July 10, 2026

The World's Smallest Critical Mineral Market Has a Very Large Problem

Consider what happens when a single company consumes nearly three-quarters of everything the world produces of a given mineral. Not a large market like copper or lithium, where thousands of buyers distribute demand across dozens of producing nations, but a market so small that its entire annual output could fit inside a standard shipping container. That is the reality of scandium, and understanding it is essential to grasping why the Bloom Energy scandium supply chain has become one of the most consequential stories in US advanced manufacturing today.

The controversy surrounding Bloom Energy is not simply a corporate governance dispute or a short-seller skirmish. It is a window into a structural vulnerability that sits beneath the surface of America's clean energy ambitions: the dependence on ultra-niche critical minerals demand that are almost entirely processed in China, that appear in no major government funding program, and that cannot be replaced without fundamentally degrading the technology they enable.

When big ASX news breaks, our subscribers know first

What Makes Scandium So Difficult to Replace

Scandium occupies an unusual position in the periodic table and in industrial chemistry. It is classified as a rare earth element by some regulatory frameworks but is technically a transition metal, and its properties do not correspond neatly to either category. What matters for the fuel cell industry is a specific characteristic: when scandium oxide is introduced as a dopant into the electrolyte layer of a solid oxide fuel cell, it dramatically increases the speed at which oxygen ions can move through the electrolyte at a given temperature.

This ionic conductivity enhancement is not a marginal improvement. It allows SOFCs to operate efficiently at temperatures several hundred degrees lower than they otherwise could, which extends the lifespan of surrounding components, reduces thermal stress, and improves overall system durability. For a company selling fuel cells into data centre infrastructure where uptime and longevity are non-negotiable, these performance characteristics translate directly into competitive advantage.

The substitution problem is equally stark. Yttria, or yttrium oxide, is the most commonly proposed alternative dopant for SOFC electrolytes, and it performs adequately at higher operating temperatures. However, shifting away from scandia-stabilised zirconia electrolytes to yttria-stabilised equivalents would require reformulating the entire electrolyte architecture, requalifying the technology with customers, and accepting measurable performance trade-offs at the operating temperatures where Bloom's products are designed to run. This is not a six-month engineering exercise.

How Scandium Compares to Other Critical Minerals

| Mineral | Annual Global Consumption | Primary Use Case | China's Market Share |

|---|---|---|---|

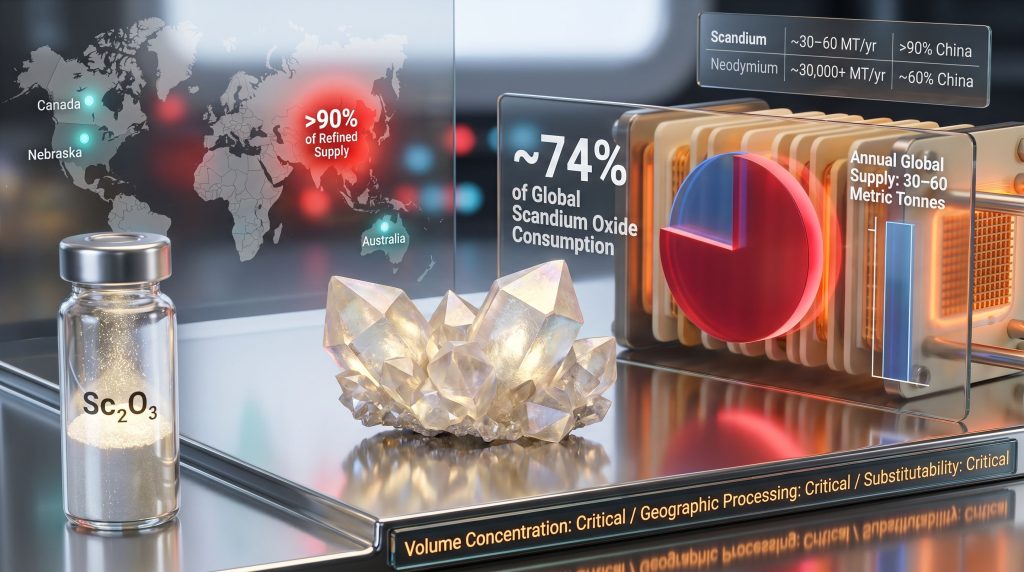

| Scandium | ~30–40 metric tonnes | SOFCs, aerospace alloys | >90% of refined supply |

