Bear Case: Why Some Forecasters See 26% Downside Risk

Conversely, the most cautious analyst forecasts point to approximately 26% downside risk. These scenarios generally assume a sustained softening of Chinese steel demand (which flows directly through to iron ore prices), potential delays or cost overruns at Jansen, and broader macroeconomic deterioration compressing commodity prices across BHP's portfolio. The fact that the bull and bear cases are almost symmetrically positioned around the current price reflects the genuine uncertainty embedded in commodity cycle forecasting. For additional context, Morningstar's solid start fiscal 2026 analysis provides a useful independent perspective on where BHP stands fundamentally.

What Operational Drivers Are Supporting BHP's Earnings Outlook?

Western Australian Iron Ore: Record Production as a Margin Anchor

BHP's Western Australian iron ore division has reached record output levels, a development that provides meaningful earnings stability even when spot iron ore prices fluctuate. The Pilbara region operations benefit from established infrastructure, long mine lives, and low strip ratios relative to many international peers, which combine to produce some of the industry's lower cash cost profiles.

Operational Highlight: Record production from Western Australian iron ore operations creates a high-volume, relatively low-cost base that shields overall group margins during periods of price softness elsewhere in BHP's commodity portfolio.

The significance of this goes beyond headline production numbers. In mining, cost positioning is the primary determinant of long-term survival and margin resilience. Producers in the lower quartile of the global cost curve remain profitable at commodity prices that render higher-cost operations uneconomic, giving them a structural advantage through the full commodity cycle.

Copper Division: Upper-Half Guidance and the Clean Energy Connection

BHP's copper operations are tracking toward the upper half of full-year production guidance, a signal of operational consistency that underpins analyst confidence in this division's contribution to group earnings. The copper supply crunch facing global markets further strengthens the strategic importance of this division. In addition, the structural importance of copper extends well beyond current production metrics:

- Copper is a central input in electric vehicle motors, wiring, and charging infrastructure, with each battery electric vehicle requiring roughly two to four times more copper than a conventional internal combustion engine vehicle.

- Utility-scale renewable energy installations, including solar farms and wind turbines, are copper-intensive relative to fossil fuel generation on a per-megawatt basis.

- Global copper supply growth has historically lagged demand growth due to long mine development timelines, grade decline at established deposits, and increasing capital intensity of new projects.

- BHP ranks among the world's largest copper producers by volume, positioning it as a significant beneficiary of structural demand growth if the energy transition continues at its current trajectory.

The Earnings Quality Argument: Why Multi-Division Consistency Matters

When multiple commodity divisions perform simultaneously, earnings quality improves significantly. The risk of a single-division shortfall dragging group results lower is reduced, cash generation becomes more predictable, and the company gains greater flexibility in capital allocation decisions. BHP's current operational position, with iron ore at record levels and copper in the upper guidance range, represents an unusually favourable alignment of its two largest earnings contributors.

Operational Cost Discipline: Protecting Margins in a High-Cost Environment

The mining industry has faced persistent cost inflation across labour, energy, and consumables since 2021. BHP's emphasis on low-cost operations and disciplined capital allocation is not merely a strategic preference but a practical necessity for margin preservation. Companies that allow cost structures to expand during periods of high commodity prices frequently face severe earnings compression when prices normalise, a dynamic that has played out repeatedly across commodity cycles.

Is BHP a Reliable Income Investment for Australian Shareholders?

Dividend History and Payout Policy Framework

For income-focused investors, BHP's dividend track record represents one of the most compelling aspects of its investment case. Key parameters of the income profile include:

- A dividend payment history spanning nearly two decades of continuous distributions.

- A structural payout policy targeting a minimum of 50% of underlying earnings, establishing a contractual-style commitment to shareholder returns rather than a discretionary approach.

- A historical dividend yield range of approximately 4% to 6%, which compares favourably to term deposit rates and many alternative ASX income opportunities.

- Fully franked dividend payments for Australian shareholders, which carry embedded tax credits that enhance after-tax yield.

