August 6, 2026

The Geological Paradox Sitting at 3,600 Metres Above Sea Level

Few mineral endowments in the world present as stark a contradiction as Bolivia's lithium reserves. The country sits atop the single largest national concentration of lithium on Earth, yet contributes less than 1% of global supply. Understanding why that gap exists, and whether the investment wave now sweeping into Bolivia can close it, requires moving beyond simple narratives about political will or resource nationalism.

The answer lies at the intersection of brine chemistry, constitutional architecture, infrastructure gaps, and the maturation of extraction technology that simply did not exist at commercial scale a decade ago. Bolivia lithium and potassium investment in 2026 is not a story about discovering new reserves. It is a story about whether the convergence of capital, technology, and institutional reform can finally unlock what geology placed there millions of years ago.

When big ASX news breaks, our subscribers know first

What Makes Bolivia's Reserves Both Extraordinary and Extraordinarily Difficult

The Chemistry Problem That Maps Don't Show

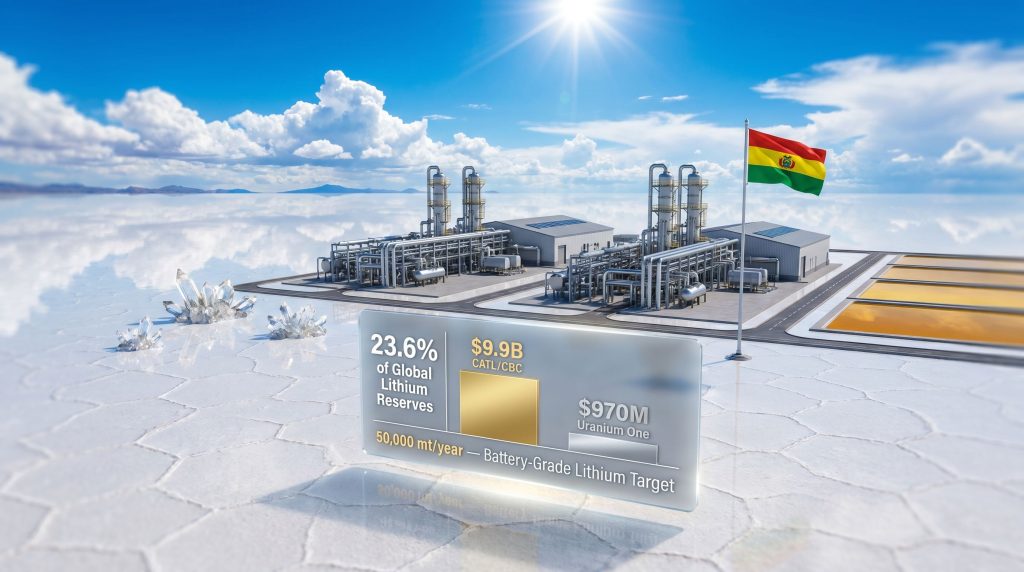

When reserve estimates are published, they convey scale but rarely convey extractability. According to the United States Geological Survey (USGS) Mineral Commodity Summaries, Bolivia holds approximately 21–23% of identified global lithium reserves, concentrated primarily in the Salar de Uyuni and the Salar de Coipasa salt flats. These figures position Bolivia among the largest lithium reserves in the world, ahead of Australia, Chile, and Argentina in raw reserve terms.

However, reserve size and extraction viability are entirely different categories of information. The brine at Uyuni presents a specific geochemical challenge that has historically undermined conventional processing approaches. Published geological analyses indicate that the magnesium-to-lithium ratio in Uyuni brine is approximately 6:1, compared to roughly 1:2 in Chile's Atacama salt flat. This matters profoundly because magnesium and lithium behave similarly during evaporation, co-precipitating together and creating costly separation problems downstream.

The salt flat's position at 3,656 metres above sea level compounds operational complexity. Equipment performance degrades under low atmospheric pressure, energy costs increase, and worker productivity faces altitude-related constraints that lower-elevation operations avoid entirely. These are not insurmountable barriers, but they do mean that Bolivia's lithium is genuinely harder to produce than reserve maps suggest.