| Gallium | ~300 metric tonnes | Semiconductors, LEDs | ~80% |

| Germanium | ~130 metric tonnes | Fibre optics, IR optics | ~60% |

| Neodymium | ~30,000+ metric tonnes | Permanent magnets | ~60% |

Key Insight: Total global scandium oxide consumption sits at just 30 to 40 metric tonnes per year according to US Geological Survey data. This means the entire annual market is smaller than the cargo capacity of a single heavy-lift truck convoy. A single large-scale buyer can, and in this case does, reshape the entire market's supply-demand equation unilaterally.

The Concentration Problem at the Heart of the Bloom Energy Scandium Supply Chain

Bloom Energy is estimated to consume approximately 74% of global scandium oxide supply annually. This figure is not widely appreciated outside specialist circles, but its implications are enormous. When one company accounts for nearly three-quarters of demand in any commodity market, its procurement decisions become the market. Its inventory cycles become price signals. Its technology roadmap becomes a de facto production planning input for every supplier on the planet.

This creates a paradox that is almost unique in industrial commodity markets. Bloom is simultaneously the world's largest buyer of scandium and the entity most exposed to supply disruption if the market fails to grow alongside its ambitions. The company's stated goal of scaling toward 25 GW of annual fuel cell production capacity would, at current consumption ratios, require roughly 220 tonnes of scandium oxide per year at the 5 GW milestone alone. Total global supply under optimistic projections sits at around 240 tonnes by 2030. The arithmetic is uncomfortable.

Projected Supply and Demand Scenarios to 2030

| Scenario | 2030 Estimated Demand | 2030 Projected Supply | Supply Gap |

|---|---|---|---|

| Business-as-usual (SOFC focus) | ~38 tonnes | ~60–80 tonnes | Manageable |

| Accelerated SOFC + EV lightweighting | ~260 tonnes | ~240 tonnes | Critical shortage |

| Full EV adoption of Al-Sc alloys | ~5,300 tonnes | <500 tonnes | Severe structural deficit |

The aerospace and defence sector adds a further complication. Aluminium-scandium alloys, which benefit from the same strength-to-weight enhancement properties that make scandium valuable in fuel cells, are attracting serious attention from manufacturers including Lockheed Martin for fighter jet applications. Furthermore, the sixty-tonne supply problem affecting the US defence industrial base illustrates how these alloys have been tested by Formula One teams seeking weight reduction without structural compromise. As defence procurement ramps up, the fuel cell sector faces growing competition for a supply base that is already insufficient to meet either sector's growth projections independently.

China's Structural Dominance and the Export Licensing Escalation

China has spent decades systematically building its capacity to recover and process scandium from industrial waste streams, particularly from titanium dioxide, nickel, cobalt, and uranium processing operations where scandium appears as a trace byproduct. This patient, incremental approach to capacity building now gives Chinese producers, led by firms such as Hunan Oriental Scandium, control over more than half of global fuel-cell-grade scandium oxide supply by that company's own account, with total Chinese refined output representing well over 90% of global refined scandium chemical production across all grades.

In April 2025, Beijing formalised this leverage by adding scandium to its strategic mineral export licensing regime, placing it alongside gallium, germanium, and select rare earth elements that had already been subject to similar controls. China's export controls on scandium mean that any company sourcing Chinese-origin material now faces regulatory risk that did not exist before: export approvals can be delayed, conditioned, or withheld as a function of broader trade policy, regardless of the commercial relationships between buyer and supplier.

This is not a theoretical risk. China has demonstrated willingness to use export licensing mechanisms as a trade policy instrument across multiple mineral categories over the past several years. For manufacturers dependent on Chinese-processed scandium, the April 2025 designation represents a structural change in the risk profile of their supply chains, not simply an administrative adjustment.