The Franking Credit Advantage for Australian Retail Investors

The franking credit mechanism is a uniquely Australian tax feature that significantly enhances the effective yield of BHP dividends for eligible domestic investors. Understanding its mechanics is important:

Investor Insight: When BHP pays fully franked dividends, the company has already paid corporate tax at the prevailing rate on those earnings. Australian resident shareholders receive a credit for this pre-paid tax, which reduces their personal tax liability. For investors in the zero or low marginal tax brackets (including those in superannuation accumulation and pension phases) the franking credits can result in effective yields materially higher than the headline cash dividend would suggest.

For self-managed superannuation funds (SMSFs) in pension phase, where earnings are tax-free, franking credits can actually generate a cash tax refund from the Australian Taxation Office, making the effective yield substantially higher than the stated cash yield.

How Commodity Price Cycles Affect Dividend Variability

While BHP's payout policy provides a structural floor, the actual quantum of dividends is variable because it is tied to underlying earnings, which fluctuate with commodity prices. During periods of commodity strength, actual payouts frequently exceed the policy minimum, sometimes significantly. During commodity downturns, payouts moderate in proportion to earnings. Investors should calibrate income expectations accordingly rather than assuming the upper end of the historical yield range is a baseline.

The next major ASX story will hit our subscribers first

What Is the Jansen Potash Project and Why Does It Matter for Long-Term Upside?

Diversifying Beyond Iron Ore and Copper: The Strategic Logic

The Jansen potash project in Saskatchewan, Canada, represents BHP's most significant strategic diversification move in recent years. The rationale is compelling: both iron ore and copper are heavily tied to industrial production and infrastructure investment cycles, which means they tend to be positively correlated during macroeconomic downturns. Adding potash, a fertiliser input driven by agricultural demand and food security dynamics, introduces an earnings stream with a meaningfully different demand profile.

Agricultural commodity demand is driven by factors including global population growth, dietary shifts in emerging markets toward protein-intensive foods, and climatic pressures on crop yields. These drivers are structurally distinct from the construction and manufacturing cycles that govern iron ore and copper demand.

Jansen Project Timeline: First Production Targeted Around Mid-2027

First production from the Jansen project is currently targeted for approximately mid-2027. Saskatchewan is one of the world's premier potash jurisdictions, hosting significant portions of global potash reserves. The province has well-established mining regulatory frameworks and substantial existing industry infrastructure, which reduces development risk relative to greenfield projects in less mature jurisdictions.

Why Potash Adds a New Earnings Stream With Distinct Demand Drivers

- Global food security dynamics create relatively inelastic demand for potash as a crop nutrient, with agricultural producers needing to maintain soil fertility regardless of broader economic conditions.

- Geographic diversification into Canadian resource development reduces BHP's operational concentration in Australia and South America.

- Reduced earnings correlation with traditional metals cycles means that a global manufacturing slowdown that compresses iron ore and copper prices may have limited impact on potash revenue, providing partial earnings insulation.

Balance Sheet Strength: How Asset Sales Have Funded Future Growth

BHP has strategically divested non-core assets in recent years, generating significant cash that has been redeployed toward its highest-conviction growth opportunities, including Jansen. This approach to portfolio management reflects capital allocation discipline: rather than spreading investment thinly across a large and diverse asset base, the company has concentrated resources in areas where it sees the strongest long-term return prospects.

What Do Long-Term Fundamental Forecasts Suggest for BHP?

Modelling BHP's Growth Trajectory Over a 3-Year Horizon

Aggregated analyst modelling as of late April 2026 points to the following fundamental projections across a three-year horizon:

| Fundamental Metric | Projected Rate |

|---|---|

| Annual earnings growth | ~4.7% |

| Revenue growth | ~0.5% |

| EPS growth | ~3.7% |

| Return on equity (3-year forecast) | ~19.4% |

Source: Aggregated from publicly available analyst modelling as of late April 2026. Forward projections are estimates only and subject to material revision. This does not constitute financial advice.

What These Numbers Mean for a Cyclical Mining Investment

A projected return on equity of approximately 19.4% is notable for a company of BHP's capital intensity. Mining businesses typically require substantial ongoing capital expenditure to maintain production, replace depleted reserves, and develop new projects, all of which weigh on returns on invested capital. An ROE at this level suggests the combination of pricing power, operational efficiency, and capital discipline is generating above-average returns relative to the capital base.