The Seasonal Factor Conventional Analysis Frequently Ignores

Uyuni experiences a pronounced austral summer wet season running from approximately November through March. During this period, the salt flat floods periodically, which not only disrupts brine concentration in conventional evaporation ponds but also physically restricts access to pond infrastructure. Traditional evaporation-based lithium brine extraction relies on 12 to 24 months of progressive solar concentration, and seasonal flooding resets that process in ways that substantially reduce annual effective operating time.

This seasonal disruption is one of the least-discussed structural barriers in mainstream analysis of Bolivia's lithium potential, yet it is a primary reason why technology selection matters so acutely in this specific geological context.

Potassium: The Underappreciated Second Commodity

The Salar de Uyuni contains not only lithium but also substantial potassium concentrations within the same brine solution. Potassium, in the form of potash (potassium chloride or potassium sulfate), is a critical agricultural input with structurally resilient demand driven by global food production intensification.

The strategic importance of potassium as a companion mineral in Bolivia's resource agenda is frequently underweighted in external analysis. Because both lithium and potassium are present in the same brine stream, processing infrastructure for one mineral can be partially shared with the other. This co-extraction model has the potential to materially improve the unit economics of Uyuni operations by distributing fixed infrastructure costs across two separate revenue-generating products simultaneously.

Bolivia's 2026 mineral strategy is not simply an acceleration of lithium production. It represents a deliberate repositioning of the national export base around two globally critical inputs: lithium for energy transition and potassium for agricultural food security supply chains. The dual-commodity structure provides meaningful exposure to different demand cycles and different buyer geographies.

Global potash demand has been structurally reinforced since 2022, when geopolitical disruptions to Russian and Belarusian potash exports created urgent supply diversification pressures across agricultural importing nations in Asia, Africa, and Latin America. Bolivia's brine-based potassium resource could, furthermore, position the country as a supplier of both minerals to regions actively seeking alternatives to concentrated export sources, as outlined in Bolivia's evolving lithium plans.

The Capital Stack: Who Is Financing Bolivia's Mineral Ambitions

China's Multi-Billion Dollar Commitment Through CATL

The anchor investment in Bolivia's lithium development program comes from China's Contemporary Amperex Technology Ltd. (CATL), the world's largest battery manufacturer by production volume, operating through its subsidiary CBC Investments. The initial phase involves the construction of two lithium carbonate processing plants at the Salar de Uyuni, with combined nameplate capacity of approximately 35,000 metric tonnes per year, deploying Direct Lithium Extraction technology with projected recovery rates of approximately 80%.

Bolivia's state lithium entity, Yacimientos de Litio Bolivianos (YLB), retains a 51% majority ownership stake in these facilities, consistent with constitutional requirements that all mineral resource production remain under state majority control. The structure means CATL operates as a minority technology and capital partner rather than as an independent operator.

CATL's total projected investment across the full value chain, including downstream battery-grade processing capacity at the Uyuni and Coipasa salt flat facilities, is reported at approximately $9.9 billion at full buildout, targeting 50,000 metric tonnes of battery-grade lithium annually. These figures are drawn from BNamericas reporting (May 2026) and have not been independently confirmed through official CATL filings at the time of publication.

For context, CATL's strategic motivation extends beyond securing lithium feedstock. Vertical integration into upstream processing provides the company with more direct cost control over one of battery manufacturing's most significant input categories, reduces dependency on third-party lithium suppliers in Chile and Argentina, and insulates production economics from spot market price volatility.

| Investment Phase | Investor | Capital Commitment | Annual Capacity Target |

|---|---|---|---|

| Phase 1: Plant Construction | CATL/CBC | ~$1 billion | 35,000 mt/year |

| Full Value Chain Buildout | CATL/CBC | ~$9.9 billion | 50,000 mt/year |

| Russian Processing Plant | Uranium One Group | ~$970 million | 14,000 mt/year |

| State-Owned YLB Plant | YLB (Bolivia) | State-funded | 15,000 mt/year |

Russia's Industrial Entry: Uranium One Group

A second major capital commitment comes from Uranium One Group, a subsidiary of Russia's state atomic energy corporation Rosatom. Uranium One signed a reported $970 million contract to construct a dedicated lithium carbonate processing facility with nameplate capacity of 14,000 tonnes per annum.