The Short-Seller Report and the Transparency Controversy

In July 2026, Hunterbrook Media, working alongside its affiliated investment vehicle Hunterbrook Capital which holds a short position in Bloom Energy, published an investigation alleging that the Bloom Energy scandium supply chain contains at least four distinct pathways back to Chinese-origin material. The report drew on global trade data, Chinese corporate filings, satellite imagery, and direct conversations with suppliers in China.

The specific allegations included:

- A Korean electrolyte substrate manufacturer that sources scandium powder from China, processes it into ceramic substrates, and exports the finished material to the United States, effectively transforming the geographic origin classification of the material through an intermediate manufacturing step

- A supplier identified as KV Materials, alleged to be owned by Vital Thin Film Materials, a Chinese company, which supplied Bloom with electrolyte raw materials

- The broader Vital Group, including its US subsidiary Vital & FHR North America, reportedly featured at Bloom's own supplier conference in May 2026 alongside Hunan Oriental Scandium and Three Circle, two entities that are openly Chinese-origin suppliers

- Trade records cited in the investigation reportedly showing Bloom receiving shipments from a Chinese-linked supplier as recently as July 8, 2026, the day before the report was published

Bloom's response was direct. The company described the report as false and misleading, reaffirmed in a regulatory filing that its supply is not dependent on China, and stated that its supply chain architecture can support 25 GW of annual fuel cell production capacity. Bloom's Chief Operating Officer noted publicly that the company deliberately keeps its sourcing network confidential to protect the resilience of its supply chain from competitive intelligence gathering.

Analytical Framing: The central question is not whether Bloom intentionally deceives investors. It is whether the multi-tier architecture of modern industrial supply chains makes it structurally possible for a company to genuinely believe its inputs are geographically diversified while remaining materially dependent on Chinese-origin processing through intermediary steps that obscure the origin of the underlying material.

This dynamic, known in supply chain risk management as tier-N opacity, is well documented across semiconductor, pharmaceutical, and rare earth supply chains. The scandium situation may represent one of its most concentrated manifestations in the energy sector.

Where Non-Chinese Scandium Can Come From

The alternative supply landscape for scandium is real but immature. Several projects are advancing toward commercial production, though the timeline gap between current availability and projected demand creates a dependency window that cannot be wished away through policy announcements alone.

Current and Developing Non-Chinese Sources

- Rio Tinto (Sorel-Tracy, Quebec, Canada): The most commercially advanced non-Chinese source in the Western Hemisphere, recovering scandium as a byproduct of titanium dioxide processing. This operation represents the benchmark for what byproduct recovery economics can look like outside China.

- NioCorp Developments (Elk Creek, Nebraska, USA): The recipient of a $10 million Pentagon contract awarded in 2025 to develop scandium production alongside niobium and titanium. The project remains pre-production, and the Pentagon contract, while symbolically significant, represents a modest capital commitment relative to the infrastructure required for commercial-scale output.

- Sunrise Energy Metals (Australia): Advancing a development-stage project specifically targeting scandium supply diversification for fuel cell manufacturers, with Australia's resource endowment offering geological scale that smaller projects cannot match.

- ElementUS and Scandium International Mining Corp.: Additional project-stage developers that contribute to a projected pipeline of up to 1,800 tonnes of annual capacity by 2030, though this figure assumes all proposed projects advance simultaneously to full production, a scenario that carries substantial execution risk.

The Timeline Problem

What these projects share is a gap between aspiration and deliverable supply. Most are multiple years from meaningful production volumes, leaving a structural window between approximately 2025 and 2028 during which Chinese producers remain the only commercially scalable source of fuel-cell-grade scandium oxide. No combination of policy rhetoric, Pentagon contracts, or junior miner investment can close this window quickly. The metallurgical processing infrastructure, the product qualification requirements for SOFC-grade material, and the capital intensity of scaling production all impose timelines that optimistic projections consistently underestimate.