The relatively modest revenue growth projection of 0.5% reflects the reality that commodity prices, rather than volume growth alone, will be the primary driver of top-line performance. Earnings growth outpacing revenue growth (at 4.7% versus 0.5%) implies analysts expect margin improvement through cost discipline and operational efficiency rather than simple volume or price expansion.

The Role of Commodity Price Recovery in Unlocking Forecast Upside

These projections carry an important caveat: they are modelled under specific commodity price assumptions that may differ materially from actual outcomes. If iron ore prices recover meaningfully from current levels, or if copper prices accelerate in response to electrification demand, actual earnings growth could significantly exceed the consensus projections. Conversely, a Chinese demand shock or global recession scenario could render these forecasts optimistic.

What Are the Key Risk Factors That Could Limit BHP's Upside?

No investment case is complete without an honest assessment of downside scenarios. Investors evaluating BHP shares upside potential should weigh the following risk factors carefully:

Commodity Price Volatility: The Unavoidable Cyclical Constraint

BHP's earnings are fundamentally linked to commodity prices that it does not control and cannot fully hedge over the long term. Iron ore, copper, and potash prices are determined by global supply and demand dynamics that can shift rapidly in response to macroeconomic events, policy changes, and technological disruptions.

China Demand Sensitivity: Iron Ore's Largest End Market

China accounts for the majority of global seaborne iron ore demand, and any sustained reduction in Chinese steel production, whether driven by property sector weakness, economic slowdown, or policy-driven decarbonisation of the steel industry, would flow directly through to BHP's largest revenue division.

Risk Callout: BHP's earnings remain highly sensitive to iron ore price movements. A sustained decline in Chinese steel demand could compress margins across its largest revenue division, potentially offsetting growth contributions from copper and potash. Investors should monitor Chinese industrial production data and property sector indicators as leading signals.

Global Macroeconomic Headwinds: Oil Prices, Inflation, and Industrial Slowdowns

Mining operations are energy-intensive, meaning that elevated energy costs create margin pressure that does not fully recover until commodity prices rise to compensate. Simultaneously, global industrial slowdowns reduce demand for BHP's outputs, creating a dual squeeze on revenue and margins.

Currency Risk: AUD/USD Dynamics and Their Impact on Reported Earnings

BHP's Australian-dollar reported earnings are affected by AUD/USD movements because most commodity sales are denominated in US dollars. A strengthening Australian dollar compresses reported AUD earnings even when USD commodity prices are stable. Conversely, a weaker AUD amplifies reported earnings growth. This currency dynamic adds a layer of complexity to earnings forecasting that is often underappreciated by retail investors focused on commodity prices alone.

Geopolitical Exposure Across Multiple Operating Jurisdictions

Operations across Australia, the Americas, and Canada introduce exposure to multiple regulatory and geopolitical environments. Changes in royalty regimes, environmental regulations, indigenous land rights frameworks, or trade policy can create project-specific risks that are difficult to anticipate and model in advance.

How Does BHP's Investment Case Compare Across Different Investor Profiles?

BHP's characteristics make it relevant across multiple investor profiles, though for different reasons:

BHP for Income-Focused Investors

The combination of a nearly two-decade dividend payment history, a structural 50% payout floor, and fully franked distributions makes BHP one of the more compelling income options within the ASX 200 resources sector. However, income investors should model for dividend variability through commodity cycles rather than assuming the upper end of the historical yield range is maintainable at all times.

BHP for Growth-Oriented Investors

The copper division's structural demand story and the Jansen potash project's earnings diversification potential provide growth angles that are not typical of mature mining companies. For investors seeking exposure to the energy transition and global food security themes within a large-cap, investment-grade structure, BHP offers a relatively low-risk entry point compared to pure-play exploration companies.

BHP for Defensive Investors

Balance sheet strength, operational scale, multi-commodity diversification, and a strong cost position within each of its major product categories give BHP defensive characteristics that smaller miners cannot match. In a market downturn, large-cap miners with strong balance sheets typically hold value better than leveraged small-cap alternatives.

BHP for SMSF Investors

The combination of fully franked dividends, a long payment history, and the potential for franking credit refunds in pension phase makes BHP particularly relevant for SMSF portfolios optimising for after-tax income. Its inclusion in a diversified SMSF portfolio aligns with blue-chip reliability and regulatory compliance requirements for prudent asset selection.