Uranium One's entry into lithium processing represents a notable business diversification for an entity historically focused on uranium mining. The strategic context is significant: following the geopolitical isolation resulting from Russia's 2022 invasion of Ukraine and subsequent Western sanctions, Russia has actively pursued industrial partnerships across Latin America, Africa, and Asia. Bolivia's lithium sector offers Rosatom an opportunity to participate in a globally critical supply chain that is largely insulated from Western capital restrictions.

The Russian investment adds a genuinely multi-polar dimension to Bolivia's capital stack, creating a structure in which Chinese and Russian capital are both embedded in a resource sector that Western capital has found structurally difficult to access under Bolivia's constitutional framework.

YLB's Independent Production Baseline

Bolivia's own state entity inaugurated a 15,000 mt/year lithium carbonate processing plant in December 2023, establishing a domestic production foundation independent of foreign partnerships. YLB's stated production ambition is to reach 49,000 tonnes of lithium carbonate per year within three years of 2024, according to statements attributed to YLB leadership.

It is worth noting that reaching 49,000 tonnes by approximately 2027 would require YLB's existing state-funded facility to operate at or near nameplate capacity while simultaneously ramping up foreign partner facilities. Historical lithium processing ramp-up data suggests new facilities typically operate at 60–70% of nameplate capacity during year one and reach 85–90% by year three, making the timeline ambitious by industry standards.

Direct Lithium Extraction: The Technology That Changes Bolivia's Equation

Why Conventional Methods Were Always Poorly Suited to Uyuni

The conventional lithium extraction model relies on solar evaporation in large, shallow, lined ponds where concentrated brine is progressively concentrated over 12 to 24 months as water evaporates. The lithium-enriched concentrate is then chemically processed into lithium carbonate or lithium hydroxide. This approach achieves recovery rates of 40 to 60% under optimal conditions in low-impurity brines like those found in Chile's Atacama.

At Uyuni, the elevated magnesium-to-lithium ratio fundamentally undermines this model. Magnesium hydroxide precipitates preferentially during evaporation, making separation from lithium-bearing compounds more costly and chemically intensive. Combined with the wet season disruption and the logistical challenge of managing very large pond areas at high altitude with limited road infrastructure, conventional evaporation was never a strong technical fit for Bolivia's brine profile.

How DLE Addresses Bolivia's Specific Geochemical Profile

Direct lithium extraction bypasses the multi-year evaporation cycle by selectively extracting lithium ions directly from brine solutions using sorbent materials, ion exchange membranes, or solvent extraction systems depending on the specific technology variant deployed. The brine is passed through the extraction medium, lithium is selectively captured, and the depleted brine is returned to the subsurface aquifer.

| Metric | Conventional Evaporation Ponds | Direct Lithium Extraction (DLE) |

|---|---|---|

| Processing Time | 12–24 months | Days to weeks |

| Recovery Rate | 40–60% | Up to 80% |

| Water Consumption | Very high | Significantly lower |

| Suitability for High-Mg Brines | Poor | Strong |

| Environmental Footprint | Large surface area required | Compact, contained systems |

| Capital Intensity | Lower upfront | Higher upfront, lower operating cost |

| Wet Season Sensitivity | High | Low |

For Bolivia specifically, DLE offers three distinct advantages over evaporation ponds:

-

Magnesium selectivity: Modern DLE sorbent systems can be engineered to preferentially capture lithium while leaving magnesium largely in solution, significantly reducing downstream purification costs.

-

Seasonal independence: DLE systems are enclosed and do not rely on solar evaporation, meaning they can operate through the Uyuni wet season without production interruption.

-

Surface footprint reduction: DLE requires a fraction of the land area needed for evaporation ponds, reducing environmental impact on the ecologically sensitive salt flat ecosystem and limiting the regulatory risk associated with large-scale surface disturbance.