A less commonly appreciated factor is the grade and purity threshold required for SOFC applications. Scandium oxide intended for fuel cell electrolytes must meet exceptional purity standards, typically exceeding 99.99% oxide purity, to ensure consistent ionic conductivity performance across the electrolyte layer. Not all scandium recovery processes can achieve this specification economically, and the qualification process for new suppliers entering the SOFC market is rigorous and time-consuming. This purity barrier further narrows the pool of credible alternative suppliers beyond what raw production volume projections suggest.

The next major ASX story will hit our subscribers first

The Policy Gap That No One Is Talking About

The Trump administration's critical minerals initiative has directed substantial funding toward rebuilding domestic supply chains, with priority allocation toward lithium, copper, and rare earth elements that appear in consumer electronics, electric vehicles, and defence magnets. These are high-volume markets where investment can move the needle at scale.

Scandium does not fit this framework. Its annual global market is measured in tens of tonnes, not thousands. Its primary industrial application, SOFC electrolytes, serves a specialised energy sector rather than a mass consumer market. Its geopolitical significance is concentrated in a single company's supply chain rather than distributed across a broad industrial base. In addition, energy transition minerals that lack mass-market scale tend to fall below the threshold of most large-scale policy interventions, despite their outsized strategic importance to the specific advanced manufacturing sectors they serve.

The result is a commercial vacuum. Chinese producers are structurally positioned to fill demand during the critical dependency window not because of any deliberate strategic master plan but simply because they built the capacity, they have the technical expertise, and no Western alternative is yet commercially ready to replace them at the required purity grade and volume.

A Framework for Assessing Supply Chain Dependency Risk

The Bloom Energy scandium supply chain provides a useful template for evaluating critical mineral exposure across the broader advanced manufacturing sector. Five dimensions of risk should be considered together rather than in isolation:

Risk Assessment Framework for Critical Mineral Dependency:

- Volume concentration risk – Does a single buyer represent more than 50% of global consumption?

- Geographic processing concentration – Does one country control more than 80% of refining capacity?

- Intermediary opacity – Are multi-tier supply chains obscuring the true geographic origin of materials?

- Substitutability – Can the material be replaced without significant performance degradation?

- Policy coverage – Is the mineral included in government diversification funding programs?

Scandium scores critically on all five dimensions simultaneously. This is what distinguishes it from minerals like lithium or copper, where geographic concentration is high but substitution pathways exist, policy coverage is substantial, and no single buyer commands a dominant market share. Consequently, understanding geopolitical mining risks of this nature is becoming essential for any investor or policymaker engaged with advanced energy technology.

What Investors Need to Understand

Bloom Energy shares appreciated by nearly 1,000% in the twelve months preceding the July 2026 controversy, driven by surging demand for reliable power infrastructure in data centre buildouts. The stock fell 5.7% on July 9, 2026, closing at $254.29, before recovering approximately 3.1% in the following session as investors weighed the allegations against Bloom's regulatory filings and public rebuttal.

Analysts at Baird Equity Research maintained a buy recommendation, arguing that the supply constraint identified in the report is a challenge the supply chain has been working to address over an extended period. This view, while reflecting a reasoned assessment of near-term business continuity, does not directly engage with the transparency allegations at the centre of the controversy. Whether Bloom's supply chain works is a separate question from whether its geographic origin disclosures are accurate.

For investors, the broader lesson extends well beyond Bloom. Companies operating at the frontier of advanced energy technology frequently depend on material inputs so specialised and so geographically concentrated that standard supply chain due diligence frameworks are insufficient to capture the actual risk exposure. When those inputs are subject to Chinese export licensing controls, processed through multi-tier intermediary networks that obscure geographic origin, and consumed at volumes that strain the capacity of the entire global market, the risk profile is qualitatively different from anything that appears in a standard critical mineral risk matrix.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking projections regarding scandium supply, demand, and pricing involve significant uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct their own due diligence and consult qualified financial advisors before making any investment decisions related to companies or sectors discussed in this article.

Want to Track the Next Critical Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the complexity of ultra-niche critical minerals like scandium to surface actionable opportunities the moment they are announced — so explore Discovery Alert's discoveries page to understand how major mineral finds have historically generated extraordinary returns, and begin your 14-day free trial today to position yourself ahead of the market.