Frequently Asked Questions: BHP Shares Upside Potential

What is the current analyst consensus on BHP shares?

As of late April 2026, analyst opinion is divided across 21 surveyed analysts: approximately 13 rate BHP as a hold, six assign buy or strong buy ratings, and two recommend selling. The average 12-month price target sits modestly above recent trading levels, with a wide dispersion between the most bullish (approximately 27% upside) and most bearish (approximately 26% downside) forecasts, reflecting differing views on commodity cycle timing and China demand trajectory.

What is BHP's dividend yield and is it fully franked?

BHP's dividend yield has historically ranged between approximately 4% and 6%, with dividends typically fully franked for Australian shareholders. The company targets a minimum payout ratio of 50% of underlying earnings, though actual payouts vary with commodity price cycles.

What is the Jansen potash project and when does production begin?

Jansen is BHP's major potash development located in Saskatchewan, Canada. First production is currently targeted for around mid-2027. The project introduces fertiliser exposure as a distinct commodity stream, diversifying BHP's earnings beyond its traditional iron ore and copper base.

Why do BHP's ASX and NYSE price targets differ so significantly?

Divergence between ASX and NYSE analyst targets reflects differences in exchange-specific pricing, currency translation between AUD and USD, analyst report timing cycles, and the composition of each platform's analyst coverage pool. Investors should consider both markets when evaluating consensus, while noting that currency assumptions embedded in each target can account for a significant portion of the apparent gap.

What is BHP's year-to-date share price performance in 2026?

BHP shares have gained approximately 18% year-to-date in 2026, including a roughly 7% rise during April. Over the trailing 12 months, the stock has returned approximately 41%, substantially outperforming the broader ASX 200 Index's approximately 7% return over the same period. Motley Fool Australia's coverage of BHP's April gains provides further context on what has driven this outperformance.

The Verdict: Does BHP's Fundamental Profile Justify Further Upside?

Synthesising the Bull and Bear Arguments

The honest conclusion is that BHP's investment case at current levels is neither obviously compelling nor obviously overvalued. The operational foundation is strong, with record iron ore production and copper guidance tracking well. The long-term structural demand thesis for copper is credible and well-supported by independent energy and vehicle electrification research. The Jansen project adds genuine diversification. The dividend track record and franking credit structure provide meaningful income support for Australian investors.

Against these positives, the 41% trailing return has already incorporated much of the good news. Analyst consensus is balanced, with a slight lean toward hold over buy, and the symmetric bull/bear target range suggests the market views further material upside as contingent on positive commodity cycle developments rather than guaranteed by operational factors alone.

Three Scenarios for BHP Shares Over the Next 12 Months

| Scenario | Key Assumption | Implied Direction |

|---|---|---|

| Bull case | Copper demand accelerates; iron ore prices stabilise; Jansen progresses on schedule | Meaningful upside toward upper analyst targets (~27%) |

| Base case | Commodity prices range-bound; operational consistency maintained; Jansen on track | Modest appreciation aligned with consensus targets (~9-15%) |

| Bear case | Chinese steel demand slows materially; global recession risk rises; AUD strengthens | Retracement toward lower analyst price targets (~26% below current) |

What Long-Term Investors Should Monitor Going Forward

Investors with existing or prospective positions in BHP should track the following indicators as leading signals for each scenario:

- Quarterly operational reports and any revisions to production guidance across iron ore, copper, and coal divisions.

- Iron ore and copper spot price trends as published by the London Metal Exchange and relevant Chinese commodity exchanges.

- Jansen project construction milestones and any updates to the mid-2027 first production target.

- Capital return announcements including interim and final dividend declarations and any buyback programs.

- Macro indicators from China's industrial and property sectors, particularly steel production volumes and property new starts data.

- AUD/USD exchange rate movements, particularly given their direct impact on BHP's AUD-reported earnings.

Disclaimer: This article contains general financial information only and does not constitute personal financial advice. BHP shares carry risks including but not limited to commodity price volatility, currency movements, and macroeconomic uncertainty. Past performance is not indicative of future results. Investors should consult a licensed financial adviser before making investment decisions. Price targets and analyst forecasts referenced are forward-looking estimates subject to material revision.

Want to Catch the Next Major ASX Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly turning complex mineral data into actionable insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.