DLE technology is not a generic improvement over evaporation ponds. It is specifically well-suited to brines with high impurity ratios and climates with significant seasonal precipitation. Bolivia's brine profile is, in a counterintuitive way, one of the more compelling use cases for DLE in the global lithium industry.

The 80% recovery rate projected for CATL's DLE deployment represents a substantial improvement over what conventional evaporation would realistically achieve in Uyuni's geochemical environment. However, it should be noted that DLE technology is still maturing at commercial scale, and projected recovery rates should be evaluated as targets rather than guaranteed outcomes until operational data from commissioned facilities is available.

The Structural Barriers That Capital Alone Cannot Solve

Constitutional Architecture and Its Investment Implications

Bolivia's Political Constitution (2009) mandates in Article 348 that all mineral resources form part of the national patrimony and must remain under permanent state ownership. Foreign investors can participate only through joint venture structures in which YLB holds at minimum a 51% majority stake.

This constitutional constraint has several practical investment implications that are rarely explained in mainstream analysis:

-

Administrative contracts cannot be transferred or used as collateral, which eliminates standard project finance structures that rely on asset-backed lending.

-

Minority partners cannot independently offtake production without state approval, limiting supply chain certainty for foreign investors.

-

YLB retains operational control rights, meaning foreign technology partners must work within a governance structure that may not prioritise production efficiency above other state objectives.

-

Contract disputes must be resolved through domestic Bolivian legal channels, as Bolivia withdrew from international arbitration frameworks, removing the treaty-based investor protection mechanisms that institutional capital typically requires.

The Investor Protection Gap

Bolivia's withdrawal from the International Centre for Settlement of Investment Disputes (ICSID) in 2007 removed access to the most widely used international arbitration mechanism for sovereign resource disputes. This absence is a genuine structural deterrent for institutional capital allocators, pension funds, and publicly listed mining companies operating under fiduciary obligations that require demonstrable risk mitigation pathways.

The result is a self-selecting investor pool: entities with higher risk tolerance, strategic non-financial motivations (such as supply chain security), or state backing of their own are better positioned to accept Bolivia's investment terms than commercially disciplined private capital. Consequently, investing in Bolivia's lithium sector remains structurally challenging for Western institutional investors without significant reform.

| Risk Category | Specific Challenge | Impact Level |

|---|---|---|

| Technical | High magnesium impurities in brine | High |

| Climatic | Wet season disruption to operations | Medium |

| Market | Sustained global lithium price weakness | High |

| Political | Civic opposition to foreign contract terms | Medium |

| Institutional | Historical governance concerns at YLB | Medium-High |

| Regulatory | No international arbitration access | High |

| Financial | No collateral use of administrative contracts | High |

Market Timing and the Lithium Price Challenge

The acceleration of Bolivia's bolivia lithium and potassium investment program in 2025 and 2026 coincides with a period of sustained lithium price weakness globally. Battery-grade lithium carbonate prices retreated significantly from their 2022 peaks, trading at multi-year lows through 2024 and 2025 as production from Australia, Chile, and Argentina exceeded near-term demand growth. This reflects a broader lithium market downturn driven by oversupply and shifting demand dynamics.

This creates a genuine economic tension. DLE technology carries higher upfront capital costs than conventional evaporation infrastructure. When commodity prices are compressed, the payback period for high-capital-intensity facilities extends, and the internal rate of return on invested capital deteriorates. Projects that are economically marginal at mid-cycle pricing become more financially vulnerable if commissioning coincides with continued price weakness. This risk is particularly relevant for Bolivia's program, as facilities that break ground in 2025–2026 may not reach full production until 2028–2030 or later.

Bolivia vs. Its Lithium Triangle Neighbours

Why Smaller Reserves Produced Larger Outputs

Chile and Argentina have converted meaningfully smaller reserve bases into dominant production positions because their regulatory frameworks actively attract and protect private capital. Chile's lithium production, primarily from SQM and Albemarle operations in the Atacama, represents approximately 25% of global supply despite holding a smaller reserve base than Bolivia. Argentina's PUNA region is expanding rapidly under a largely open investment model.

| Dimension | Bolivia | Chile | Argentina |

|---|---|---|---|

| Known Lithium Reserves | ~21-23% of global total | ~11% of global total | ~10% of global total |

| Current Production Share | Under 1% of global supply | ~25% of global supply | ~5% of global supply |

| Primary Extraction Method | DLE (transitioning) | Evaporation ponds | Mixed (DLE expanding) |

| Private Investment Access | Restricted (51% state minimum) | Partially liberalised | Largely open |

| International Arbitration | Withdrawn | Active | Active |

| Brine Complexity | High (Mg impurities) | Moderate | Variable |

The core lesson from the comparative regional picture is that geological endowment is a necessary but insufficient condition for production leadership. Regulatory design, investor protection, and operational flexibility are the variables that determine which reserves become producing assets and which remain geological inventory. Furthermore, the shifts reshaping the global lithium market are placing additional pressure on all producing nations to improve their competitive positioning.

Bolivia's current investment acceleration is essentially an attempt to substitute state-directed capital from strategic partners for the private institutional capital it cannot attract under its existing constitutional framework.

The next major ASX story will hit our subscribers first

The Road Ahead: Near-Term Catalysts and Long-Term Conditions

Milestones to Watch Through 2027

Several concrete developments will serve as meaningful indicators of Bolivia's ability to translate investment commitments into operational output:

-

Commissioning progress on CATL's initial two DLE processing plants at Uyuni, including first production volumes and actual recovery rate performance against the 80% target.

-

Uranium One Group's construction timeline and any disclosed commissioning schedule for the 14,000 tonne per annum facility.

-

YLB's demonstrated production against the 49,000 tonne three-year target, particularly the utilisation rate of the existing state-funded facility.

-

Outcomes of ongoing negotiations with European and Australian companies, which would signal whether Bolivia is successfully diversifying beyond Chinese and Russian capital.

-

Advancement of potassium co-extraction pilot programs and whether dual-mineral processing economics prove out at meaningful scale.

What Structural Reform Would Unlock Bolivia's Full Potential

Capital commitment alone will not resolve Bolivia's production gap. Realising the country's full bolivia lithium and potassium potential over the long term would likely require:

-

Investor protection reform, including potential re-engagement with international arbitration mechanisms or bilateral treaty structures that provide risk mitigation for institutional capital.

-

Operational flexibility, potentially through regulatory adjustments that permit greater technical autonomy for foreign technology partners without requiring changes to the 51% state ownership threshold.

-

Infrastructure investment in transport corridors, energy supply to remote processing sites, and water management systems suited to high-altitude operations.

-

Governance strengthening at YLB, addressing historical institutional credibility concerns that have affected investor confidence in the state entity's operational management.

The critical question confronting Bolivia's mineral program is not geological. The reserves are real, large, and confirmed. The question is whether the institutional, regulatory, and market conditions can align sufficiently to translate multi-billion dollar capital commitments into sustained, commercially viable production at scale. That alignment has not historically been Bolivia's strength, which is precisely why 2026 carries both genuine promise and substantial uncertainty.

Bolivia's pursuit of simultaneous lithium and potassium development, backed by significant Chinese and Russian capital commitments, represents the most consequential mobilisation of resources in the country's mineral sector in decades. Whether that mobilisation produces lasting economic transformation depends less on the scale of investment announced and more on the institutional conditions that will govern its execution over the years that follow.

This article contains forward-looking statements and projections based on publicly available information and industry analysis. Production targets, investment figures, and recovery rate estimates are subject to material change based on operational outcomes, commodity price movements, regulatory developments, and geopolitical factors. Readers should not rely on this content as financial or investment advice. Independent professional advice should be sought before making investment decisions.

Want to Track ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across more than 30 commodities — including lithium and potash — turning complex geological and market data into actionable investment insights for both short-term traders and long-term investors. Explore how major mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial to position yourself ahead of the market.